Forestry Software Market Size 2024-2028

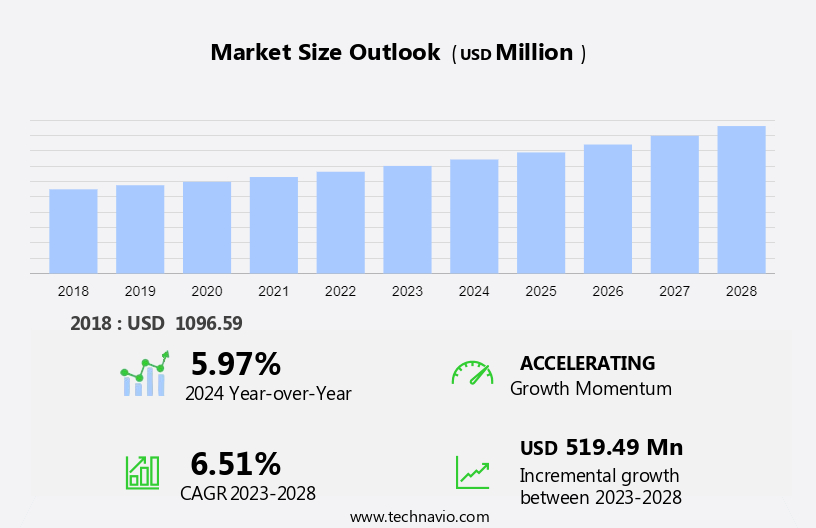

The forestry software market size is forecast to increase by USD 519.49 million at a CAGR of 6.51% between 2023 and 2028. The market is witnessing significant growth due to several key trends. The adoption of cloud-based forestry software is on the rise, as it offers benefits such as real-time data access, cost savings, and scalability. Another trend is the increasing demand for artificial intelligence based forestry software, which utilizes machine learning algorithms to analyze data and provide insights for optimizing forest management.

Additionally, the availability of open-source forestry software is expanding, offering more affordable options for small and medium-sized forestry businesses. These trends are driving the growth of the market and are expected to continue shaping its development in the coming years.

What will be the size of the Forestry Software Market During the Forecast Period?

Forestry software is a vital technology solution for forest management and logging operations. The market for forestry software includes both on-premises and cloud-based options, catering to the varying needs of forestry businesses. On-premises forestry software is installed and operated on a business's own servers, providing complete control over data and operations. In contrast, cloud-based forestry software allows for remote access and real-time data sharing, making it ideal for large-scale forestry operations. Key functionalities of forestry software include inventory management, logistics management, mapwork harvester planning, cut-to-length optimization, geospatial analysis, fire detection, and artificial intelligence. These features enable efficient forest management, improved logistics, and enhanced productivity.

Additionally, the integration of big data and mobile technology further enhances the capabilities of forestry software, allowing for real-time data analysis and remote monitoring. Overall, forestry software is a critical technology investment for forestry businesses seeking to optimize their operations and increase profitability.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Million" for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- End-user

- Large enterprise

- Small

- medium enterprise

- Deployment

- On-premises

- Cloud based

- Geography

- North America

- Canada

- US

- Europe

- APAC

- China

- South America

- Brazil

- Middle East and Africa

- North America

By End-user Insights

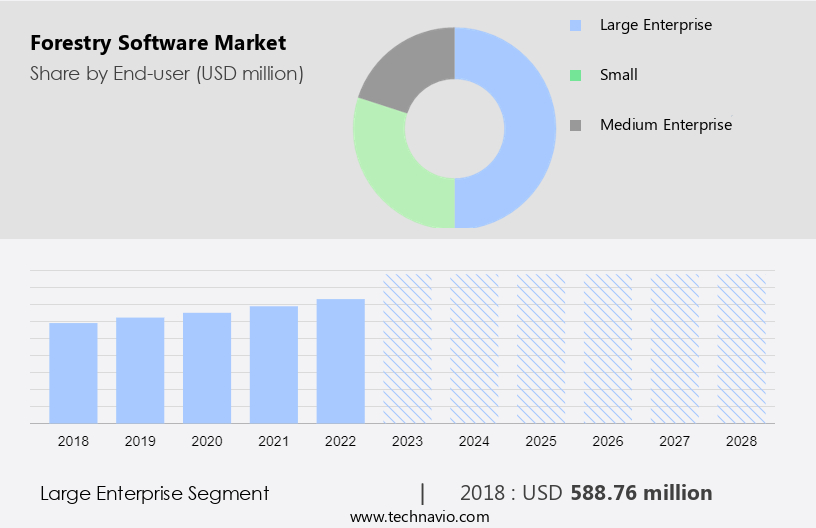

The large enterprise segment is estimated to witness significant growth during the forecast period. Forestry software plays a crucial role in optimizing forest management and resource utilization for large enterprises. These solutions enable effective inventory monitoring and forecasting of crop seasons and productivity. Additionally, they facilitate compliance with regulations and standard practices, reducing paperwork and documentation processes. Cloud-based and On-Premises forestry software offer integrated procedures for managing tasks related to forest management, logging management, mapwork harvester, and logistics management. The application of these technologies, including AI-based forestry, big data, and mobile technology, results in reduced operational time and expenses. The rise in adoption of forestry software is gaining momentum due to digitalization and the increasing recognition of technology's pivotal role in the industry.

Furthermore, advanced features like cut-to-length, geospatial analysis, fire detection, and pricing tools are enhancing profitability and product dominance. The market for forestry software is expected to grow significantly during the forecast period as more enterprises embrace technology to streamline their forest operations.

Get a glance at the market share of various segments Request Free Sample

The large enterprise segment was valued at USD 588.76 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

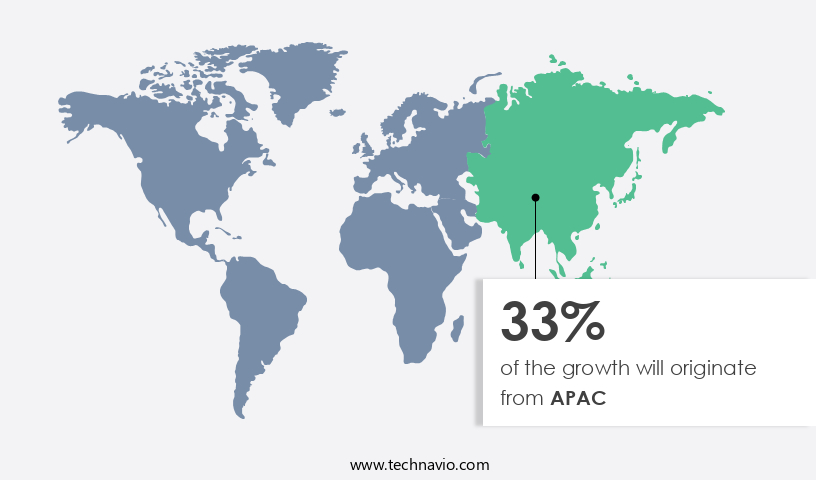

APAC is estimated to contribute 33% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in North America is experiencing significant growth due to the increasing adoption of forestry software and the dominance of technology-driven forestry solutions in the region. Forest management and logging operations in North America are increasingly leveraging forestry software to optimize inventory, logistics, and mapwork harvester operations. Advanced technologies such as cloud-based solutions, artificial intelligence, geospatial mapping, fire detection, and data analytics are gaining momentum in the market. These technologies enable real-time monitoring, predictive analytics, and automation of forest operations, leading to increased profitability and pricing efficiency. The US and Canada are the major markets for forestry software in North America, with several companies based in the region offering solutions that cater to cut-to-length logging, trade regulations, and product dominance. The integration of mobile technology and sensor systems is further enhancing the capabilities of forestry software, making it an essential tool for forestry companies in the region.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Forestry Software Market Driver

The rise in adoption of cloud-based forestry software is the key driver of the market. Cloud-based forestry software is experiencing a significant rise in adoption among forestry businesses due to its numerous advantages over traditional on-premises solutions. One of the primary benefits of cloud-based forestry software is the reduction in operational costs, which stem from software/server updates, infrastructure failures, and hardware replacements. This technology offers a cost-effective alternative with a lower up-front cost and shorter implementation time compared to on-premise forestry software. Cloud-based forestry software eliminates the need for companies to procure and install storage and computing hardware, providing them with scalability, speed, and agility. This software enables forest management, logging management, mapwork harvester, inventory, and logistics management from anywhere, ensuring business consistency across geographically dispersed and remote locations.

