Enjoy complimentary customisation on priority with our Enterprise License!

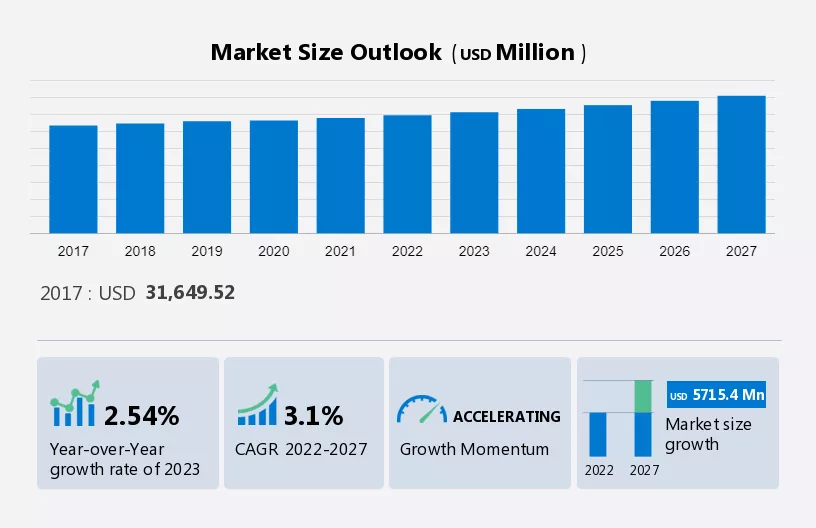

The beverage can market size is forecast to increase by USD 5.72 billion at a CAGR of 3.1% between 2022 and 2027. Market expansion is influenced by several pivotal factors. One such factor is the escalating demand for metal cans, driven by various industries' reliance on durable and versatile packaging solutions. Particularly noteworthy is the rising prominence of the energy and juice drinks market, where metal cans are preferred for their ability to preserve freshness and enhance shelf life. Additionally, the market's growth trajectory is further propelled by the increasing consumer awareness surrounding sustainability. This awareness has led to a preference for eco-friendly packaging options like metal cans, which are recyclable and contribute to reducing environmental impact. The convergence of these factors underscores a significant shift in consumer preferences and industry practices towards sustainable packaging solutions in the beverages sector.

To learn more about this report, Download Report Sample

This report extensively covers market segmentation by application (non-alcoholic beverages and alcoholic beverages), material (aluminum and steel), and geography (North America, APAC, Europe, Middle East and Africa, and South America). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

The market encompasses various types of beverages, including carbonated soft drinks, beer, and cider. Manufacturers continue to explore alternative packaging solutions, such as metal and aluminum cans, to reduce the carbon footprint associated with transportation and refrigeration. Labeling, printing, and design innovations are crucial in this market, ensuring that beverages stand out on retail shelves. Plastic products, such as PET and polyester bottles, remain popular due to their lightweight and recyclability. However, concerns regarding the use of raw materials and the recycling rate have led to increased interest in more sustainable options. Sterilization is another critical factor in the market, ensuring that beverages remain safe for consumption. Innovations in can manufacturing, such as the use of steel and aluminum, have led to significant reductions in greenhouse gas (GHG) emissions compared to glass bottles and plastic bottles. The recyclability of aluminum cans, for instance, makes them an attractive alternative for retail operations and consumers alike. Overall, the market continues to evolve, with a focus on sustainability, innovation, and consumer convenience. Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market growth is being notably propelled by the increased need for metal cans. Metal packaging, particularly aluminum and steel, offers advantages such as superior hermetic seals, resistance to breakage during transit, and stability in fast-processing environments and varying temperatures. Labeling, printing, and design innovations further enhance the appeal of metal cans for manufacturers. Natural resources, including metal recycling, play a crucial role in reducing the carbon footprint of the industry. The European Commission, RUSAL, ELVAL, and the International Aluminium Institute are key players in this market.

Moreover, metal cans have a higher volume share compared to glass bottles and plastic bottles in the global market. The recyclability of metal cans, which can be recycled infinitely without loss of quality, is a significant advantage over plastic products. However, the raw material sterilization process and structure and integrity maintenance are essential considerations. Hence, such factors are driving market growth during the forecast period.

The growing market of RTD coffee and tea is an emerging trend in the market. Driven by increasing health awareness and disposable income, RTD tea and coffee have gained popularity, particularly among millennials. Metal, specifically aluminum and steel, is a key material in beverage can manufacturing. Labeling, printing, and design innovations are essential for brand differentiation. Manufacturers strive for sustainable solutions, such as metal recycling, which is supported by the European Commission.

Moreover, the global market utilizes natural resources, with metal recycling reducing greenhouse gas emissions (GHGs) and carbon footprint. RUSAL and ELVAL are significant aluminum producers. Recyclability, including PET and polyester, is a critical consideration in the industry's structure and integrity. The International Aluminium Institute and the International Aluminum Association promote recycling rates and sustainable practices. Hence, the rising demand for RTD coffee and tea is expected to fuel the global market during the forecast period.

The rising popularity of alternatives is a major challenge impeding the market growth. The market, primarily comprised of carbonated soft drinks, beer, cider, and other beverages like cold coffee, fruit juices, frappes, and iced teas, is predominantly reliant on metal, specifically aluminum and steel, for its production. The global market for beverage cans is influenced by various factors, including labeling, printing, design innovations, and the decisions of key manufacturers.

Moreover, the price of steel, a significant raw material, is anticipated to rise due to China's reduction in steel production by 15.18% in September 2022 compared to the previous year. This increase is expected to continue during the forecast period. As an alternative to metal packaging, plastic products have emerged, but metal cans offer advantages such as structure and integrity, sterilization, and recyclability. Hence, as the popularity of alternatives such as PET rises, the demand for metal cans will decrease, which will hinder the growth of the global market during the forecast period.

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

CANPACK SA - The company offers different types of beverage cans, metal closures, and others. The key offerings of the company include beverage cans.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

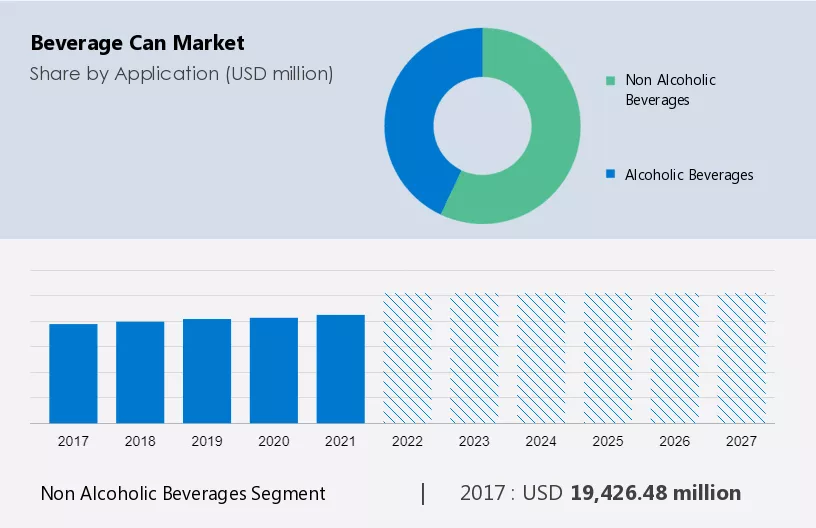

The market share growth by the non-alcoholic beverages segment will be significant during the forecast period. The global market encompasses various non-alcoholic beverages, including carbonated soft drinks (CSDs), energy drinks, juices, beer, cider, and alternative packaging solutions for cold coffee, fruit juices, frappes, iced teas, flavored sodas, and more. Metal cans, primarily made of aluminum and steel, dominate the market due to their hermetic seal and barrier against oxygen and sunlight. In 2022, Europe, particularly the UK, showed a preference for canned beverages due to taste and convenience.

Get a glance at the market contribution of various segments Request a PDF Sample

The non-alcoholic beverages segment was valued at USD 19.42 billion in 2017 and continued to grow until 2021. Drivers for market growth include rising global temperatures and disposable income, while challenges include health concerns over artificially sweetened beverages. Manufacturers are addressing this by introducing low-sugar or sugar-free options. The market structure includes raw material suppliers like RUSAL and ELVAL, labeling, printing, and design innovators, and manufacturers. Therefore, the abovementioned factors will drive segment growth during the forecast period.

For more insights on the market share of various regions Request PDF Sample now!

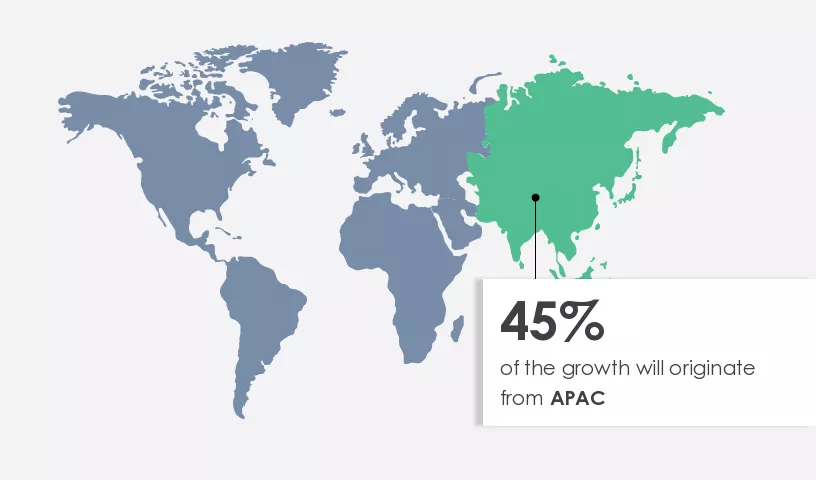

APAC is estimated to contribute 45% to the growth of the global market during the forecast period. Another region offering significant growth opportunities to companies is North America. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The demand for the packaging of processed and ready-to-eat (RTE) food products, fruit juices, aerated drinks, and energy drinks is mounting in North America and is expected to boost the market in upcoming years. The market in North America is anticipated to experience significant growth due to increasing demand for packaging RTE food products, fruit juices, aerated drinks, energy drinks, and aluminum beverage cans. Retail operations benefit from the convenience and ease of transportation offered by lightweight, 100% recyclable aluminum cans.

Moreover, the metal recycling market plays a crucial role in reducing environmental concerns, as aluminum cans are environmentally friendly and energy efficient. Raw material producers and packaging manufacturers are investing in research and development to enhance the performance of aluminum cans, offering energy drinks, dietary supplements, and other beverages to young adults and the younger generation. However, competition from alternative packaging options, such as cartons, may impact market growth. Assumptions regarding raw material costs and consumer preferences for organic options, real coffee beans, and specific caffeine content will influence product lines in health sections. These factors will boost the regional market growth during the forecast period.

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2023 to 2027, as well as historical data from 2017 to 2021 for the following segments.

In the market, aluminum cans have emerged as a popular choice for consumers due to their numerous benefits. Drinks produced in these containers, such as soda, water, and beer, offer extended shelf life and enhanced protection against light and oxygen. The use of these containers is also eco-friendly as they are recyclable and lightweight, making transportation and distribution more efficient. Furthermore, the production process for aluminum cans is cost-effective and energy-efficient, contributing to the overall profitability of beverage companies. The global aluminum market is expected to grow significantly in the coming years, driven by increasing consumer preference for convenient, portable, and sustainable packaging solutions. The market is further fueled by advancements in technology, which enable the production of innovative designs and shapes for these containers. Overall, the aluminum market is a dynamic and evolving industry that continues to shape the way we consume and enjoy beverages.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.1% |

|

Market growth 2023-2027 |

USD 5.72 billion |

|

YoY growth 2022-2023(%) |

2.54 |

|

Regional analysis |

North America, APAC, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 45% |

|

Key countries |

US, China, India, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Amcor Plc, Ardagh Group SA, Ball Corp., BangkokCan Manufacturing Co. Ltd., Can One Berhad, CANPACK SA, CPMC Holdings Ltd., Crown Holdings Inc., Envases Ohringen GmbH, GZ Industries Ltd., Kian Joo Can Factory Bhd, Mahmood Saeed Co. Ltd., Mitsubishi Materials Corp., Nampak Ltd., ORG Technology Co. Ltd., Orora Ltd., Shengxing Group, Silgan Holdings Inc., Toyo Seikan Group Holdings Ltd., and Trivium Packaging B.V |

|

Market dynamics |

Parent market analysis, market growth analysis, Market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Material

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.