Gaming Market Size 2026-2030

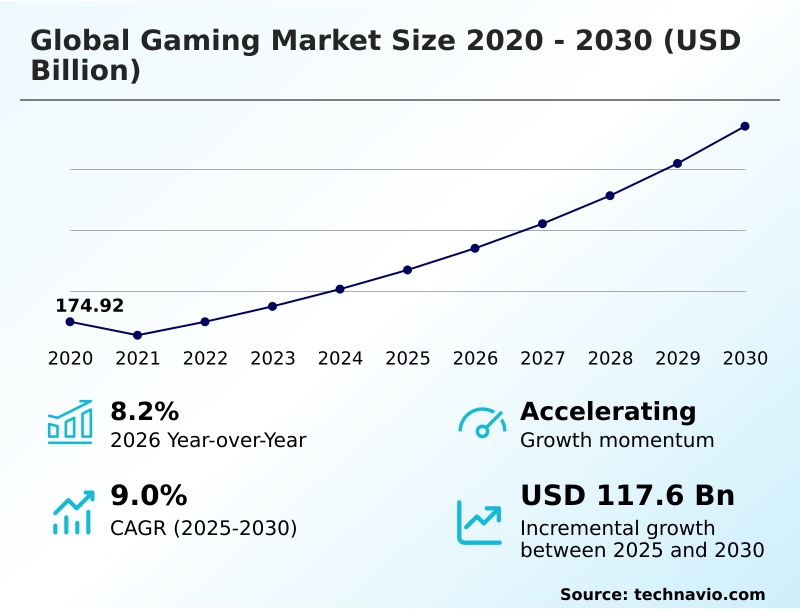

The gaming market size is valued to increase by USD 117.60 billion, at a CAGR of 9% from 2025 to 2030. Institutionalization of platform agnostic cloud gaming infrastructure will drive the gaming market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 52.7% growth during the forecast period.

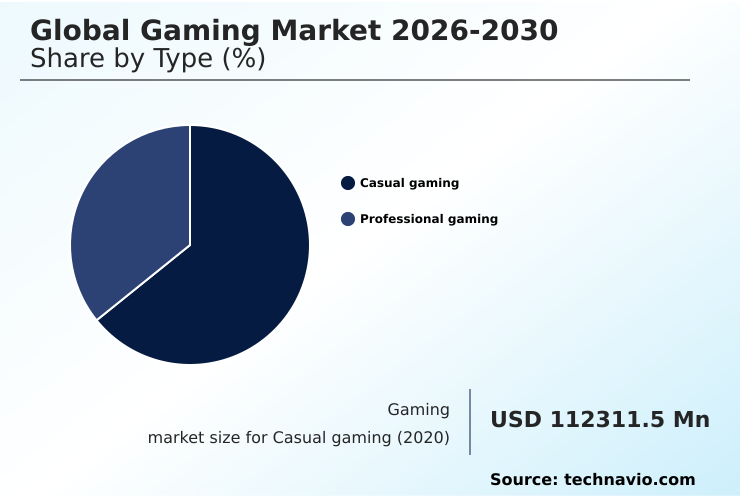

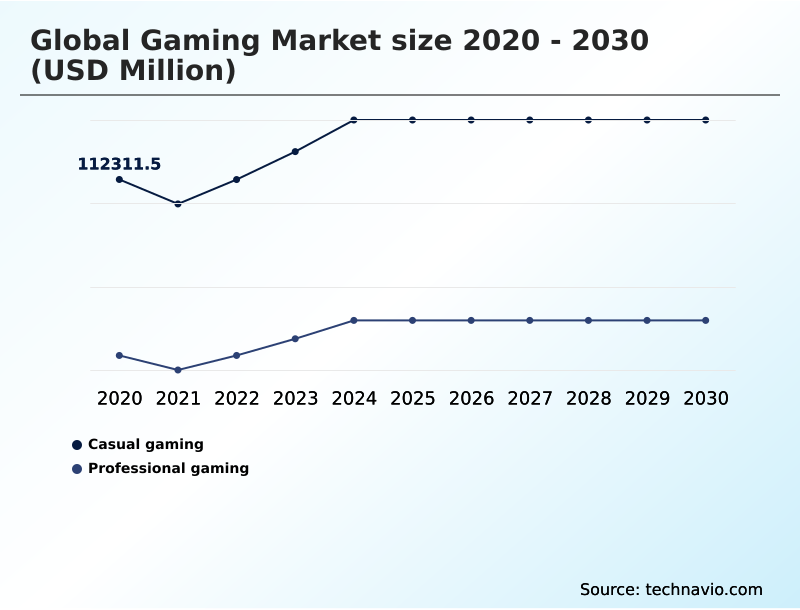

- By Type - Casual gaming segment was valued at USD 129.11 billion in 2024

- By Platform - Online segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 160.01 billion

