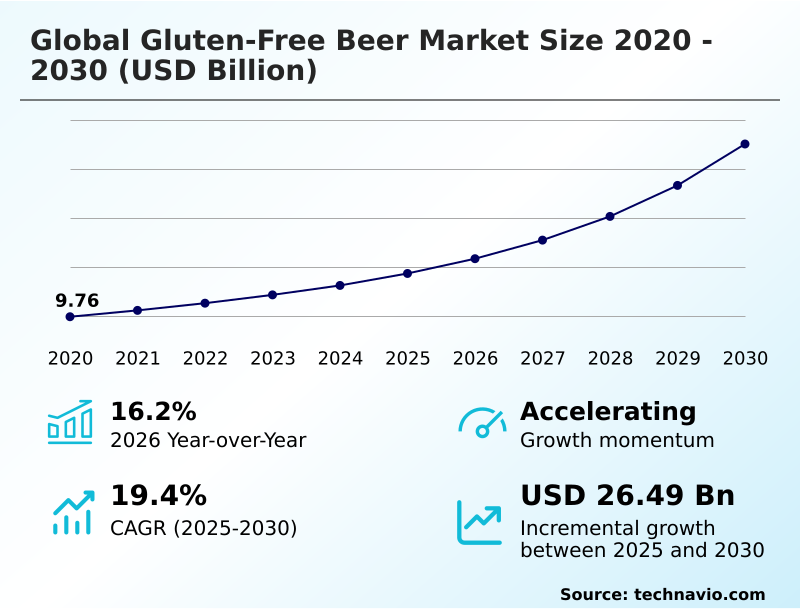

Gluten-free Beer Market Size 2026-2030

The gluten-free beer market size is valued to increase by USD 26.49 billion, at a CAGR of 19.4% from 2025 to 2030. Growing awareness of health benefits of gluten-free food products will drive the gluten-free beer market.

Major Market Trends & Insights

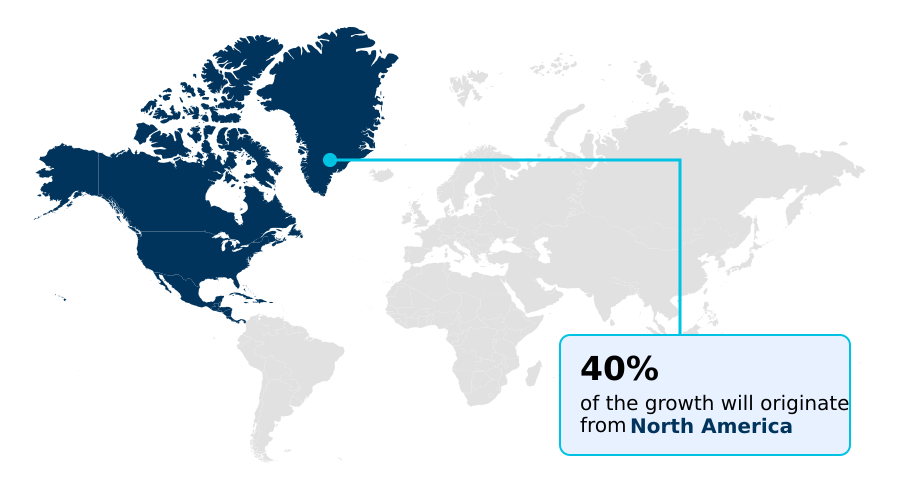

- North America dominated the market and accounted for a 39.8% growth during the forecast period.

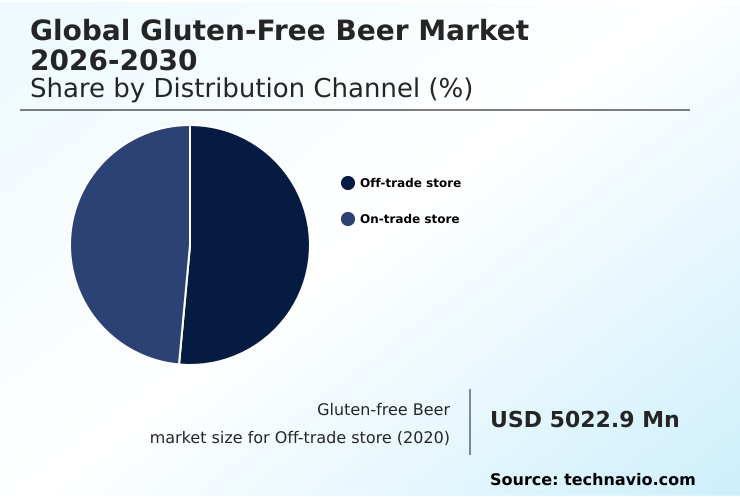

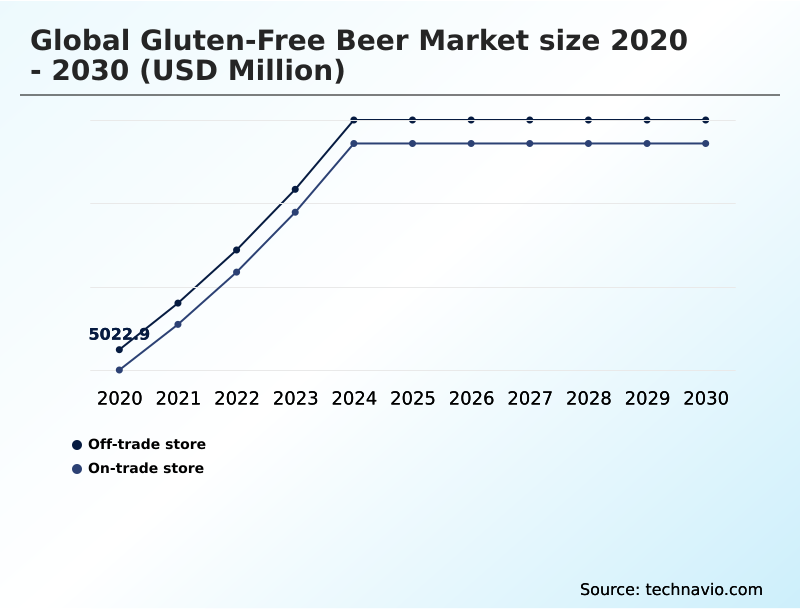

- By Distribution Channel - Off-trade store segment was valued at USD 8.25 billion in 2024

- By Type - Sorghum corn and rice segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 35.33 billion

- Market Future Opportunities: USD 26.49 billion

- CAGR from 2025 to 2030 : 19.4%

Market Summary

- The gluten-free beer market is evolving from a niche category into a significant lifestyle segment, driven by heightened celiac disease awareness and broader consumer dietary trends toward health-conscious consumption. A key dynamic is the continuous craft brewing innovation aimed at achieving sensory quality enhancement in products.

- This involves using alternative grains, advanced brewing enzymes, and sophisticated fermentation control systems to create compelling allergen-free beverages. For instance, a mid-sized brewery aiming for niche market expansion must navigate complex supply chain logistics for specialty grain sourcing.

- A critical business scenario involves implementing a transparent brewing process to ensure cross-contamination prevention in a dedicated gluten-free facility, which builds consumer brand loyalty. This requires rigorous quality control and often gluten-free certification.

- However, the market also contends with challenges like competition from other dietary friendly alternatives and the complexities of regulatory compliance management, which can impact market entry strategy and product portfolio diversification. The adoption of sustainable brewing practices and clean label ingredients is becoming a standard expectation, influencing both production methods and brand storytelling marketing.

What will be the Size of the Gluten-free Beer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Gluten-free Beer Market Segmented?

The gluten-free beer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Off-trade store

- On-trade store

- Type

- Sorghum corn and rice

- Buckwheat

- Others

- Packaging

- Bottles

- Cans

- Kegs

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Turkey

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The off-trade store segment is estimated to witness significant growth during the forecast period.

The off-trade store segment is the principal growth driver, commanding approximately 65% of total market sales. This channel's dominance stems from the widespread availability of products in supermarkets, hypermarkets, and liquor stores, supporting a robust off-trade retail strategy.

The expansion of e-commerce beverage platforms further facilitates health-conscious consumption by offering convenient access to a wide range of allergen-free beverages. This direct-to-consumer sales model enhances the visibility of innovations like sorghum-based ale and buckwheat brewing.

Producers are focusing on sustainable brewing practices and advanced filtration methods to meet consumer dietary trends and ensure product quality, bolstering consumer brand loyalty and driving niche market expansion through organized retail penetration, which is critical for the specialty beverage market.

The Off-trade store segment was valued at USD 8.25 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Gluten-free Beer Market Demand is Rising in North America Get Free Sample

The global landscape is led by North America, which accounts for nearly 40% of the incremental growth opportunity, driven by high celiac disease awareness and a mature craft beer community.

The region's sophisticated supply chain logistics for alternative grains have enabled producers to reduce raw material waste by over 15%.

Europe follows as a key region, characterized by stringent regulatory compliance management and strong on-trade channel expansion, especially in the UK and Germany.

Meanwhile, APAC is the fastest-growing market, fueled by rising health-conscious consumption and the premiumization of beverages in urban centers across China and Australia.

This horeca sector demand is creating new avenues for product portfolio diversification and niche market expansion, pushing for greater food service inclusivity worldwide and prompting innovations in rice malt production.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The increasing demand for gluten-free beer is reshaping the alcoholic beverage sector, driven primarily by consumers seeking options for gluten-free beer for celiac disease and those interested in gluten-free beer and digestive health. This has spurred innovations in gluten-free brewing techniques, with many producers brewing gluten-free beer with sorghum or exploring the benefits of buckwheat in gluten-free beer.

- Craft breweries with gluten-free options are at the forefront, developing diverse gluten-free ipa and stout varieties and expanding the availability of non-alcoholic gluten-free beer brands. A key technological driver is the use of enzyme technology for gluten removal, which allows for a wider range of flavor profiles.

- The gluten-free beer market in North America remains a dominant force, though producers globally face challenges in gluten-free brewing ingredients. The competitive landscape of gluten-free beer is becoming more complex, influencing gluten-free beer packaging trends cans vs bottles. The consumer perception of gluten-free beer taste is steadily improving due to advancements like rice-based gluten-free lager production.

- Companies that deploy effective marketing strategies for gluten-free beer, particularly through online retail for gluten-free beverages, see customer engagement rates more than double those of competitors. This growth is happening alongside the need to navigate the impact of regulations on gluten-free beer and promote sustainable practices in gluten-free brewing.

What are the key market drivers leading to the rise in the adoption of Gluten-free Beer Industry?

- The primary driver for market growth is the increasing consumer awareness of the health benefits associated with gluten-free food and beverage products.

- Growth is fundamentally driven by rising celiac disease awareness and a broader shift toward health-conscious consumption.

- The presence of clean label ingredients is a key purchasing factor, with products highlighting a transparent brewing process showing a 25% higher rate of adoption among new consumers.

- Increased organized retail penetration has also been critical, as placement in mainstream supermarkets boosts a product's initial sales velocity by over 50% compared to specialty store-only distribution.

- This accessibility, combined with constant artisanal beverage production and innovation, expands the market beyond medical necessity.

- As consumer dietary trends evolve, the demand for high-quality, functional beverage ingredients and dietary friendly alternatives continues to strengthen, reinforcing the need for product portfolio diversification and a solid market entry strategy.

What are the market trends shaping the Gluten-free Beer Industry?

- The growing influence of online retailing is a transformative trend shaping the market. Digital commerce enhances accessibility and brand discovery for both niche and established producers.

- The market is increasingly shaped by the influence of online retailing and continuous craft brewing innovation. The adoption of e-commerce beverage platforms allows for a direct-to-consumer sales model, enabling brands to achieve up to 40% greater market penetration in new regions compared to relying on traditional retail alone.

- This digital shift supports the premiumization of beverages and provides a platform for brand storytelling marketing. Concurrently, the trend of small-batch production is accelerating product development, with craft producers launching new fruit-infused lager and botanical-infused beer styles in half the time of larger competitors.

- This agility meets the demand for a transparent brewing process and strengthens consumer brand loyalty within the taproom and brewpub culture, driving the overall lifestyle beverage choice.

What challenges does the Gluten-free Beer Industry face during its growth?

- A key challenge impacting industry growth is the restricted availability of specialized gluten-free brewing ingredients.

- Key challenges center on operational and competitive pressures, including the complexities of specialty grain sourcing and strict regulatory compliance management. The cost of certified organic ingredients and other alternative grains can be up to 35% higher than conventional malt, directly impacting price competitiveness and market entry strategy.

- Furthermore, navigating international gluten-free certification standards adds significant overhead, extending product launch timelines by an average of six months. The industry also faces intense rivalry from a widening array of dietary friendly alternatives. Firms must focus on sensory quality enhancement and efficient supply chain logistics to maintain margins.

- This environment demands continuous innovation in fermentation control systems and malting process alternatives to overcome inherent production hurdles and secure a competitive footing.

Exclusive Technavio Analysis on Customer Landscape

The gluten-free beer market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gluten-free beer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Gluten-free Beer Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, gluten-free beer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ALT Brew - The portfolio includes sorghum-based gluten-free beers and gluten-reduced variants, catering to diverse dietary needs through established global brands and innovative formulations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALT Brew

- Anheuser Busch InBev SA NV

- Bards Tale Beer Co.

- Brasserie de Brunehaut SA

- Brasseurs Du Monde

- Brewery Rickoli

- Burning Brothers Brewing LLC

- Dohler GmbH

- DSM Firmenich AG

- Duck Foot Brewing Co.

- Epic Brewing Co.

- Ghostfish Brewing Co.

- Ground Breaker Brewing

- Holidaily Brewing Co.

- Ipswich Ale Brewery

- Lakefront Brewery Inc.

- Molson Coors Beverage Co.

- New Belgium Brewing Co. Inc.

- New Planet Beer Co.

- Stone Brewing Co. LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Gluten-free beer market

- In November, 2024, Darling Brew launched its Break Free gluten-free lager, expanding its portfolio to cater to the health-conscious consumer segment with a product praised for its flavor and sustainable production methods.

- In January, 2025, Kati Patang, an Indian craft beverage company, acquired a minority stake in the UK-based Chadlington Brewery to scale the production and European distribution of its saffron-infused, gluten-free lager.

- In April, 2025, Japanese brewery Rice Hack introduced its Oryvia range, a new line of rice-based, allergen-free beers targeting urban professionals and capitalizing on the appeal of using familiar, indigenous grains.

- In May, 2025, Anheuser-Busch InBev entered into a strategic partnership with a prominent Canadian craft producer to co-develop and market a new line of innovative sorghum-based ales for the mass market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Gluten-free Beer Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 19.4% |

| Market growth 2026-2030 | USD 26486.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, South Africa, UAE, Turkey, Israel and Saudi Arabia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a strategic transformation, moving beyond its origins in addressing non-celiac gluten sensitivity to become a mainstream choice for lifestyle-oriented consumers. This shift is underpinned by significant craft brewing innovation and advancements in gluten reduction technology, including sophisticated brewing enzymes and malting process alternatives.

- A critical boardroom-level decision involves weighing the investment in a dedicated gluten-free facility, which ensures absolute cross-contamination prevention, against the operational flexibility of using enzymatic gluten removal in existing lines. The focus on sensory quality enhancement has led to the development of diverse products such as sorghum-based ale, botanical-infused beer, and low-calorie beer formulation.

- Breweries utilizing advanced filtration methods report a 20% improvement in product consistency. The use of alternative grains like millet and quinoa, alongside developments in rice malt production and yeast strain development, is expanding the range of available allergen-free beverages.

- Achieving gluten-free certification for these functional beverage ingredients and clean label ingredients remains a priority, reinforcing consumer trust and market position through beverage flavor profiling and high-protein grain brewing in pilot-scale brewing labs.

What are the Key Data Covered in this Gluten-free Beer Market Research and Growth Report?

-

What is the expected growth of the Gluten-free Beer Market between 2026 and 2030?

-

USD 26.49 billion, at a CAGR of 19.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Off-trade store, and On-trade store), Type (Sorghum corn and rice, Buckwheat, and Others), Packaging (Bottles, Cans, and Kegs) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing awareness of health benefits of gluten-free food products, Restricted availability of gluten‑free brewing ingredients

-

-

Who are the major players in the Gluten-free Beer Market?

-

ALT Brew, Anheuser Busch InBev SA NV, Bards Tale Beer Co., Brasserie de Brunehaut SA, Brasseurs Du Monde, Brewery Rickoli, Burning Brothers Brewing LLC, Dohler GmbH, DSM Firmenich AG, Duck Foot Brewing Co., Epic Brewing Co., Ghostfish Brewing Co., Ground Breaker Brewing, Holidaily Brewing Co., Ipswich Ale Brewery, Lakefront Brewery Inc., Molson Coors Beverage Co., New Belgium Brewing Co. Inc., New Planet Beer Co. and Stone Brewing Co. LLC

-

Market Research Insights

- The market's momentum is shaped by the convergence of consumer wellness goals and retail evolution. The expansion of the direct-to-consumer sales model has been a pivotal shift, with brands that leverage this channel reporting up to a 20% higher customer lifetime value compared to those relying solely on traditional distribution.

- This strategy supports the premiumization of beverages and aligns with the demand for a transparent brewing process. Concurrently, food service inclusivity is driving on-trade channel expansion, as establishments that offer dietary friendly alternatives see a 15% increase in traffic from groups with mixed dietary needs.

- This growth is reinforced by organized retail penetration, where clear allergen-safe recommendations and product placement boost trial rates. These dynamics transform a lifestyle beverage choice into a cornerstone of modern retail and hospitality, emphasizing the importance of a sophisticated market entry strategy.

We can help! Our analysts can customize this gluten-free beer market research report to meet your requirements.

RIA -

RIA -