Enjoy complimentary customisation on priority with our Enterprise License!

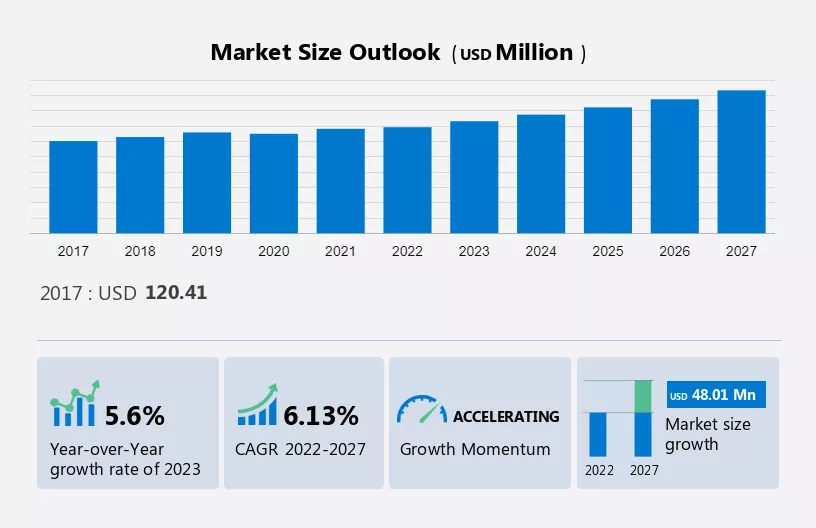

The Gaming Software Market size is estimated to grow at a CAGR of 6.13% between 2022 and 2027. The market size is forecast to increase by USD 48.01 million. The growth of the market depends on several factors, including revolutionary improvements in gaming engines, growing developments in cross-platform gaming support, and in-app purchases from freemium customers.

This report extensively covers market segmentation by type (mobile games, console games, and PC games), revenue stream (BOX/CD game, shareware, freeware, and in-app purchases), and geography (APAC, North America, Europe, South America, and Middle East and Africa). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report consists of historic market data from 2017 to 2021.

Figure 1: Gaming Software Market Share

Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Growing developments in cross-platform gaming support is a key factor driving the growth of the market. A rapid increase in the number of gamers using multiple gaming platforms, ranging from gaming consoles to mobile phones, has created significant demand for the development of cross-platform supportability. Cross-platform games are allowing gamers to play online multiplayer games together, irrespective of their hardware platforms.

The growing popularity of online multiplayer games, specifically in the MOBA genre (such as PUBG from Tencent Games, Fortnite from Epic Games, and Call of Duty from Activision Blizzard), has led to many developments in online multiplayer cross-platform gaming software among vendors. Vendors are offering either partially or fully supporting cross-platform compatibility.

Integration with social media platforms is a key trend influencing the growth of the market. The market is witnessing a significant trend with the rise of instant gaming software on social media platforms. Global users are spending more time on these platforms, creating a vast customer base for vendors. In 2018, daily social media usage increased by 63%, reaching 2-2.5 hours on average.

Capitalizing on this, vendors are creating and releasing instant games in popular genres like arcade and strategy on platforms such as Facebook, Steam, WeChat, Anook, and Reddit. Collaborations with social media giants are also on the rise. For instance, Ubisoft partnered with WeChat to launch games, while Facebook opened its instant game platform to all developers. This expansion of instant gaming software on social media is propelling market growth and revenue.

Growth in online hacking and data breaches is a major challenge hindering the growth of the market. The surge in adopting online gaming software has made gamers vulnerable to heightened cybercrime risks. These gamers use interconnected platforms with inadequate security measures, providing easy entry points for hackers to access personal data. Some platforms even mandate saving credit/debit card info for in-game purchases, which hackers exploit using Trojans and ransomware for financial fraud.

