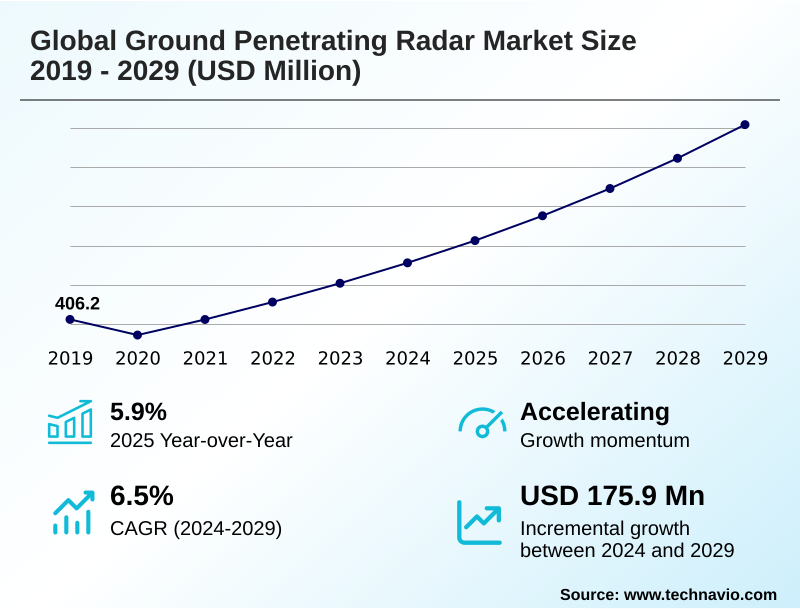

Ground Penetrating Radar Market Size 2025-2029

The ground penetrating radar market size is valued to increase by USD 175.9 million, at a CAGR of 6.5% from 2024 to 2029. Rise in concerns related to safety and protection of underground utilities will drive the ground penetrating radar market.

Major Market Trends & Insights

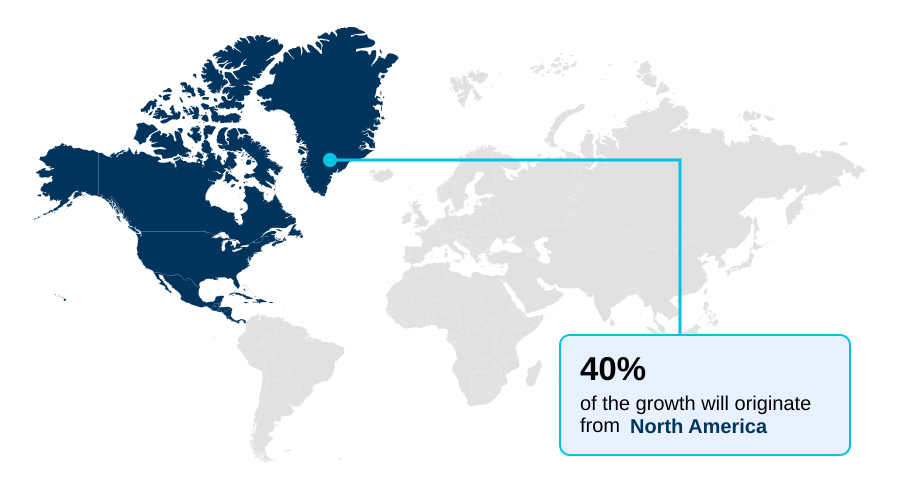

- North America dominated the market and accounted for a 39.5% growth during the forecast period.

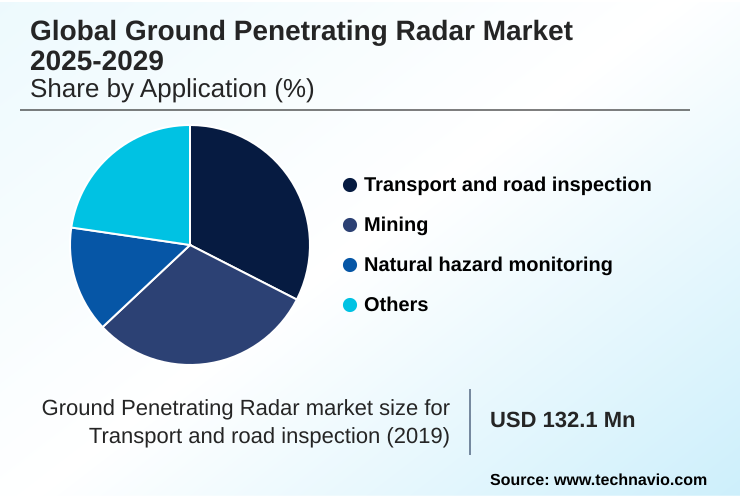

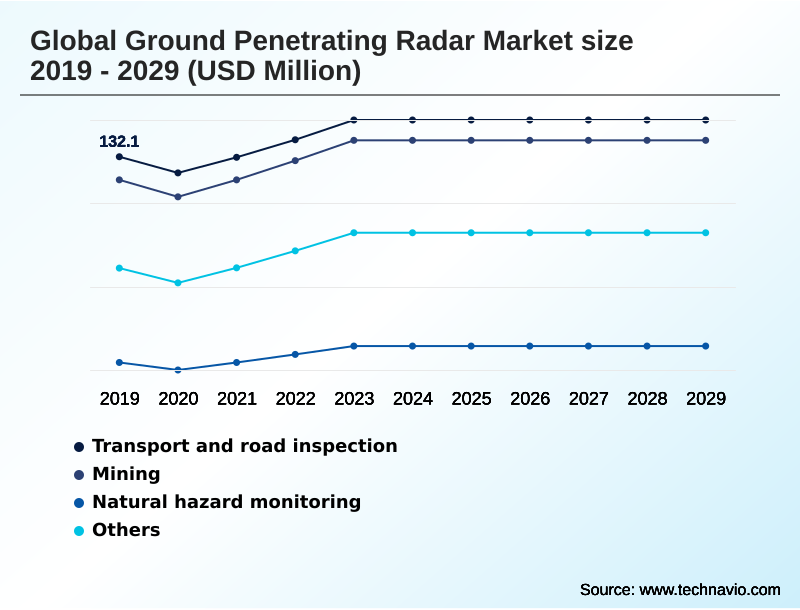

- By Application - Transport and road inspection segment was valued at USD 145.3 million in 2023

- By Type - Cart-based systems segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 247.9 million

- Market Future Opportunities: USD 175.9 million

- CAGR from 2024 to 2029 : 6.5%

Market Summary

- The ground penetrating radar market is defined by its critical role in non-invasive subsurface imaging, a capability essential for modern infrastructure development and management. Growth is fueled by stringent safety regulations and the high cost of accidental utility strikes, pushing industries toward proactive detection methods.

- In construction, for instance, deploying GPR for concrete scanning and utility detection is standard practice to prevent project delays and ensure worker safety, mitigating risks that could otherwise halt operations for weeks.

- Key trends include the integration of AI and machine learning into GPR software platforms for automated data analysis, which reduces the reliance on highly specialized operators and accelerates decision-making. Concurrently, hardware innovations are leading to more portable and powerful systems, such as drone-mounted GPR, expanding applications into previously inaccessible environments.

- However, the market is constrained by the high capital cost of equipment and the persistent need for skilled technicians to interpret complex data, a factor that influences purchasing decisions, particularly for smaller enterprises. The technology's application in geotechnical surveys and environmental assessments further underscores its value in risk management and compliance.

What will be the Size of the Ground Penetrating Radar Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Ground Penetrating Radar Market Segmented?

The ground penetrating radar industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Transport and road inspection

- Mining

- Natural hazard monitoring

- Others

- Type

- Cart-based systems

- Handheld systems

- Vehicle-mounted systems

- Component

- Hardware

- Services

- Software

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Application Insights

The transport and road inspection segment is estimated to witness significant growth during the forecast period.

The transport and road inspection segment is critical, driven by the need for non-destructive testing to ensure infrastructure safety and longevity.

Effective structural health monitoring of transportation networks relies on technologies like GPR for precise pavement analysis and bridge deck assessment. This approach is instrumental in identifying subsurface issues such as void detection, delamination detection, and moisture intrusion before they escalate.

Integrating gpr data interpretation with infrastructure management workflows improves defect identification accuracy by over 15% compared to visual inspection alone.

This use of subsurface mapping is vital for proactive maintenance scheduling, enhancing public safety, and optimizing asset integrity, thereby reducing long-term repair costs and extending the lifecycle of critical transportation assets through advanced condition assessment.

The Transport and road inspection segment was valued at USD 145.3 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ground Penetrating Radar Market Demand is Rising in North America Get Free Sample

North America commands the largest market portion, accounting for nearly 40% of the geographic opportunity, with Europe following at approximately 27%. This dominance is sustained by robust government mandates for infrastructure safety and significant investment in underground asset management.

