Enjoy complimentary customisation on priority with our Enterprise License!

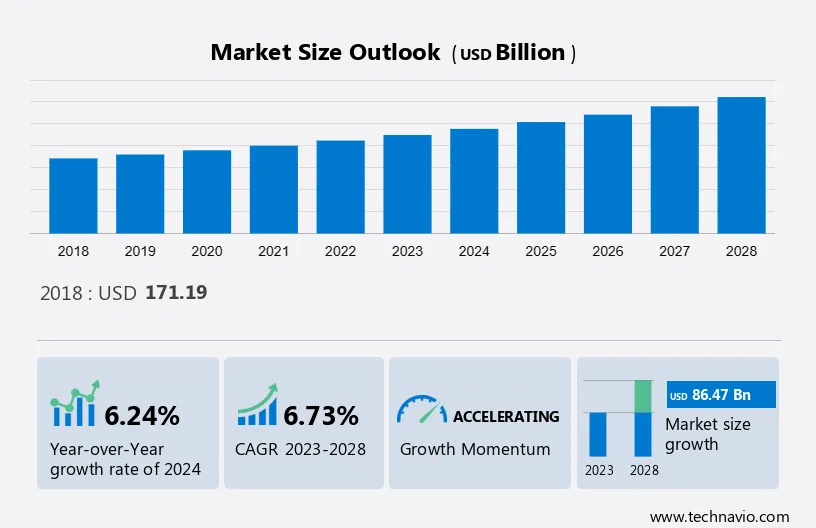

The Active Pharmaceutical Ingredients (API) Market size is estimated to grow by USD 86.47 billion at a CAGR of 6.73% between 2023 and 2028.

The active pharmaceutical ingredients market is currently witnessing an upward trend of intent to outsource APIs by leading players in the pharmaceutical industry. For emerging biopharmaceutical and virtual pharmaceutical companies, a vast majority of the API and intermediate manufacturing is done by outsourcing providers. This trend is also observed in generic drug manufacturing, where orchestration is done by the generic drug manufacturer to have the API manufacturing outsourced by a large portion. In addition, API manufacturers are known to obtain a cost advantage through economies of scale and the availability of low-cost labour and land. Various large pharmaceutical companies, such as Pfizer, have been sourcing a large share of their manufacturing activities of bulk actives used for the preparation of finished drugs, primarily generic drugs, to focus on the expansion of their pipelines for various major indications. The growing need for pharmaceutical companies to focus on their core competencies is expected to contribute to the growth of the API market during the forecast period.

Technavio has segmented the market into Manufacturing Type, Type, and Geography

It also includes an in-depth analysis of drivers, trends, and challenges. Our report examines historical data from 2018-2022, besides analyzing the current market scenario.

To learn more about this report, Request Free Sample

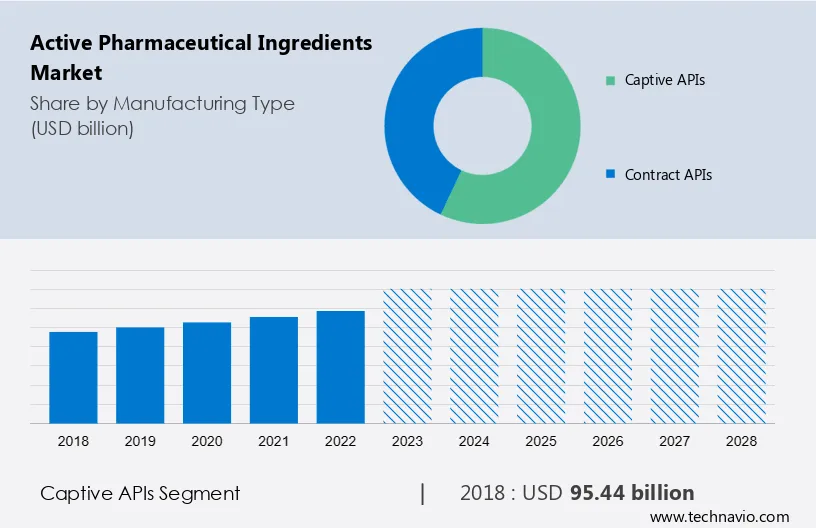

The market share growth by the captive APIs segment will be significant during the forecast period. In 2023, the captive API manufacturing segment accounted for the largest share of the global active pharmaceutical ingredients active pharmaceutical ingredients (API) market. The increased adoption of healthcare services has benefited the global active pharmaceutical ingredients market significantly.

Get a glance at the market contribution of various segments Download PDF Sample

The captive APIs segment was the largest and was valued at USD 95.44 billion in 2018. Furthermore, the increasing emphasis of healthcare regulatory authorities on quality control of APIs and their production facilities is a growing concern for manufacturers, resulting in increased dependency on in-house capabilities for the manufacturing of high-quality APIs. Drug manufacturers are advised to strictly adhere to the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH) guidelines and the US Non-adherence to these guidelines can lead to batch recalls, thus exposing drug manufacturers to an increased financial burden. To overcome these barriers, innovators rely on their in-house capabilities for manufacturing APIs, which is the major factor driving the growth of this segment. Thus, major companies such as Pfizer, Novartis, Sanofi, and GlaxoSmithKline Plc are investing in in-house API capabilities, which will drive the growth of the captive API segment and thereby expand the growth of the API market during the forecast period.

Innovative APIs refer to new or novel pharmaceutical ingredients that have never been used in a commercial product before. Innovative APIs may include new chemical entities (CIs), new biologics, new biosimilars, or other novel formulations. Innovative APIs represent the latest innovations in the pharmaceutical sector and help drive new and better drug therapies. Additionally, innovative APIs are in high demand due to a variety of factors, including an increase in chronic diseases, an increase in healthcare spending, and an aging population around the world. Additionally, regulatory agencies' focus on strict quality and safety requirements further fuels the active pharmaceutical ingredients (API) market for innovative APIs. Thus, the increasing demand for the innovative APIs segment will accelerate the growth of the global API market during the forecast period.

Generic APIs are those that are subject to patent expiry and can be manufactured and marketed by a variety of manufacturers. Generally, generic APIs are chemically equivalent to branded drugs and are manufactured after the expiration of the patent exclusivity. Generic APIs comprise therapeutic areas, including cardiovascular, central nervous system, respiratory, anti-diabetes, and other areas. This classification enables pharmaceutical companies to tailor their strategies to the specific requirements of each therapeutic segment by taking into account the prevalence of disease, patient needs, regulatory needs, and pricing dynamics. These abovementioned features and properties will drive the demand for generic APIs and will expand the growth of the API market during the forecast period.

For more insights about the market share of various regions Download PDF Sample now!

Asia is estimated to contribute 52% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that will shape the market during the forecast period. Asia accounted for the largest share of the active pharmaceutical ingredients (API) market in 2022. Indian companies have become very proficient at the manufacturing of pharmaceutical products in compliance with the good manufacturing practice (GMP) standards, meeting the regulatory needs of the US- and Europe-based generic drug companies and commercializing their bulk products at a large scale. Several Indian manufacturers, including Lupin Ltd. (Lupin) and Sun Pharmaceutical Industries Ltd. (Sun Pharma), are successfully competing in the US generic drug market.

Furthermore, the presence of key companies in the region, such as Cipla, Sun Pharmaceutical Industries Ltd., Aurobindo Pharma Ltd., and Dr Reddys Laboratories Ltd., coupled with government efforts to boost the API production in the country, will drive the growth of the active pharmaceutical ingredients market in the region during the forecast period.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

AbbVie Inc. - The company offers active pharmaceutical ingredients such as organometallic and gaseous HCl.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

There are multiple factors influencing market growth. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges.

The increasing number of type II drug master files (DMF) is notably driving the market growth. Apart from the increased healthcare expenditure by the urban population across the world and a rapid surge in the aged population, the active pharmaceutical ingredient market stands to gain additional traction from the increase in the number of DMFs filing for APIs. A DMF is submitted to the US FDA, which provides detailed information about the facilities, processes, and materials used in the manufacturing, processing, and packaging of drugs intended for human use. The information contained in a DMF may be used to support an investigational new drug (IND) application, a new drug application (NDA), an abbreviated new drug application (ANDA), another DMF, an export application, or related documents. There are five types of DMFs that can be granted, each requiring a different type of information.

Moreover, the active pharmaceutical ingredient market is rapidly emerging as pharmaceutical manufacturers are increasingly relying on API manufacturers for outsourcing bulk actives for manufacturing generic drugs and high-end, difficult-to-manufacture patented drugs. Globally, API manufacturers have been leveraging the increased outsourcing demand for APIs or intermediates, which is reflected through the aggressive DMF filings made by these manufacturers. This increasing number of type II drug master files is expected to drive the growth of the API market during the forecast period.

The increasing geriatric population is an emerging trend shaping the market growth. The active pharmaceutical ingredient market is expected to benefit from the increasing geriatric population. The risk of acquiring or developing chronic illness in people increases with their age, which, in turn, propels the demand for various therapeutics for their treatment, consequently leading to an increase in demand for APIs. Comorbid conditions among geriatric people (aged 65 years and above), along with sleep, cognition, strength, and physical balance, are the factors that negatively impact a person's ability to function properly and make disease management more difficult. Moreover, the CDC estimates that the total healthcare spending in the US will increase by 25% by 2030, largely due to the increasing geriatric population.

However, to reduce the impact of economic burden, national healthcare regulatory bodies promote the use of generic drugs for the treatment of geriatric patients, resulting in increased approval of generics. This, in turn, leads to increased penetration of generic drug manufacturers in the US and Europe. These generic drug manufacturers outsource raw materials from API manufacturers to provide cost-effective therapeutics, which contributes to the growth of the API market during the forecast period.

Capacity utilization constraints are a significant challenge hindering the market growth. Currently, the active pharmaceutical ingredient market is facing a major threat from constraints related to capacity utilization. Capacity utilization is a measure of actual production compared with the potential production of a company when the capacity is completely utilized. It has a major role in the production of APIs, particularly for manufacturing biologics, due to the complex manufacturing process. API capacity is strategic in terms of vertical integration and supply to regulated markets. Drug manufacturers are expected to make additional investments in capacity creation and capacity building. Most companies face a challenge with developing advanced downstream purification technologies, which are used for the recovery and purification of biosynthetic products.

Moreover, the limited number of approved manufacturing facilities is also causing a capacity constraint. The lack of new and experienced scientists, technical staff, and production staff; the shortage of cost-effective single-use products; and limitations in advanced cell culture systems for upstream performance are also causing constraints in the global active pharmaceutical ingredients market, which is expected to hinder the growth of API market during the forecast period.

The market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Active Pharmaceutical Ingredients Market Customer Landscape

The active pharmaceutical ingredients market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

|

Active Pharmaceutical Ingredients Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.73% |

|

Market Growth 2024-2028 |

USD 86.47 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.24 |

|

Regional analysis |

Asia, North America, Europe, and Rest of World (ROW) |

|

Performing market contribution |

Asia at 52% |

|

Key countries |

US, Germany, China, India, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

AbbVie Inc., Amneal Pharmaceuticals Inc., Apotex Inc., Aurobindo Pharma Ltd., Cadila Pharmaceuticals Ltd., Cambrex Corp., Cipla Ltd., Dr Reddys Laboratories Ltd., GlaxoSmithKline Plc, Indena S.p.A., INTERNATIONAL CHEMICAL INVESTORS S.E., Koninklijke DSM NV, Lupin Ltd., Novartis AG, Pfizer Inc., Sanofi SA, Sun Pharmaceutical Industries Ltd., Teva Pharmaceutical Industries Ltd., Thermo Fisher Scientific Inc., and Viatris Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

Download Sample PDF at your Fingertips

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Manufacturing Type

7 Market Segmentation by Type

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Market Analysis Asia, North America, Europe, Rest of World (ROW) - US, Germany, China, India, Japan - Size and Forecast 2024-2028")