Field Service Management (FSM) Software Market Size 2026-2030

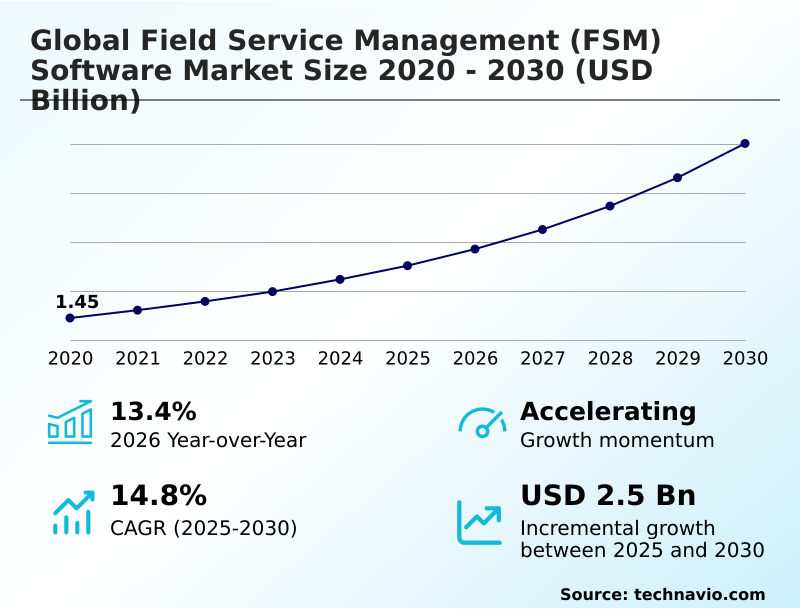

The field service management (fsm) software market size is valued to increase by USD 2.50 billion, at a CAGR of 14.8% from 2025 to 2030. Increasing demand for predictive maintenance will drive the field service management (fsm) software market.

Major Market Trends & Insights

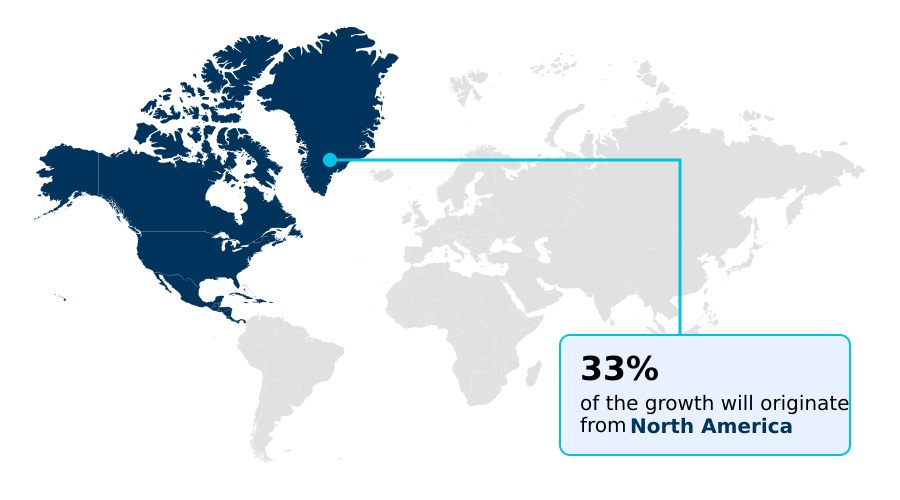

- North America dominated the market and accounted for a 32.9% growth during the forecast period.

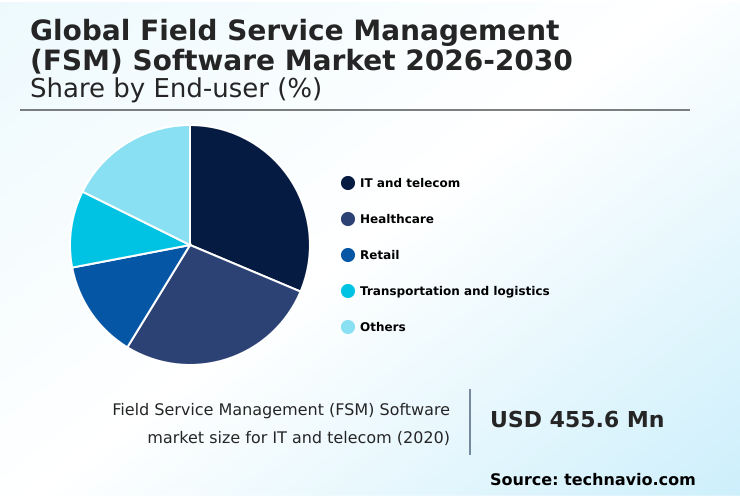

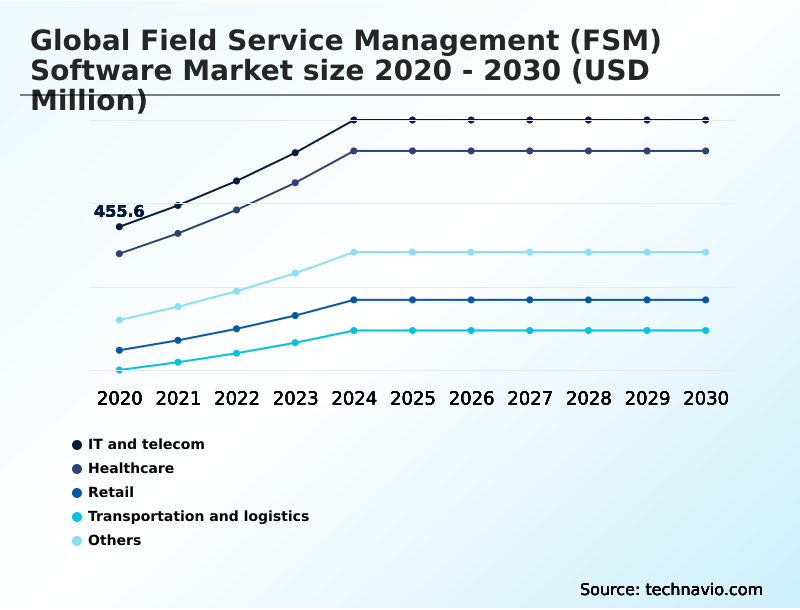

- By End-user - IT and telecom segment was valued at USD 683.1 million in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.57 billion

- Market Future Opportunities: USD 2.50 billion

- CAGR from 2025 to 2030 : 14.8%

Market Summary

- The Field Service Management (FSM) Software Market is defined by a continuous push toward operational excellence, driven by the need to manage a distributed and mobile workforce with greater efficiency. Core functionalities center on work order management, intelligent scheduling engine, and real-time communication platform to ensure seamless coordination.

- A key trend is the integration of predictive maintenance solution, which utilizes AI-driven scheduling and real-time asset monitoring to shift from reactive repairs to proactive interventions. For instance, a logistics company can use telematics data integration to predict vehicle failures, scheduling maintenance to prevent unplanned downtime reduction and improve service level agreement compliance.

- However, challenges such as legacy system integration and the high costs of digital process redesign temper adoption rates. The move toward cloud-native FSM architecture, augmented reality guidance, and no-code automation platform is further shaping the competitive landscape, enabling more agile service organization and enhanced customer experience orchestration.

- These advancements help businesses improve first-time fix rate improvement and optimize total cost of ownership analysis for their service operations.

What will be the Size of the Field Service Management (FSM) Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Field Service Management (FSM) Software Market Segmented?

The field service management (fsm) software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- IT and telecom

- Healthcare

- Retail

- Transportation and logistics

- Others

- Deployment

- On-premises

- Cloud-based

- Component

- Solutions

- Services

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By End-user Insights

The it and telecom segment is estimated to witness significant growth during the forecast period.

The IT and telecom segment is advancing due to the expansion of digital infrastructure. The rollout of 5G networks, requiring extensive installation and maintenance, drives demand for sophisticated work order management and scheduling and dispatch automation.

Centralized platforms that enable end-to-end service management and mobile-first application design are crucial. These systems must coordinate internal and third-party technicians, ensure service execution and asset performance, and manage asset and inventory tracking.

Effective platforms also integrate automated billing and reporting and support a unified communication platform.

This digital coordination helps companies achieve service contract profitability, with some achieving a 20% improvement in first-time fix rates through preventative work order automation and the use of AI-assisted insights.

The IT and telecom segment was valued at USD 683.1 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Field Service Management (FSM) Software Market Demand is Rising in North America Get Free Sample

Geographic dynamics in the market are shaped by regional needs for asset performance management and customer experience orchestration.

In developed regions, there is a strong focus on advanced field service automation, including preventive maintenance scheduling for critical infrastructure and contractor management module for complex projects.

The need to reduce carbon footprint by over 15% is driving the adoption of geographic information system integration for route optimization. In emerging markets, the focus is on scaling operations with third-party contractor management and ensuring digital compliance documentation.

Across all regions, industrial asset lifecycle management and hyper-personalized service delivery are becoming key differentiators.

The use of mixed-reality support for after-sales service support and emergency dispatch system for rapid response is also growing, supported by workforce skill-based assignment to optimize talent allocation.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Achieving operational excellence in the Field Service Management (FSM) Software Market hinges on mastering specific, high-impact use cases. Optimizing field service scheduling software is fundamental, as it directly influences technician productivity and customer satisfaction. The next level of maturity involves integrating IoT with field service management, which enables real-time data streams for implementing predictive maintenance in FSM.

- This proactive approach significantly helps in improving first-time fix rates with software, a key metric for service profitability. Businesses are also evaluating the benefits of AR in field service, where technicians receive guided instructions, and using digital twins for technician training to accelerate skill development.

- Another critical area is managing third-party field service providers efficiently, which requires robust platforms that can handle compliance management in field service software seamlessly. For asset-intensive sectors, such as the field service software for telecom industry and managing FSM for renewable energy assets, accurate inventory tracking for field service technicians is non-negotiable.

- Ultimately, decisions between cloud vs on-premise FSM solutions and the adoption of no-code platforms for field service workflows will define an organization's agility. The effectiveness of AI-powered dispatching for field service, mobile FSM apps for technicians, and route optimization software for service fleets is measured by data analytics in field service operations, which tracks FSM software and customer satisfaction metrics.

- Overcoming the challenges of FSM legacy system integration is a prerequisite for a successful digital transformation with FSM software.

What are the key market drivers leading to the rise in the adoption of Field Service Management (FSM) Software Industry?

- The increasing demand for predictive maintenance capabilities is a key driver propelling the growth of the Field Service Management (FSM) Software Market.

- The market's growth is primarily fueled by the pursuit of operational efficiency optimization and significant service delivery cost reduction.

- A key driver is the shift toward a predictive maintenance solution, which leverages a sophisticated intelligent scheduling engine and real-time asset monitoring to forecast equipment failures.

- This approach facilitates unplanned downtime reduction by up to 40% and ensures service level agreement compliance. The expansion of the mobile workforce management necessitates a real-time communication platform and telematics data integration for effective coordination.

- Furthermore, the focus on first-time fix rate improvement is addressed by AI-driven scheduling and dynamic scheduling capabilities, which optimize technician assignments and routes. This enhances workforce productivity maximization, directly impacting profitability and customer satisfaction in competitive service environments.

What are the market trends shaping the Field Service Management (FSM) Software Industry?

- The integration of augmented reality tools is an emerging market trend. This technology enhances field operations by providing technicians with real-time, interactive digital information.

- Key trends are reshaping the market, with a focus on empowering technicians and automating complex decisions. The adoption of augmented reality guidance and remote expert assistance is becoming standard, enabling a single expert to support multiple field workers and improving first-time fix rates by over 20%.

- This is complemented by immersive training solutions built on a spatial computing interface and digital twin simulation, which reduces onboarding time. Concurrently, edge computing intelligence allows for remote diagnostics capability and the operation of autonomous service units in locations with poor connectivity.

- The rise of no-code automation platform and low-code development tools is fostering a more agile service organization, where non-technical users can customize workflows. This democratization of technology enables proactive customer service and accelerates data-driven decision making across the enterprise.

What challenges does the Field Service Management (FSM) Software Industry face during its growth?

- The rising initial costs associated with software implementation present a significant challenge to the growth of the Field Service Management (FSM) Software Market.

- Significant challenges constrain market adoption, led by difficulties with legacy system integration. Connecting a modern, cloud-native FSM architecture with outdated on-premise systems often requires extensive digital process redesign and costly custom development, complicating enterprise resource planning integration.

- The total cost of ownership analysis frequently reveals hidden expenses, particularly for data migration and employee training, with initial implementation costs sometimes exceeding software license fees by 50%. Ensuring technician safety and wellness necessitates investment in ruggedized mobile hardware with reliable offline data synchronization.

- Furthermore, the lack of effective employee engagement tools can lead to poor adoption and inaccurate mobile data capture, undermining inventory loss prevention efforts and the overall return on investment. A multi-cloud strategy enablement can add another layer of complexity to data management.

Exclusive Technavio Analysis on Customer Landscape

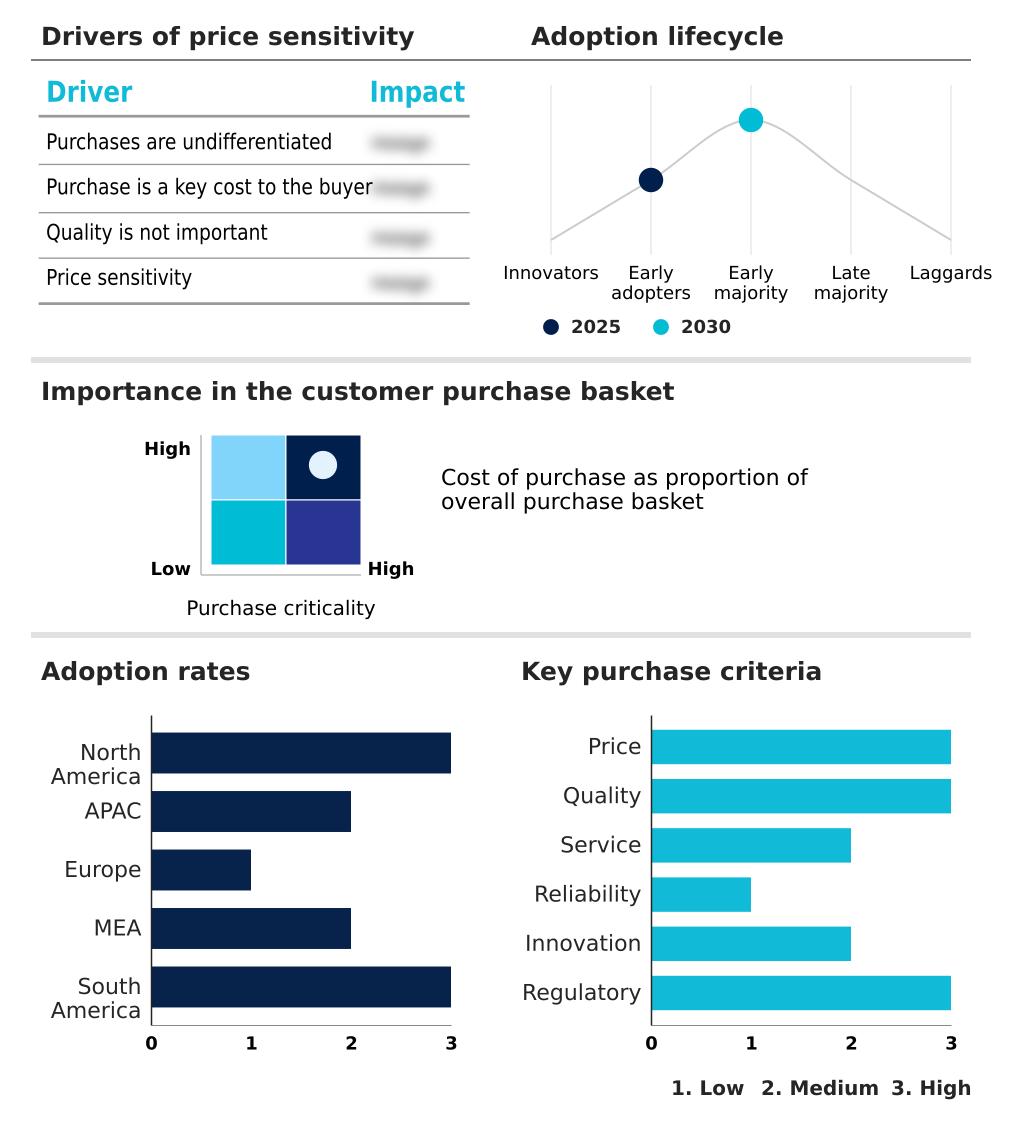

The field service management (fsm) software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the field service management (fsm) software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Field Service Management (FSM) Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, field service management (fsm) software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accruent - Key solutions focus on integrated workforce scheduling, mobile app deployment, and real-time tracking to optimize field operations across diverse industrial and utility sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accruent

- Comarch SA

- FieldAware Group Ltd.

- FieldEZ

- Fortive Corp.

- GeoConcept SAS

- IFS World Operations AB

- Infor Inc.

- Microsoft Corp.

- MSI Data LLC

- Oracle Corp.

- OverIT S.p.A

- PTC Inc.

- Salesforce Inc.

- SAP SE

- ServicePower Inc.

- Simpro Group

- Syncron Holding AB

- Trimble Inc.

- Zinier Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Field service management (fsm) software market

- In August 2024, Oracle Corp. highlighted the complexities utility companies encounter when integrating modern service tools with legacy grid management systems, which can lead to data fragmentation.

- In September 2024, Microsoft Corp. released a report on the industrial skills gap, indicating that a significant majority of companies face challenges in recruiting workers proficient with data-driven management tools.

- In January 2025, PTC Inc. announced its service platform will incorporate advanced digital twin simulations to enhance the training programs for new field service technicians.

- In February 2025, Salesforce Inc. introduced updates to its data cloud, enabling more proactive customer service through capabilities driven by real-time asset monitoring and analytics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Field Service Management (FSM) Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14.8% |

| Market growth 2026-2030 | USD 2497.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.4% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Field Service Management (FSM) Software Market continues to evolve, driven by the imperative to transform service operations into strategic, revenue-generating functions. Boardroom decisions now focus on deploying solutions that offer not just efficiency but also competitive differentiation through hyper-personalized service delivery and end-to-end service lifecycle management.

- The adoption of AI-assisted insights and dynamic scheduling capabilities is central to this shift, enabling companies to automate complex processes and improve responsiveness. Key technologies such as AI-driven scheduling, mixed-reality support for technicians, and a unified communication platform are becoming standard.

- For instance, organizations leveraging a robust scheduling and dispatch automation system have reported reductions in travel time by up to 25%. The integration of mobile-first application design, offline data synchronization, and ruggedized mobile hardware ensures that technicians remain productive in any environment.

- This technological convergence enables superior asset and inventory tracking, automated billing and reporting, and ultimately, enhanced service contract profitability through better data-driven decision-making.

What are the Key Data Covered in this Field Service Management (FSM) Software Market Research and Growth Report?

-

What is the expected growth of the Field Service Management (FSM) Software Market between 2026 and 2030?

-

USD 2.50 billion, at a CAGR of 14.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (IT and telecom, Healthcare, Retail, Transportation and logistics, and Others), Deployment (On-premises, and Cloud-based), Component (Solutions, and Services) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for predictive maintenance, Rising initial software implementation costs

-

-

Who are the major players in the Field Service Management (FSM) Software Market?

-

Accruent, Comarch SA, FieldAware Group Ltd., FieldEZ, Fortive Corp., GeoConcept SAS, IFS World Operations AB, Infor Inc., Microsoft Corp., MSI Data LLC, Oracle Corp., OverIT S.p.A, PTC Inc., Salesforce Inc., SAP SE, ServicePower Inc., Simpro Group, Syncron Holding AB, Trimble Inc. and Zinier Inc.

-

Market Research Insights

- The market is driven by a focus on operational efficiency optimization and service delivery cost reduction, with organizations achieving up to a 30% decrease in maintenance expenses through a predictive maintenance solution. Workforce productivity maximization is another key objective, addressed by tools that support mobile data capture and improve first-time fix rate improvement.

- Platforms now offer advanced data-driven decision making and remote diagnostics capability to enhance after-sales service support. However, a significant skills gap persists, as nearly 60% of companies struggle to find workers with the necessary digital literacy.

- This challenge is met with immersive training solutions and employee engagement tools designed to improve adoption and ensure technician safety and wellness, ultimately leading to better service contract profitability and proactive customer service.

We can help! Our analysts can customize this field service management (fsm) software market research report to meet your requirements.

RIA -

RIA -