US Food Service Market Size 2026-2030

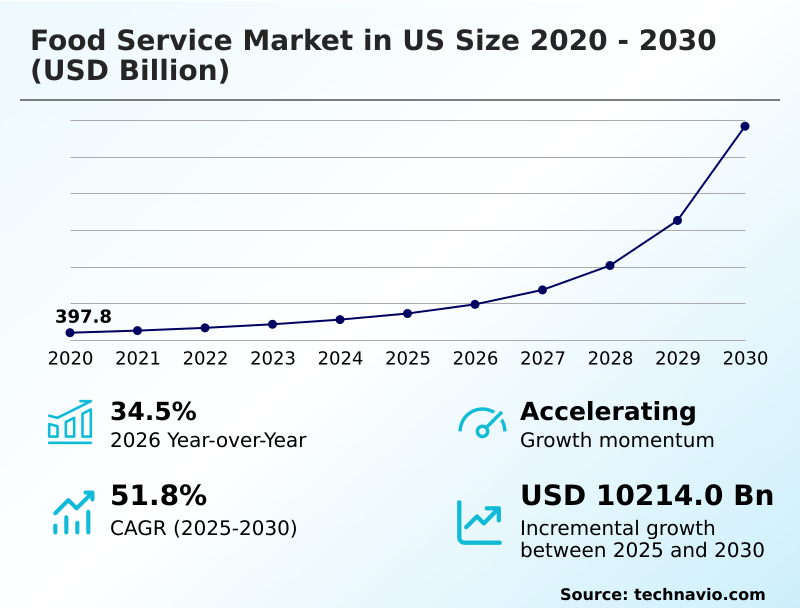

The us food service market size is valued to increase by USD 10214 billion, at a CAGR of 51.8% from 2025 to 2030. Increased snacking and indulgence consumption will drive the us food service market.

Major Market Trends & Insights

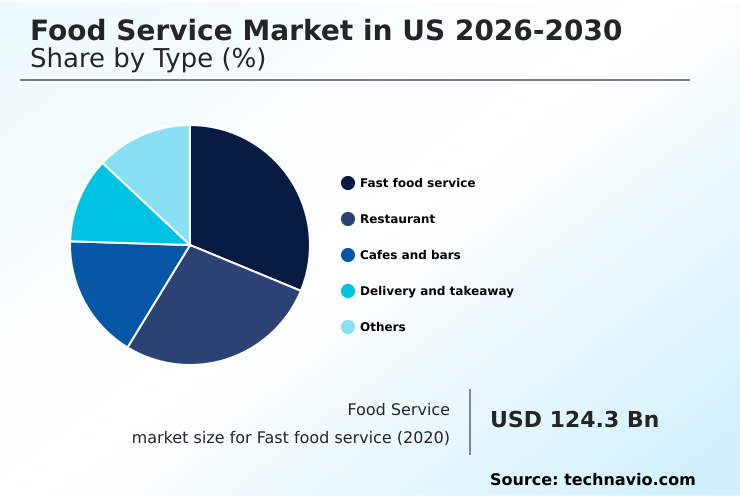

- By Type - Fast food service segment was valued at USD 345.3 billion in 2024

- By Solution - Conventional segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 11262.1 billion

- Market Future Opportunities: USD 10214 billion

- CAGR from 2025 to 2030 : 51.8%

Market Summary

- The food service market in US is undergoing a significant transformation, driven by the convergence of digital technology and evolving consumer behaviors. Key drivers include the demand for convenience, which is met by the proliferation of food delivery apps and digital ordering platforms, and a growing emphasis on health, leading to more allergen-free dining and plant-based menu options.

- A primary trend is the rise of virtual brands and ghost kitchens, which lower market entry barriers and allow for rapid menu experimentation without the overhead of a traditional restaurant. For example, a business can leverage centralized commissary units to prepare meals for multiple delivery-only concepts, optimizing supply chains and reducing waste.

- However, the industry faces challenges from persistent labor shortages and rising operational costs, pushing operators toward automation solutions like voice ordering systems and kitchen display systems. Increased at-home cooking also presents a challenge, compelling food service providers to enhance the experiential dining value proposition to attract customers.

- Success in this environment requires a dual focus on operational efficiency through technology and creating unique, high-quality customer experiences that cannot be replicated at home.

What will be the Size of the US Food Service Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the US Food Service Market Segmented?

The us food service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

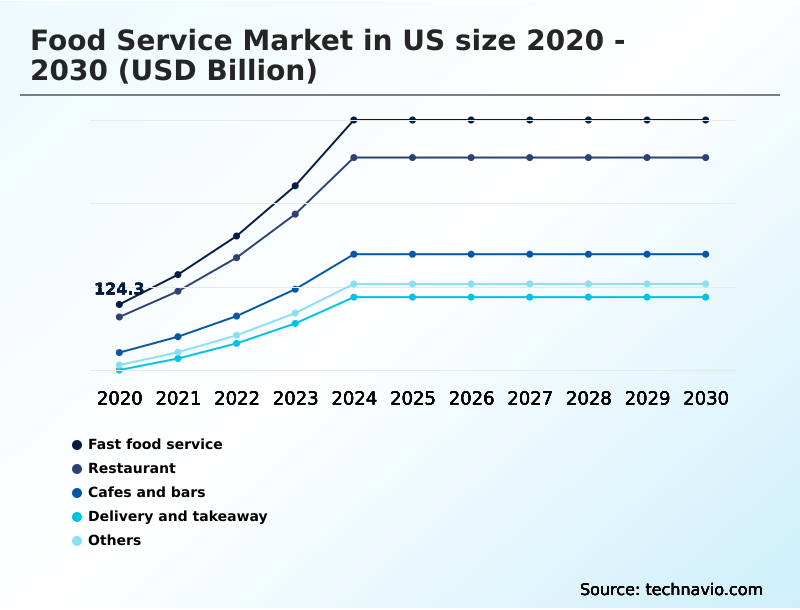

- Type

- Fast food service

- Restaurant

- Cafes and bars

- Delivery and takeaway

- Others

- Solution

- Conventional

- Centralized

- Ready-prepared

- Assembly-serve

- Sector

- Commercial

- Non-commercial

- Business segment

- Chains

- Independent

- Geography

- North America

- US

- North America

By Type Insights

The fast food service segment is estimated to witness significant growth during the forecast period.

The fast food service segment in the US is defined by its focus on convenience, value, and rapid adoption of technology.

This sector is increasingly shaped by the integration of mobile ordering platforms and sophisticated menu engineering to appeal to price-sensitive consumers. Operators are implementing data-driven menu engineering to refine value propositions and manage rising input costs.

The use of AI-driven ovens and other automation is becoming standard for improving consistency and throughput.

While large chains dominate, independent operators are gaining ground by focusing on niche offerings, with some achieving profit margins of 10.5% by optimizing their operational models and leveraging localized supply chains.

This dynamic underscores a broader industry pivot toward digital-first interactions and operational efficiency in the food service market in US.

The Fast food service segment was valued at USD 345.3 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the modern food service market in US 2026-2030 requires a deep understanding of evolving operational models and consumer demands. An analysis of centralized vs conventional kitchen models reveals critical trade-offs between standardization and flexibility.

- Technology adoption in QSR operations is no longer optional, with a focus on drive-thru efficiency improvement techniques and the integration of robotics in food assembly and service to manage rising labor costs. The impact of ghost kitchens on real estate is profound, creating new opportunities for virtual brand portfolio management.

- As operators optimize food delivery logistics, a key focus is maintaining food quality in takeaway packaging. Strategies for allergen-free menu development and a secure supply chain for plant-based offerings are essential for capturing health-conscious segments. Furthermore, using consumer data for personalized marketing through loyalty programs integrated with mobile apps is a key differentiator.

- Data analytics for menu pricing and hyperlocal marketing for independent restaurants help maintain competitiveness. The cost-benefit of subscription models is also a key consideration, alongside sustainability in food service packaging and ensuring compliance with food safety regulations.

- Businesses leveraging technology for reducing food waste report efficiency gains that are often double those of businesses using manual methods, showcasing the tangible benefits of strategic technology adoption for enhancing customer experience in casual dining.

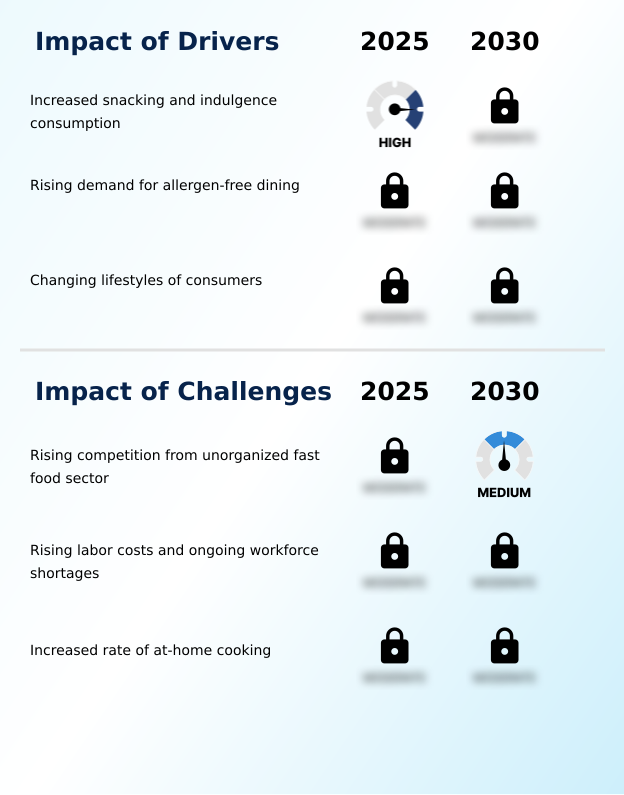

What are the key market drivers leading to the rise in the adoption of US Food Service Industry?

- An increase in snacking and indulgent food consumption, driven by modern on-the-go lifestyles, is a primary driver for the food service market.

- Market growth is significantly fueled by changing consumer lifestyles that prioritize convenience and personalized health.

- The adoption of digital ordering platforms and contactless payments has become standard, with nearly 91% of consumers owning smartphones, which serve as the primary gateway to these services. This digital shift supports the demand for fast-casual formats and quick-service restaurants.

- Concurrently, the increasing focus on wellness is driving the expansion of allergen-free dining and plant-based menu options.

- Food service operators that transparently label menus and implement strict cross-contamination protocols have seen customer loyalty from households with allergies increase by up to 20%. These drivers compel businesses to innovate their service models and menu offerings continually.

What are the market trends shaping the US Food Service Industry?

- The growing diversity of the US population is fueling a significant trend in the food service market, as consumers increasingly seek authentic ethnic cuisines and global flavors.

- Key trends reshaping the food service market include the rise of virtual kitchens and the expansion of experiential dining concepts. The proliferation of ghost kitchens and virtual brands, powered by food delivery apps, allows operators to reach new customers with lower overhead, with some platforms reducing market entry costs by over 50% compared to traditional brick-and-mortar locations.

- These delivery-only concepts thrive on efficiency. Simultaneously, full-service establishments are focusing on social media engagement to promote unique dining experiences that cannot be replicated at home. The clean label movement continues to gain traction, pushing for more transparency in menus.

- This blend of high-tech convenience and high-touch experience defines the current competitive landscape, where data-driven menu engineering informs both value and premium offerings.

What challenges does the US Food Service Industry face during its growth?

- Heightened competition from the unorganized fast food sector, including food trucks and ghost kitchens, presents a key challenge to the growth of established food service chains.

- The primary challenges in the food service market center on operational costs and intense competition. Persistent labor shortages are forcing chained operations and independent outlets alike to invest in technology for labor scheduling and service automation, as high staff turnover can inflate training-related expenses by over 25%. Advanced kitchen display systems and other technologies are being deployed to improve efficiency.

- Simultaneously, rising competition from the unorganized sector, which leverages hyperlocal marketing and lean operational models, puts pressure on pricing and margins. The need for constant food safety management and supply chain optimization adds another layer of complexity, demanding significant capital and strategic planning to maintain profitability in a fragmented market.

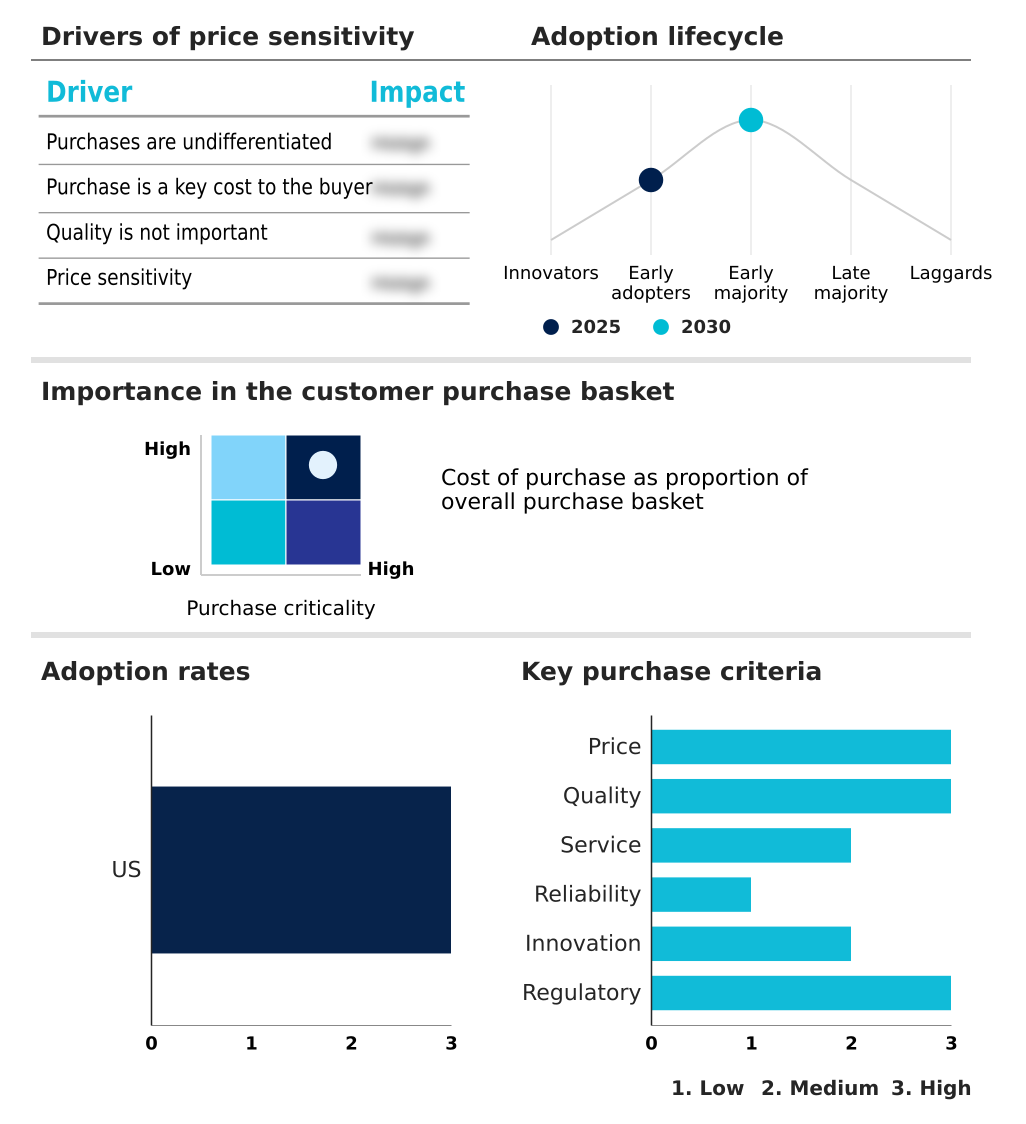

Exclusive Technavio Analysis on Customer Landscape

The us food service market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the us food service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Food Service Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, us food service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Dairy Queen Corp. - Offerings include a diverse range of quick-service, fast-casual, and delivery-focused dining options, emphasizing convenience, menu variety, and customizable meal experiences for consumers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Dairy Queen Corp.

- Chick fil A Inc.

- Chipotle Mexican Grill Inc.

- Dominos Pizza Inc.

- Five Guys Enterprises LLC

- Inspire Brands Inc.

- Jack in the Box Inc.

- Jersey Mikes Franchise Systems

- Jimmy Johns Franchisor SPV LLC

- McDonald Corp.

- MTY Food Group Inc.

- Papa Johns International Inc.

- Penn Station Inc.

- Pret A Manger

- Restaurant Brands Inc.

- Starbucks Corp.

- The Subway Group

- The Wendys Co.

- YUM Brands Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Us food service market

- In April, 2025, Presto Phoenix launched its voice AI phone-ordering division at the Restaurant Leadership Conference, providing a solution to address labor shortages and enhance order accuracy for the quick-service restaurant sector.

- In October, 2024, YUM Brands Inc. announced a leadership transition, appointing a new chief executive officer to spearhead its global unit development and accelerate the deployment of proprietary technology platforms across its brand portfolio.

- In November, 2024, Chipotle Mexican Grill Inc. celebrated the opening of its 4,000th location, a milestone in its strategy to expand its footprint and improve transaction speed through the continued rollout of its Chipotlane drive-thru format.

- In February, 2025, Starbucks Corp. presented its comprehensive transformation plan at an investor event, outlining initiatives focused on a reimagined loyalty program and the use of artificial intelligence to optimize store throughput and customer personalization.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Food Service Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 207 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 51.8% |

| Market growth 2026-2030 | USD 10214.0 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 34.5% |

| Key countries | US |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The food service market in US is navigating a period of intense operational recalibration. The rise of ghost kitchens and the broader cloud kitchen sector is compelling operators to rethink physical footprints, with many pivoting to drive-thru-only formats or delivery-centric models.

- Technology is at the core of this shift, with voice ordering systems and kitchen display systems becoming integral for efficiency. The assembly-serve model, supported by automated chilling technology and advanced rethermalization carts, allows for service with minimal on-site labor. Establishments are using sophisticated inventory management software and menu engineering to combat rising costs.

- In response to consumer health trends, allergen-free dining protocols and diverse plant-based menu options are now mainstream. This evolution is evident as independent full-service establishments that master these operational and menu strategies have successfully returned to double-digit profit margins, reaching 10.5%.

- The market is also defined by the expansion of virtual brands facilitated by food delivery apps and contactless payments, a trend that directly impacts boardroom decisions on brand portfolio strategy and investment in AI-driven ovens and robotic arms for future growth.

What are the Key Data Covered in this US Food Service Market Research and Growth Report?

-

What is the expected growth of the US Food Service Market between 2026 and 2030?

-

USD 10214 billion, at a CAGR of 51.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Fast food service, Restaurant, Cafes and bars, Delivery and takeaway, and Others), Solution (Conventional, Centralized, Ready-prepared, and Assembly-serve), Sector (Commercial, and Non-commercial), Business Segment (Chains, and Independent) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Increased snacking and indulgence consumption, Rising competition from unorganized fast food sector

-

-

Who are the major players in the US Food Service Market?

-

American Dairy Queen Corp., Chick fil A Inc., Chipotle Mexican Grill Inc., Dominos Pizza Inc., Five Guys Enterprises LLC, Inspire Brands Inc., Jack in the Box Inc., Jersey Mikes Franchise Systems, Jimmy Johns Franchisor SPV LLC, McDonald Corp., MTY Food Group Inc., Papa Johns International Inc., Penn Station Inc., Pret A Manger, Restaurant Brands Inc., Starbucks Corp., The Subway Group, The Wendys Co. and YUM Brands Inc.

-

Market Research Insights

- The food service market is defined by a dynamic interplay of technology adoption and shifting consumer expectations. The move toward digital-first interactions is nearly universal, supported by data showing that 91% of the population owns a smartphone, which directly enables mobile ordering and subscription-based models.

- Operators are refining their value propositions to capture loyalty, with effective loyalty programs demonstrably boosting customer retention. Establishments that implement clear cross-contamination protocols for allergen-sensitive diners report up to a 20% increase in repeat business from affected consumer groups.

- The customer journey is increasingly managed through data analytics, allowing for personalized promotions and streamlined service, which has become a critical differentiator in a crowded marketplace. This focus on technology-driven personalization and safety is reshaping the competitive landscape.

We can help! Our analysts can customize this us food service market research report to meet your requirements.

RIA -

RIA -