Additionally, the software's geospatial capabilities facilitate forest operations, while fire detection and AI-based forestry solutions enhance productivity and profitability. Big data and mobile technology integration further improve decision-making and pricing processes, ensuring compliance with trade regulations and maintaining product dominance in the market.

Forestry Software Market Trends

Increasing demand for AI-based forestry is the upcoming trend in the market. The forestry industry is experiencing a significant rise in the adoption of technology, particularly in the areas of forest management and logging operations. Forestry software, which includes both On-Premises and Cloud-Based solutions, is playing a pivotal role in optimizing forestry processes. AI-based forestry software is gaining momentum, revolutionizing the sector with advanced capabilities such as predictive analytics, geospatial mapping, fire detection, and inventory management. These intelligent systems enable forestry companies to forecast harvest production, manage inventory levels, and analyze demand patterns more effectively. AI also enhances logistics management by optimizing transportation routes and reducing fuel consumption. Cut-to-length harvesting and product dominance are other key areas where AI-based forestry software is making a significant impact.

Moreover, the integration of big data, mobile technology, and trade regulations into forestry software solutions is streamlining forest operations. The use of AI in forestry is spreading across all regions, with companies leveraging its potential to improve profitability, pricing strategies, and overall operational efficiency.

Forestry Software Market Challenge

The availability of open-source forestry software is a key challenge that is affecting market growth. The market is witnessing a significant shift towards open-source solutions due to their affordability and ease of implementation. Forest departments in developing economies, such as China, India, and South America, are increasingly adopting open-source forestry software due to limited capital investment for licensed software. This trend is particularly prevalent among small forestry companies with a low number of employees. Cloud-based and on-premises forestry software solutions offer functionalities for forest management, logging management, mapwork harvester, inventory, logistics management, and more. Advanced technologies like Artificial Intelligence (AI), Big data, geospatial analysis, fire detection, and cut-to-length are gaining momentum in forest operations. However, open-source software poses a threat to the market due to its cost-effectiveness.

The rise of digitalization, mobile technology, and technology-driven forestry are also contributing to the market's growth. Despite the challenges posed by open-source software, the market for forestry software is expected to grow due to the increasing need for profitability, pricing optimization, and compliance with trade regulations.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AFRY AB - The company offers forestry software as namely AFRY Smart Forestry Manager for the mapping, monitoring and simulating of forest supply chains.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ArborNote

- ArboStar

- Assisi Software Corp

- Caribou Software

- Creative Information Systems Inc.

- Disprax Pty Ltd

- Enfor Consultants Ltd.

- Esri Global Inc.

- Forest Metrix

- Forestry Systems Inc.

- Legna Software LLC

- Mason Bruce and Girard Inc.

- Microforest Pty Ltd

- Orbis

- PlanIT Geo

- Remsoft

- Softree Technical Systems Inc.

- TRACT

- Trimble Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Forestry software has gained momentum in recent years due to the digitalization of forest operations. The market for forestry software includes both on-premises and cloud-based solutions, catering to the diverse needs of forest management and logging operations. Forestry software enables effective inventory management, logistics management, and mapwork harvester planning. The integration of geospatial technology, artificial intelligence, and big data analytics in forestry software has led to the development of AI-based forestry solutions. These advanced technologies aid in cut-to-length optimization, fire detection, and trade regulations compliance. The rise in the adoption of forestry software is driven by the need for improved profitability, pricing accuracy, and operational efficiency.

Further, mobile technology has further expanded the accessibility of forestry software, enabling real-time monitoring and decision-making. The market for forestry software is expected to continue gaining momentum due to the increasing focus on sustainable forest management and the growing demand for technology-driven solutions in the forest industry.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.51% |

|

Market Growth 2024-2028 |

USD 519.49 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.97 |

|

Regional analysis |

North America, Europe, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 33% |

|

Key countries |

US, Canada, China, Russia, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AFRY AB, ArborNote, ArboStar, Assisi Software Corp, Caribou Software, Creative Information Systems Inc., Disprax Pty Ltd, Enfor Consultants Ltd., Esri Global Inc., Forest Metrix, Forestry Systems Inc., Legna Software LLC, Mason Bruce and Girard Inc., Microforest Pty Ltd, Orbis, PlanIT Geo, Remsoft, Softree Technical Systems Inc., TRACT, and Trimble Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -