Enjoy complimentary customisation on priority with our Enterprise License!

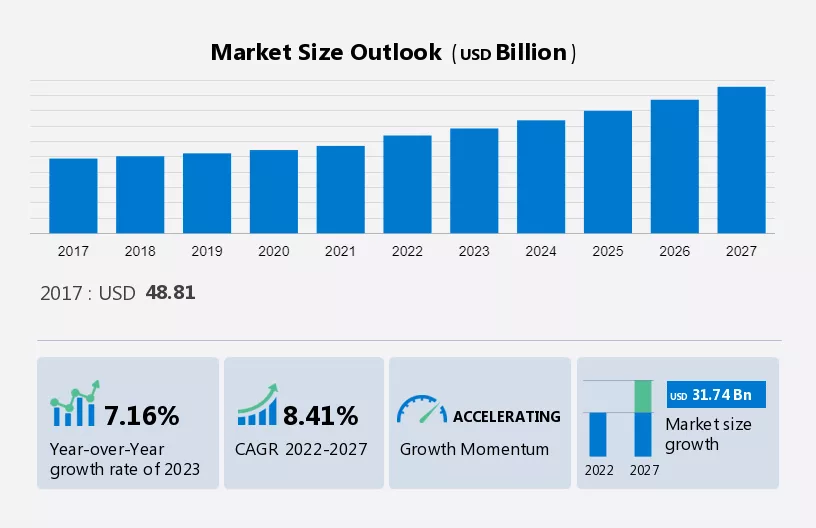

The Alcoholic Beverage Packaging Market size is estimated to grow by USD 31.74 billion between 2022 and 2027 and the size of the market is forecast to increase at a CAGR of 8.41%. Market expansion hinges on various factors, notably the escalating consumption of alcohol, a trend fueling demand for metal cans within the craft beer sector. Additionally, the widespread adoption of PET packaging in the alcoholic beverage industry contributes significantly to market growth. This surge in demand for metal cans and PET packaging reflects evolving consumer preferences and the industry's shift toward more sustainable and convenient packaging solutions. The rising popularity of craft beers, coupled with the convenience and recyclability of metal cans and PET packaging, continues to drive market expansion. These trends underscore the importance of innovative packaging solutions in meeting consumer demands and fostering sustainability in the alcoholic beverage market.

To learn more about this report, Download Sample Report

This market research report extensively covers market segmentation by material (glass, metal, and others), application (beer, wine, and spirits), and geography (Europe, APAC, North America, South America, and Middle East and Africa). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

The market encompasses a wide array of packaging formats catering to various alcoholic beverages like beer, wine, spirits, and whiskey. This market is characterized by the use of different materials such as glass, metal, and plastics, with a notable trend towards eco-friendly packaging. Metal containers and glass bottles remain popular choices for distilled spirits like vodka and Calvados, known for their premium and sophisticated appeal. In recent years, there has been a surge in recycling efforts within the alcohol packaging market. Recycled glass bottles and packaging pouches made from eco-friendly materials like apple pulp are gaining traction due to their sustainable attributes. Additionally, kegs are being utilized extensively for beer production, offering convenience and environmental benefits through reduced packaging waste. The market's segmentation is evident in the diverse preferences of consumers, ranging from glass bottles for wine enthusiasts to metal cans for beer lovers seeking portability and convenience. Alcohol packaging continues to evolve, with innovative designs such as paper wine bottles and whiskey pouches catering to modern and eco-conscious consumers.

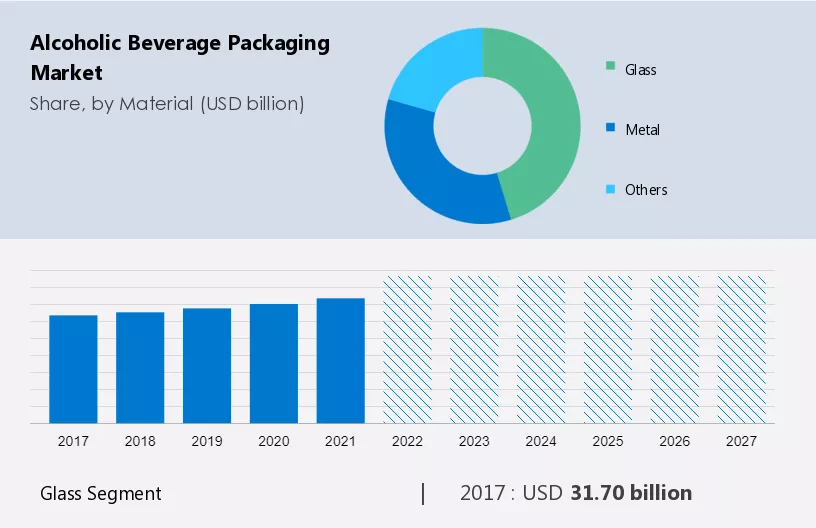

The glass segment is estimated to witness significant growth during the forecast period. On the basis of materials, the market is segmented into glass, metal, and others. The market share growth by the glass segment will be significant during the forecast period. The growth of the beer and wine market, where glass packaging is prominently used, is expected to increase the demand for glass packaging further. The global wine market is largely dominated by European and North American countries. Countries such as the US, France, Italy, and Spain are some of the largest producers and consumers of wine. Although the consumption of wine in these countries is slowing down, wine consumption is growing in the emerging economies of Asia, such as China.

Get a glance at the market contribution of various segments View PDF Sample

The glass segment shows a gradual increase in the market share of USD 31.70 billion in 2017 and continued to grow by 2023. The global whiskey market is expected to grow at a CAGR of more than 2% during the forecast period. The market is expected to grow due to the rise in product innovations in whiskey; for example, the whiskey industry is seeing the launch of many organic whiskeys that do not contain any artificial colors. Companies such as Benromach and The Organic Spirits offer organic whiskey. The growing nature of the whiskey and wine market is expected to increase the demand for alcoholic glass beverage packaging during the forecast period.

Beer, wine, and spirits come under the umbrella of application analysis. Beer production involves steeping a starch source, usually cereal grains such as rice, corn, and barley, in water and fermenting the sugar-containing liquid with yeast. Beer is not considered a healthy beverage due to its high-calorie content. This segment holds the highest share of the global market in 2022, and it is expected to continue to dominate the market during the forecast period. Mostly, glass bottles are used for the packaging of beer as it helps maintain the high quality of beer. Another widely used material for beer packaging is metal cans. These cans are generally made of aluminum because of its lightweight, and aluminum cans can be efficiently shipped and stored. Southeast Asia is becoming a promising market for beer producers, owing to the presence of a young population and high economic growth compared with developed countries such as Germany. International companies such as Heineken and Carlsberg Breweries AS (Carlsberg) are continuously expanding their businesses in this region by acquiring various dominant local brands. Such factors will drive the demand for alcoholic beverage packaging materials during the forecast period. Hence, the beer segment in the global market is expected to grow during the forecast period.

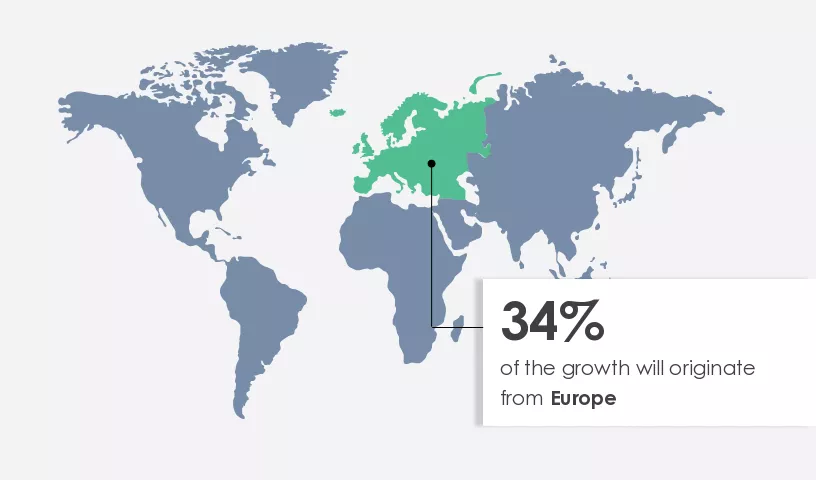

Europe is expected to account for 34% of market growth by 2023. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions View PDF Sample now!

People in Europe are among the highest consumers of alcohol globally. As of 2020, more than 60% of adults in Europe consumed alcohol. The per capita consumption in terms of pure alcohol in Europe was more than 9.5 liters in 2019. People living in countries such as Luxembourg, Ireland, Germany, Poland, Lithuania, and the UK, on average, had more than two alcoholic drinks every day in 2019. People in Lithuania are one of the world's heaviest drinkers. They consumed more than 16 liters of pure alcohol per person in 2019, which was over 20% more than the 2014 value. Similarly, the consumption of alcohol in Iceland is growing significantly. For example, as of 2020, households spent on average, roughly 46 billion Icelandic kronurs on alcoholic beverages. Such factors are expected to drive the growth of the global market during the forecast period.

The market is driven by the increasing demand for glass, metal, and plastic containers, especially cans and bottles, reflecting the diversity of alcoholic beverages like beer, wine, and spirits. Premium spirit bottles, eco-friendly packaging, and innovations such as paper wine bottles and whiskey pouches are notable trends. Challenges include balancing sustainability with branding needs and addressing recycling complexities. As consumers seek convenience and environmental responsibility, the market is navigating packaging formats to align with evolving consumer preferences while ensuring product integrity and regulatory compliance.

Growing demand for metal cans from the craft beer industry will notably drive the alcoholic beverage market growth. Aluminum cans are used extensively for alcoholic beverages, especially beer, which is one of the most commonly consumed alcoholic beverages worldwide. Metal cans provide certain advantages over other materials in packaging alcoholic beverages such as beer.

For example, metal cans can block out light and oxygen, both of which can react with the beer and have an undesirable effect on its chemical properties, such as the generation of a foul aroma. In addition, less material is required to manufacture around five packs of cans when compared with bottles. These factors contribute to the increase in demand for metal cans in the beer industry.

The growing popularity of standup pouches and bag-in-box packaging is a major trend driving the growth of the alcoholic beverage market. The bag-in-box type of packing offers several advantages over glass bottles, such as lower weight and portability, which are driving the market for bag-in-box packing. The bag-in-box is a type of container where a plastic bag that is generally made of several layers of metalized film or other plastics is packed inside a corrugated fiberboard box.

Companies such as DS Smith offer bag-in-box packing for wine. The global market was valued at around USD 2.7 billion in 2019 and is expected to grow at a CAGR of over 5% during the forecast period. The rising popularity of standup pouches and bag-in-box packing is expected to drive the global market in the future.

The rising cost of raw materials and energy increasing the production cost of packaging may impede market growth. In addition, the use of fuels such as coal increases operational costs. Therefore, any increase in the prices of raw materials and energy poses a major challenge to the companies operating in the global market.

Glass manufacturers must deal with a rise in manufacturing costs due to the increasing cost of raw materials such as sand and energy. Hence, the rising demand for huge quantities of sand from shale companies in the US is increasing the cost of the sand.

The market research report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Market Customer Landscape

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Amcor - The company offers alcoholic beverage packaging such as the shelving closure system designed for wine.

The alcoholic beverage market report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

Qualitative and quantitative market research and growth analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. In market growth analysis, data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2023 to 2027, as well as historical data from 2017 to 2021 for the following segments

The market is witnessing diverse trends driven by consumer preferences and sustainability initiatives. Packaging formats like paper wine bottles and whiskey pouches showcase the industry's shift towards sustainable packaging products. Companies like Avallen and Silent Pool Distillers are embracing eco-friendly practices with recycled glass bottles and apple pulp labels. Eco-friendly materials and recycling efforts address environmental factors and consumer well-being. Innovative packaging designs, unique finishes, and security systems enhance brand differentiation and attract consumer attention. Labelling standards ensure safety and transparency, catering to consumer preferences for premium experiences and authenticity. The industry's focus on environmental responsibility includes reducing carbon footprints, increasing recycling rates, and minimizing plastic packaging to safeguard wildlife and marine ecosystems. Collaborative efforts across manufacturing, transportation, and recycling sectors drive the alcoholic beverage packaging market towards sustainability and user experience while ensuring product freshness and consumer safety.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

170 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.41% |

|

Market growth 2023-2027 |

USD 31.74 billion |

|

Market structure |

Fragmented |

|

YoY growth 2022-2023(%) |

7.16 |

|

Regional analysis |

Europe, APAC, North America, South America, and Middle East and Africa |

|

Performing market contribution |

Europe at 34% |

|

Key countries |

US, China, India, Germany, and France |

|

Competitive landscape |

Leading companies, Market Positioning of companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Amcor Plc, Ardagh Group SA, Ball Corp., Beatson Clark Ltd., Berry Global Group Inc., Brick Packaging, Compagnie de Saint Gobain SA, Crown Holdings Inc., Diageo Plc, DS Smith Plc, Gerresheimer AG, KRONES AG, Mondi plc, O I Glass Inc., Orora Ltd., Smurfit Kappa Group, Tetra Laval S.A., Vetreria Etrusca Spa, and Vidrala SA |

|

Market dynamics |

Parent market analysis, Market forecasting, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Material

7 Market Segmentation by Application

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.