Cybercriminals view gaming as a lucrative avenue for stealing and selling data or coercing users into sharing banking info through social engineering. High-profile platforms like Sony PlayStation Network, Microsoft Xbox Live, and Steam are prime targets. Globally, gamers have faced numerous credential-stuffing attacks, hampering online transactions and impacting vendors' revenues. Moreover, games often require social media access, demanding stringent data privacy adherence from vendors. Breaches can erode trust and operational efficiency, posing challenges to market growth.

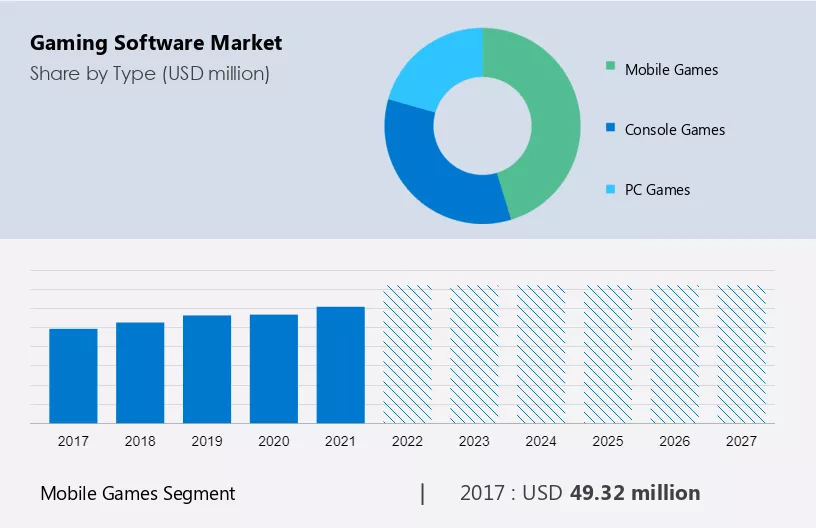

The market share growth by the mobile games segment will be significant during the forecast period. Mobile games include gaming software developed for mobile phones and tablets. The availability of low-cost, large-screen mobile phones with high display resolution and the growing access to high-speed internet through 5G technology in countries such as China, the US, Germany, and the UK is driving the adoption of mobile devices as a gaming platform.

Figure 2: Gaming Software Market by Type (2017-2027)

Get a glance at the market contribution of various segments View the PDF Sample

The mobile games segment started at USD 49.32 million in 2017, growing continuously until 2021. Increased profits in the global mobile gaming market, coupled with a rising number of casual and dedicated gamers, spurred numerous product launches. Many of these releases are free-to-play games with optional in-app purchases, now major revenue sources. Gamers often opt for in-app purchases to customize characters or access premium features. Flagship games, like Call of Duty: Mobile by Activision Blizzard, quickly gained traction, amassing over 35 million downloads within four days of launch in October 2019. Successful launches prompted vendors to port popular console and PC games to mobile platforms using advanced gaming engines, fueling further growth in this segment.

Based on the revenue stream BOX/CD game segment holds the largest market share. The segment is expected to grow slower than the overall market during the forecast period. Its position will remain the same as the largest market in 2027. Box/CD game dominate the global gaming software market as they provide an enhanced gaming experience to users. One of the major drivers of the market is the rising purchasing power of gamers. Increased purchasing power, along with the need for an enhanced gaming experience, has prompted gamers to opt for a higher generation of box/CD games with the 3D feature, which has fueled the adoption of box/CD games.

Even though the segment is expected to exhibit strong growth rates during the forecast period, premium pricing of home box/CD games and related accessories may impede the growth of the box/CD games during the forecast period. Moreover, the sales of gaming software through physical mediums, such as compact disks (CDs) and digital video disks (DVDs), are declining as most of the gamers are opting for digital distribution channels and cloud-based gaming services. Thus, the segment is expected to have a sluggish growth during the forecast period.