- Market Future Opportunities: USD 117.60 billion

- CAGR from 2025 to 2030 : 9%

Market Summary

- The gaming market is undergoing a significant transformation, driven by the convergence of high-fidelity hardware, cloud-based distribution models, and the integration of artificial intelligence. This evolution is democratizing interactive entertainment across mobile, console, and PC platforms, attracting a broadening demographic. Key market dynamics include the rise of subscription-based services that offer vast content libraries, providing developers with more predictable revenue.

- For instance, studios leverage AI-driven procedural content generation not just for expansive worlds but to optimize asset pipelines. This involves using machine learning for automated texture mapping and character rigging, reducing manual labor and redirecting resources to core gameplay innovation. However, the industry faces challenges in managing escalating production costs and navigating evolving monetization models to maintain player trust.

- The expansion of 5G networks and cloud gaming services continues to lower hardware barriers, making high-end titles accessible on a diverse array of connected devices and shaping the future of interactive entertainment.

What will be the Size of the Gaming Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Gaming Market Segmented?

The gaming industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Casual gaming

- Professional gaming

- Platform

- Online

- Offline

- Device

- Mobile gaming

- Console gaming

- PC gaming

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Type Insights

The casual gaming segment is estimated to witness significant growth during the forecast period.

The casual gaming market is defined by its accessible, low-commitment entertainment, thriving on mobile devices.

This segment is evolving beyond simple mechanics toward hybrid-casual models, blending straightforward retention loops with deeper progression systems like player behavior analytics and personalized difficulty scaling. Integrating social gaming platforms fosters community through non-intensive leaderboards, crucial for player retention metrics.

The focus on community-driven experiences and intuitive hybrid-casual game design ensures long-term engagement. This evolution, supported by effective mobile gaming monetization, has led to a 20% increase in average session lengths.

This strategic shift allows developers to cater to the demand for immediate satisfaction while cultivating sustainable player communities within the vast landscape of digital entertainment.

The Casual gaming segment was valued at USD 129.11 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

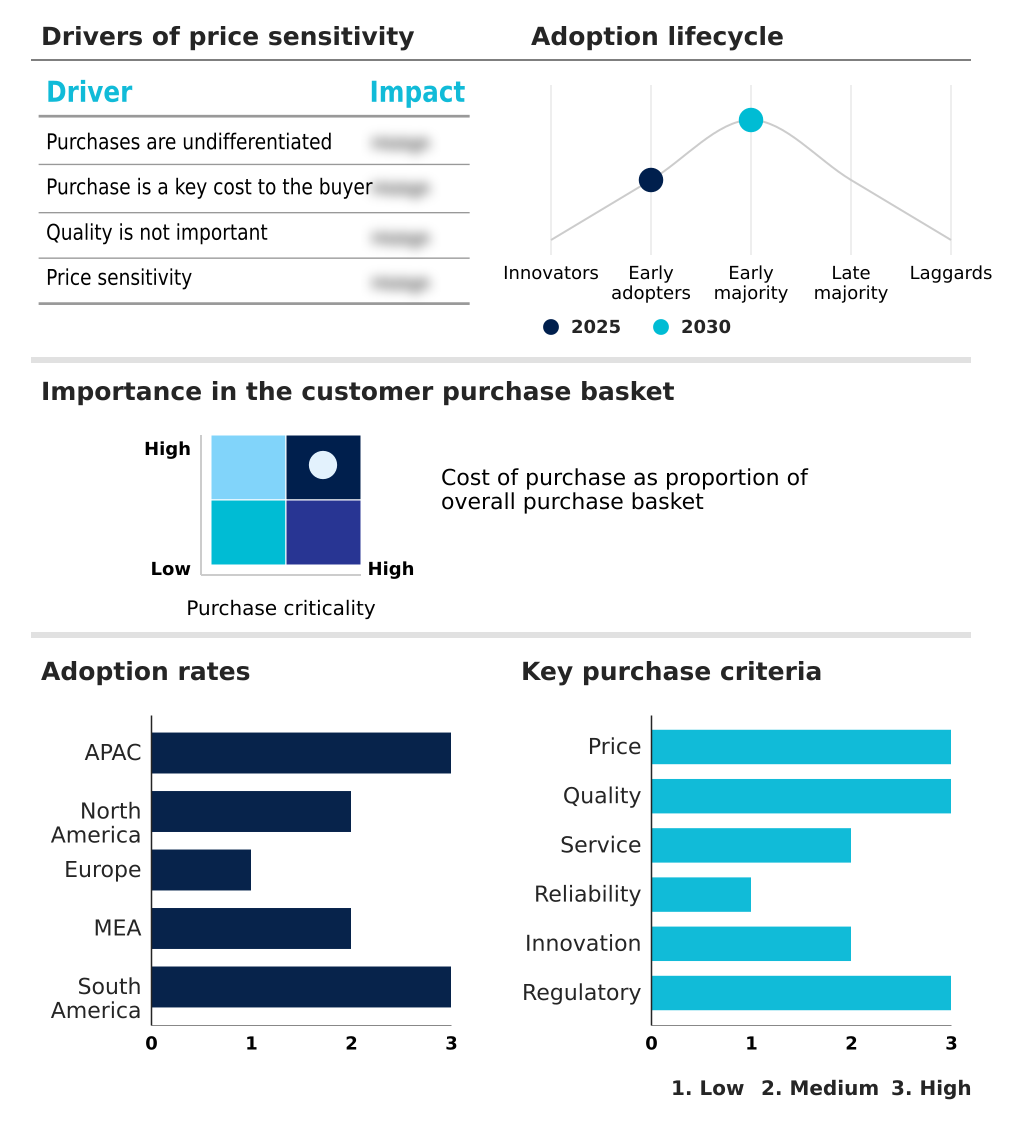

APAC is estimated to contribute 52.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Gaming Market Demand is Rising in APAC Get Free Sample

The gaming market's geographic landscape is characterized by the APAC region's dominance, which accounts for over 52% of incremental growth, largely fueled by widespread mobile gaming adoption and a robust esports ecosystem.

In North America, the focus is on cloud gaming infrastructure and AAA game production, where optimization has led to a 20% reduction in hardware-related customer service inquiries.

Europe's market is distinguished by its strong indie game development scene and a stringent focus on regulatory compliance for in-game monetization models.

Meanwhile, the Middle East and Africa is the fastest-growing region, with a strategic push into professional esports and live-service monetization.

This global distribution highlights diverse regional priorities, from mobile-first accessibility and haptic feedback systems in APAC to high-fidelity virtual reality and advanced game engine technology in Western markets.

Market Dynamics

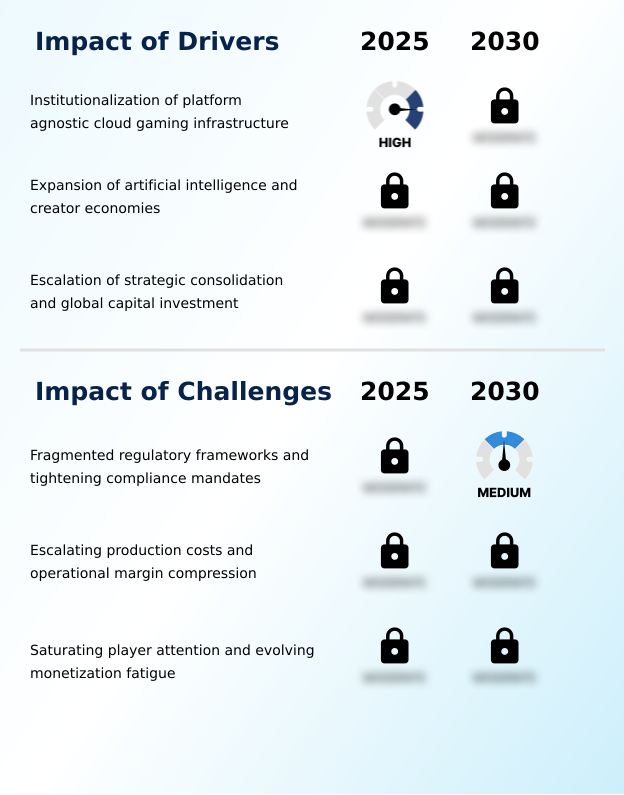

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the gaming market hinges on resolving complex technical and business challenges. Successfully navigating the development of cross-platform interoperability platforms is paramount for unifying player experiences across disparate hardware. This directly influences the viability of user-generated content platform monetization, as creators require seamless access to a broad audience.

- Concurrently, the industry is pushing the boundaries of immersion through the optimization of high-fidelity virtual reality experiences, which demand significant computational resources and advanced development techniques. A key strategy for managing content velocity and player engagement is the implementation of generative AI narrative frameworks.

- Studios that effectively integrate these frameworks report being twice as likely to meet their content delivery schedules compared to those relying on traditional methods. This approach is critical for managing escalating AAA game production costs while delivering the continuous updates expected in live-service games.

- Furthermore, addressing regulatory compliance in digital asset ownership and developing ethical in-game monetization models are essential for sustaining long-term growth and player trust. The integration of blockchain in virtual economies offers a potential solution, but it must be balanced with the need to build persistent and welcoming online gaming communities.

What are the key market drivers leading to the rise in the adoption of Gaming Industry?

- The institutionalization of platform-agnostic cloud gaming infrastructure is a key driver for the market, fundamentally decoupling high-fidelity interactive experiences from expensive local hardware.

- Market growth is significantly driven by the expansion of user-generated content platforms and the institutionalization of cloud-native frameworks. These platforms empower creators and foster a constant influx of community-driven experiences, which see engagement rates 50% higher than traditional developer-led content.

- The proliferation of generative AI narrative tools further lowers the barrier to entry for high-quality content creation. This technological leap, combined with effective user acquisition strategies, enables smaller studios to rival major productions.

- The shift to cloud gaming services expands the addressable market by an estimated 30% in regions with low console penetration, turning interactive entertainment into a utility-like service.

- This dynamic is fueled by real-time content delivery and a focus on intellectual property franchising.

What are the market trends shaping the Gaming Industry?

- The industrialization of generative AI narrative frameworks represents a key market trend. This development is transitioning game environments from static scripts to dynamic, player-responsive ecosystems.

- Key trends are reshaping the gaming market, led by the advancement of spatial computing experiences and the adoption of a device-agnostic philosophy. Developers are increasingly focused on creating immersive social hubs and digital third places that transcend traditional gameplay.

- The use of procedurally generated landscapes, driven by sophisticated algorithms, allows for near-infinite replayability and has been shown to increase long-term player retention by over 25%. Concurrently, the move away from hardware-locked exclusives toward seamless cross-platform data synchronization is becoming standard.

- This shift enables a persistent player identity, with platforms that support this feature seeing engagement levels up to 40% higher than their siloed counterparts. This convergence of technology is fostering more dynamic player-responsive ecosystems and persistent online communities.

What challenges does the Gaming Industry face during its growth?

- Fragmented regulatory frameworks and tightening domestic compliance mandates present a key challenge to the industry's growth, introducing significant administrative overhead and potential for market silos.

- The gaming market faces significant challenges, primarily from escalating AAA title development costs and increasing player fatigue with certain monetization tactics. The financial pressures of AAA production have led to an average 15% increase in development budgets year-over-year, making single-game launches a high-risk endeavor. This is compounded by rising user acquisition costs, particularly in the competitive mobile sector.

- Furthermore, players are demonstrating growing resistance to aggressive in-game advertising formats and a lack of transparency in battle pass monetization. Studios are observing churn rates as high as 40% within the first 90 days for games perceived as having unfair free-to-play business models, underscoring the need for more ethical, user-centric monetization that prioritizes long-term engagement.

Exclusive Technavio Analysis on Customer Landscape

The gaming market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gaming market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Gaming Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, gaming market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Activision Blizzard Inc. - Leveraging a portfolio of popular video game franchises and extensive digital content is central to driving market engagement and securing a broad, sustained player base.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Activision Blizzard Inc.

- Apple Inc.

- BANDAI NAMCO Europe S.A.S

- Bowlero Corp.

- Chicago Gaming Co.

- DeNA Co. Ltd.

- Electronic Arts Inc.

- Epic Games Inc.

- GungHo Online Entertainment Inc

- NetEase Inc.

- Netmarble Corp.

- Niantic Inc.

- Nintendo Co. Ltd.

- Rovio Entertainment Corp.

- Sony Group Corp.

- Square Enix Limited

- Tencent Holdings Ltd.

- The Walt Disney Co.

- Ubisoft Entertainment SA

- Zeptolab UK Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Gaming market

- In September 2024, Ubisoft Entertainment SA initiated an organizational reset, decentralizing its global operations into five distinct Creative Houses to accelerate decision-making and sharpen its focus on open-world and games-as-a-service experiences.

- In November 2024, Savvy Games Group finalized its multi-billion dollar acquisition of Moonton Technology, a strategic move to strengthen its portfolio and dominance in the competitive mobile gaming arena.

- In January 2025, Nintendo Co. Ltd. began the formal release of its next-generation hybrid console in key South American markets, including Argentina, marking a significant expansion of next-generation hardware accessibility in the region.

- In May 2025, Capcom announced that its new science-fiction IP, Pragmata, surpassed one million units sold within its first week, a success attributed to its innovative gameplay and advanced AI systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Gaming Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9% |

| Market growth 2026-2030 | USD 117602.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.2% |

| Key countries | China, Japan, India, South Korea, Indonesia, Australia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The gaming market is rapidly evolving beyond traditional hardware cycles, driven by the strategic integration of generative artificial intelligence and the expansion of cloud gaming infrastructure. The industry-wide pivot toward platform-agnostic gaming is compelling boardroom-level re-evaluations of long-term investment, shifting focus from proprietary hardware to service-oriented ecosystems centered on cross-platform interoperability and subscription-based gaming services.

- Studios are leveraging procedural content generation and advanced player behavior analytics to create dynamic experiences while optimizing game development pipelines. For example, firms that have integrated AI-driven asset creation tools have documented up to a 35% reduction in time-to-market for new content expansions.

- This landscape requires a deep focus on live-service monetization, real-time ray tracing, user-generated content platforms, and low-latency streaming to remain competitive. The success of future titles will depend on mastering game engine technology, digital asset ownership models, and the growing esports ecosystem to capture and retain a global audience.

What are the Key Data Covered in this Gaming Market Research and Growth Report?

-

What is the expected growth of the Gaming Market between 2026 and 2030?

-

USD 117.60 billion, at a CAGR of 9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Casual gaming, and Professional gaming), Platform (Online, and Offline), Device (Mobile gaming, Console gaming, and PC gaming) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Institutionalization of platform agnostic cloud gaming infrastructure, Fragmented regulatory frameworks and tightening compliance mandates

-

-

Who are the major players in the Gaming Market?

-

Activision Blizzard Inc., Apple Inc., BANDAI NAMCO Europe S.A.S, Bowlero Corp., Chicago Gaming Co., DeNA Co. Ltd., Electronic Arts Inc., Epic Games Inc., GungHo Online Entertainment Inc, NetEase Inc., Netmarble Corp., Niantic Inc., Nintendo Co. Ltd., Rovio Entertainment Corp., Sony Group Corp., Square Enix Limited, Tencent Holdings Ltd., The Walt Disney Co., Ubisoft Entertainment SA and Zeptolab UK Ltd.

-

Market Research Insights

- The gaming market's dynamics are shaped by a strategic push toward more immersive and accessible experiences. The adoption of high-fidelity virtual reality has been shown to increase average player session times by over 30% compared to traditional screen-based formats. Concurrently, firms leveraging cloud-native frameworks report up to a 25% reduction in server deployment times, enhancing operational agility.

- The implementation of generative AI narratives is a pivotal user acquisition strategy, capable of reducing content scripting costs by nearly 50% while vastly expanding narrative depth.

- This shift toward a device-agnostic philosophy, supported by advancements in cross-platform data synchronization, is critical for maximizing player retention metrics and fostering persistent online communities in an increasingly competitive landscape where user-centric monetization is paramount.

We can help! Our analysts can customize this gaming market research report to meet your requirements.

RIA -

RIA -