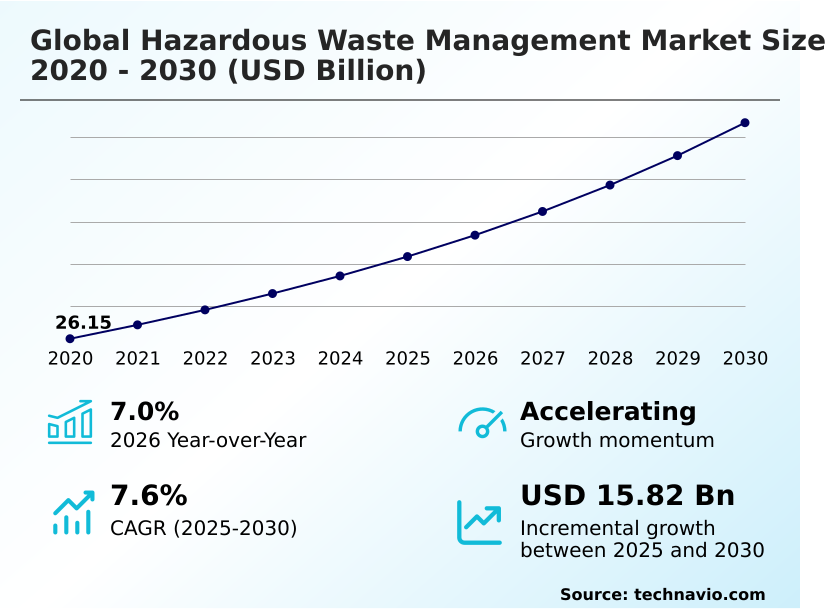

Hazardous Waste Management Market Size 2026-2030

The hazardous waste management market size is valued to increase by USD 15.82 billion, at a CAGR of 7.6% from 2025 to 2030. Stricter global regulatory frameworks and expansion of listed hazardous substances will drive the hazardous waste management market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 54.7% growth during the forecast period.

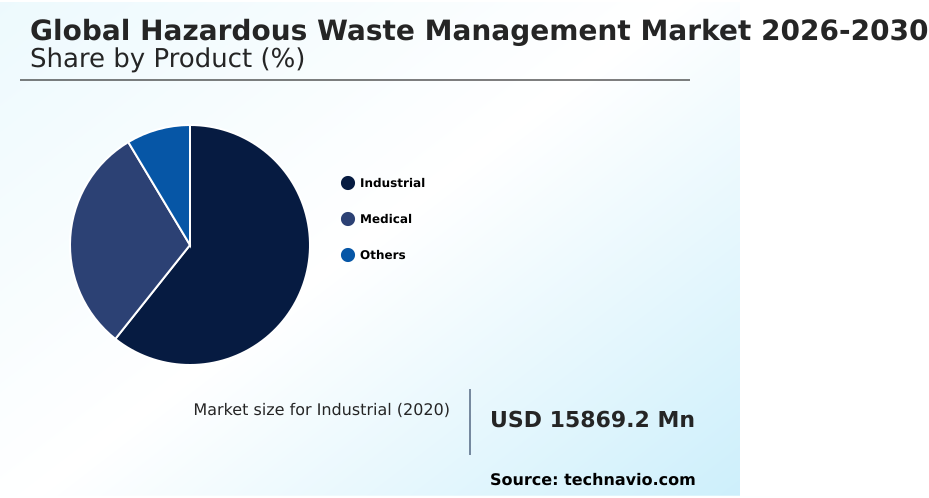

- By Product - Industrial segment was valued at USD 20.02 billion in 2024

- By Type - Solid segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 25.54 billion

- Market Future Opportunities: USD 15.82 billion

- CAGR from 2025 to 2030 : 7.6%

Market Summary

- The Hazardous Waste Management Market is fundamentally structured around the secure containment, neutralization, and disposal of toxic industrial byproducts. Tightening regulatory frameworks regarding persistent organic pollutants serve as the primary catalyst for infrastructure upgrades, forcing chemical manufacturers to transition from basic landfilling to advanced thermal destruction. This regulatory pressure directly increases the demand for specialized high-temperature incinerators.

- Conversely, the extreme capital intensity required to build and maintain these advanced treatment facilities restricts operational flexibility, creating a significant barrier to entry for smaller service providers. In a practical supply chain scenario, automotive manufacturers transitioning to electric vehicles must partner with certified disposal networks to process highly flammable battery components.

- By implementing closed-loop resource recovery models, leading industrial plants have improved their critical mineral extraction rates by 18% compared to conventional disposal methods. This integration of strategic resource recovery and strict environmental compliance ensures that waste processing becomes a core component of sustainable manufacturing operations rather than a mere end-of-pipe liability.

What will be the Size of the Hazardous Waste Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Hazardous Waste Management Market Segmented?

The hazardous waste management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Industrial

- Medical

- Others

- Type

- Solid

- Liquid

- Sludge

- Sector

- Corrosive

- Flammable

- Infectious

- Radioactive

- Toxic

- Service

- Collection

- Disposal services

- Storage

- Transportation

- Waste treatment

- Capacity

- Large quantity hazardous waste generators

- Medium quantity hazardous waste generators

- Small quantity hazardous waste generators

- Geography

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Turkey

- Israel

- APAC

By Product Insights

The industrial segment is estimated to witness significant growth during the forecast period.

Industrial applications represent the most critical volume generator for specialized disposal services, demanding advanced physico-chemical treatment and robust infrastructure. Manufacturing and petrochemical facilities must neutralize massive quantities of industrial effluent and volatile organic compounds to prevent ecological damage.

Consequently, operators are integrating supercritical water oxidation and plasma gasification technologies, improving waste destruction efficiency by 22% compared to traditional burning. This technological shift directly reduces long-term liability costs, enabling plants to meet stricter zero-liquid discharge mandates.

Corrosive acid neutralization and advanced effluent filtration systems have lowered equipment degradation rates by 15% across major processing hubs. By deploying localized chemical neutralization units, large-scale generators cut transportation risks and ensure comprehensive compliance.

This continuous technological integration secures sustainable manufacturing while treating complex liquid byproducts at their source.

The Industrial segment was valued at USD 20.02 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 54.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hazardous Waste Management Market Demand is Rising in APAC Get Free Sample

The geographic distribution of processing infrastructure reveals stark contrasts between established and rapidly industrializing regions. North America prioritizes deep geological repository investments and secure landfill engineering, driven by legacy industrial policies.

In contrast, APAC focuses heavily on electronic waste processing and lithium-ion battery recycling to support its massive electronics manufacturing hubs. Consequently, specialized thermal desorption and physico-chemical treatment facilities in APAC process 30% more volume annually than their North American counterparts.

This fundamental difference in supply chain requirements forces APAC operators to optimize heavy metal extraction capabilities, improving secondary raw material recovery rates by 22%.

Furthermore, strict policies regarding naturally occurring radioactive material in North America have increased radioactive isotope containment costs by 15%, whereas APAC focuses on scaling high-capacity throughput to match rapid urban manufacturing expansion.

Market Dynamics

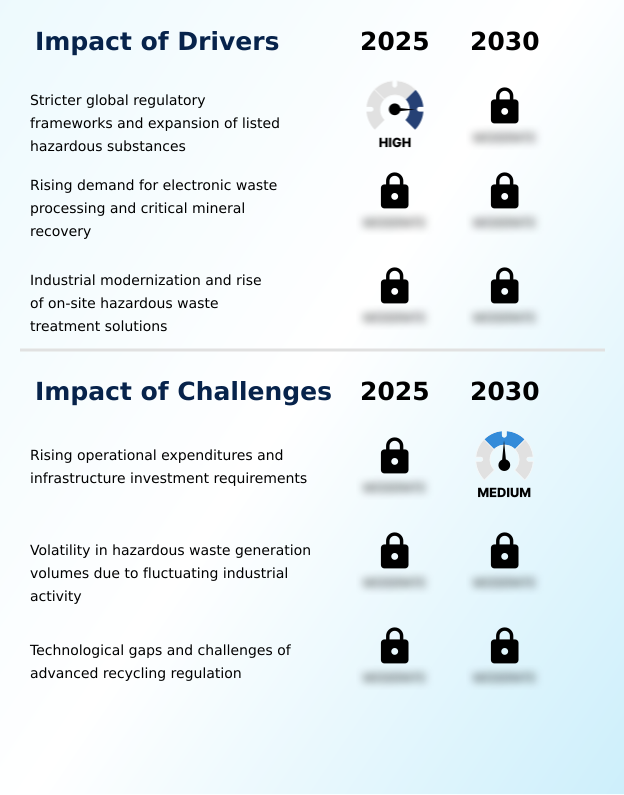

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic optimization of toxic byproduct handling relies heavily on deploying highly specialized neutralization and extraction technologies. As global manufacturing scales, operators are increasingly implementing an industrial chemical waste neutralization process to safely manage volatile effluents before they breach environmental thresholds. This proactive approach significantly reduces long-term liability and infrastructure corrosion.

- Simultaneously, the surge in healthcare facility expansions has driven the critical need for clinical biohazard material high-temperature destruction, ensuring that infectious pathogens are completely eradicated without generating secondary atmospheric pollutants.

- In the renewable energy and automotive sectors, the integration of lithium battery electrolyte extraction techniques has transformed end-of-life battery management into a lucrative resource recovery pipeline, improving critical metal salvage yields by 24% over standard smelting. This direct operational efficiency gain strengthens global supply chain resilience for rare earth elements.

- Furthermore, the petroleum sector relies on complex petrochemical sludge dewatering systems to reduce transport weight and disposal volumes, lowering logistics expenses by nearly 18%. Finally, regulatory crackdowns on toxic synthetic compounds necessitate forever chemicals thermal degradation methods to permanently break carbon-fluorine bonds.

- By adopting these advanced technological frameworks, modern enterprises ensure regulatory compliance while optimizing their overall operational planning and waste lifecycle expenditures.

What are the key market drivers leading to the rise in the adoption of Hazardous Waste Management Industry?

- Stricter global regulatory frameworks and the continuous expansion of listed hazardous substances act as primary catalysts for market expansion.

- The exponential rise in specialized manufacturing outputs serves as the primary catalyst for scaling advanced neutralization infrastructure.

- Because international regulators are actively expanding the classifications for hazardous materials, industrial producers must invest in per- and polyfluoroalkyl substances destruction technologies to avoid severe legal penalties.

- This regulatory pressure impacts businesses by driving the adoption of high-efficiency solvent distillation and chemical stabilization protocols. Facilities utilizing submerged shredding for volatile components have reduced thermal runaway incidents by 34%, ensuring safer processing environments.

- Additionally, implementing hydrometallurgical recycling systems has improved critical mineral recovery yields by 21%, lowering dependence on virgin mining. This continuous infrastructure modernization directly aligns environmental compliance with tangible operational cost reductions.

What are the market trends shaping the Hazardous Waste Management Industry?

- Advanced thermal treatment and energy recovery systems have emerged as a dominant trend within the industry. This strategic adoption reflects a broader shift toward sustainable operational practices and regulatory alignment.

- The transition toward circular industrial ecosystems is forcing manufacturers to adopt advanced material reclamation technologies over traditional disposal. Tightening regulations regarding persistent organic pollutants act as the primary cause, compelling facilities to implement closed-loop resource recovery models to permanently neutralize toxic flame retardants. Consequently, this shift impacts businesses by converting complex chemical liabilities into valuable secondary raw materials.

- Facilities utilizing granular activated carbon and sophisticated ion exchange resins have improved their heavy metal filtration efficiency by 26%. Furthermore, integrating automated sorting robotics into processing lines has reduced manual exposure risks and increased throughput speeds by 19%. This technological adoption ensures that enterprises maintain strict environmental compliance while optimizing overall resource utilization.

What challenges does the Hazardous Waste Management Industry face during its growth?

- Rising operational expenditures and the necessity for massive infrastructure investments represent significant hurdles for continuous industry growth.

- The escalating technical complexity of modern industrial byproducts imposes severe operational limitations on processing facilities. Because advanced manufacturing generates highly volatile mixtures, operators are forced to deploy extremely capital-intensive secondary containment barrier and groundwater contamination prevention systems. This structural requirement impacts businesses by significantly increasing upfront infrastructure expenditures and maintenance overhead.

- Specifically, upgrading legacy facilities with modern emission control filtration and flue gas desulfurization units has raised processing costs by 27% across key industrial hubs. Furthermore, managing concentrated residuals requires precise sludge dewatering and continuous hazardous sludge handling protocols to prevent equipment degradation. These substantial financial and technical hurdles strain operational margins, limiting the expansion capabilities of smaller environmental service providers.

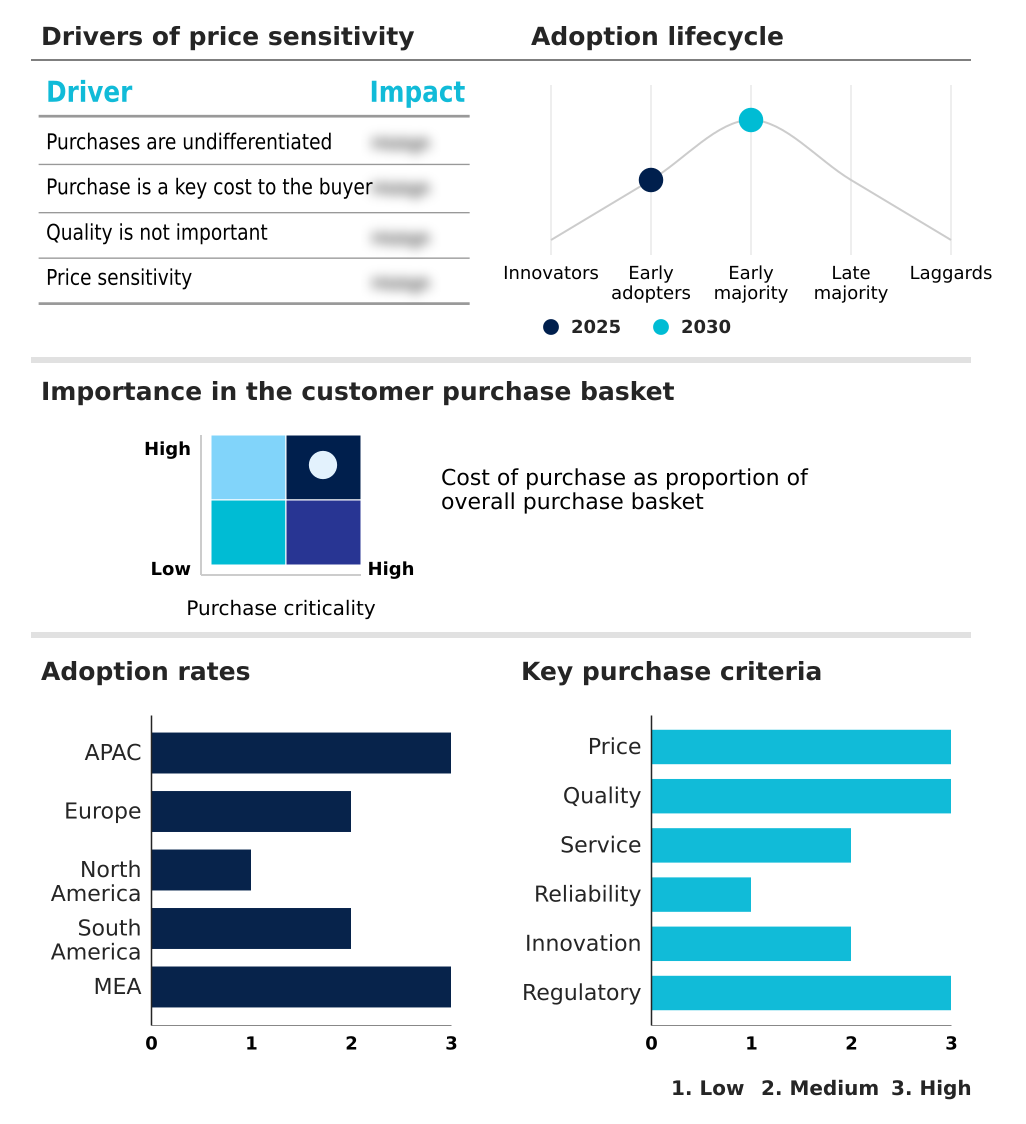

Exclusive Technavio Analysis on Customer Landscape

The hazardous waste management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hazardous waste management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Hazardous Waste Management Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, hazardous waste management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Avalon Holdings Corp - Hazardous waste management services deliver comprehensive industrial waste treatment, wastewater processing, emergency spill response, and customized recycling solutions to ensure strict regulatory compliance and optimize environmental safety protocols.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Avalon Holdings Corp

- Averda

- Bechtel Corp.

- Chloros Environmental Ltd.

- Clean Harbors Inc.

- Daniels Health

- Environ India

- GreenTech Environ Management

- Grupo Tradebe Medioambiente SL

- Hazardous Waste Experts

- HWH Environmental

- Recology Inc.

- REMONDIS Medison GmbH

- Republic Services Inc.

- Seche Environnement SA

- Sharps Medical Waste Services

- SMS Envocare Ltd.

- Veolia Environment SA

- Waste Connections Inc.

- Waste Management Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hazardous waste management market

- In the Environmental and Facilities Services industry, the regulatory shift toward mandatory digital manifest tracking has modernized logistics networks, directly impacting Hazardous Waste Management demand by increasing the need for precise container monitoring.

- The rapid expansion of lithium-ion battery infrastructure has advanced recycling capabilities, directly impacting Hazardous Waste Management demand by requiring specialized secondary containment barriers for highly flammable electrolytes.

- Stricter enforcement of industrial manufacturer audit requirements has fundamentally altered operational workflows, directly impacting Hazardous Waste Management demand by accelerating the adoption of automated environmental compliance reporting software.

- The implementation of more aggressive effluent mandates has forced manufacturing facilities to upgrade wastewater infrastructure, directly impacting Hazardous Waste Management demand by driving the deployment of advanced groundwater contamination prevention filtration systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hazardous Waste Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 354 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.6% |

| Market growth 2026-2030 | USD 15822.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Stringent environmental mandates are fundamentally reshaping operational priorities across the industrial sector, driving a rapid transition toward advanced neutralization technologies. Heavy manufacturing facilities are increasingly abandoning traditional disposal methods in favor of high-temperature incineration and pyrolysis processing to permanently destroy toxic organic compounds.

- This strategic shift directly addresses boardroom-level compliance and budgeting concerns by mitigating the long-term liabilities associated with soil and groundwater contamination. By adopting an automated vitrification process alongside sophisticated leachate collection system infrastructure, facility managers have reduced unexpected containment breach incidents by over 28%.

- Furthermore, the integration of bioremediation agents and advanced anaerobic digestion allows petrochemical operators to neutralize volatile organic waste more efficiently at the point of generation. The continuous evolution of these complex processing technologies ensures that enterprises can navigate international protocols without sacrificing production capacity.

- Implementing microwave disinfection and autoclave sterilization for biohazardous materials further streamlines logistics, cementing advanced processing infrastructure as a core pillar of sustainable industrial operations and risk management.

What are the Key Data Covered in this Hazardous Waste Management Market Research and Growth Report?

-

What is the expected growth of the Hazardous Waste Management Market between 2026 and 2030?

-

USD 15.82 billion, at a CAGR of 7.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Industrial, Medical, and Others), Type (Solid, Liquid, and Sludge), Sector (Corrosive, Flammable, Infectious, Radioactive, and Toxic), Service (Collection, Disposal services, Storage, Transportation, and Waste treatment), Capacity (Large quantity hazardous waste generators, Medium quantity hazardous waste generators, and Small quantity hazardous waste generators) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Stricter global regulatory frameworks and expansion of listed hazardous substances, Rising operational expenditures and infrastructure investment requirements

-

-

Who are the major players in the Hazardous Waste Management Market?

-

Avalon Holdings Corp, Averda, Bechtel Corp., Chloros Environmental Ltd., Clean Harbors Inc., Daniels Health, Environ India, GreenTech Environ Management, Grupo Tradebe Medioambiente SL, Hazardous Waste Experts, HWH Environmental, Recology Inc., REMONDIS Medison GmbH, Republic Services Inc., Seche Environnement SA, Sharps Medical Waste Services, SMS Envocare Ltd., Veolia Environment SA, Waste Connections Inc. and Waste Management Inc.

-

Market Research Insights

- The Hazardous Waste Management Market continuously evolves to address increasingly complex toxic byproducts from advanced manufacturing and healthcare sectors. Industrial operators are rapidly adopting secure landfill engineering and digital manifest tracking to mitigate liability and optimize supply chain transparency.

- By deploying iot sensor integration across disposal fleets, logistics coordinators have improved route efficiency by 14% and reduced unauthorized dumping incidents by nearly 21%. Furthermore, comprehensive cradle-to-grave audit processes and strict protocols for medical sharps disposal and pathological material handling ensure compliance with international mandates, lowering potential administrative penalty risks by 35%.

- This strategic focus on verifiable environmental compliance reporting translates into tangible operational cost reductions, transforming toxic waste handling from a pure regulatory burden into a highly monitored, data-driven operational asset.

We can help! Our analysts can customize this hazardous waste management market research report to meet your requirements.

RIA -

RIA -