In the US, projects leveraging subsurface utility engineering with GPR report up to a 20% reduction in planning delays. APAC is an emerging region, where rapid urbanization fuels demand for utility detection and geotechnical surveys.

The application of step-frequency radar and real-time data visualization is becoming more common in these developing markets, supporting complex construction and infrastructure projects and enhancing operational efficiency through superior subsurface diagnostics.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The versatility of ground penetrating radar is evident in its wide array of specialized applications, each demanding distinct technological approaches. For instance, GPR for concrete structure inspection relies on high-frequency antennas for detailed rebar and void detection, whereas GPR applications in mining safety utilize lower frequencies for greater depth penetration to identify geological hazards.

- The debate over comparing GPR and electromagnetic locators continues, though many professionals now favor a combined approach for comprehensive subsurface utility mapping standards. A key differentiator is the multi-frequency GPR antenna benefits, which allow a single system to adapt to various targets, from deep geological strata to shallow utilities like those found with locating plastic pipes with GPR.

- The processing of this complex data is critical; advanced software for GPR data analysis can reduce interpretation time by over 50% compared to manual methods, a vital efficiency gain in large-scale projects like utility mapping with GPR and GIS. For specific tasks, specialized hardware like handheld GPR systems for tight spaces and vehicle-mounted GPR for large-scale surveys offer tailored solutions.

- Innovations in GPR signal processing for noise reduction and automated target recognition in GPR data are making systems more accessible. This is also seen in niche uses such as GPR for railway ballast inspection, assessing bridge deck deterioration with GPR, and using drone-based GPR for hazardous areas.

- Whether detecting voids beneath concrete slabs, conducting non-destructive pavement layer analysis, or exploring GPR techniques for archaeological sites, the technology continues to evolve, with real-time 3D GPR imaging systems setting new standards for subsurface visualization and soil moisture content measurement using GPR opening new environmental applications.

What are the key market drivers leading to the rise in the adoption of Ground Penetrating Radar Industry?

- Heightened concerns regarding the safety and protection of underground utilities serve as a primary market driver, necessitating accurate subsurface detection to prevent damage during excavation activities.

- A primary market driver is the intensified focus on utility strike prevention and managing underground asset management. Regulations mandating subsurface utility engineering before excavation have spurred the adoption of non-destructive testing tools.

- The deployment of vehicle-mounted GPR arrays for large-scale urban mapping projects has increased efficiency by 30% compared to traditional cart-based survey systems. This proactive approach to subsurface inspection services, using techniques like time-domain impulse radar, helps create accurate digital records.

- Integrating this data into digital twin integration frameworks provides a comprehensive view of underground infrastructure, reducing accidental damages and associated service disruptions. This reliance on non-invasive exploration ensures compliance and enhances public safety.

What are the market trends shaping the Ground Penetrating Radar Industry?

- Growing demand within the oil and gas sector for precise subsurface mapping and infrastructure integrity assessment is a notable market trend. It reflects a wider industry shift toward non-destructive methods to improve operational safety and efficiency.

- A significant trend is the expansion of GPR systems in environmental monitoring and geological mapping. The use of drone-mounted GPR systems facilitates rapid surveys over large or inaccessible areas, with adoption rates in this niche growing by nearly 25% year-over-year. This remote sensing technology enables more efficient condition assessment for applications like landfill characterization and contamination plume tracking.

- The integration of advanced signal processing and GIS mapping allows for high-resolution 3D mapping of subsurface geology. This capability improves resource exploration efficiency by providing clearer subsurface diagnostics, a significant advancement over traditional survey methods that improves data accuracy by up to 20%.

What challenges does the Ground Penetrating Radar Industry face during its growth?

- The substantial initial investment required for ground penetrating radar products poses a key challenge, restricting adoption among smaller organizations or for single-use applications.

- A key challenge is the need for specialized expertise in GPR data interpretation, which can limit broader adoption despite hardware advancements in handheld GPR scanners. The complexity of signal attenuation and subsurface anomaly detection requires significant training, presenting a barrier for organizations without dedicated geophysical survey teams.

- While GPR software platforms are evolving with automated feature recognition, effective deployment still relies on skilled operators. The investment in training can be substantial, with firms reporting that it takes up to six months for an operator to become proficient.

- This skills gap is particularly evident in applications requiring nuanced analysis, such as archaeological investigation or forensic investigation, impacting the return on investment for the equipment.

Exclusive Technavio Analysis on Customer Landscape

The ground penetrating radar market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ground penetrating radar market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ground Penetrating Radar Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ground penetrating radar market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Chemring Group Plc - Key offerings include integrated ground penetrating radar systems that provide essential non-destructive subsurface imaging for utility detection, concrete scanning, and geophysical surveys across diverse industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Chemring Group Plc

- Geophysical Survey Systems Inc.

- Geoscanners AB

- Geotech LLC

- Guideline Geo AB

- Hexagon AB

- Hilti Corp.

- IDS GeoRadar Srl

- Leica Geosystems AG

- Lockheed Martin Corp.

- Penetradar Corp.

- Pipehawk Plc

- Radiodetection Ltd.

- Sensors and Software Inc.

- US Radar Inc.

- Utsi Electronics Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ground penetrating radar market

- In September, 2024, Guideline Geo AB announced the launch of its new compact, multi-channel GPR array system, designed to enhance high-resolution 3D data acquisition for utility mapping and archaeological surveys.

- In November, 2024, Hexagon AB revealed a strategic partnership with a leading digital twin software provider to integrate its IDS GeoRadar GPR data streams, aiming to create comprehensive subsurface digital replicas for urban planning.

- In February, 2025, Geophysical Survey Systems Inc. completed the acquisition of a specialized AI software firm to embed advanced machine learning algorithms into its GPR systems for automated target recognition and data interpretation.

- In April, 2025, Radiodetection Ltd. launched a global initiative to standardize GPR operator training and certification, aligning with new international infrastructure safety protocols to improve data quality and consistency.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ground Penetrating Radar Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 291 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.5% |

| Market growth 2025-2029 | USD 175.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 5.9% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ground penetrating radar market is advancing through innovations in hardware and software, fundamentally changing how subsurface investigation is conducted. The adoption of multi-channel antenna arrays enables data collection that is up to 50% faster than single-channel systems, a critical efficiency gain for large-area geotechnical surveys and infrastructure management.

- This shift is driven by the need for more comprehensive non-destructive testing and subsurface utility engineering. Key technologies such as time-domain impulse radar and step-frequency radar are being refined for better performance in challenging environments. The emphasis on improved GPR data interpretation is leading to the integration of AI into control unit designs for real-time imaging and 3D reconstruction.

- Applications are expanding beyond traditional utility detection and concrete scanning to include detailed pavement analysis, bridge deck assessment, and soil stratification. Boardroom decisions are increasingly influenced by the ability of GPR to ensure compliance and mitigate risk, particularly in tasks like rebar mapping and detecting moisture intrusion, void detection, and delamination detection.

- This makes proficiency in electromagnetic wave propagation, signal attenuation, and non-metallic utility locating essential for modern structural health monitoring and archaeological investigation.

What are the Key Data Covered in this Ground Penetrating Radar Market Research and Growth Report?

-

What is the expected growth of the Ground Penetrating Radar Market between 2025 and 2029?

-

USD 175.9 million, at a CAGR of 6.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Transport and road inspection, Mining, Natural hazard monitoring, Others), Type (Cart-based systems, Handheld systems, Vehicle-mounted systems), Component (Hardware, Services, Software) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rise in concerns related to safety and protection of underground utilities, High initial cost of GPR products

-

-

Who are the major players in the Ground Penetrating Radar Market?

-

Chemring Group Plc, Geophysical Survey Systems Inc., Geoscanners AB, Geotech LLC, Guideline Geo AB, Hexagon AB, Hilti Corp., IDS GeoRadar Srl, Leica Geosystems AG, Lockheed Martin Corp., Penetradar Corp., Pipehawk Plc, Radiodetection Ltd., Sensors and Software Inc., US Radar Inc. and Utsi Electronics Ltd.

-

Market Research Insights

- The market's dynamics are shaped by a push for greater operational efficiency and accuracy in subsurface diagnostics. Advanced GPR systems now improve target identification accuracy by over 25% compared to legacy models, directly impacting asset integrity programs.

- Furthermore, the adoption of digital twin integration is accelerating, with firms that incorporate GPR data into project workflows reporting a 40% reduction in planning-stage errors related to underground asset management. This shift toward data-centric methodologies enables more reliable utility strike prevention.

- The market is also seeing a rise in demand for comprehensive subsurface inspection services, moving beyond simple equipment sales to full-service data acquisition and analysis, driven by the need for actionable insights.

We can help! Our analysts can customize this ground penetrating radar market research report to meet your requirements.

RIA -

RIA -