Grid Congestion Management Systems Market Size 2026-2030

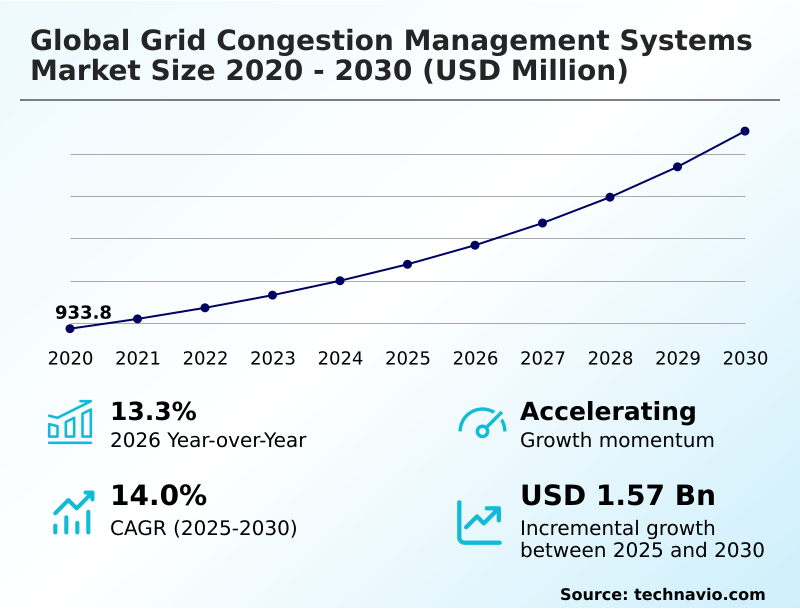

The grid congestion management systems market size is valued to increase by USD 1.57 billion, at a CAGR of 14% from 2025 to 2030. Integration of variable renewable energy sources will drive the grid congestion management systems market.

Major Market Trends & Insights

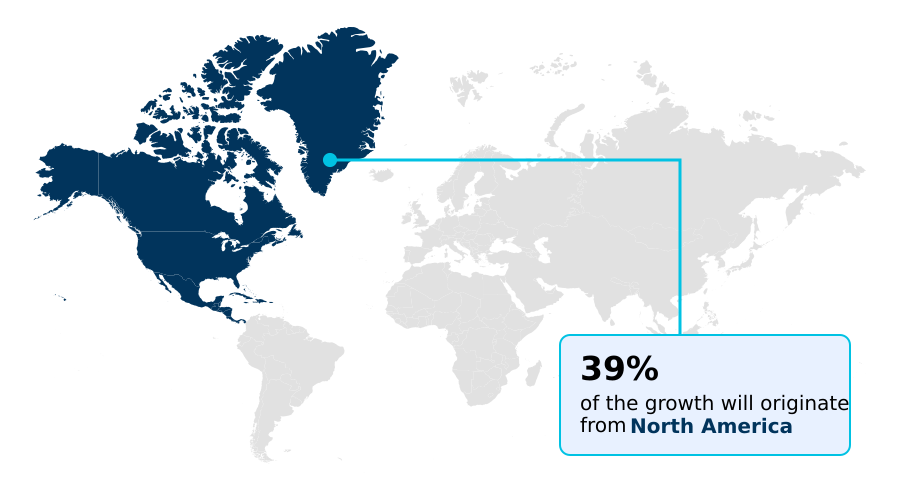

- North America dominated the market and accounted for a 39.3% growth during the forecast period.

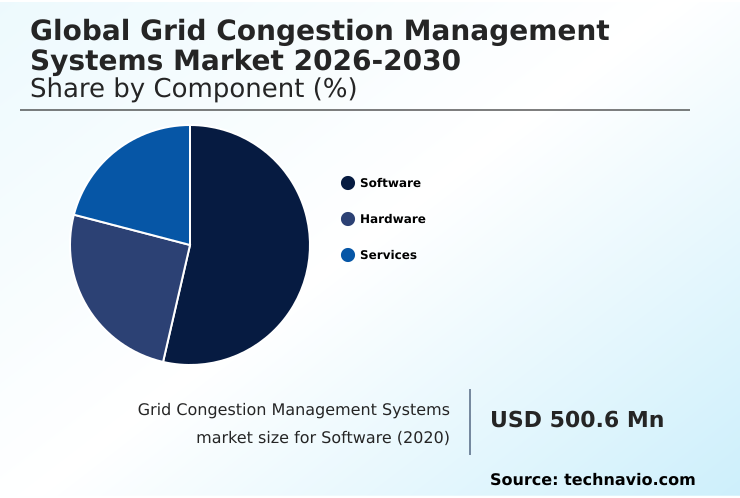

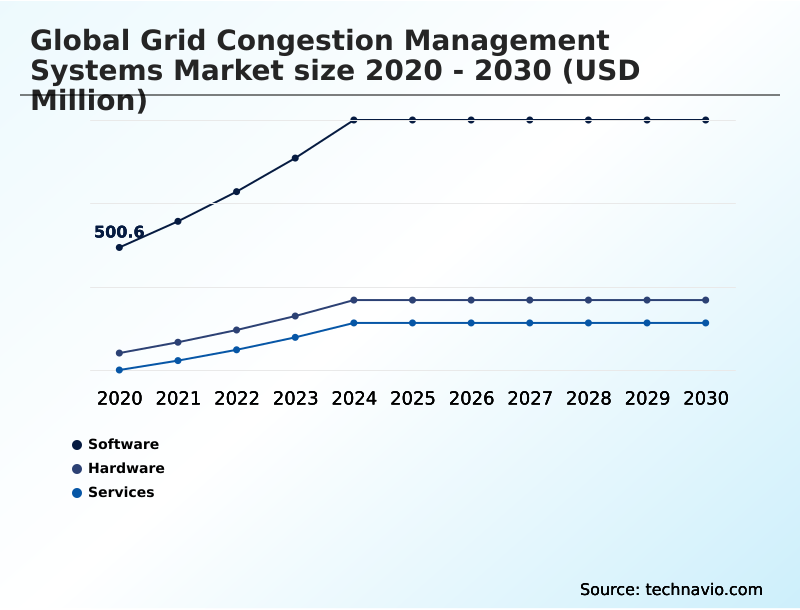

- By Component - Software segment was valued at USD 818 million in 2024

- By Type - Real-time congestion management segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.33 billion

- Market Future Opportunities: USD 1.57 billion

- CAGR from 2025 to 2030 : 14%

Market Summary

- The grid congestion management systems market is undergoing a significant transformation, driven by the need for enhanced transmission network stability amid the large-scale integration of variable power sources. Modernization of aging infrastructure and the increasing electrification of transport are compelling utilities to adopt non-wire alternatives.

- These solutions leverage technologies such as digital twin technology and predictive grid analytics to maximize the efficiency of existing assets. A key trend is the shift toward probabilistic forecasting, which allows operators to anticipate and mitigate bottlenecks before they impact the grid.

- For instance, a utility can use a congestion forecasting model to analyze weather patterns and historical load data, proactively adjusting power flows from renewable sources to prevent curtailment and ensure grid reliability. However, challenges related to the interoperability of new systems with legacy supervisory control and data acquisition (SCADA) infrastructure persist.

- The market's evolution is defined by this balance between technological innovation and the practicalities of upgrading complex, interconnected power networks, all while addressing heightened smart grid cybersecurity risks.

What will be the Size of the Grid Congestion Management Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Grid Congestion Management Systems Market Segmented?

The grid congestion management systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Hardware

- Services

- Type

- Real-time congestion management

- Congestion forecasting and prediction

- Market-based congestion management

- Others

- End-user

- Transmission system operators

- Distribution system operators

- Utilities and energy retailers

- Renewable energy developers and aggregators

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is central to the global grid congestion management systems market 2026-2030, driven by the need for advanced analytical tools.

Platforms like advanced distribution management systems (ADMS) and distributed energy resource management systems (DERMS) are critical for distribution network optimization. These solutions employ grid orchestration software and predictive congestion modeling to enhance grid visibility enhancement and manage behind-the-meter assets.

By leveraging AI, utilities can perform probabilistic forecasting to anticipate bottlenecks, enabling proactive energy dispatch optimization and thermal overload prevention.

For instance, recent deployments of autonomous congestion relief modules have shown a capability to reduce emergency redispatching actions by over 25%, demonstrating a clear operational efficiency gain and supporting overall grid modernization efforts.

The Software segment was valued at USD 818 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Grid Congestion Management Systems Market Demand is Rising in North America Get Free Sample

The geographic landscape of the grid congestion management systems market reflects diverse regional priorities. North America, accounting for 39.3% of the market's incremental growth, focuses on grid modernization and deploying power flow controllers for renewable energy integration.

Europe prioritizes cross-border electricity trade and demand-side flexibility, utilizing cross-border interconnectors and market-based redispatching to ensure transmission network stability.

The APAC region, with the highest projected growth, is rapidly adopting wide-area monitoring systems (WAMS) and decentralized control algorithms to manage its expanding energy transition infrastructure.

Implementations of dynamic line rating in Europe have demonstrated the ability to increase transmission capacity maximization by over 20%. These regional approaches underscore a global commitment to congestion relief mechanisms.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global grid congestion management systems market 2026-2030 is increasingly shaped by complex operational challenges and technological solutions. The impact of EV charging on grid congestion is a primary concern, driving the development of software solutions for real-time congestion and smart charging infrastructure.

- At the same time, grid operators are increasingly using AI for predictive grid congestion, moving beyond reactive measures. The debate between dynamic line rating vs static rating highlights a key industry shift, with dynamic systems offering superior asset utilization.

- Managing congestion from renewable sources remains a central task, where DERMS for distribution network congestion and VPPs in localized congestion management play a crucial role. These non-wire alternatives demonstrate clear benefits, often deferring costly physical upgrades.

- For instance, utilities employing digital twin for transmission grid simulation can identify and resolve potential bottlenecks twice as fast as those relying on traditional methods. However, cybersecurity risks in congestion management are a growing concern.

- Market-based congestion management mechanisms and regulatory frameworks for grid flexibility are evolving to address these issues, while integrating storage for congestion relief and deploying FACTS devices for power flow control offer technical solutions. The role of PMUs in grid monitoring and the use of HVDC for long-distance power transmission are foundational.

- Success in this landscape also hinges on reducing renewable energy curtailment costs and overcoming challenges of legacy system integration, particularly in congestion management in smart cities and optimizing cross-border energy trading.

What are the key market drivers leading to the rise in the adoption of Grid Congestion Management Systems Industry?

- The integration of variable renewable energy sources is a key driver for the market, creating a critical need for advanced systems to manage grid volatility and intermittency.

- Market growth is fundamentally driven by the global energy transition. The massive scale of renewable energy integration introduces volatility that necessitates sophisticated load balancing solutions and topology optimization.

- The modernization of aging grids provides an opportunity to deploy non-wire alternatives, which can defer capital-intensive projects for over five years in some cases.

- Concurrently, the electrification of transport is creating new demand patterns that require smart charging stations and advanced demand response management. These systems support distribution network optimization by managing flexible industrial loads and residential consumption.

- Deploying secondary substation sensors has been shown to improve real-time operational visibility by 30%, enabling more precise congestion cost reduction and voltage stability control.

What are the market trends shaping the Grid Congestion Management Systems Industry?

- The proliferation of artificial intelligence and machine learning for predictive grid management is a defining market trend. This shift enables more accurate forecasting and proactive mitigation of network congestion.

- Key trends are defined by the convergence of AI and advanced hardware to create more predictive and autonomous systems. The use of digital twin technology is becoming widespread, allowing operators to run simulations that improve grid visibility enhancement and asset health monitoring. For instance, some virtual models have improved congestion forecasting accuracy by up to 15%.

- This trend toward probabilistic forecasting and grid-edge intelligence enables proactive curtailment reduction strategies and more efficient management of peer-to-peer energy trading. The proliferation of grid-forming inverters and modular power flow controllers provides the physical tools for system inertia support and fine-tuned control.

- The shift from centralized to decentralized energy orchestration is driving the growth of virtual power plants (VPPs), with some pilot projects demonstrating a 20% reduction in local congestion.

What challenges does the Grid Congestion Management Systems Industry face during its growth?

- Technological interoperability and the integration of modern solutions with legacy assets represent a key challenge, potentially impeding market growth and slowing digitalization efforts.

- Significant challenges persist, primarily around technological and regulatory hurdles. The integration of modern grid orchestration software with legacy supervisory control and data acquisition (SCADA) systems is a major barrier, often constrained by a lack of interoperability standards. This can increase deployment costs by up to 40%.

- The absence of harmonized regulatory compliance frameworks for market-based redispatching and local flexibility markets slows investment in software-led solutions. Furthermore, the expansion of interconnected devices elevates smart grid cybersecurity risks, requiring robust security protocols for everything from phasor measurement units (PMUs) to behind-the-meter assets.

- A single breach could disrupt autonomous grid operations, making security a paramount concern for maintaining the integrity of the energy transition infrastructure.

Exclusive Technavio Analysis on Customer Landscape

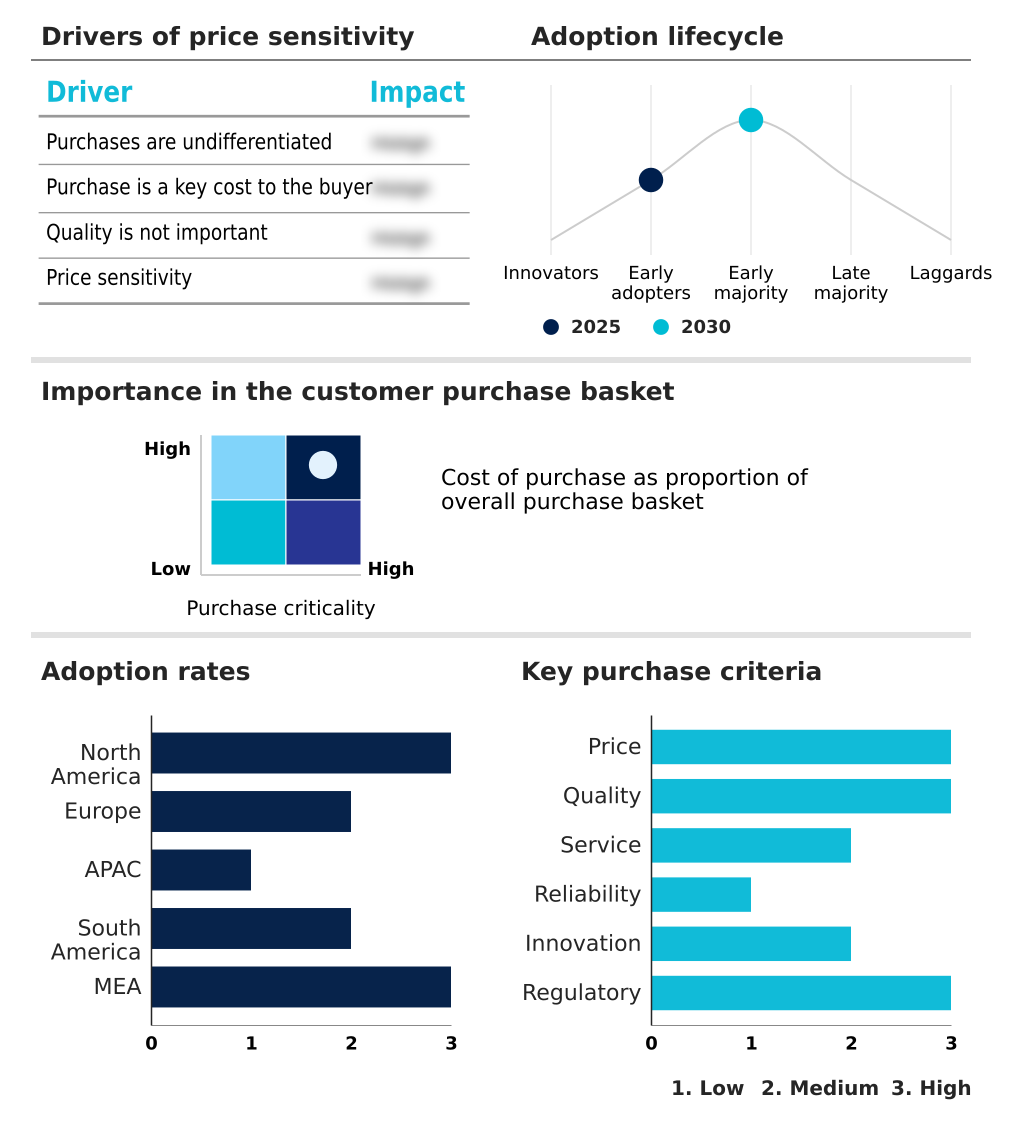

The grid congestion management systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the grid congestion management systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Grid Congestion Management Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, grid congestion management systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Integrated grid management platforms use AI-driven analytics to optimize power flow, enhance stability, and manage distributed energy resources, addressing the complexities of modern electrical networks.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Eaton Corp. Plc

- Emerson Electric Co.

- Enphase Energy Inc.

- GE Vernova Inc.

- Generac Power Systems Inc.

- Hitachi Energy Ltd.

- Honeywell International Inc.

- IBM Corp.

- Itron Inc.

- Landis Gyr AG

- LineVision Inc.

- Mitsubishi Electric Corp.

- Nexans SA

- Open Text Corp.

- Oracle Corp.

- Prysmian S.p.A

- Schneider Electric SE

- Siemens AG

- Tesla Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Grid congestion management systems market

- In August 2024, a regional utility in Australia launched a market-based congestion management pilot utilizing a decentralized platform to incentivize residential battery owners to discharge power during periods of high local network stress.

- In April 2025, a major transmission system operator in California successfully deployed a machine learning-based congestion forecasting module, integrating satellite imagery and localized weather sensor data to reduce solar power curtailment.

- In May 2025, the Federal Energy Regulatory Commission in the United States noted that the lack of standardized compensation for non-wire alternatives remains a significant barrier to private investment in congestion software.

- In May 2025, Schneider Electric released a comprehensive update to its grid orchestration software suite, introducing an autonomous congestion relief module designed to manage the influx of residential electric vehicle charging.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Grid Congestion Management Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 317 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 14% |

| Market growth 2026-2030 | USD 1573.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The grid congestion management systems market is advancing through the integration of sophisticated digital technologies to enhance grid resilience and capacity. Core components such as phasor measurement units (PMUs), advanced distribution management systems (ADMS), and grid orchestration software are becoming standard.

- The deployment of power flow controllers and flexible alternating current transmission systems (FACTS) like static synchronous compensators (STATCOM) and thyristor-controlled series capacitors (TCSC) is critical for managing real-time grid telemetry. For boardroom decisions on capital expenditure, the adoption of digital twin technology is pivotal, as it allows for the simulation of network topology optimization and defers costly physical upgrades.

- This approach has proven to increase transmission capacity by over 20% in certain deployments. As grids incorporate more behind-the-meter assets and smart charging stations, systems like distributed energy resource management systems (DERMS) and virtual power plants (VPPs) are essential.

- Technologies including high-voltage direct current (HVDC), solid-state transformers, and grid-forming inverters are enabling more robust and autonomous grid operations, while remedial action schemes (RAS) and transmission contingency analysis ensure stability.

What are the Key Data Covered in this Grid Congestion Management Systems Market Research and Growth Report?

-

What is the expected growth of the Grid Congestion Management Systems Market between 2026 and 2030?

-

USD 1.57 billion, at a CAGR of 14%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Hardware, and Services), Type (Real-time congestion management, Congestion forecasting and prediction, Market-based congestion management, and Others), End-user (Transmission system operators, Distribution system operators, Utilities and energy retailers, and Renewable energy developers and aggregators) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of variable renewable energy sources, Technological interoperability and legacy asset integration

-

-

Who are the major players in the Grid Congestion Management Systems Market?

-

ABB Ltd., Eaton Corp. Plc, Emerson Electric Co., Enphase Energy Inc., GE Vernova Inc., Generac Power Systems Inc., Hitachi Energy Ltd., Honeywell International Inc., IBM Corp., Itron Inc., Landis Gyr AG, LineVision Inc., Mitsubishi Electric Corp., Nexans SA, Open Text Corp., Oracle Corp., Prysmian S.p.A, Schneider Electric SE, Siemens AG and Tesla Inc.

-

Market Research Insights

- The market is characterized by a dynamic shift toward digitalization to enhance grid resilience and operational efficiency. The adoption of demand response management programs and local flexibility markets allows for active participation from consumers and distributed assets, improving load balancing solutions.

- This move toward decentralized energy orchestration has demonstrated significant results; for example, leveraging flexible industrial loads can reduce peak demand by up to 15%. Furthermore, predictive grid analytics platforms are achieving forecast accuracy rates of over 98% in some regions, substantially improving congestion cost reduction.

- The focus on real-time operational visibility and automated rerouting protocols is central to managing the complexities of modern energy systems and ensuring reliable power delivery.

We can help! Our analysts can customize this grid congestion management systems market research report to meet your requirements.

RIA -

RIA -