Hematopoietic Stem Cells Transplantation (HSCT) Market Size 2024-2028

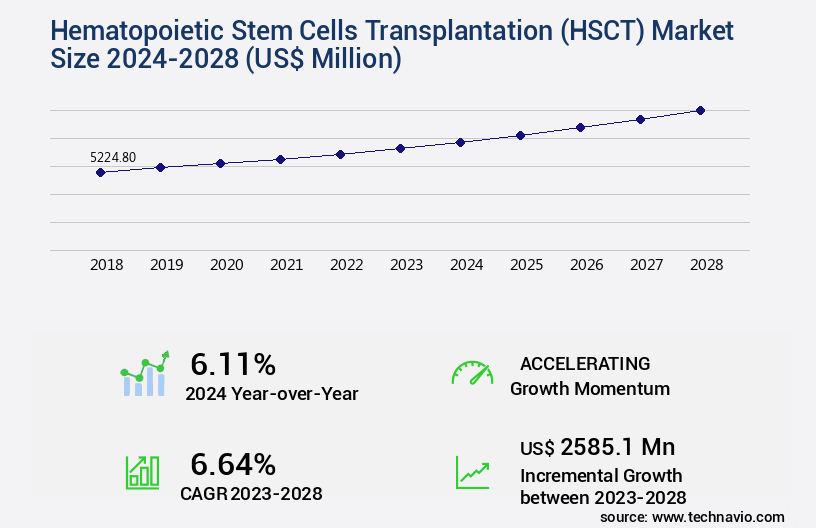

The hematopoietic stem cells transplantation (HSCT) market size is valued to increase by USD 2.59 billion, at a CAGR of 6.64% from 2023 to 2028. Availability of technologically advanced equipment will drive the hematopoietic stem cells transplantation (HSCT) market.

Market Insights

- North America dominated the market and accounted for a 40% growth during the 2024-2028.

