Gaming Software Market Size 2025-2029

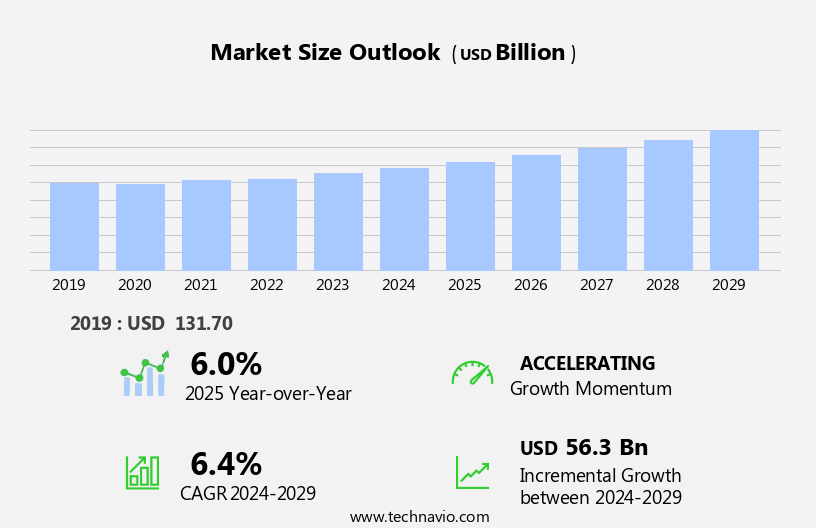

The gaming software market size is forecast to increase by USD 56.3 million, at a CAGR of 6.4% between 2024 and 2029.

- The market is experiencing significant growth, driven by revolutionary advancements in gaming engines that support experiences in tablet games. This technological evolution is attracting a larger player base and fueling the market's expansion. Another key trend is the increasing popularity of eSports, which has transformed gaming from a pastime into a professional sport, creating new revenue streams and opportunities for market participants. However, the high capital requirement for developing advanced gaming software and the need for strong online platforms and development tools pose challenges.

- Companies must invest heavily in research and development, marketing, and infrastructure to compete effectively in this dynamic and competitive landscape. To capitalize on market opportunities and navigate challenges, gaming software companies must stay abreast of emerging technologies and consumer preferences, while also maintaining a strong financial position. Augmented reality and virtual reality technologies are revolutionizing the gaming industry, providing new dimensions to gaming experiences.

What will be the Size of the Gaming Software Market during the forecast period?

- The market is witnessing significant advancements, with artificial intelligence (AI) playing a pivotal role in enhancing game accessibility and player experience. The market also caters to video gamers on mobile devices, including smartphones and tablets, through mobile gaming software. Cultural sensitivity is a growing concern, leading to the adoption of inclusive design and localization tools. Game preservation is another trend, with data mining and procedural generation techniques used to revive legacy games. Live operations, game events, and player behavior analysis are essential for monetization strategies, which include content updates, player support, and game balance adjustments.

- Game Engines are being optimized with AI to improve performance and enable cross-platform development. Machine learning algorithms are employed for game economy modeling and player segmentation. Cloud infrastructure, edge computing, and game physics are crucial for delivering seamless gaming experiences. Security is paramount, with game updates addressing vulnerabilities and advertising networks ensuring player privacy. Game modding and graphical fidelity continue to be key areas of focus for developers.

How is this Gaming Software Industry segmented?

The gaming software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Mobile games

- Console games

- PC games

- Revenue Stream

- Box and CD game

- Shareware

- Freeware

- In-app purchases

- Platform

- Game engine

- Gaming tools

- Audio engine

- Physics engine

- End-user

- Individual

- Enterprise

- Geography

- North America

- US

- Canada

- Europe

- Germany

- Russia

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

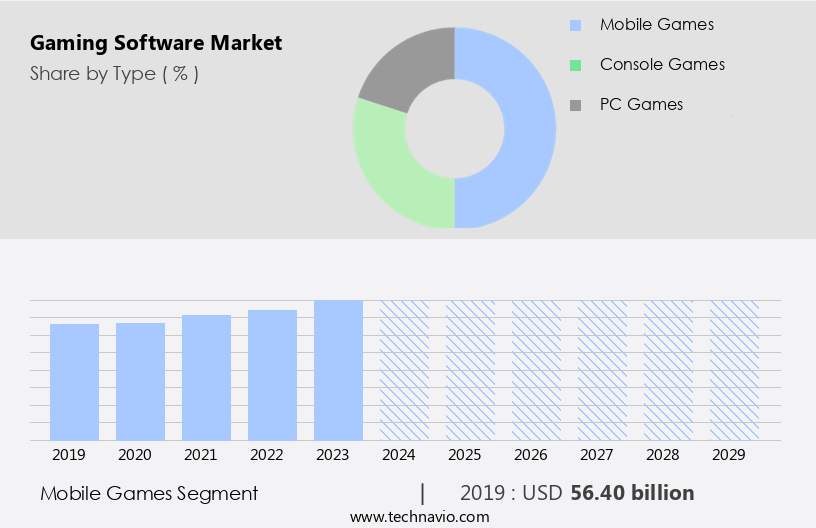

By Type Insights

The mobile games segment is estimated to witness significant growth during the forecast period. Mobile Gaming software, a segment of the dynamic gaming industry, has witnessed significant growth due to the widespread use of mobile phones and tablets. The availability of affordable, high-resolution mobile devices and increasing access to high-speed Internet through 5G technology in major markets like China, the US, Germany, and the UK, has boosted mobile gaming as a preferred platform. In 2024, approximately 2 billion mobile gamers were active worldwide. Mobile games dominate online application stores such as Apple App Store and Google Play, accounting for 25%-30% of the applications downloaded on Android and iOS platforms in 2023.

One significant segment of this market includes games used for competitive play, such as those in the E-sports scene. These include popular titles like Dota 2 and League of Legends, which are supported by platforms like Faceit and ESL. Game analytics, an essential component of the gaming industry, is used to monitor and analyze player behavior, game performance, and user experience. AI scripting and physics engines power game mechanics, ensuring realistic gameplay user experiences. App stores serve as crucial distribution channels for game developers, enabling them to reach a global audience. Game streaming and cloud gaming have emerged as new trends, offering players the convenience of playing games on various devices without the need for high-end hardware. Game design software, including level design, level editor, user experience design, user interface design, and game narrative tools, enable developers to create engaging and captivating games.

The Mobile games segment was valued at USD 56.40 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth, particularly in the Asia Pacific (APAC) region. With China, Japan, and India as leading countries, APAC dominates the market due to the largest number of mobile gamers. The increase in smartphone penetration and high-speed Internet services have led to increased engagement with mobile applications, specifically video games. Major players, such as Nintendo, Tencent, Bandai Namco Entertainment, Sega Games, and Sony, are based in APAC and contribute to the market's growth by continuously developing new gaming software for smart devices. These companies focus on upgrading game elements, including graphics, scripts, music, and software programs, to enhance the user experience.

Game analytics, AI scripting, and game design software are essential tools for creating engaging games. Game mechanics, level design, level editor, user experience design, and quality assurance ensure the game's functionality and user-friendliness. Game localization, testing, and game publishing help expand the reach of gaming software to diverse audiences. Strategy games, physics engine, augmented reality, online gaming, and virtual reality are emerging trends in the market. Console games, social gaming, and user-generated content are popular gaming genres, while in-app purchases and player engagement strategies are crucial for monetization. Game development tools, 3D modeling, and indie games are essential components of the market's ecosystem. Game marketing, character animation, cloud gaming, PC games, digital distribution, and audio middleware are other vital aspects of the gaming software industry. Version control, game engine, game design patterns, and player engagement are essential for efficient game development and maintenance. The market is expected to continue growing as technology advances and gaming becomes more accessible to a broader audience.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Gaming Software market drivers leading to the rise in the adoption of Industry?

- The significant advancements in gaming engines serve as the primary catalyst for market growth in this sector. The market is experiencing significant advancements, driven by the evolution of technologies in rendering, loading, animation, collision, graphical user interface, AR, VR, and AI. These improvements are revolutionizing gaming engines, enabling programmers to create more deep gameplay environments. Advanced gaming engines, such as Unity, Godot, CryENGINE, Unreal, and XNA Shader 3D Game Engine, offer enhanced features and are increasingly popular due to their multi-platform support. Companies prioritize gaming engines that provide core architecture and programming codes, as well as act as middleware in game development.

- Indie game developers and publishers are leveraging these tools to create engaging experiences for players. Version control, game design patterns, audio middleware, and in-app purchases are essential features that gaming engines offer to ensure player engagement and monetization. Game development tools, including these engines, continue to be a crucial investment for businesses in the gaming industry.

What are the Gaming Software market trends shaping the Industry?

- The growing popularity of eSports represents a significant market trend in the professional gaming industry. This burgeoning sector continues to attract substantial attention and investment. The market is experiencing significant growth due to the increasing popularity of eSports tournaments. ESports, which involves professional gamers competing in multiplayer video games for large audiences, is gaining traction worldwide. Countries such as the US, India, China, Sweden, and the UK host numerous eSports events, with organizations like the International eSports Federation and the World Esports Association playing a crucial role in their organization. As these tournaments require the use of gaming software, the market's revenue growth is directly linked to the frequency and participation in these events. Gaming software developers hold the intellectual property rights to the multiplayer games used in eSports, making it a lucrative business opportunity.

