Enjoy complimentary customisation on priority with our Enterprise License!

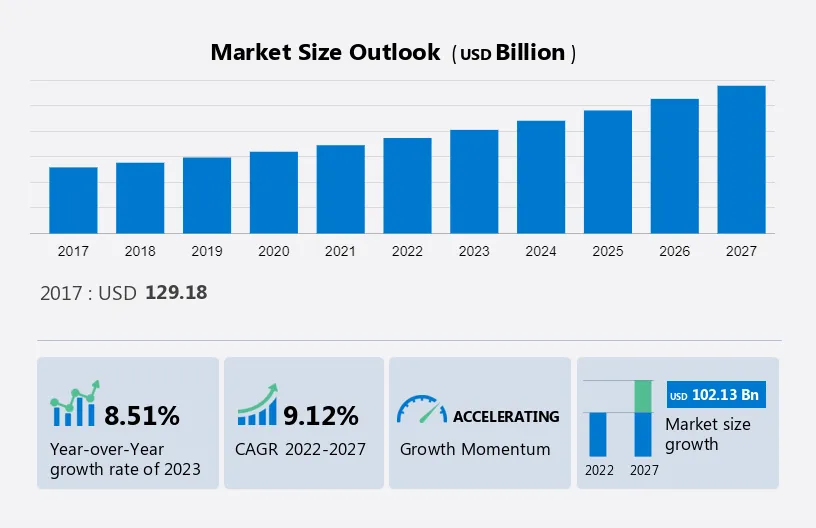

The Gaming Market size is estimated to grow by USD 102.13 billion, accelerating at a compound annual growth rate (CAGR) of 9.12% between 2022 and 2027.

The market is propelled by the burgeoning adoption of augmented reality (AR) and virtual reality (VR) games, catering to a diverse audience. The surge in e-sports popularity further fuels market expansion, with competitive gaming becoming a mainstream entertainment choice. Additionally, strategic partnerships and acquisitions among industry giants contribute significantly to market dynamics, fostering innovation and enhancing gaming experiences. As technology continues to evolve, the gaming sector stands at the forefront of entertainment, offering immersive experiences and driving unprecedented growth opportunities.What will be the Size of the Gaming Market During the Forecast Period?

To learn more about this report, Request Free Sample in PDF

The market continues to thrive on various fronts, driven by diverse factors such as the integration of education into gaming experiences, fostering learning and skill development. Family game time remains a cherished activity, promoting bonding and social interaction within households. Indoor games, spanning across genres like action, sports, and tactical missions, offer entertainment options for individuals of all ages. Enhanced by 3D realistic graphics, gaming experiences across platforms like tablets, mobile phones, consoles, and PCs are increasingly immersive and engaging. Moreover, insights from reports like the GSMA report provide valuable industry analysis, guiding stakeholders in navigating the dynamic landscape of the market.

In our comprehensive market report, we provide critical insights equip stakeholders with strategic tools to navigate the dynamic gaming industry landscape effectively. Here's how our report empowers decision-makers:

The market continues to flourish as a leading form of entertainment, providing stress relief, teamwork opportunities, and a sense of achievement for players of all ages. From kids to older adults, gaming on platforms like iPads offers joy and self-satisfaction. With the rise of home entertainment systems, families engage in bonding experiences through gaming sessions. The youth population drives demand for indoor games, including shooters, action, and sports genres, featuring 3D realistic graphics and tactical missions. Moreover, advancements like 5G connectivity, as highlighted in the GSMA report, enhance the gaming experience across tablets, mobile phones, TVs/consoles, and PCs/MMOs. Our researchers analyzed the data with 2022 as the base year and the key drivers, trends, and challenges. A holistic analysis of upcoming trends and challenges will help companies refine their marketing strategies to gain a competitive advantage.

The growing adoption of AR and VR games is a major factor driving the market share. AR/VR is the integration of visual and audio content with a user's environment in real time. With the rising awareness of AR gaming, the adoption of AR/VR devices is likely to increase during the forecast period. Therefore, game developers prefer AR and VR devices to traditional devices. Companies such as Sony and Microsoft are developing these platforms using cutting-edge three-dimensional (3D) technologies. In addition, developers have started developing AR games for HoloLens, a product of Microsoft. For instance, in January 2022, Microsoft HoloLens 2 was launched in India, which includes sensors that enable head and eye tracking and is designed to allow users to interact with holograms.

The affordability and wide availability of mobile AR games are driving the growth of the global market. For instance, in November 2021, Niantic Inc. partnered with Fold, a cryptocurrency debit card company, and launched a new game dubbed FoldAR. The game is a part of the metaverse and is similar to Pokemon GO. Thus, the rising adoption of AR and VR games will drive the growth of the global market during the forecast period.

The increasing emergence of cloud gaming is an ongoing trend in the market share. This can be accessed through Internet-connected devices for free or through paid subscriptions. This technology enables users to stream video games from the web. The increasing popularity of social media and mobile is supporting the growth of cloud gaming. These services have the potential to reach non-core gamers who play games on social media and mobile devices because of the cost-effective price structure of cloud gaming.

Furthermore, this eliminates the need for high-quality graphic cards in PCs and mandatory PC upgrades and offers an enhanced experience on any device that has average processing capability. Therefore, it allows users to access these games on PCs with less storage and processing capacity. Thus, the emergence of this technology will drive the growth of the global market during the forecast period.

Regulation of loot boxes is a major challenge restricting the growth of the market. Loot boxes are virtual items that players can purchase with real money in order to obtain randomized in-game rewards. While they can enhance the experience for some players, they have also been criticized for promoting gambling and exploiting vulnerable individuals, particularly children. Regulators in various countries have been taking action to address these concerns. For example, in 2020, the UK government announced that loot boxes would be classified as gambling and regulated accordingly. Similarly, the Belgian Gaming Commission has banned loot boxes altogether, while other countries such as Australia and the Netherlands have also taken steps to regulate them.

These regulations can have significant implications for game developers and publishers, who may need to modify their games or business models in order to comply. They may also affect player behavior, as some may be less willing to purchase loot boxes if they are subject to stringent regulations, which will restrict the growth of the market in the forecast period.

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Market Customer Landscape

In the type channel segment of the market, diverse preferences cater to various demographics and interests. Role-playing games offer immersive experiences for players seeking entertainment and escapism, fostering a sense of achievement and satisfaction. Video games, accessible across platforms like iPads and home entertainment systems, provide stress relief and joy, appealing to both kids and older adults. Additionally, multiplayer games promote teamwork and social interaction, making them ideal for family game time or bonding among peers. Indoor games serve as educational tools, engaging youth populations and addressing social anxiety through interactive gameplay. Shooter games offer action-packed entertainment, further diversifying the gaming experience and attracting enthusiasts looking for excitement and challenge.

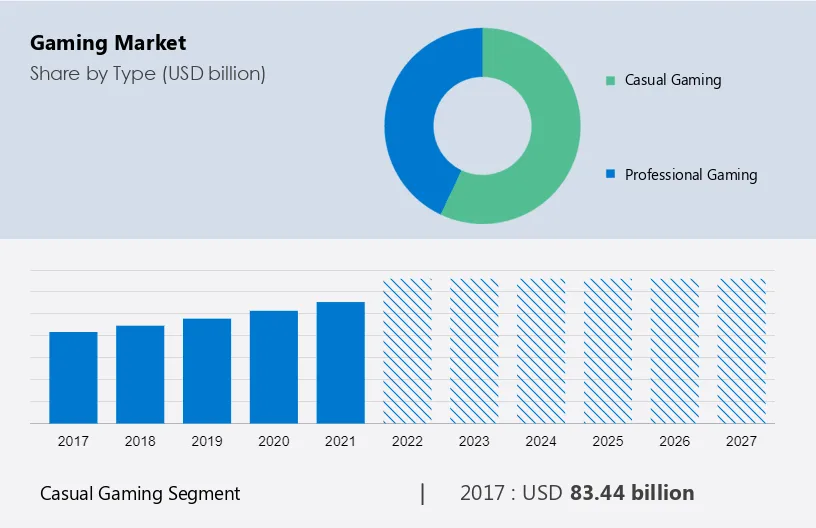

The market share growth by the casual gaming segment will be significant during the forecast period. The term casual refers to games that don't require a great deal of time to be played, won, and earned. Casual gamers are gamers who don't spend a lot of time playing video games. These service providers generate revenue by licensing software to end users. The casual games segment is growing with the spread of mobile games. Casual gamers don't spend money on these peripherals. Most casual gamers prefer mobile devices over PCs and consoles because of easy access to the games. In addition, casual gamers play games online on their mobile devices, as it is easy for them to play games of their choice from anywhere at any time.

Get a glance at the market contribution of various segments View the PDF Sample

The segment was valued at USD 83.44 billion in 2017 and continued to grow until 2021. The segment has become increasingly popular, driven by a number of factors such as its accessibility, where the games are easy to pick up and play, and they can be played on a variety of devices, including smartphones, tablets, and PCs. This makes them accessible to a wide range of players, and another such drive can be its social Interaction model, where many casual games are designed to be played with friends or family members, either locally or online. This social element adds an extra layer of fun and engagement to the experience, which can drive the segment in the forecast period.

For more insights on the market share of various regions Download PDF Sample now!

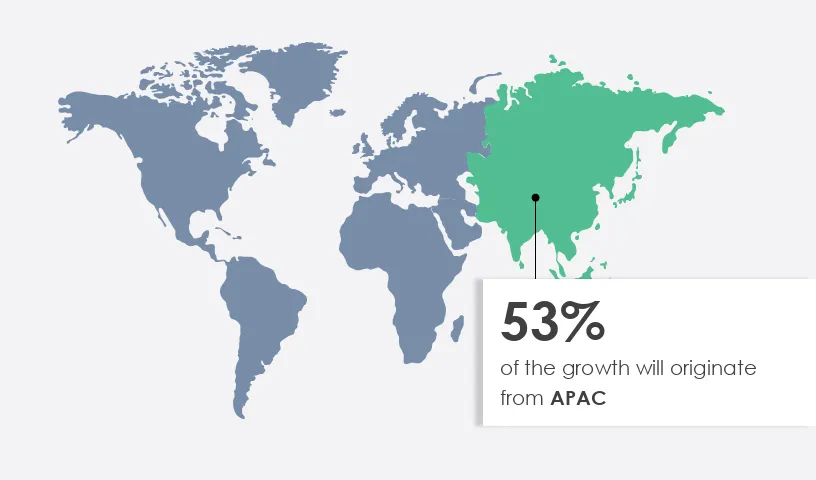

APAC is estimated to contribute 53% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

APAC is considered the center of pro gamers. The prevalence of e-sports in developing countries such as Taiwan, Malaysia, and Singapore will contribute to the growth of the market in APAC during the forecast period. Major digital gaming companies operating in the region include China-based Tencent and GungHo Online Entertainment. In addition, most hardware suppliers, including Sony and Nintendo, are based in Japan, so most innovations in this technology are adopted in Japan. China dominates the market in this region. The country has over 700 million active internet users. These factors have increased the popularity in the country.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Microsoft Corp.- The company offers various games such as Asphalt 9, Hill climbing racing games, Minecraft, and Robolox games.

The report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

.The market offers more than just entertainment; it provides avenues for stress relief, teamwork, and a sense of achievement. From kids to older adults, gaming consoles like TV/console, PC/MMO, tablet, and mobile phone cater to diverse demographics, fostering joy and self-satisfaction through immersive experiences. As the youth population increasingly embraces gaming, it intertwines with education through educational courses and tactical missions, leveraging 3D realistic graphics and 5G technology. Gaming serves as a platform for family game time and home entertainment systems, combating social anxiety and promoting teamwork. Reports like the GSMA report highlight the industry's growth and significance, showcasing its pivotal role in modern society's leisure and educational landscapes.

The market caters to diverse preferences, offering indoor games and leisure activities like painting and crafting for individuals seeking self-satisfaction and traction in their downtime. With 4G connectivity and mobile cellular subscriptions, players delve into interactive social media games, though concerns regarding addiction issues persist, especially in intense gaming genres like shooter ones and role-playing games featuring attractive weapons. Multiplayer game functionality enhances social interaction, creating immersive game worlds where players engage in sports simulations and collaborative ventures, sometimes even integrating education courses. Technological advancements like cloud gaming services and emerging economies drive the market forward, facilitating seamless internet connectivity and bandwidth network connectivity, shaping the future of gaming experiences globally.

The market report forecasts market growth by revenue at global, regional & country levels and provides market trends and analysis and growth opportunities from 2017 to 2027.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

182 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 9.12% |

|

Market growth 2023-2027 |

USD 102.13 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

8.51 |

|

Regional analysis |

APAC, North America, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 53% |

|

Key countries |

US, China, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Activision Blizzard Inc., Apple Inc., Bandai Namco Holdings Inc., Bowlmor AMF, Chicago Gaming Co., DeNA Co. Ltd., Electronic Arts Inc., Epic Games Inc., GungHo Online Entertainment Inc., Microsoft Corp., NetEase Inc., Netmarble Corp., Niantic Inc., Nintendo Co. Ltd., Rovio Entertainment Corp., Sony Group Corp., Square Enix Holdings Co. Ltd., The Walt Disney Co., Ubisoft Entertainment, and Zeptolab UK Ltd. |

|

Market dynamics |

Parent market analysis, Market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, market growth analysis for market forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Platform

8 Market Segmentation by Device

9 Customer Landscape

10 Geographic Landscape

11 Drivers, Challenges, and Trends

12 Vendor Landscape

13 Vendor Analysis

14 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.