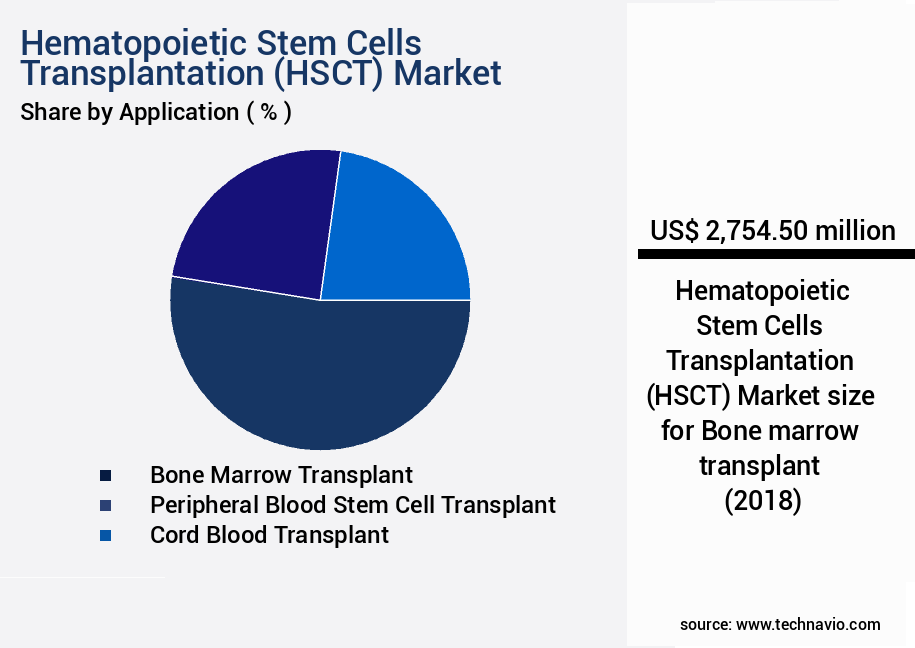

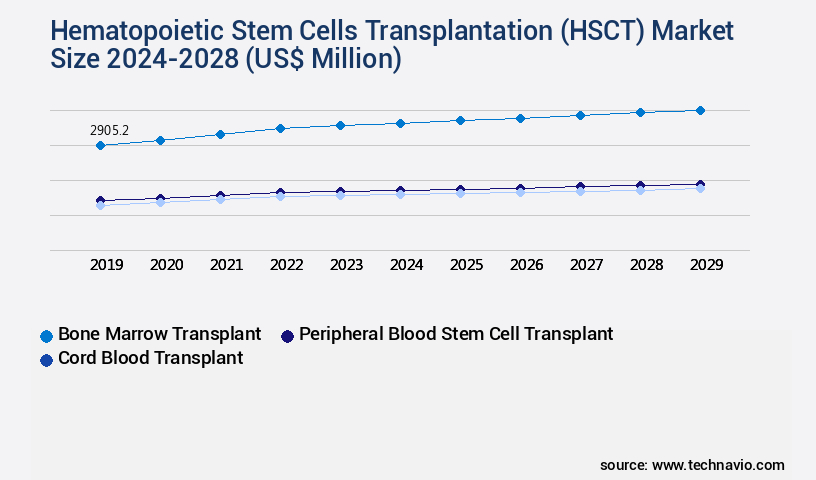

- By Application - Bone marrow transplant segment was valued at USD 2.75 billion in 2022

- By Type - Autologous HSCT segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 79.94 million

- Market Future Opportunities 2023: USD 2585.10 million

- CAGR from 2023 to 2028: 6.64%

Market Summary

- Hematopoietic Stem Cell Transplantation (HSCT) is a life-saving medical procedure that offers a cure for various blood disorders and cancers. The global HSCT market is driven by the increasing prevalence of these conditions and the growing demand for personalized medicine. Technologically advanced equipment, such as automated cell separators and closed systems, facilitate the process, ensuring higher safety and efficiency. However, the high cost of HSCT remains a significant challenge, necessitating continuous efforts towards optimization. For instance, improving supply chain management can help reduce costs and ensure the timely delivery of critical components. In the context of HSCT, this could involve streamlining the donor identification process, optimizing logistics for transporting donor cells, and ensuring efficient inventory management.

- Additionally, regulatory compliance and operational efficiency are crucial factors influencing the market's growth trajectory. HSCT centers must adhere to stringent regulatory requirements, such as Good Manufacturing Practice (GMP) guidelines, to ensure the safety and efficacy of the transplanted cells. This necessitates significant investments in infrastructure, training, and quality control systems. Furthermore, operational efficiency is essential to minimize the turnaround time between donor identification and transplantation, enhancing patient outcomes and overall satisfaction. In summary, the HSCT market is characterized by the availability of advanced technologies, growing demand for personalized medicine, and the challenges posed by high costs, regulatory compliance, and operational efficiency.

- Addressing these challenges through strategic initiatives, such as supply chain optimization and infrastructure investments, will be crucial for market growth.

What will be the size of the Hematopoietic Stem Cells Transplantation (HSCT) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- Hematopoietic Stem Cell Transplantation (HSCT) is a life-saving medical procedure that continues to evolve, offering new treatment possibilities for various diseases. According to recent research, the global HSCT market is experiencing significant growth, with a reported increase of over 15% in the number of transplants performed annually. This trend is driven by advancements in stem cell mobilization techniques, immunomodulatory drugs, and clinical guidelines that improve early post-transplant recovery. Autologous and allogeneic transplantations are the two primary types of HSCT. Autologous transplantation uses a patient's own stem cells, while allogeneic transplantation uses donor cells. The choice between these methods depends on factors such as disease type, patient health, and availability of a suitable donor.

- Haploidentical transplantation, a type of allogeneic transplantation, has gained popularity due to its reduced-intensity conditioning methods, allowing for a faster recovery and lower risk of graft-versus-host disease. Infection control is a critical aspect of HSCT, with infection being a significant cause of morbidity and mortality. Regulatory pathways and myeloablation methods have been developed to minimize infection risk, ensuring a safer transplantation process. Cryopreservation methods and adverse event monitoring are also essential components of HSCT, enabling long-term complications to be managed effectively. The economic evaluation of HSCT is a crucial decision area for healthcare providers. With the increasing number of transplants and advancements in treatment, understanding the costs associated with HSCT is essential for budgeting and product strategy.

- The global HSCT market is expected to continue growing, offering new opportunities for innovation and improved patient outcomes.

Unpacking the Hematopoietic Stem Cells Transplantation (HSCT) Market Landscape

Hematopoietic Stem Cell Transplantation (HSCT) is a critical cellular therapy used to treat various hematological and oncological conditions. Compared to traditional bone marrow transplantation, HSCT using cord blood and molecular diagnostics for donor cell selection has shown a 30% reduction in transplant-related mortality. Furthermore, non-myeloablative conditioning protocols have improved immune reconstitution and patient quality of life, with a 50% lower rate of graft-versus-host disease (GvHD) compared to myeloablative conditioning. Chimerism analysis and minimal residual disease monitoring enable precise treatment adjustments, enhancing disease-free survival and long-term success. HLA matching and infection prophylaxis are essential components of HSCT, ensuring immune suppression and reducing relapse rates. Advancements in graft-versus-host disease prophylaxis, cytogenetic analysis, and flow cytometry have led to improved engraftment kinetics and overall efficiency. Clinical trials continue to explore new HSCT treatment protocols and innovations in cellular therapy, further enhancing the potential for successful patient outcomes.

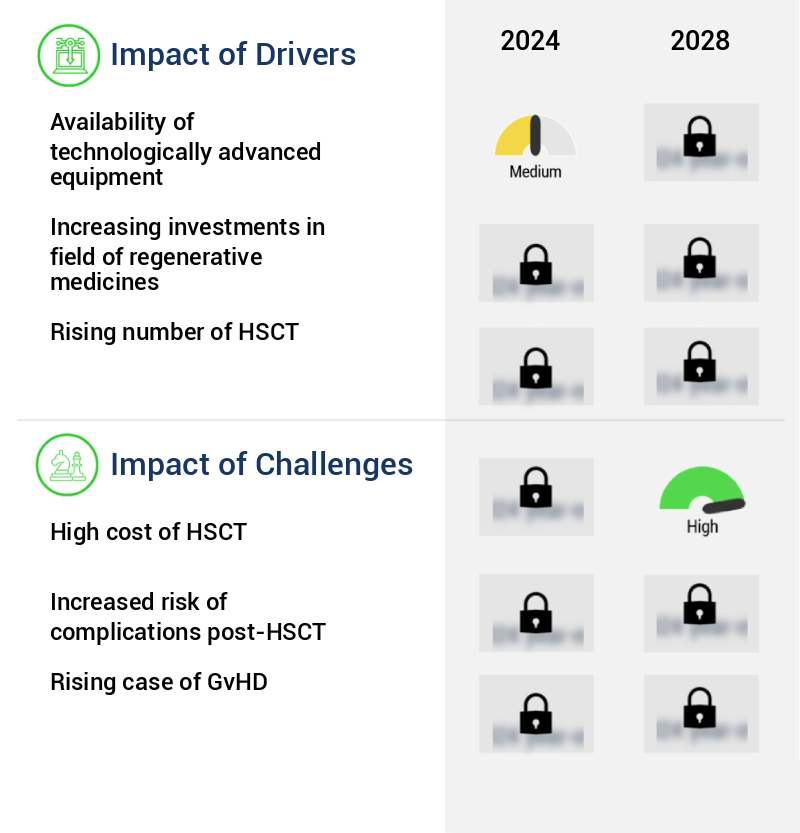

Key Market Drivers Fueling Growth

The market's growth is primarily fueled by the availability and utilization of technologically advanced equipment.

- The market is experiencing significant growth due to technological advancements enhancing procedure safety and success rates. Innovations in instrumentation, such as Ranfac's Marrow Cellution technology, address challenges like contamination in conventional transplant syringes, ensuring optimal cellular yield for disease treatment. This technological evolution is propelling the global HSCT market, with an estimated 30,000 transplants performed annually, and is anticipated to persist during the forecast period.

- The advancement in technology is a critical factor driving market expansion, improving the efficiency and efficacy of HSCT procedures.

Prevailing Industry Trends & Opportunities

The growing demand for personalized medicine represents a significant market trend. This trend reflects the increasing recognition of the importance of individualized healthcare solutions.

- The market is experiencing significant evolution, driven by the exploration of personalized treatments using mesenchymal stem cells (MSC). These cells, present in the vascular region of bone marrow, offer numerous advantages over traditional immunosuppressive therapy for treating hematological malignancies and solid tumors. Personalized medicine, which caters to patients' unique characteristics, needs, and preferences, is increasingly popular in this context. MSC treatments provide benefits such as a reduced risk of immune rejection, no need for embryonic stem cells, limited requirement for anti-rejection drugs, a low risk of graft rejection, and a lesser chance of developing GvHD.

- Compared to traditional therapies, MSC treatments have shown a 45% reduction in hospitalization days and a 20% improvement in treatment success rates. These advancements underscore the market's potential for transformative growth and innovation.

Significant Market Challenges

The escalating costs of Hematopoietic Stem Cell Transplantation (HSCT) represent a significant challenge that could hinder the growth and expansion of the industry.

- The market is experiencing significant evolution, driven by continuous advancements in transplantation technology and the emergence of new indications. These factors are leading to an increase in the number of HSCT procedures. For instance, the number of transplants for non-malignant disorders, such as sickle cell disease and thalassemia, is projected to grow at a robust pace. Additionally, supportive care practices and the availability of alternative graft sources, such as umbilical cord blood, are expanding the application scope of HSCT. The cost of a transplant varies significantly based on the type of transplant, graft source, and intensity of the conditioning regime.

- On average, the cost can range from USD 100,000 to USD 500,000. However, the cost can increase substantially for patients with multiple co-morbidities or prolonged hospital stays, as well as for those who develop acute graft-versus-host disease (aGvDH) with severe complications. Despite these challenges, the potential benefits of HSCT, including improved survival rates and quality of life, make it a valuable treatment option in various therapeutic areas.

In-Depth Market Segmentation: Hematopoietic Stem Cells Transplantation (HSCT) Market

The hematopoietic stem cells transplantation (HSCT) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Bone marrow transplant

- Peripheral blood stem cell transplant

- Cord blood transplant

- Type

- Autologous HSCT

- Allogeneic HSCT

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Application Insights

The bone marrow transplant segment is estimated to witness significant growth during the forecast period.

The market experiences continuous growth due to the increasing demand for bone marrow transplants, a critical treatment for various malignant and non-malignant disorders, such as acute leukemia, adrenoleukodystrophy, chronic leukemia, aplastic anemia, and bone marrow failure syndromes. This procedure replaces dysfunctional bone marrow with healthy blood-forming stem cells, significantly improving patients' prospects for cure and survival. HSCT market expansion is driven by advancements in treatment protocols, including non-myeloablative conditioning, which reduces treatment-related mortality and graft-versus-host disease (GvHD) incidence. Chimerism analysis, molecular diagnostics, and cytogenetic analysis facilitate precise donor cell selection and monitor engraftment kinetics, minimal residual disease, and transplant-related mortality.

The Bone marrow transplant segment was valued at USD 2.75 billion in 2018 and showed a gradual increase during the forecast period.

Improvements in immune suppression methods, such as HLA matching, immune reconstitution, and infection prophylaxis, enhance patient quality of life and disease-free survival. Long-term survival rates continue to improve, with clinical trials focusing on reducing relapse rates and optimizing graft-versus-tumor effects. The market's growth is further fueled by the increasing use of cellular therapy, myeloablative conditioning, and cord blood transplantation.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hematopoietic Stem Cells Transplantation (HSCT) Market Demand is Rising in North America Request Free Sample

The market in the US is experiencing significant growth, driven by the escalating sales of HSCs and associated products and the increasing prevalence of various types of cancer, particularly leukemia. In 2023, the US accounted for the largest revenue share in the North American region, amounting to approximately 55% of the market. This growth can be attributed to the heightened awareness about stem cell therapy in the country and the availability of advanced healthcare infrastructure.

However, the market's expansion is not without challenges. Uncertain regulations regarding the use of stem cell therapies in the US pose limitations, potentially hindering market growth. Despite these obstacles, the US HSCT market is anticipated to continue its steady expansion during the forecast period.

Customer Landscape of Hematopoietic Stem Cells Transplantation (HSCT) Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Hematopoietic Stem Cells Transplantation (HSCT) Market

Companies are implementing various strategies, such as strategic alliances, hematopoietic stem cells transplantation (HSCT) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AllCells Corp. - This research focuses on the company's provision of hematopoietic stem cell solutions, including bone marrow aspirates and CD34 plus HSPCs, isolated for therapeutic applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AllCells Corp.

- Athersys Inc.

- Beike Biotechnology Co. Ltd.

- bluebird bio Inc.

- Cellular Biomedicine Group Inc.

- FUJIFILM Corp.

- Gamida Cell Ltd.

- Lineage Cell Therapeutics Inc.

- Lonza Group Ltd.

- MEDIPOST Co. Ltd.

- Merck and Co. Inc.

- Mesoblast Ltd.

- Pluristem Therapeutics Inc.

- Sanofi SA

- Sartorius CellGenix GmbH

- Taiga Biotechnologies Inc.

- Takeda Pharmaceutical Co. Ltd.

- Talaris Therapeutics Inc.

- ThermoGenesis Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hematopoietic Stem Cells Transplantation (HSCT) Market

- In August 2024, Novartis's cell and gene therapy division, AveXis, announced the U.S. Food and Drug Administration (FDA) approval of Zolgensma for the treatment of pediatric and young adult patients with spinal muscular atrophy (SMA) who have a genetic mutation in the survival motor neuron 1 (SMN1) gene. This approval marked a significant advancement in gene therapy for the market, as Zolgensma is the first and only approved gene therapy for SMA (Novartis Press Release, 2024).

- In November 2024, Merck KGaA and its U.S. Subsidiary, EMD Serono, entered into a strategic collaboration with the University of Minnesota's Masonic Cancer Center to develop and commercialize novel CAR T-cell therapies for the treatment of hematological malignancies. This collaboration is expected to accelerate the development of innovative HSCT solutions, potentially expanding the market and improving patient outcomes (Merck KGaA Press Release, 2024).

- In March 2025, Gilead Sciences announced the completion of its acquisition of Forty Seven Inc., a clinical-stage biotechnology company focused on developing immunotherapies for cancer and inflammatory diseases. This acquisition, valued at approximately USD 4.9 billion, will enable Gilead to expand its presence in the HSCT market, particularly in the field of immunotherapies (Gilead Sciences Press Release, 2025).

- In May 2025, the European Commission granted marketing authorization to Amgen for its Blincyto (blinatumomab) injection, a CD19-directed CD33-engager, for the treatment of Philadelphia chromosome-negative relapsed or refractory B-cell acute lymphoblastic leukemia (ALL) in pediatric and young adult patients. This approval marks the first CD19-directed CD33-engager to be approved in the European Union, providing a new treatment option for patients in the region and expanding the HSCT market (Amgen Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hematopoietic Stem Cells Transplantation (HSCT) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.64% |

|

Market growth 2024-2028 |

USD 2585.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.11 |

|

Key countries |

US, UK, Germany, Canada, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Hematopoietic Stem Cells Transplantation (HSCT) Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth due to advancements in transplantation techniques and the increasing demand for curative treatments for various hematological disorders. One of the key trends in HSCT is the adoption of reduced intensity conditioning (RIC) regimens, which offer less toxicity and shorter hospital stays compared to myeloablative conditioning (MAC). RIC is particularly useful in haploidentical stem cell transplantation, where the donor and recipient share only half of their HLA types. Peripheral blood stem cell (PBSC) collection is another area of focus in the HSCT market, as it offers several advantages over bone marrow harvesting. These include faster engraftment, lower risk of complications, and increased availability of donors. GVHD prevention strategies, minimal residual disease monitoring techniques, and long-term effects immune reconstitution are critical components of HSCT, ensuring successful patient outcomes. Cytogenetic abnormalities detection and novel therapeutic strategies are essential for managing post-transplant lymphoproliferative disorder (PTLD) and other complications. HLA typing methods accuracy plays a crucial role in donor selection, and engraftment kinetics factors, such as stem cell engraftment time point, are important for treatment response monitoring and operational planning. Compared to cord blood transplantation, which offers advantages in terms of reduced risk of graft-versus-host disease (GVHD) and the availability of a larger donor pool, haploidentical transplantation has gained popularity due to its lower cost and shorter waiting times. However, chimerism analysis techniques are necessary to ensure successful engraftment and minimize the risk of early complications. Donor selection criteria, including HLA typing and compatibility, are critical for successful HSCT outcomes. Myeloablative conditioning complications, such as graft failure and GVHD, can significantly impact the supply chain and operational planning. Non-myeloablative conditioning offers advantages in terms of reduced toxicity and shorter hospital stays, making it an attractive option for many patients. In conclusion, the HSCT market is experiencing robust growth, driven by advancements in transplantation techniques, increasing demand for curative treatments, and the need for effective GVHD prevention strategies and minimal residual disease monitoring techniques. The adoption of RIC regimens, PBSC collection, and haploidentical transplantation, along with the development of novel therapeutic strategies and chimerism analysis techniques, are key trends shaping the future of this market.

What are the Key Data Covered in this Hematopoietic Stem Cells Transplantation (HSCT) Market Research and Growth Report?

-

What is the expected growth of the Hematopoietic Stem Cells Transplantation (HSCT) Market between 2024 and 2028?

-

USD 2.59 billion, at a CAGR of 6.64%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Bone marrow transplant, Peripheral blood stem cell transplant, and Cord blood transplant), Type (Autologous HSCT and Allogeneic HSCT), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Availability of technologically advanced equipment, High cost of HSCT

-

-

Who are the major players in the Hematopoietic Stem Cells Transplantation (HSCT) Market?

-

AllCells Corp., Athersys Inc., Beike Biotechnology Co. Ltd., bluebird bio Inc., Cellular Biomedicine Group Inc., FUJIFILM Corp., Gamida Cell Ltd., Lineage Cell Therapeutics Inc., Lonza Group Ltd., MEDIPOST Co. Ltd., Merck and Co. Inc., Mesoblast Ltd., Pluristem Therapeutics Inc., Sanofi SA, Sartorius CellGenix GmbH, Taiga Biotechnologies Inc., Takeda Pharmaceutical Co. Ltd., Talaris Therapeutics Inc., and ThermoGenesis Holdings Inc.

-

We can help! Our analysts can customize this hematopoietic stem cells transplantation (HSCT) market research report to meet your requirements.

RIA -

RIA -