- Moreover, advancements in game analytics, asset management, AI scripting, user experience design, level design, level editor, and game mechanics are enhancing the overall gaming experience. App stores and game streaming platforms have made it easier for gamers to access a wide range of games, further fueling market growth. Quality assurance practices ensure the delivery of high-quality gaming software, maintaining customer satisfaction and loyalty.

How does Gaming Software market face challenges during its growth?

- A high capital requirement poses a significant challenge to the industry's growth trajectory. In order to expand and remain competitive, companies within this sector must secure substantial financial resources, which can be a major obstacle for smaller businesses and startups. This capital constraint can hinder innovation, limit market penetration, and ultimately impede industry progression. The market is experiencing significant growth due to the increasing demand for deep gaming experiences. Developers are investing heavily in research and development to deliver high-performing games, with a focus on advanced game design software, user interface design, and physics engines. This includes the use of tools like SpeedTree for realistic tree modeling and custom graphics creation for large-scale games. Game localization and testing are also crucial aspects, ensuring games are accessible to a global audience and free of bugs. Strategic games, augmented reality, and online gaming are popular genres driving market growth.

- Game narrative and marketing are essential elements in the competitive landscape, with companies investing in innovative storytelling and effective marketing strategies. The market dynamics necessitate a substantial investment in game development, with the cost of producing a game like Grand Theft Auto V reaching approximately USD 270 million.

Exclusive Customer Landscape

The gaming software market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gaming software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, gaming software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Activision Blizzard Inc. - This company specializes in advanced gaming software, enabling users to engage in multiplayer mode for various online games, including StarCraft, with unparalleled efficiency and performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Activision Blizzard Inc.

- Aristocrat Leisure Ltd.

- Bandai Namco Holdings Inc.

- Capcom Co. Ltd.

- Electronic Arts Inc.

- Epic Games Inc.

- Konami Group Corp.

- Krafton Inc.

- Microsoft Corp.

- Nintendo Co. Ltd.

- Playtika Holding Corp.

- Roblox Corp.

- Sega Sammy Holdings Inc.

- Sony Group Corp.

- Take Two Interactive Software Inc.

- Tencent Holdings Ltd.

- Ubisoft Entertainment SA

- Unity Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Gaming Software Market

- In February 2023, Unity Technologies, a leading gaming software development company, announced the launch of Unity WebGL 3, a significant upgrade to its web-based game engine, enabling developers to create high-performance, 3D and 2D games directly for the web without the need for plugins (Unity Technologies Press Release, 2023).

- In May 2024, Microsoft and Sony, major players in the gaming industry, revealed a strategic partnership to expand their gaming ecosystems, allowing Microsoft's Xbox Game Pass subscription service to be accessible on Sony's PlayStation consoles (Microsoft News Center, 2024).

- In October 2024, Epic Games, the creator of Fortnite, raised USD 2 billion in a funding round, bolstering its position as a dominant player in the market and fueling its ongoing efforts in metaverse development (Bloomberg, 2024).

- In January 2025, Apple announced the launch of its App Store for Macs, enabling developers to distribute gaming software directly to Mac users, expanding the reach of gaming software and potentially disrupting traditional distribution channels (Apple Newsroom, 2025).

Research Analyst Overview

The market continues to evolve, with dynamic market activities unfolding across various sectors. Asset management tools facilitate the efficient organization and maintenance of game data, while game analytics provide valuable insights into player behavior and market trends. AI scripting enhances game mechanics, enabling more sophisticated player interactions experiences. App stores serve as crucial distribution channels for mobile games, while game streaming platforms expand accessibility to a broader audience. Level design and level editor tools allow for the creation of engaging game environments, and user experience design ensures seamless gameplay and player satisfaction. Quality assurance processes ensure the delivery of high-quality games, while game localization and testing cater to diverse player communities.

Game design software, game distribution channels, and user interface design tools are essential for creating and delivering deep gaming experiences. Game narrative, strategy games, physics engines, and augmented reality technologies add depth and complexity to games. Online gaming, console games, and social gaming communities foster player engagement and interaction. Game monetization strategies, including in-app purchases and player engagement techniques, have become increasingly sophisticated. Game development tools, including version control systems, game engines, and audio middleware, enable the creation of high-quality games. Game design patterns and player engagement strategies continue to evolve, shaping the future of the gaming industry.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Gaming Software Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

243 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.4% |

|

Market growth 2025-2029 |

USD 56.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.0 |

|

Key countries |

China, US, Japan, India, Germany, South Korea, UK, Canada, Australia, and Russia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Gaming Software Market Research and Growth Report?

- CAGR of the Gaming Software industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the gaming software market growth of industry companies

We can help! Our analysts can customize this gaming software market research report to meet your requirements.

RIA -

RIA -