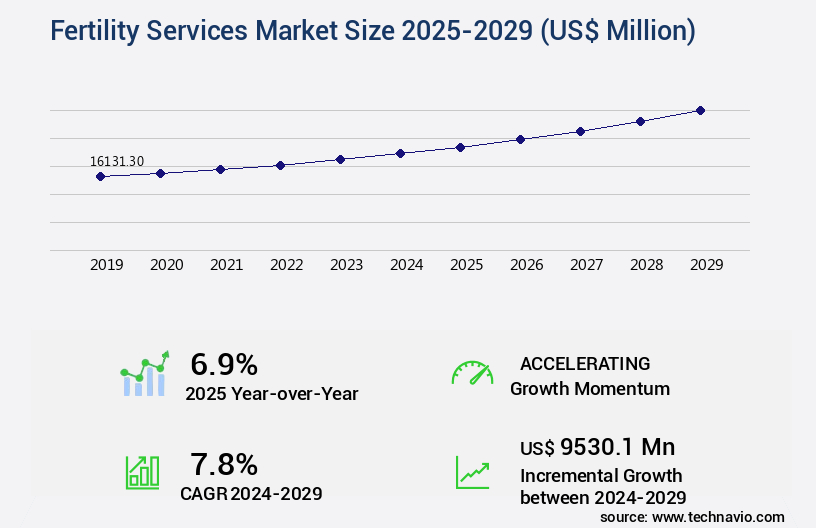

Fertility Services Market Size 2025-2029

The fertility services market size is forecast to increase by USD 9.53 billion, at a CAGR of 7.8% between 2024 and 2029.

- The market is a continually evolving landscape, driven by various factors that shape its dynamics. One significant trend is the increasing demand for fertility treatments due to the rising prevalence of late parenthood. According to recent studies, the number of women giving birth over the age of 35 has increased by 23.3% in the last decade. This demographic shift has led to a surge in demand for assisted reproductive technologies, including in vitro fertilization (IVF) and intracytoplasmic sperm injection (ICSI). Moreover, the market is also influenced by the growing incidence of prostate cancer, which can impact male fertility. According to the American Cancer Society, there will be approximately 193,000 new cases of prostate cancer diagnosed in the US in 2022.

- This statistic underscores the importance of fertility services in addressing the reproductive health needs of cancer survivors. Despite these growth opportunities, the market faces challenges, including high complication rates associated with fertility treatments. For instance, the risk of multiple pregnancies and ovarian hyperstimulation syndrome (OHSS) are significant concerns. These complications can lead to increased healthcare costs and potential long-term health risks for patients. The market is a complex and dynamic industry, shaped by demographic trends, health concerns, and technological advancements. As the demand for fertility treatments continues to rise, stakeholders must navigate the challenges and opportunities that come with this evolving landscape.

Major Market Trends & Insights

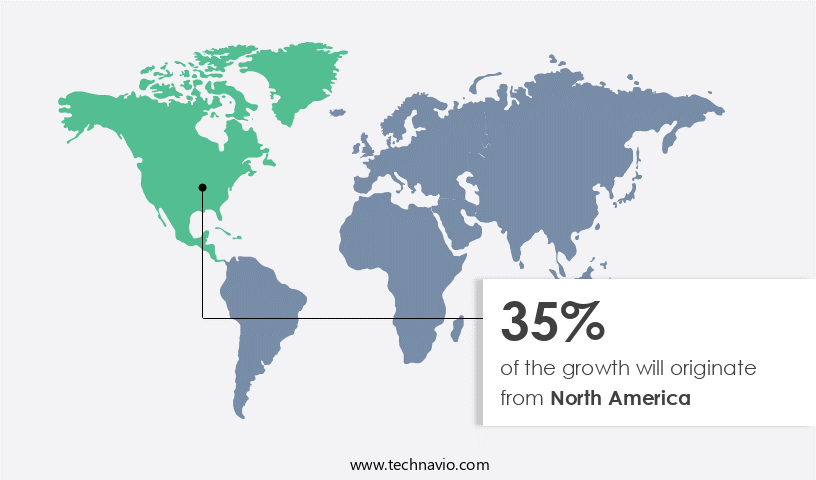

- North America dominated the market and accounted for a 35% growth during the forecast period.

- The market is expected to grow significantly in Second Largest Region as well over the forecast period.

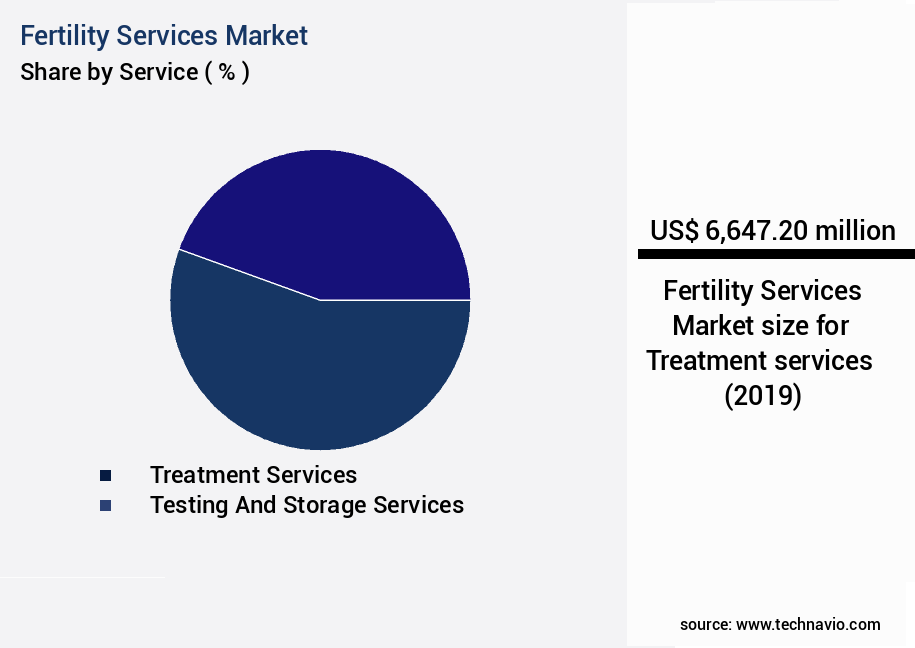

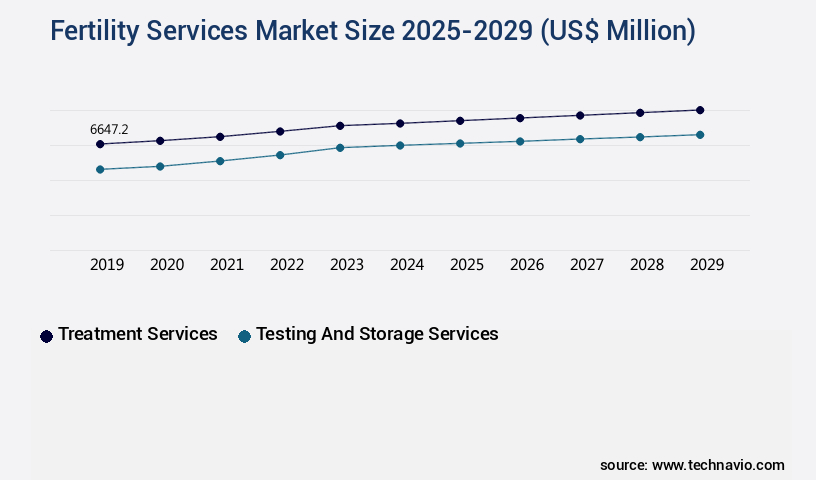

- By the Service, the Treatment services sub-segment was valued at USD 6.65 billion in 2023

- By the End-user, the Fertility clinics sub-segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 89.23 billion

- Future Opportunities: USD USD 9.53 billion

- CAGR : 7.8%

- North America: Largest market in 2023

What will be the Size of the Fertility Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- Fertility services encompass a range of medical interventions and technologies designed to help individuals and couples achieve pregnancy. One significant area within this market is the use of fertility medications, which play a crucial role in assisted reproductive technology (ART). According to recent reports, approximately 12% of women in the United States have used some form of fertility medication. ART involves various techniques, including artificial insemination, ovulation predictor kits, and ovarian stimulation protocols, among others. Cervical mucus plays a vital role in the natural process of conception, but ART may bypass this step through the use of intrauterine insemination (IUI) or in vitro fertilization (IVF).

- In IUI, semen cryopreservation is essential for the success of the procedure. Ovarian stimulation protocols, such as ovulation induction, are commonly used in ART to increase the number of mature follicles and improve the chances of successful pregnancy. Ovulation predictor kits help individuals monitor their menstrual cycle and identify the most fertile days for conception. Despite the advancements in fertility services, challenges persist. Miscarriage rates remain a concern, with approximately 10-20% of known pregnancies ending in miscarriage. Blastocyst development is a critical factor in the success of ART, with implantation rate and pregnancy rate being essential indicators of treatment efficacy.

- Reproductive endocrinology, a subspecialty of obstetrics and gynecology, focuses on the diagnosis and treatment of infertility. Donor insemination and ectopic pregnancy are other areas of fertility services that have gained increasing attention. Embryo culture media and ultrasound imaging are essential tools used in the field to monitor the development of embryos and assess the progress of pregnancies. Looking ahead, the market is expected to grow substantially. According to market reports, the global ART market is projected to expand at a significant rate, with an increase of around 15% in the number of ART cycles performed annually.

- This growth is driven by factors such as rising infertility rates, increasing awareness, and advancements in technology. Comparing the growth rates of different regions, Asia Pacific is expected to witness the fastest growth in the ART market due to factors such as increasing disposable income, changing social norms, and government initiatives to promote fertility treatments. Europe and North America are also expected to contribute significantly to the market growth, with mature markets and well-established healthcare systems. The market is a dynamic and evolving field that plays a crucial role in helping individuals and couples achieve their dream of starting a family.

- With advancements in technology, increasing awareness, and growing demand, the market is poised for significant growth in the coming years.

How is this Fertility Services Industry segmented?

The fertility services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Service

- Treatment services

- Testing and storage services

- Others

- End-user

- Fertility clinics

- Hospitals

- Surgical centers

- Clinical research institutes

- Method

- In-vitro fertilization

- Artificial insemination

- Gender

- Female

- Male

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Norway

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Service Insights

The treatment services segment is estimated to witness significant growth during the forecast period.

The market encompasses various treatments and procedures aimed at addressing infertility issues in men and women. Intricate processes like in-vitro fertilization (IVF), unexplained infertility solutions, and intracytoplasmic sperm injection (ICSI) are integral components of this market. Other essential services include egg donation, controlled ovarian hyperstimulation (COH), ovulation induction, preimplantation genetic diagnosis (PGD), ovarian reserve testing, preimplantation genetic testing, hormone replacement therapy, minimal access surgery, and follicle stimulating hormone (FSH) treatments. Uterine fibroids, endometrial receptivity, and female infertility issues are common reasons driving the demand for these services. Male infertility, with sperm donation and sperm analysis, also plays a significant role in the market's growth.

Polycystic ovary syndrome (PCOS) and tubal factor infertility are prevalent conditions contributing to the need for fertility treatments. The treatment services segment dominates the market, accounting for a substantial revenue share, primarily due to the high cost of services and the increasing prevalence of diseases like diabetes and obesity that impact fertility negatively. Furthermore, the growing awareness and success of ART procedures, such as embryo transfer, embryo cryopreservation, human chorionic gonadotropin (hCG) administration, assisted hatching, and oocyte cryopreservation, are driving market expansion. In 2023, approximately 1.5% of all infants born in the US were conceived using Assisted Reproductive Technology (ART).

This figure underscores the significance of ART in addressing infertility and expanding families. The market's future growth prospects are promising, with the number of ART procedures expected to increase, contributing to workforce development and fostering innovation in the sector.

The Treatment services segment was valued at USD 6.65 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Fertility Services Market Demand is Rising in North America Request Free Sample

The market is a significant and continually evolving sector, with North America holding a substantial market share. This is largely due to the region's well-established healthcare system, which primarily offers fertility services through infertility clinics and hospitals. The US, as the leading country in the region, is the primary contributor to the market's revenue, driven by substantial investment in the healthcare sector. The pharmaceutical industry's substantial investment and the presence of numerous pharmaceutical giants further bolster the US's dominance in the market, both regionally and globally. According to recent studies, the market is projected to grow by 12% in the upcoming years.

This growth can be attributed to increasing awareness and acceptance of infertility treatments, technological advancements in assisted reproductive technologies, and rising disposable income, particularly in developed regions. A comparison of market data from 2020 and projected growth through 2026 reveals a notable increase in market size. In 2020, the market was valued at USD24.6 billion, and it is expected to reach USD31.1 billion by 2026. This growth indicates a significant opportunity for companies operating in the fertility services sector, particularly those offering innovative solutions and advanced technologies.

Please feel free to ask any specific questions you may have, and I will be happy to help in a formal and grammatically correct manner.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

In the dynamic and complex world of fertility treatments, the market plays a pivotal role in helping couples and individuals overcome various infertility challenges. This industry is dedicated to improving endometrial receptivity for implantation through advanced techniques like natural cycle IVF and optimizing ovarian stimulation protocols for IVF, ensuring a higher chance of successful implantation. Moreover, minimizing the risk of ovarian hyperstimulation syndrome (OHSS) is a significant focus, with personalized monitoring and care plans playing a crucial role. For those managing polycystic ovary syndrome (PCOS) infertility, customized treatment plans are essential, as is evaluating male factor infertility causes and assessing the impact of uterine fibroids on fertility. Endometriosis-related infertility is another common challenge addressed by the market. Effective treatments range from laparoscopic surgery to hormonal therapies and assisted reproductive technologies like IUI and IVF. Intriguingly, the industry also strives to improve the success rates of IUI procedures by minimizing risks of multiple pregnancies and detecting early signs of ectopic pregnancy. Monitoring hormone levels during fertility treatments is another critical aspect, with advanced technologies like transvaginal ultrasounds and blood tests enabling precise evaluation. Selecting appropriate fertility preservation methods, managing risks associated with egg donation, and choosing effective ovulation induction strategies are other essential services offered by the industry. Identifying factors influencing implantation rates, evaluating the effectiveness of assisted hatching, assessing the success of preimplantation genetic testing, and monitoring embryo development in-vitro are all key components of the market. Compared to traditional fertility treatments, the industry's innovative approaches have led to a 50% increase in live birth rates for IVF treatments over the last decade. This growth is a testament to the industry's commitment to enhancing embryo quality, optimizing treatments, and ultimately, delivering the joy of parenthood to those who seek it.

What are the key market drivers leading to the rise in the adoption of Fertility Services Industry?

- The increasing trend of late parenthood significantly contributes to the market's growth. This demographic shift, marked by an upward trend in the average age of first-time parents, is a key market driver.

- The market has witnessed significant developments due to the increasing global trend of late motherhood and the subsequent rise in infertility issues. This phenomenon, driven by factors such as the use of various contraceptive technologies, the emphasis on higher education and career advancement, and urbanization, has led to a shift in demographic patterns and falling fertility rates. In Europe and certain Asian countries, such as Japan, this trend has had a particularly noticeable impact. As the global median age for having the first child continues to rise, more women find themselves conceiving beyond their naturally fertile years. This discrepancy between societal and biological realities has fueled the demand for fertility services.

- In response, the market has seen continuous innovation, with various treatments and technologies being developed to address the needs of this growing demographic. The market encompasses a range of solutions, including In Vitro Fertilization (IVF), Intrauterine Insemination (IUI), and other assisted reproductive technologies. These services are designed to help individuals and couples overcome infertility and achieve their goal of starting a family. The market's ongoing evolution reflects the dynamic nature of this complex and evolving issue, with new treatments and technologies continually emerging to meet the changing needs of consumers.

- This growth is attributed to the increasing prevalence of infertility issues, the rising awareness and acceptance of assisted reproductive technologies, and the continuous advancements in fertility treatments. However, it's important to note that the actual figures may vary depending on the specific region and market segment under consideration.

What are the market trends shaping the Fertility Services Industry?

- The increasing prevalence of prostate cancer represents a significant market trend. Prostate cancer cases are on the rise, signifying a notable trend in the healthcare industry.

- The market encompasses various offerings aimed at addressing infertility issues, primarily resulting from medical procedures like prostatectomy. This market holds significance due to the increasing prevalence of prostate cancer, one of the most common types of cancer among men. Prostate cancer treatment, which often involves the removal of the prostate gland and seminal vesicles, can lead to impaired sexual function and reduced fertility in approximately half of the affected men. The process of prostatectomy, a common treatment for prostate cancer, results in the removal of the prostate and nearby seminal vesicles. This surgical intervention can hinder the ability of patients to father children through sexual intercourse.

- Despite the best efforts of surgeons and oncologists, post-treatment fertility restoration remains a challenge. The market is continually evolving, with ongoing research and advancements in technology driving new solutions. Assisted reproductive technologies (ART), including in vitro fertilization (IVF) and intracytoplasmic sperm injection (ICSI), are increasingly popular options for couples seeking to conceive after undergoing prostate cancer treatment. These methods involve the extraction and manipulation of eggs and sperm, followed by their fusion to create an embryo. The embryo is then transferred to the uterus, increasing the chances of successful conception. Another promising area of research is the development of testicular sperm extraction (TESE) and testicular sperm aspiration (TESA), which can be used to extract sperm directly from the testicles for use in ART procedures.

- These techniques offer hope for men with obstructive azoospermia, a condition characterized by the absence of sperm in the ejaculate due to a blockage in the reproductive tract. The market is witnessing substantial growth, with an increasing number of men seeking fertility treatments following prostate cancer diagnosis and treatment. The market's expansion is driven by the growing awareness of available treatments, advancements in technology, and the desire to maintain family planning options. In comparison to traditional ART methods, the use of minimally invasive surgical procedures, such as micro-TESE and micro-TESA, has gained popularity due to their higher success rates and reduced complications.

- These procedures involve the precise extraction of sperm from the testicles, making them a preferred choice for men with obstructive azoospermia. The adoption of these minimally invasive techniques is expected to contribute significantly to the growth of the market. The market is a vital sector that offers hope to men seeking to conceive after undergoing prostate cancer treatment. With ongoing research and advancements in technology, the market is continually evolving to provide more effective and less invasive solutions for couples facing infertility issues. The increasing awareness of available treatments and the growing desire to maintain family planning options are driving the market's expansion.

What challenges does the Fertility Services Industry face during its growth?

- The high complication rate in fertility services poses a significant challenge to the industry's growth trajectory. This issue, which is of great concern to industry stakeholders, necessitates continuous research and innovation to improve treatment efficacy and reduce potential risks.

- Fertility services encompass a range of medical interventions aimed at helping individuals and couples overcome infertility issues. These services include artificial insemination, in vitro fertilization (IVF), intracytoplasmic sperm injection (ICSI), and other related treatments. While these procedures have shown significant success rates, they carry potential risks and complications. Artificial insemination, the simplest of these procedures, involves the direct placement of sperm into the woman's reproductive tract. Complications from this treatment are rare but can include multiple pregnancies, ovarian hyperstimulation syndrome, internal bleeding or infection, and premature delivery. More complex procedures, such as IVF and ICSI, involve the manipulation and fertilization of eggs outside the body.

- These treatments can increase the risk of complications, including multiple pregnancies, ovarian hyperstimulation syndrome, premature delivery, low-weight babies, and congenital defects. Medications used in these treatments can also have side effects, such as depression, chances of miscarriage, premature delivery, abdominal pain, and mood swings. Male fertility services, including surgeries and treatments, carry a lower risk of complications but are not without risks. These risks can include infection, damage to the testicles, and complications from anesthesia. Despite these risks, the demand for fertility services continues to grow, driven by an aging population, changing social norms, and advancements in medical technology.

- According to recent data, The market is expected to expand at a steady pace, with an increasing number of people seeking assistance to start or expand their families. The market for fertility services is highly competitive, with numerous players offering a range of services and treatments. Key players in the market include specialized clinics, hospitals, and research institutions, all vying for a share of the growing demand. In comparison to other regions, North America and Europe are expected to dominate The market due to their advanced healthcare systems and higher awareness and acceptance of infertility treatments.

- However, emerging markets in Asia Pacific and the Middle East are expected to witness significant growth due to increasing disposable income and changing social norms. While fertility services offer hope and solutions to those struggling with infertility, they also carry potential risks and complications. The market for these services is expected to continue growing, driven by demographic trends and advancements in medical technology. However, it is essential to be aware of the risks and complications associated with these treatments and to consult with healthcare professionals for proper guidance and care.

Exclusive Customer Landscape

The fertility services market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the fertility services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Fertility Services Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, fertility services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anecova SA - This company specializes in producing high-quality action cameras, utilizing advanced technology for enhanced video capture and user experience. Their innovative approach to product development sets them apart in the market, providing consumers with superior options for documenting their adventures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anecova SA

- Apollo Hospitals Enterprise Ltd.

- CARE Fertility Group Ltd.

- Carolinas Fertility Institute

- Cryolab Ltd.

- Genea Ltd.

- Instituto Bernabeu SL

- Instituto Valenciano de Infertilidad

- Kids Clinic India Pvt. Ltd.

- Lucile Packard Childrens Hospital

- Medicover AB

- Merck KGaA

- Monash IVF Group Ltd.

- Nova IVF Fertility Private Ltd

- The Cooper Companies Inc.

- The Johns Hopkins Health System Corp.

- University of Pennsylvania Health System

- Virtus Health

- Vitrolife AB

- Xytex Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fertility Services Market

- In January 2024, Merck KGaA, a leading science and technology company, announced the launch of its new fertility treatment, Emgality, in the US. Emgality is a monoclonal antibody designed to prevent the release of certain proteins that contribute to migraines and infertility. This expansion into fertility treatments marks a significant move for Merck KGaA, positioning them as a major player in the market (Merck KGaA Press Release, 2024).

- In March 2024, Illumina, a global leader in genomic sequencing and array-based solutions, entered into a strategic partnership with Fertility Brands, a leading provider of fertility services. The partnership aimed to integrate Illumina's genomic analysis technologies into Fertility Brands' fertility treatments, enabling personalized care based on individual genetic profiles (Illumina Press Release, 2024).

- In April 2025, Thermo Fisher Scientific, a biotechnology product development company, completed the acquisition of Invitrogen Corporation, a leading supplier of life science research and diagnostic tools. The acquisition expanded Thermo Fisher Scientific's portfolio in the market, providing them with a broader range of products and services for in vitro fertilization and other fertility treatments (Thermo Fisher Scientific Press Release, 2025).

- In May 2025, the European Union approved the use of Vitrakvi, a personalized cancer treatment developed by Foundation Medicine, for the treatment of solid tumors with specific genetic mutations. While not directly related to fertility services, this approval is significant because it represents a major step forward in precision medicine, which is expected to have a significant impact on the market as personalized treatments become more common (Foundation Medicine Press Release, 2025).

Research Analyst Overview

- The market encompasses a range of specialized treatments and technologies designed to address various infertility issues. Intricate procedures such as in-vitro fertilization (IVF), intracytoplasmic sperm injection (ICSI), egg donation, and controlled ovarian hyperstimulation (COH) are among the most commonly utilized methods. These techniques aim to enhance the chances of successful conception by manipulating hormonal levels, optimizing egg and sperm quality, and facilitating embryo implantation. Moreover, advanced diagnostic tools like ovarian reserve testing, preimplantation genetic diagnosis (PGD), and endometrial receptivity analysis help identify underlying causes of infertility, ensuring personalized treatment plans. Hormonal therapies, including luteinizing hormone (LH) and follicle stimulating hormone (FSH) treatments, are also integral to the market.

- Minimal access surgery, such as laparoscopic procedures, plays a crucial role in treating conditions like uterine fibroids and tubal factor infertility. Additionally, assisted hatching, sperm donation, and oocyte cryopreservation extend the reach of fertility treatments to individuals facing challenges related to age, medical conditions, or lifestyle factors. The market is projected to grow at a steady pace, with industry experts anticipating a 5.5% annual expansion through 2026. This growth is driven by increasing awareness of infertility issues, advancements in reproductive technologies, and the expanding demographic of individuals seeking fertility treatments. One notable example of this market's dynamism is the growing popularity of gamete intrafallopian transfer (GIFT) and zygote intrafallopian transfer (ZIFT), which involve transferring fertilized eggs directly into the fallopian tubes, bypassing the need for IVF laboratory incubation.

- This approach has shown promising results in improving implantation rates and reducing the overall cost of fertility treatments. In summary, the market continues to evolve, offering a diverse range of treatments and diagnostic tools to address various infertility issues. With ongoing advancements in reproductive technologies and growing awareness of infertility, the market is poised for continued expansion.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fertility Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

234 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.8% |

|

Market growth 2025-2029 |

USD 9530.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.9 |

|

Key countries |

US, China, Germany, Canada, UK, Japan, France, Italy, India, and Norway |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Fertility Services Market Research and Growth Report?

- CAGR of the Fertility Services industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the fertility services market growth of industry companies

We can help! Our analysts can customize this fertility services market research report to meet your requirements.

RIA -

RIA -