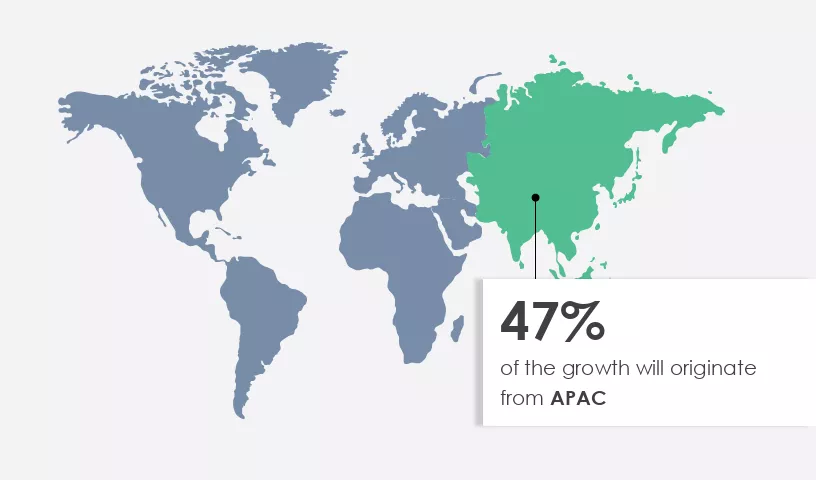

Figure 3: Gaming Software Market by Region

For more insights on the market share of various regions Download PDF Sample now!

APAC is estimated to contribute 47% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

APAC dominates the gaming software market led by China, Japan, and India, hosting the largest mobile gamer population. Smartphone proliferation and high-speed internet usage drive mobile gaming growth, supported by key players like Nintendo, Tencent, and Sony. Japan, South Korea, and China lead in online gamers due to strong internet infrastructure. Emerging Asian countries, including India, offer growth opportunities with rising smartphone use and impending 5G. PC and console-based AAA games thrive, fueled by higher incomes. China's lifted console ban spurs gaming growth, while Australia and New Zealand embrace freemium games and in-app purchases. APAC's rise continues with expanding smartphones and 5G.

The regional market experienced a positive impact from the COVID-19 pandemic in 2020-2021 as lockdowns prompted increased adoption of gaming software for recreation. This trend was particularly notable in developing nations like India. Furthermore, regional expansion by vendors is set to boost the market's growth. Diverse devices with varying screen sizes and graphics enhance user experiences, aligning with evolving technology trends that heighten gaming appeal and demand for software. This anticipates continued growth in the regional gaming software market throughout the forecast period.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Tencent- The company offers gaming software Tencent QQ which is designed to play online social games like Pub G.

The research report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Activision Blizzard Inc., Aristocrat Leisure Ltd., AT and T Inc., Bandai Namco Holdings Inc., Capcom Co. Ltd., Daybreak Game Co. LLC, Electronic Arts Inc., Epic Games Inc., Konami Group Corp., Krafton Inc., Microsoft Corp., Nintendo Co. Ltd., Playtika Holding Corp., Roblox Corp., Sega Sammy Holdings Inc., Sony Group Corp., Take Two Interactive Software Inc., Tencent Holdings Ltd., Ubisoft Entertainment, and Unity Software Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The report forecasts market growth by revenue at global, regional & country levels and analyzes the latest trends and growth opportunities from 2017 to 2027.

|

Gaming Software Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.13% |

|

Market growth 2023-2027 |

USD 48.01 million |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

5.6 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 47% |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Activision Blizzard Inc., Aristocrat Leisure Ltd., AT and T Inc., Bandai Namco Holdings Inc., Capcom Co. Ltd., Daybreak Game Co. LLC, Electronic Arts Inc., Epic Games Inc., Konami Group Corp., Krafton Inc., Microsoft Corp., Nintendo Co. Ltd., Playtika Holding Corp., Roblox Corp., Sega Sammy Holdings Inc., Sony Group Corp., Take Two Interactive Software Inc., Tencent Holdings Ltd., Ubisoft Entertainment, and Unity Software Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements.

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Type

7 Market Segmentation by Revenue Stream

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights