Feminine Hygiene Products Market Size 2024-2028

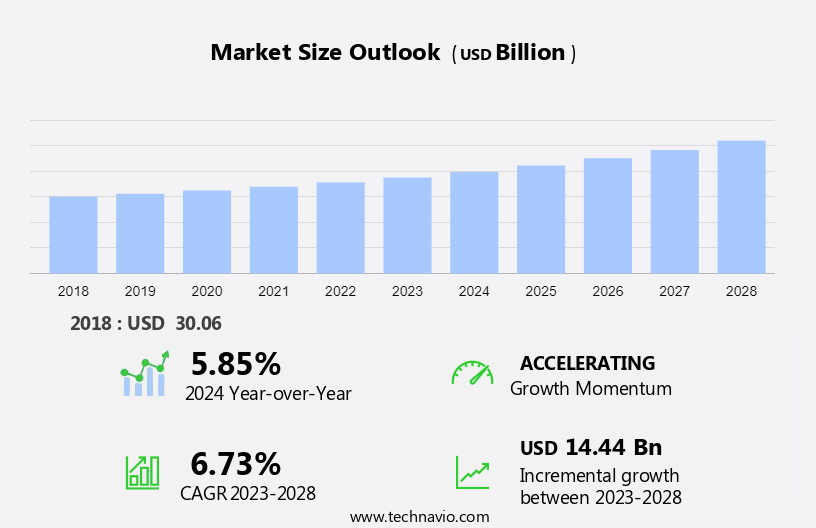

The feminine hygiene products market size is forecast to increase by USD 14.44 billion at a CAGR of 6.73% between 2023 and 2028. The market is fueled by the increasing consumer demand for products offering convenience and benefits. Align with market growth analysis, Western European markets like the UK, France, and Germany play a pivotal role, in the rising consumption of menstrual cups and tampons. Awareness programs and the introduction of new products with organic ingredients drive trends. Despite the tradition and culture influencing purchase decisions, global influences are evident, with education on feminine hygiene starting early in schools.

However, challenges remain, particularly in Eastern Europe, where product availability impacts the market. High disposable incomes drive demand for premium products, leading to increased online sales and forecasts for continued growth.

Market Analysis

The market is evolving with a strong focus on comfort, environmental responsibility, and sustainable innovations. Concerns over leaks and discomfort during menstrual flow have prompted the industry to develop products that enhance both physical and emotional well-being of the female population. The market landscape depends on the packaging category, bottles or jars segment, eco friendly and sustainable options , eco friendly materials, Low cost products, Internal cleansers and sprays, Biodegradable and organic, Synthetic and carcinogenic materials, Non biodegradability, Menstrual hygiene, Vaginal discharge, Vulva and vagina, Menstruation stigma, Eco friendly menstrual cups. Education levels and cultural shifts are driving demand for intimate hygiene solutions that are eco-friendly and biodegradable, addressing ecological impacts and reducing pollution from disposable menstrual products like cotton pads and tampons.

Furthermore, the feminine hygiene industry is undergoing significant transformation, driven by cultural and societal shifts toward gender equality and personal hygiene. As daily activities emphasize both physical well-being and emotional well-being, consumers seek creative product solutions that prioritize absorption and comfort. Innovative materials science plays a crucial role in developing eco-friendly and sustainable options, including reusable period underwear and pads that challenge cultural and social stigmas. This shift is particularly impactful in rural and isolated areas, where access to traditional products may be limited. By embracing reusable and alternative green products, the market not only supports personal health but also promotes environmental sustainability, appealing to a growing demographic that values both quality and responsibility.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Distribution Channel

- Offline

- Online

- Product

- Sanitary napkins

- Tampons

- Pantyliners

- Menstrual cups

- Feminine hygiene wash

- Geography

- Europe

- Germany

- UK

- North America

- US

- APAC

- China

- Japan

- South America

- Middle East and Africa

- Europe

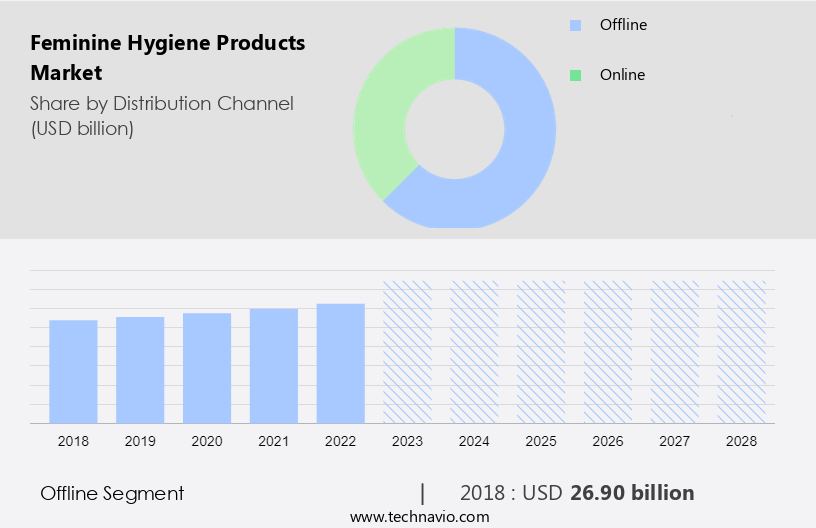

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period. The market encompasses a range of products specifically catering to women's needs during their menstrual cycles. companies employ various strategies, such as branding through signages and discounts, to attract consumers. Women's empowerment is a significant factor driving the demand for these products, as they enable women to manage their menstrual cycles with dignity and convenience. However, allergic reactions and rashes caused by certain materials and additives in these products can pose health concerns.

Furthermore, biodegradable materials, such as organic cotton and compostable bioplastic, are gaining popularity due to their eco-friendly properties. Fragrance additives, on the other hand, are a subject of debate, with some arguing they contribute to waste and others finding them essential for hygiene and comfort. Wipes, tampons, panty liners, pads, menstrual cups, and disposable deodorizing wipes are some of the common products in this market. Surveys and studies suggest that literacy rates and education of girls are crucial factors influencing the use and availability of menstrual hygiene products. Ignorance, societal stigma, cultural taboos, and conventions surrounding menstruation continue to impact women's health and access to these products.

Furthermore, waste reduction initiatives, such as reusable menstrual products, are gaining traction as a sustainable alternative to disposable options. Plastic Oceans International highlights the environmental impact of disposable menstrual products, emphasizing the need for more sustainable solutions. Reusable menstrual cups, for instance, offer a long-term, cost-effective, and eco-friendly alternative to disposable sanitary napkins.

Get a glance at the market share of various segments Request Free Sample

The offline segment was valued at USD 26.90 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

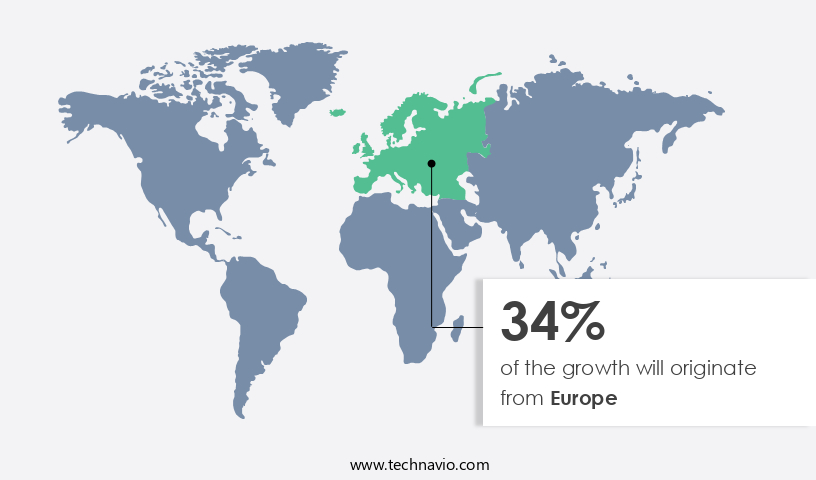

Europe is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Women's menstrual health and hygiene have gained significant importance in Europe, driven by the increasing number of women in the workforce in countries like the UK, France, and Germany. This financial empowerment enables them to invest in feminine hygiene products, such as menstrual cups and tampons, to cater to their hygiene needs. The Western European region, including Germany, France, Italy, Spain, and the UK, has been instrumental in fueling the growth of the market. The expansion of this market can be linked to heightened awareness programs regarding menstrual health and the introduction of new organic feminine hygiene products. These products, available in various colors, shapes, sizes, and price points, cater to diverse preferences and needs.

Moreover, the rise of biodegradable materials, such as organic cotton and compostable bioplastic, in menstrual products addresses concerns related to allergic reactions and rashes caused by synthetic materials and fragrance additives. Surveys and studies indicate that women's literacy rates and education levels have a positive impact on their access to and usage of feminine hygiene products. As societal stigma, cultural taboos, and conventions surrounding menstruation gradually dissipate, there is a growing emphasis on women's health and well-being. Waste reduction initiatives, such as the adoption of reusable menstrual products like menstrual cups, have gained traction, contributing to the market's growth.

Furthermore, disposable deodorizing wipes and sanitary napkins continue to dominate the market, but there is a growing trend toward reusable menstrual cups and biodegradable alternatives. Plastic Oceans International's efforts to reduce plastic waste and promote eco-friendly alternatives have further fueled the demand for compostable and biodegradable menstrual products. Certified vegan and synthetic dye-free options cater to consumers seeking ethical and environmentally conscious choices.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The increasing in aggressive marketing by companies is the key driver of the market. Women's menstrual health and hygiene have gained significant attention in recent years, driven by the marketing efforts of market participants. This trend is particularly noticeable among women, who are increasingly seeking out feminine hygiene products to ensure their personal well-being. The visibility of these products has been enhanced through dedicated sections in major grocery stores and pharmacies, where they are often displayed alongside sanitary napkins and tampons. During the forecast period, the feminine hygiene market is expected to expand due to the introduction of new and innovative products, as well as targeted advertisements aimed at attracting female consumers, particularly the younger generation.

Moreover, in nations with high literacy rates and education for girls, such as China and India, the Internet has become a crucial marketing channel for these products. However, it is essential to consider the potential allergic reactions and rashes that some women may experience due to the use of certain materials, fragrance additives, and synthetic dyes in feminine hygiene products. To address these concerns, market participants are turning to biodegradable materials, such as organic cotton and compostable bioplastic, as well as certified vegan options. Surveys and studies have shown that societal stigma, cultural taboos, and conventions surrounding menstruation continue to impact women's health and access to menstrual products.

Furthermore, reusable menstrual products, such as menstrual cups and reusable wipes, have gained popularity as alternatives to disposable options, contributing to waste reduction initiatives. Moreover, organizations like Plastic Oceans International have highlighted the environmental impact of disposable menstrual products, further driving the demand for more sustainable options. As women continue to prioritize their health and well-being, the feminine hygiene market is poised for growth, offering a range of products that cater to diverse needs and preferences.

Market Trends

The growing popularity of organic products is the upcoming trend in the market. Women's menstrual health and hygiene have gained significant attention in recent years, with an increasing number of females in developed nations, such as the UK and the US, expressing a preference for organic feminine hygiene products. This shift is driven by the perceived health benefits and higher quality standards associated with these products. Allergic reactions and rashes caused by fragrance additives and synthetic materials in conventional wipes, tampons, panty liners, and pads have become a concern for many women. Organic feminine hygiene products are typically made from biodegradable materials, such as certified organic cotton, which is free from genetically modified organisms, fragrances, dyes, rayon, and other synthetic materials.

Furthermore, these products cater to the growing demand for eco-friendly and health-conscious alternatives. Surveys and studies suggest that women's empowerment and education play a crucial role in this trend. As literacy rates and education levels rise, women are becoming more aware of their menstrual cycles and the importance of maintaining good menstrual health. Ignorance and societal stigma surrounding menstruation have long perpetuated the use of disposable sanitary napkins and deodorizing wipes, which contribute to waste and environmental degradation. Reusable menstrual products, such as menstrual cups and reusable pads, are gaining popularity as sustainable alternatives to disposable options. These products are not only better for the environment but also offer health benefits, as they do not contain synthetic dyes or fragrance additives.

Moreover, the growing awareness of the environmental impact of plastic waste, as highlighted by organizations like Plastic Oceans International, has led to a push for waste reduction initiatives in various sectors, including feminine hygiene. The use of compostable bioplastic and certified vegan materials in feminine hygiene products further underscores this trend. In conclusion, the feminine hygiene market is witnessing a shift towards organic and eco-friendly products, driven by women's empowerment, health concerns, and environmental awareness. This trend is expected to continue as more women become educated about their menstrual cycles and the importance of maintaining good menstrual health while reducing their environmental footprint.

Market Challenge

The increasing prevalence of side-effects is a key challenge affecting the market growth. Women's menstrual health and hygiene are of paramount importance, yet concerns persist regarding the potential side effects of certain feminine hygiene products. These concerns include allergic reactions, rashes, and infections caused by components such as synthetic dyes, fragrance additives, and bleaching agents found in sanitary napkins, tampons, and panty liners. The use of biodegradable materials, compostable bioplastic, and organic cotton in menstrual products is a step towards empowering women by promoting their health and reducing societal stigma surrounding menstruation. Surveys and studies indicate that a significant number of women are unaware of the potential risks associated with using non-organic menstrual products.

Furthermore, ignorance and cultural taboos surrounding menstruation hinder women's education and literacy rates, perpetuating a cycle of societal conventions that prioritize disposable deodorizing wipes and sanitary napkins over reusable menstrual cups and other eco-friendly alternatives. Organizations like Plastic Oceans International highlight the environmental impact of disposable menstrual products, which contribute significantly to plastic waste. The shift towards reusable menstrual products not only benefits women's health but also contributes to waste reduction initiatives. Certified vegan menstrual products, free from animal-derived ingredients, are gaining popularity as a more ethical and sustainable alternative. As societal norms evolve, it is crucial to prioritize women's health and well-being by promoting the use of safe and eco-friendly menstrual products.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

BeYou: The company offers feminine hygiene products such as forehead patches, menstrual cup and chafing cream.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Corman SpA

- Edgewell Personal Care Co.

- Essity AB

- First Quality Enterprises Inc.

- Hengan International Group Co. Ltd.

- Johnson and Johnson

- Kao Corp.

- Kimberly Clark Corp.

- Lagom Labs Private Limited

- Maxim Hygiene Products Inc.

- Ontex BV

- Premier

- The Good Glamm Group

- The Honest Co. Inc.

- The Procter and Gamble Co.

- The SCA Group LLC

- TZMO SA

- Unicharm Corp.

- Unitex Composite Mills Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of items designed for women's menstrual and post-menopausal needs. These products include sanitary napkins, tampons, menstrual cups, and various other forms of panty liners. The market witnesses continuous growth due to increasing awareness and acceptance of these products. Women's empowerment and changing societal norms have led to a shift towards more convenient and discreet options.

Additionally, the rise in disposable income and urbanization have contributed to the market's expansion. Manufacturers focus on innovation and sustainability to cater to evolving consumer preferences. The market is segmented by product type, distribution channel, and geography. Sanitary napkins and tampons dominate the market share, while menstrual cups and other alternatives gain traction. The market is expected to grow significantly in the coming years, driven by increasing population, rising disposable income, and changing consumer preferences.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

178 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.73% |

|

Market growth 2024-2028 |

USD 14.44 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.85 |

|

Regional analysis |

Europe, North America, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

Europe at 34% |

|

Key countries |

US, China, Japan, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

BeYou, Corman SpA, Edgewell Personal Care Co., Essity AB, First Quality Enterprises Inc., Hengan International Group Co. Ltd., Johnson and Johnson, Kao Corp., Kimberly Clark Corp., Lagom Labs Private Limited, Maxim Hygiene Products Inc., Ontex BV, Premier, The Good Glamm Group, The Honest Co. Inc., The Procter and Gamble Co., The SCA Group LLC, TZMO SA, Unicharm Corp., and Unitex Composite Mills Ltd |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -