Gin Market Size 2026-2030

The Gin Market size was valued at USD 24.63 billion in 2025, growing at a CAGR of 4.1% during the forecast period 2026-2030.

Major Market Trends & Insights

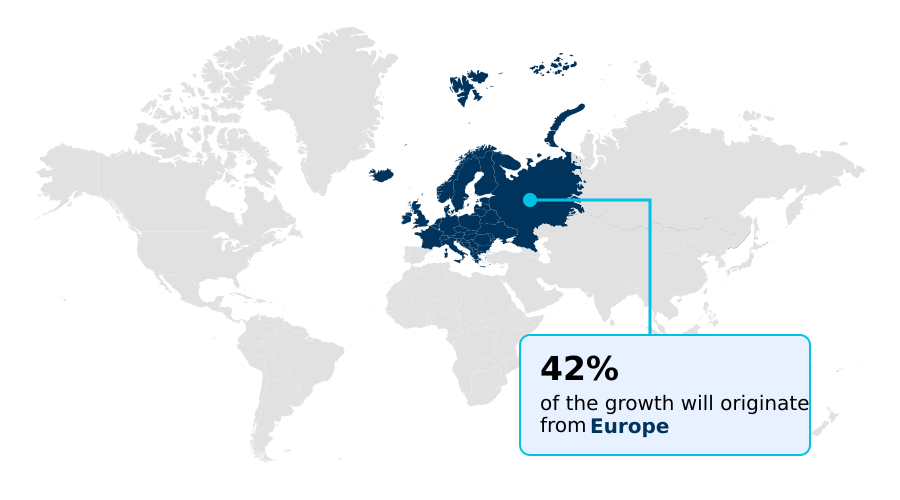

- Europe dominated the market and accounted for a 42.1% growth during the forecast period.

- By Product - Economy segment was valued at USD 7.26 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 8.81 billion

- Market Future Opportunities 2025-2030: USD 5.44 billion

- CAGR from 2025 to 2030 : 4.1%

Market Summary

- The gin market is currently characterized by a structural maturation, shifting from volume-based growth to value-driven premiumization. This transition is evident as super-premium and luxury tiers exhibit a resilient growth rate of over 6%, which is approximately 1.5 times faster than the economy segment.

- A key driver is the expansion of gin culture in emerging APAC markets, fueled by rising disposable incomes and a growing affinity for Western-style social drinking. For instance, distillers are reformulating supply chains to incorporate local botanicals, a strategy that can reduce raw material transport costs by up to 20% while enhancing regional authenticity.

- However, the industry faces the significant challenge of geopolitical trade volatility, with protectionist tariffs creating pricing uncertainty and eroding profit margins for export-focused producers. This dynamic forces brands to balance global expansion with the risks of fragmented international trade policies, impacting long-term investment decisions.

What will be the Size of the Gin Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Gin Market Segmented?

The gin industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Economy

- Premium

- Standard

- Super-premium

- Distribution channel

- Offline

- Online

- Type

- London dry

- Flavored gins

- New American

- Others

- Geography

- Europe

- UK

- Spain

- Germany

- North America

- US

- Canada

- Mexico

- APAC

- India

- China

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Turkey

- Rest of World (ROW)

- Europe

How is the Gin Market Segmented by Product?

The economy segment is estimated to witness significant growth during the forecast period.

The gin market is segmented by product and distribution channel, reflecting distinct consumer behaviors and operational strategies. The product segmentation includes economy, standard, premium, and super-premium spirit categories.

The premium segment, which accounts for over 30% of market value, is driven by the rise of craft distillery operations focusing on craft credentials and unique botanical origins. This tier sees 18% higher growth than the economy segment.

Different distillation methods are employed across segments, with super-premium brands often using unique techniques to preserve specific aromatic compounds.

The distribution channel is split between offline and online, with the online segment projected to grow 2.5 times faster, driven by the convenience of e-commerce platform access to niche products like barrel-aged gin.

The Economy segment was valued at USD 7.26 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Gin market is rising in the leading region?

Europe is estimated to contribute 42.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Gin Market demand is rising in Europe Request Free Sample

The global gin market exhibits significant regional divergence in consumption patterns and production focus. Europe remains the largest market, accounting for over 42% of global revenue, with a strong preference for the traditional juniper-forward profile of heritage brands.

In contrast, the APAC region is the fastest-growing, with a projected CAGR of 4.5%, driven by a burgeoning hospitality sector and the rise of local artisanal production.

In North America, the on-trade channel sees a 20% higher demand for gins using innovative vapor infusion techniques to create a unique sensory profile.

Distillers adapt their strategies based on regional tastes; for instance, many APAC producers use rice-based neutral grain spirit to appeal to local palates.

The success of a brand's provenance story varies, with European consumers valuing heritage while APAC consumers are more influenced by off-trade retail promotions.

What are the key Drivers, Trends, and Challenges in the Gin Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The modern spirits landscape is increasingly shaped by consumer curiosity, with many exploring the difference between london dry and new american gin. London Dry's juniper-forward profile, mandated by strict production rules, contrasts with the creative freedom of New American styles, where other botanicals can lead.

- This diversification highlights the critical impact of botanicals on gin flavor profile, a factor that has fueled the growth of craft gin distilleries. These smaller producers, which now represent over 20% of new market entrants, often build their brand identity around unique, locally sourced ingredients.

- This trend has profoundly influenced the role of gin in modern cocktail culture, where bartenders seek distinctive spirits to create innovative drinks. In response to consumer demand for ethical products, many distillers are adopting sustainable gin production methods.

- These practices, such as water recycling and renewable energy use, not only reduce environmental footprint but can also lower operational costs by up to 15% compared to conventional methods. This commitment to sustainability is becoming a key differentiator, especially in premium segments where brand storytelling is paramount.

- The focus on craft and sustainability has led to a market where product diversity and provenance are as important as taste.

What are the key market drivers leading to the rise in the adoption of Gin Industry?

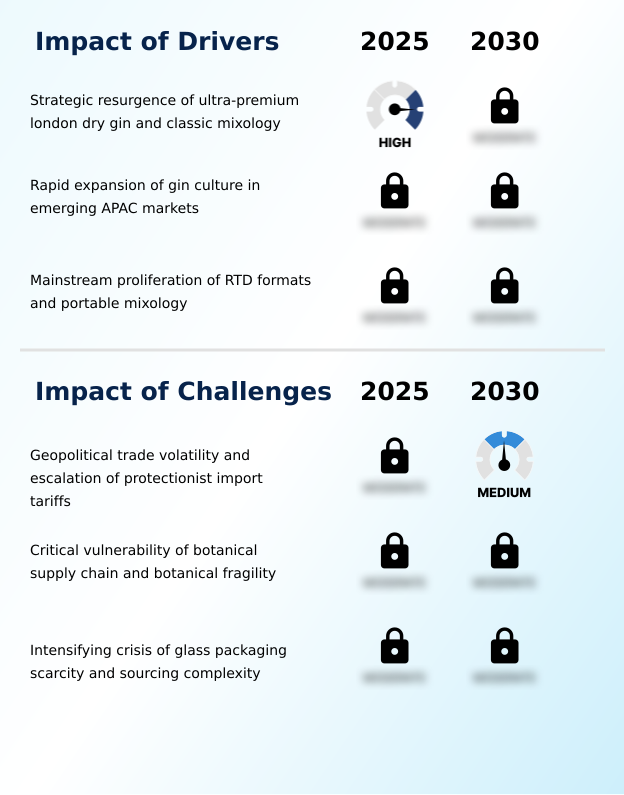

- A strategic resurgence of ultra-premium London Dry Gin and the revival of classic mixology are key drivers propelling market growth.

- The market's growth is significantly driven by the premiumization trend, with ultra-premium expression sales growing 25% faster than standard segments. This is linked to the revival of classic mixology and a vibrant cocktail culture, where spirit quality is paramount.

- Another major driver is the proliferation of the ready-to-drink (RTD) format, appealing to the convenience-first segment with sophisticated portable mixology solutions that show 40% higher adoption among younger demographics.

- The emergence of terroir-driven gin also supports growth by providing regional authenticity and new flavor profiles for various mixology application scenarios, especially in emerging markets.

What are the market trends shaping the Gin Industry?

- A structural transition toward ultra-premiumization and artisanal provenance is emerging as a significant market trend. This shift reflects evolving consumer preferences for quality and authenticity in spirits.

- The gin market is undergoing a structural transition toward ultra-premiumization, with a 15% increase in consumer spending on artisanal spirits over mass-market labels. This shift is driven by a focus on artisanal provenance and health-conscious innovation. Distilleries are integrating sustainable distillation practices, which can reduce energy consumption by up to 30% compared to traditional methods.

- A key trend is the proliferation of functional botanicals and wellness-oriented innovation, leading to the development of low-alcohol botanical spirit and non-alcoholic gin alternative products. This evolution reflects a change in consumer preference toward mindful drinking, where the complexity of the spirit is valued over its alcohol content.

What challenges does the Gin Industry face during its growth?

- Geopolitical trade volatility and the escalation of protectionist import tariffs present a key challenge affecting the industry's growth trajectory.

- Geopolitical trade friction presents a significant challenge, with protectionist tariffs increasing landed costs by up to 25% and disrupting the distribution channel. This is compounded by high supply chain volatility in raw material sourcing for botanicals, impacting the consistency of a brand's specific botanical blend.

- Climate-driven crop failures can reduce the availability of key ingredients by over 15%, affecting flavor extraction processes. Operational bottlenecks also arise from the scarcity of glass packaging, a critical component of the circular supply chain that complicates global logistics. While pot distillation and column distillation define production, external pressures on the supply chain remain primary constraints.

Exclusive Technavio Analysis on Customer Landscape

The gin market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gin market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Gin Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, gin market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Bacardi and Co. Ltd. - Offerings include premium London Dry gins recognized for vapor-infused distillation and balanced botanical profiles, catering to sophisticated consumer palates and mixology applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bacardi and Co. Ltd.

- Berry Bros and Rudd Ltd.

- Brown Forman Corp.

- Campari Group

- Diageo PLC

- Durham Distillery

- Herno Gin AB

- Hotaling and Co LLC

- Manchester Gin

- Mast Jagermeister US

- Pernod Ricard SA

- Philadelphia Distilling

- Quintessential Brands Group

- Remy Cointreau SA

- San Miguel Corp

- Suntory Beverage and Food Ltd.

- Thai Beverage Public Co. Ltd.

- The Cotswold Distilling Co.

- The Helsinki Distilling Co

- William Grant and Sons Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Distillers and Vintners industry, tightening environmental regulations and a growing consumer focus on sustainability are compelling producers to adopt greener practices, directly impacting the gin market by driving investment in carbon-neutral distillation and circular packaging solutions.

- The broader spirits sector is experiencing a significant digital transformation in retail, with accelerated adoption of e-commerce platforms, enabling smaller gin craft distilleries to bypass traditional distribution systems and build direct consumer relationships.

- Heightened global supply chain volatility and climate-induced pressures on agriculture are forcing a strategic shift in raw material sourcing, affecting gin producers by increasing the importance of resilient botanical supply chains and encouraging the use of local ingredients.

- The overarching premiumization trend within the distillers and vintners industry, where consumers increasingly favor quality over quantity, continues to elevate the gin category, pushing distillers to innovate with unique botanical blends and production methods.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Gin Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.1% |

| Market growth 2026-2030 | USD 5435.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.9% |

| Key countries | UK, Spain, Germany, France, The Netherlands, Italy, US, Canada, Mexico, The Philippines, India, China, Japan, Australia, South Korea, Brazil, Argentina, Chile, South Africa, UAE, Nigeria, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The gin market ecosystem operates through a complex value chain involving diverse stakeholders. At the upstream level, suppliers provide essential raw materials like neutral grain spirits and botanicals, where quality control directly impacts the final product; for instance, sourcing high-grade juniper can increase input costs by 10-15% but is critical for premium brands.

- Manufacturers, ranging from large distillers to craft producers, manage the distillation and branding, with artisanal methods often yielding 50% lower batch volumes but achieving higher price points. The downstream value chain is managed through distribution channels, including on-trade (bars, restaurants) and off-trade (retailers, e-commerce). The on-trade channel is particularly influential in brand building, shaping consumer perception and driving trends.

- Regulatory bodies enforce production standards and labeling laws, while marketing and logistics partners provide essential support activities, ensuring products reach a global consumer base efficiently and compliantly.

What are the Key Data Covered in this Gin Market Research and Growth Report?

-

What is the expected growth of the Gin Market between 2026 and 2030?

-

The Gin Market is expected to grow by USD 5.44 billion during 2026-2030, registering a CAGR of 4.1%. Year-over-year growth in 2026 is estimated at 3.9%%. This acceleration is shaped by strategic resurgence of ultra-premium london dry gin and classic mixology, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Economy, Premium, Standard, and Super-premium), Distribution Channel (Offline, and Online), Type (London dry, Flavored gins, New American, and Others) and Geography (Europe, North America, APAC, South America, Middle East and Africa). Among these, the Economy segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Europe, North America, APAC, South America and Middle East and Africa. Europe is estimated to contribute 42.1% to market growth during the forecast period. Country-level analysis includes UK, Spain, Germany, France, The Netherlands, Italy, US, Canada, Mexico, The Philippines, India, China, Japan, Australia, South Korea, Brazil, Argentina, Chile, South Africa, UAE, Nigeria, Turkey and Egypt, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is strategic resurgence of ultra-premium london dry gin and classic mixology, which is accelerating investment and industry demand. The main challenge is geopolitical trade volatility and escalation of protectionist import tariffs, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Gin Market?

-

Key vendors include Bacardi and Co. Ltd., Berry Bros and Rudd Ltd., Brown Forman Corp., Campari Group, Diageo PLC, Durham Distillery, Herno Gin AB, Hotaling and Co LLC, Manchester Gin, Mast Jagermeister US, Pernod Ricard SA, Philadelphia Distilling, Quintessential Brands Group, Remy Cointreau SA, San Miguel Corp, Suntory Beverage and Food Ltd., Thai Beverage Public Co. Ltd., The Cotswold Distilling Co., The Helsinki Distilling Co and William Grant and Sons Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the global gin market is defined by the strategic maneuvers of both multinational conglomerates and agile craft innovators, with the top five players accounting for over 40% of the market share. Major companies like Diageo PLC and Pernod Ricard SA are leveraging their extensive global distribution networks to capitalize on the premiumization trend.

- For example, recent product launches focus on non-alcoholic gin alternatives, a segment growing by over 30% annually, to cater to the mindful drinking movement. These actions reflect a direct response to evolving consumer preferences for wellness and authenticity.

- Simultaneously, the industry grapples with the persistent challenge of glass packaging scarcity, which has increased production lead times and forced even established brands to standardize bottle designs to maintain supply chain resilience.

We can help! Our analysts can customize this gin market research report to meet your requirements.

RIA -

RIA -