High Protein-based Food Market Size 2026-2030

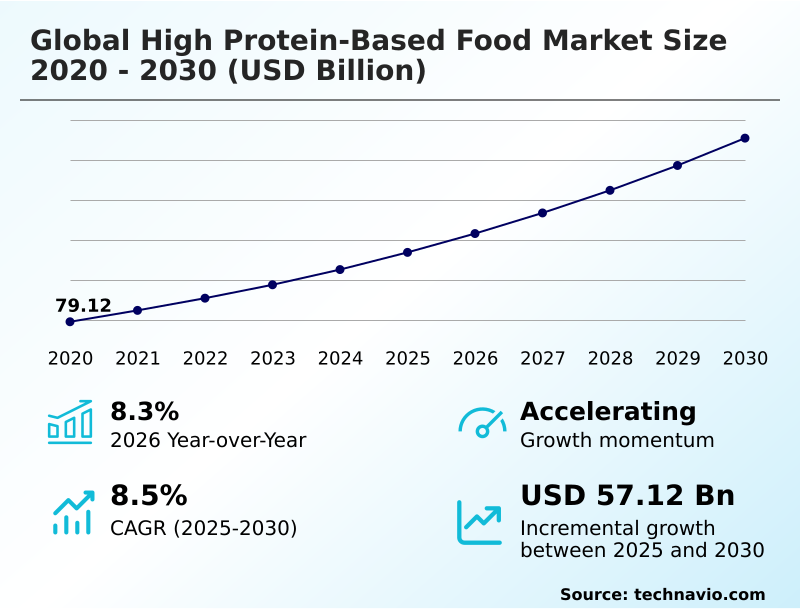

The high protein-based food market size is valued to increase by USD 57.12 billion, at a CAGR of 8.5% from 2025 to 2030. Rising demand for metabolic health and body composition optimization will drive the high protein-based food market.

Major Market Trends & Insights

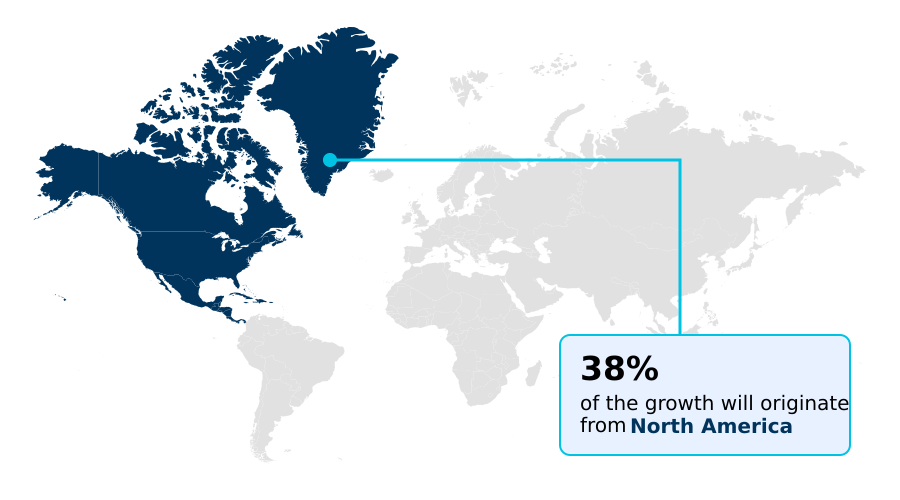

- North America dominated the market and accounted for a 38.3% growth during the forecast period.

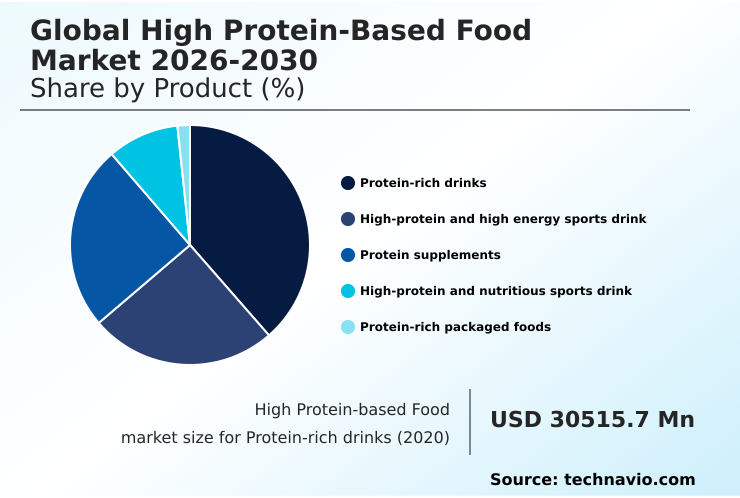

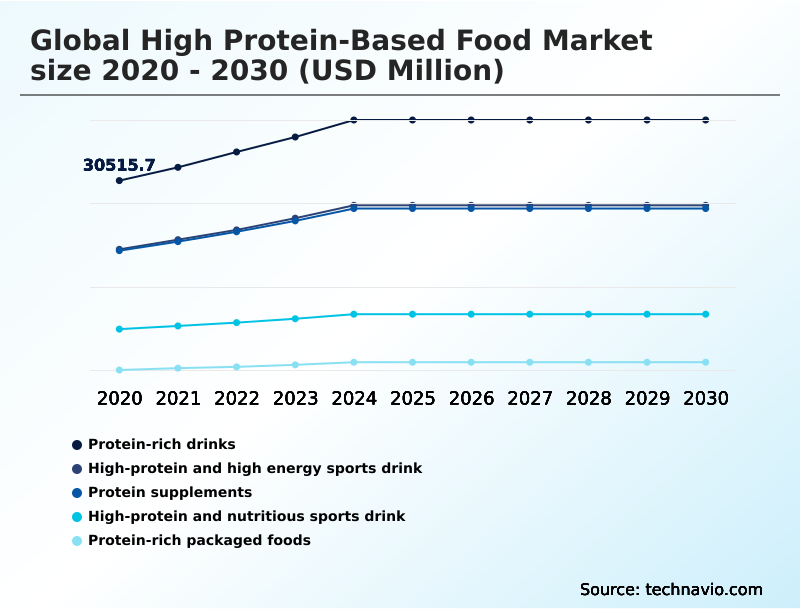

- By Product - Protein-rich drinks segment was valued at USD 39.85 billion in 2024

- By Distribution Channel - Offline channel segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 91.81 billion

- Market Future Opportunities: USD 57.12 billion

- CAGR from 2025 to 2030 : 8.5%

Market Summary

- The High Protein-Based Food Market is undergoing a significant transformation, driven by a global shift towards functional nutrition and proactive health management. Consumers now prioritize dietary protein for its role in muscle maintenance, metabolic regulation, and achieving satiety, moving beyond its traditional association with athletic performance.

- This has spurred innovation across the industry, with a focus on developing a diverse range of products.

- One key business scenario involves the reformulation of mass-market snacks; a food conglomerate, for instance, might re-engineer a popular biscuit line to include a fortified food matrix with a plant-based protein blend, aiming to improve its nutritional profile without altering the taste consumers expect. This requires overcoming technical hurdles in high-protein extrusion and implementing effective flavor masking technology.

- The market is also characterized by the growing demand for clean-label protein source options and sustainable protein production methods, compelling companies to innovate in areas like precision fermentation protein and mycoprotein texturization to meet evolving consumer and regulatory expectations.

What will be the Size of the High Protein-based Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the High Protein-based Food Market Segmented?

The high protein-based food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Protein-rich drinks

- High-protein and high energy sports drink

- Protein supplements

- High-protein and nutritious sports drink

- Protein-rich packaged foods

- Distribution channel

- Offline channel

- Online channel

- Source

- Animal-based

- Plant-based

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- North America

By Product Insights

The protein-rich drinks segment is estimated to witness significant growth during the forecast period.

The protein-rich drinks segment is rapidly evolving beyond niche applications, targeting mainstream consumers with ready-to-consume formats that emphasize convenience.

A key focus is improving the sensory experience, with significant R&D dedicated to advanced flavor masking technology and texture modification agent use to create a smoother mouthfeel in shelf-stable protein beverage options.

Formulations are increasingly clean-label, featuring non-GMO protein isolate and other premium ingredients. These products, often positioned as a high-protein meal replacement or a functional protein beverage, cater to busy lifestyles.

Innovations in enzymatic protein modification have improved digestibility in some offerings by over 15%, enhancing amino acid bioavailability. The goal is to provide a nutritionally dense, convenient boost without compromising on taste, appealing to a broad consumer base.

The Protein-rich drinks segment was valued at USD 39.85 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How High Protein-based Food Market Demand is Rising in North America Get Free Sample

The geographic landscape is marked by rapid growth in APAC, which is projected to contribute nearly 27% of the global market's incremental growth, driven by rising health awareness in countries like China and India.

Formulations using a clean-label protein source and sustainable protein production methods are gaining traction globally.

In North America, which accounts for over 38% of market share, the demand for grass-fed dairy protein and products supporting a keto-friendly protein snack trend is robust.

European markets show a strong preference for non-GMO protein isolate and products with transparent sourcing, with some manufacturers achieving a 10% reduction in supply chain waste through localized plant protein extraction.

The focus on nutritional density optimization is a universal driver, influencing product development worldwide.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The High Protein-Based Food Market is increasingly shaped by specific consumer inquiries and sophisticated nutritional goals. The debate over whey vs casein for muscle growth continues to drive segmentation in sports nutrition, while concerns about pea protein vs soy protein taste influence plant-based product development.

- Consumers seeking the best protein powder for weight loss are a significant driver for innovation in satiety-inducing formulations. The market is also expanding to address specific health needs, creating demand for high-protein snacks for diabetics and clarifying how to increase protein intake without meat.

- Functional benefits are also a key focus, with strong interest in the benefits of collagen for joint health and the role of protein in sarcopenia prevention. The demand for transparency is pushing manufacturers to focus on clean label protein bar ingredients and offer more lactose-free protein shake options.

- Sustainability is another critical factor, with a growing emphasis on sustainable plant-based protein sources. In response, food scientists are exploring advances in precision fermentation for protein, which promises higher efficiency than traditional methods. As demographic needs shift, understanding protein requirements for elderly adults and developing high-protein breakfast ideas for kids have become important R&D areas.

- Formulators also face technical hurdles, such as the challenges of formulating high-protein beverages and making protein shakes taste better. The diversification is evident as protein fortification in baked goods becomes more common, requiring a deep understanding of consumer trends in protein consumption.

- Furthermore, navigating the regulatory landscape for novel proteins is critical for market entry, where companies with streamlined compliance processes are showing a 20% faster time-to-market compared to competitors.

What are the key market drivers leading to the rise in the adoption of High Protein-based Food Industry?

- The rising consumer demand for solutions promoting metabolic health and optimizing body composition serves as a key driver for the market.

- A fundamental driver is the growing consumer understanding of macronutrients, spurring demand for satiety-inducing formulation and products that support a high muscle protein synthesis rate.

- This scientific literacy has expanded the market beyond athletes to include those focused on weight management and healthy aging, leading to a 35% growth in the geriatric nutrition food segment.

- The diversification of protein sources, from traditional grass-fed dairy protein to innovative precision fermentation protein, allows manufacturers to cater to varied dietary preferences.

- The demand for convenience is met with products like the shelf-stable protein beverage, with data showing that portable formats can increase consumption frequency by up to 50%. This drive for accessibility and functional benefits is a cornerstone of market expansion.

What are the market trends shaping the High Protein-based Food Industry?

- A prominent market trend is the integration of high-protein formulations into nostalgic and traditional breakfast staples. This bridges the gap between indulgent taste and functional nutrition for health-conscious consumers.

- A transformative trend is the adoption of next-generation sustainable ingredients, including algae-based protein source and insect protein bar options, which are gaining consumer acceptance. This shift is driven by a desire for environmentally friendly nutrition and is supported by advancements in cellular agriculture protein.

- The mainstreaming of these novel sources is evident as some retail chains report that products featuring a fermented protein ingredient have seen a 25% increase in repeat purchases. The market is also seeing a surge in specialized products like protein-enriched pasta and high-protein baking flour, which allow for seamless nutritional enhancement of everyday meals.

- This integration strategy improves consumer adoption by over 40% compared to products requiring new habits. The expansion of dairy-free protein drink and low-carb protein food categories further diversifies the market.

What challenges does the High Protein-based Food Industry face during its growth?

- Volatility in the cost of raw materials and the need for supply chain stabilization present a key challenge affecting industry growth.

- A primary challenge is balancing nutritional goals with sensory appeal, particularly in products with high concentrations of whey protein isolate or certain plant-based protein blend options. Formulators invest heavily in flavor masking technology, which can increase production costs by up to 15%.

