Enjoy complimentary customisation on priority with our Enterprise License!

The 3D printing market in healthcare industry size is estimated to grow by USD 3.43 billion at a CAGR of 18.12% between 2022 and 2027. The increased demand for personalized or customized medical devices, driven by factors such as the need for patient-specific solutions and the advancements in medical imaging technologies, is a significant driver. The adoption of 3D printing technology by medical professionals is also increasing, thanks to its ability to create complex structures and improve patient outcomes. Additionally, the cost efficiency and productivity gains offered by 3D printing are making it an attractive option for medical device manufacturing.

It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

To learn more about this report, View Report Sample

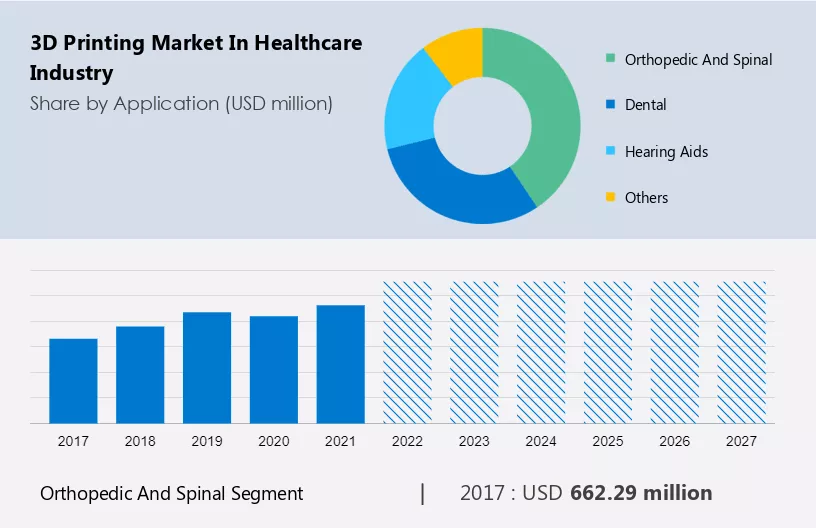

This market report extensively covers market segmentation by application (orthopedic and spinal, dental, hearing aids, and others), technology (stereolithography, granular materials binding, and others), and geography (North America, Europe, Asia, and the Rest of the World (ROW)).

The market share growth by the orthopedic and spinal segment will be significant during the forecast period. 3D printing is used for the fabrication of standard-sized orthopedic implants, patient-matched implants for individuals who have typical bone and joint anatomy, and custom implants for individuals that have bone or joint deformities. Many end-users, such as hospitals and ambulatory surgery centers, are increasingly adopting 3D printing to fabricate orthopedic implants. They can manufacture complex structures that cannot be produced using conventional production methods and create devices that are individually matched to a patient's anatomy.

Get a glance at the market contribution of various segments View the PDF Sample

The orthopedic and spinal segment was valued at USD 662.29 million in 2017. 3D-printed orthopedic implants are often made of titanium. This technique allows for greater implant porosity than when using traditional manufacturing techniques. Greater porosity may promote bone ingrowth and improve implant stability. They also enable implant developers to enhance the design of spinal implants. This technology enables the development of interbody fusion devices using proven biocompatible and osteoconductive materials.

Moreover, this technology is also used in the fabrication of prosthetic limbs. The technology significantly speeds up the manufacturing process of prosthetic limbs. It also significantly reduces manufacturing costs while offering the same functionality as that of traditionally manufactured prosthetics. The low cost of these products makes them particularly suitable for children, who quickly outgrow their prosthetic limbs. Such factors will increase segment growth during the forecast period.

For more insights on the market share of various regions Download PDF Sample now!

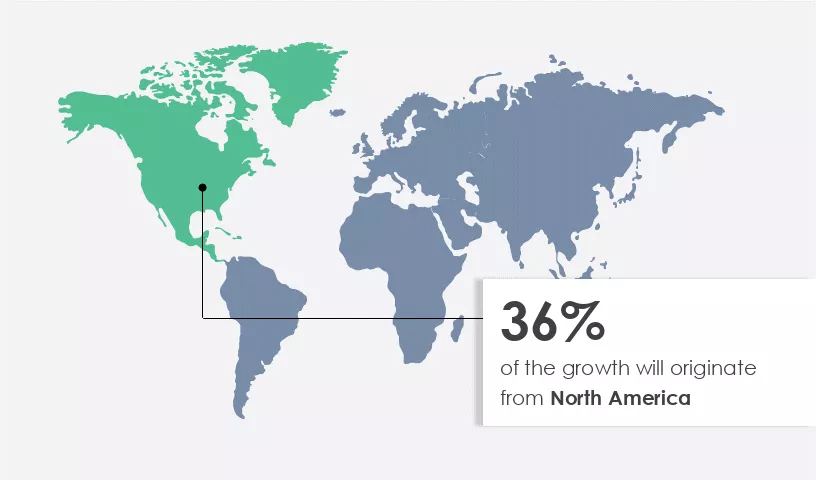

North America is estimated to contribute 36% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. A rapidly aging population and growing need for advanced healthcare services are also increasing the demand for 3D printed healthcare products. The 65-year-old population in Canada will exceed 7 million in 2022. Customers in the region have access to technologically advanced healthcare services due to the increasing disposable income of the population. 3D printed healthcare products have direct and indirect costs that increase healthcare spending. Favorable government support, the presence of local suppliers, and the increasing number of companies in the region developing these products are expected to drive market growth in North America.

3D printing in the healthcare industry, also known as additive manufacturing, enables the creation of customized medical devices and personalized healthcare facilities. This technology utilizes 3D advanced technology to produce patient-specific implants and equipment with high production accuracy. Surgeons, dentists, mechanical engineers, and biomedical engineers, among others, benefit from technological developments in this field. With public-private funding supporting research, additive manufacturing has transformed healthcare by offering personalized medical care and solutions for reconstructive surgeries. However, challenges such as operative risks and infections due to anesthesia exposure must be addressed to ensure the technology's safe and effective use in healthcare. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Increased demand for personalized or customized medical devices is the key factor driving the growth of the market. Personalization by printing patient-specific anatomical models and synthetic organs to illustrate health conditions and treatment plans to help patients understand surgical procedures. Individualized surgical instruments such as clamps, hemostats, and forceps can make surgery less painful and deliver better results. Surgical instruments made from biocompatible materials such as thermoplastics and metals and made with 3D printing technology can achieve higher precision and lower costs. The use of 3D-printed implants can significantly reduce the cosmetic deformities associated with such surgeries. These advancements are part of a broader trend towards customized medical devices and personalized healthcare facilities, driven by 3D advanced technology and supported by public-private funding. These technological developments enable the production of patient-specific implants with increased production accuracy.

3D printing is increasingly used in the construction of custom joint prostheses. In addition to enhanced patient comfort, 3D printing can be used to develop customized prosthetics that suit and fit the wearer. The low cost of these products makes them particularly suitable for children, who quickly outgrow their prosthetic limbs. Nearly 99% of the hearing aids that fit into the ear are custom-made using 3D printing. The technology allows customization of the hearing aids as per the unique anatomy of the patient's ear canal while being cost-effective and efficient. Such factors will increase the market growth during the forecast period.

Strategic collaborations and M&A is the primary trend in the market The market in the healthcare industry is seeing an increase in strategic collaborations. Various research centers are looking to develop new technologies and expand the scope of application of the technology. For instance, in April 2021, Ralph H. Johnson VA Medical Center based in Charleston, applied for US FDA approval for its 3D-printed hearing aids. The market is also recording an increasing trend in M&A.

In March 2021, 3D Systems announced the collaboration with Huntington Ingalls Industries' Newport News Shipbuilding division to develop Copper-Nickel (CuNi) and Nickel-Copper (NiCu) alloys for powder bed fusion additive manufacturing. Such factors are expected to fuel the growth of the market during the forecast period.

The high initial setup cost of 3D printing facilities are major challenge to the growth of the market. The high capital cost of 3D-printed healthcare products has limited their widespread adoption. The high cost is primarily due to the equipment required for 3D printing or outsourced print service contracts and sophisticated software for post-processing. The cost of a desktop FDM or SLA machine is typically between USD 3,000 and USD 15,000. However, the higher-end additive manufacturing printers (SLS, material jetting, and metal printing) range from USD200,000 to USD850,000 and sometimes even several millions of dollars. Another source of high costs of printing is the proprietary raw materials that 3D printer manufacturers sell at high profit margins. Furthermore, end-users must make significant investments in training or hiring skilled personnel to ensure the production of high-quality devices.

A clinical 3D printing laboratory requires trained ancillary staff to carry out the actual printing of the model. The time required to produce most 3D printers, while dependent on the number of layers to be printed, typically ranges from hours to days. This limits the viability of mass manufacturing in certain areas unless several hundred 3D printers are purchased and operated simultaneously. Such factors are expected to hinder the growth of the market during the forecast period.

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

3D Systems Corp.: The company offers SLA 750 3D printer model, which is designed and used to create concept models, cosmetic prototypes, and complex parts with intricate geometries.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

The market is evolving rapidly, with significant contributions from the academic and industrial level and the additive manufacturing community. This technology offers biocompatible solutions for biomedical applications, including bioprinting tissues & organs, revolutionizing healthcare industries. Customization & personalization are key drivers, enabling the production of customized medical equipment and products. Despite regulatory hurdles and reimbursement challenges, the market continues to grow, driven by technological advancements and strategic decisions. The Competitive outlook remains strong, supported by skilled professionals such as anatomists, prosthetists, and software engineers, ensuring safety assessments and value chain optimization.

The market is marked by additive processes that enable innovative solutions with biocompatibility for various medical applications. Clinical trials are exploring the potential of this technology, while copyright & patent concerns remain relevant. A diverse customer base and geographic expansions indicate growing acceptance and adoption. The use of 3D printing in healthcare infrastructure is enhancing nasal medication delivery and improving radiographic and clinical outcomes. Regulatory guidelines and trade regulations influence the market, but the rise in pharmaceutical applications and the use of pure titanium and titanium alloy drive technological innovations and projections for the future. Skilled labor and the exchange of knowledge through platforms like the Springer Journal contribute to the industry's growth and advancement.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.12% |

|

Market growth 2023-2027 |

USD 3.43 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

17.35 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 36% |

|

Key countries |

US, Germany, France, China, and Japan |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

3D Systems Corp., Allevi Inc., Anatomics Pty Ltd., Dentsply Sirona Inc., Desktop Metal Inc., EOS GmbH, Formlabs Inc., General Electric Co., Groupe Gorge SA, INTAMSYS TECHNOLOGY CO. LTD., Materialise NV, Mecuris GmbH, Organovo Holdings Inc., Proto Labs Inc., Rapid Shape GmbH, Renishaw Plc, Roland DG Corp., SLM Solutions Group AG, Stratasys Ltd., and Ultimaker BV |

|

Market dynamics |

Parent market analysis, Market Forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period. |

|

Customization purview |

If our market forecast report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Technology

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights