Enjoy complimentary customisation on priority with our Enterprise License!

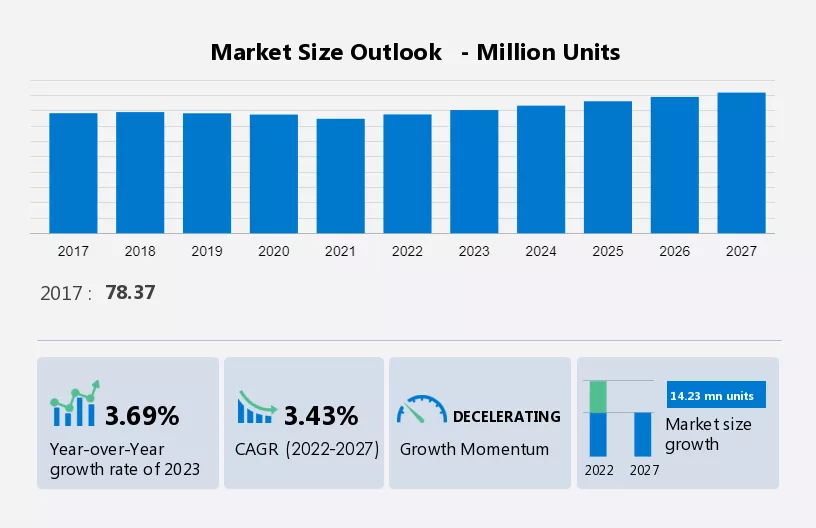

The automotive engine market is estimated to grow by 14.23 million units declining at a CAGR of 3.43% between 2022 and 2027. The market experiences growth driven by the high volume growth in the premium vehicle segment. There is a growing demand to enhance vehicle performance, prompting advancements in engine technologies. Additionally, the increasing vehicle population worldwide contributes to market expansion as consumers seek efficient and reliable engines to meet their transportation needs.

To learn more about this report, Download Report Sample

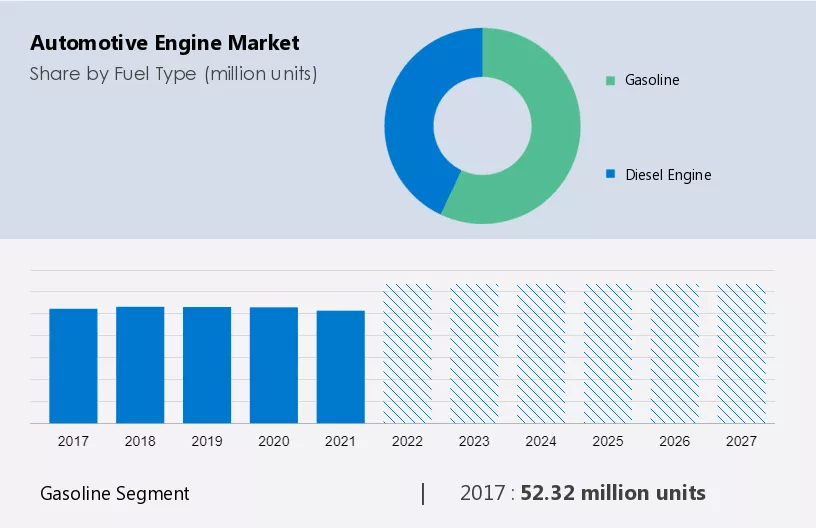

This report extensively covers market segmentation by fuel type (gasoline and diesel engine), type (in-line engine, v-type engine, and flat engine), and geography (APAC, North America, Europe, South America, and Middle East and Africa).

The market share growth by the gasoline segment will be significant during the forecast period. Gasoline-powered engines are common in passenger cars as they emit lower pollutants, create less vibration and noise, and are lightweight. Another major factor propelling demand for gasoline engines is engine downsizing, which makes the size of a gasoline engine smaller than a diesel engine. In addition, diesel-powered cars are more expensive than gasoline-powered passenger cars, and with the reduced price gap between diesel and gasoline in booming automotive markets such as India and China, the growth of diesel engines has got curtailed.

Get a glance at the market contribution of various segments Request a PDF Sample

The gasoline segment was valued at 52.32 million units in 2017 and continue to grow by 2021. Gasoline engines dominate the passenger cars segment across the three geographies. This is because, for a given displacement and engine weight, petrol engines produce greater horsepower through lower torque at a higher RPM than a corresponding diesel engine. In addition, a gasoline engine is also cost-effective to manufacture compared to a similar-sized diesel engine. Moreover, the demand for global passenger cars has been growing significantly, which will drive the market in focus during the forecast period.

For more insights on the market share of various regions Request PDF Sample now!

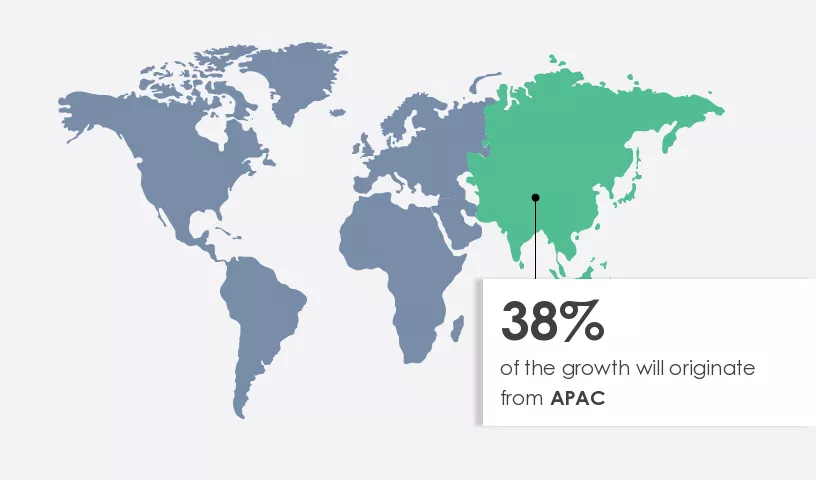

APAC is estimated to contribute 38% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. In terms of production volume, China and India account for the largest share of the market in APAC due to the presence of a large automotive production base. The reduction in the prices of components and the availability of more stable and advanced systems are expected to attract low-cost manufacturers to enter the market in APAC, especially in China, during the forecast period.

The market witnesses robust growth driven by the production of automobiles worldwide. Consumers' desire for high-performance and fuel-efficient engines fuels rising sales of both passenger and commercial vehicles, particularly in developing countries. Stringent regulatory requirements for fuel economy push manufacturers towards technologically sophisticated engines. Intensive research by leading OEMs and automakers drives innovation, although challenges such as the lack of semiconductors persist. Post-pandemic, the automotive sector seeks recovery through cutting-edge technologies like engine control unit repair. New engine technologies such as VDEs, hydrogen, and hybrids offer excellent speed and fuel efficiency, catering to consumer preferences and addressing emissions levels, especially in smaller, compact cars.

The high growth volume for the premium vehicle segment is notably driving the market growth, although factors such as the increasing popularity of electric vehicles may impede the market growth. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The increased volume of premium vehicle sales serves as a primary catalyst for market expansion. Anticipated growth in the sales of performance, premium, and sport utility vehicles reflects evolving consumer preferences. Over the next decade, market design trends will pivot towards prioritizing high-quality and comfortable vehicles, aligning with consumer desires. The sustained surge in demand for SUVs, witnessed over the past four years, is forecasted to persist. Moreover, burgeoning markets like China and India witness a surge in the demand for luxury vehicles, driven by stable economic conditions and growing disposable incomes. This escalating adoption of luxury cars is poised to drive market growth in the forecast period.

The increasing demand for fuel efficiency is one of the primary market trends. The automotive industry is witnessing a growing demand for fuel efficiency, safety, and emission reduction to promote a better driving and travel experience for consumers. This increases the efficiency of car engines, which helps reduce fuel costs.

Moreover, automotive OEMs prefer efficient automotive engine suppliers due to their demands for high performance and low fuel consumption. Therefore, the demand for efficient vehicles drives the demand for automotive engines, which can increase the efficiency of vehicles and in turn drive the market during the forecast period

The increasing popularity of electric vehicles is a major challenge to the global market growth. The increasing emphasis on using sustainable energy and using environmentally friendly means to limit carbon dioxide emissions has increased the demand for electric cars. Government subsidies, lower prices for battery electric vehicles (BEVs), and the adoption of cost-effective electric vehicles are the main factors that have increased the demand for electric vehicles in several countries. The rapid expansion of electric car charging infrastructure, increasing consumer awareness and total or partial bans on the use of fuel-engine vehicles are also increasing the demand for electric cars worldwide.

Although the sales of EVs in 2020 were less than that of conventional fuel-based vehicles, the demand for EVs is expected to increase due to the presence of government policies supporting the use of energy-efficient vehicles. As EVs do not require any engine valves, an increase in the demand for such vehicles will negatively impact the demand for automotive engines during the forecast period.

The market growth analysis report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market research and growth report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Volvogroup - The company offers automotive engines such as the Volvo D11 engine, Volvo D13TC engine, and X15 engine.

The market growth and forecasting report also includes detailed analyses of the competitive landscape of the market and information about 15 market Companies, including:

Qualitative and quantitative analysis of Companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize Companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize Companies as dominant, leading, strong, tentative, and weak.

The market witnesses robust growth driven by the increasing production of automobiles and consumer desire for high-performance engines. Rising sales of passenger and commercial vehicles, particularly in developing countries, propel market demand. Stringent regulatory requirements for fuel economy further fuel the demand for technologically sophisticated engines. Consumers prefer high-performance and fuel-efficient cars, leading to intensive research from leading OEMs and automakers. However, challenges such as the lack of semiconductors and post-pandemic disruptions persist. Advanced engine technologies like VDEs, hydrogen, and hybrids cater to the need for improved performance and greater fuel economy, while stricter emissions regulations drive the creation of pollution-free engines. Market participants focus on engine control systems to meet legislative requirements and address environmental concerns, contributing to the growth of the market.

The desire for automotive engines with extended lifespans aligns with the rising demand for luxury vehicles. As emissions regulations tighten, particularly for smaller cars, legislative organizations impose stringent standards to curb greenhouse gas emissions and combat environmental air pollution. Concerns over harmful automobile emissions, including carbon monoxide pollution, drive the adoption of Engine Management Systems (EMS) for effective fuel flow regulation. Taxation changes and the production of diesel cars prompt a shift towards electric buses and alternative fuel vehicles like Battery Electric Vehicles (BEVs) and Fuel Cell Electric Vehicles (FCEVs). Engine control unit replacement supports the transition to lighter, fuel-efficient cars, catering to market demands for high-performance vehicles in both in-line and W-engine market categories.

The market research report forecasts market decline by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Automotive Engine Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

178 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Decelerate at a CAGR of 3.43% |

|

Market growth 2023-2027 |

14.23 million units |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

3.69 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 38% |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AB Volvo, BMW AG, Cummins Inc., Dr. Ing. h.c. F. Porsche AG, Eicher Motors Ltd., Ford Motor Co., General Motors Co, Honda Motor Co. Ltd, Hyundai Motor Co., MAHLE GmbH, Maruti Suzuki India Ltd., Mazda Motor Corp., Mercedes Benz Group AG, Mitsubishi Motors Corp., Renault SAS, Stellantis NV, Toyota Motor Corp., Trelleborg AB, and Yamaha Motor Co. Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period. |

|

Customization purview |

If our market forecasting report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Fuel Type

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.