- Another hurdle is navigating the complex supply chain for specialized ingredients like hydrolyzed collagen peptides and casein micellar structure components, where disruptions have led to lead time increases of 20%. Ensuring high amino acid bioavailability while maintaining a clean-label protein source presents a continuous technical challenge.

- The development of a viable plant-based meat alternative with the right texture and taste remains a high-stakes R&D focus for many companies, requiring mastery of high-protein extrusion and mycoprotein texturization.

Exclusive Technavio Analysis on Customer Landscape

The high protein-based food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the high protein-based food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of High Protein-based Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, high protein-based food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Delivering therapeutic nutrition and performance-focused protein powders, including high-protein shakes and specialized drinks, to support diverse health and wellness objectives.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Archer Daniels Midland Co.

- Beyond Meat Inc.

- Cargill Inc.

- Chobani Global Holdings LLC

- Conagra Brands Inc.

- Danone SA

- General Mills Inc.

- Hormel Foods Corp.

- Kellanova

- Maple Leaf Foods Inc.

- Mars Inc.

- Mondelez International Inc.

- Nestle SA

- PepsiCo Inc.

- The Campbell Co.

- The Coca Cola Co.

- The Kraft Heinz Co.

- Tyson Foods Inc.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in High protein-based food market

- In May, 2025, Danone SA, through its North American division, introduced a new line of Oikos brand shelf-stable protein shakes, each formulated with thirty grams of protein.

- In May, 2025, a European Union regulatory body issued a directive that streamlined the commercial approval process for insect-based protein isolates in food applications.

- In March, 2025, a California-based food technology firm announced the nationwide commercial launch of its precision-fermented dairy protein, offering an alternative to traditional whey.

- In February, 2025, General Mills Inc. expanded its Nature Valley snack line with savory nut bars featuring increased protein content to meet consumer demand for high-satiety options.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled High Protein-based Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.5% |

| Market growth 2026-2030 | USD 57119.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.3% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Australia, Brazil, Argentina, Chile, South Africa, UAE, Saudi Arabia, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The High Protein-Based Food Market is defined by intense innovation aimed at improving the nutritional density and sensory appeal of food products. Key developments center on the sourcing and processing of ingredients, with significant investment in whey protein isolate and ultra-filtered milk protein for superior purity.

- The industry is also advancing mycoprotein texturization and high-protein extrusion techniques to create more palatable plant-based alternatives. A core boardroom-level focus is aligning product portfolios with consumer demand for a clean-label protein source and sustainable protein production, influencing budgeting for R&D in areas like enzymatic protein modification.

- Success hinges on mastering flavor masking technology and selecting the right texture modification agent to create appealing products. Formulations are increasingly complex, incorporating bioactive peptides and hydrolyzed collagen peptides to offer targeted health benefits beyond basic nutrition. This technical sophistication is demonstrated by a 30% improvement in amino acid bioavailability in next-generation products.

- The evolution of the fortified food matrix and plant protein extraction methods is pivotal for creating allergen-free protein and non-GMO protein isolate options that meet stringent consumer expectations.

What are the Key Data Covered in this High Protein-based Food Market Research and Growth Report?

-

What is the expected growth of the High Protein-based Food Market between 2026 and 2030?

-

USD 57.12 billion, at a CAGR of 8.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Protein-rich drinks, High-protein and high energy sports drink, Protein supplements, High-protein and nutritious sports drink, and Protein-rich packaged foods), Distribution Channel (Offline channel, and Online channel), Source (Animal-based, and Plant-based) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising demand for metabolic health and body composition optimization, Volatility in raw material costs and supply chain stabilization

-

-

Who are the major players in the High Protein-based Food Market?

-

Abbott Laboratories, Archer Daniels Midland Co., Beyond Meat Inc., Cargill Inc., Chobani Global Holdings LLC, Conagra Brands Inc., Danone SA, General Mills Inc., Hormel Foods Corp., Kellanova, Maple Leaf Foods Inc., Mars Inc., Mondelez International Inc., Nestle SA, PepsiCo Inc., The Campbell Co., The Coca Cola Co., The Kraft Heinz Co., Tyson Foods Inc. and Unilever PLC

-

Market Research Insights

- Market dynamics are defined by a shift toward functional convenience and personalized nutrition. The demand for products like a high-protein meal replacement and post-workout recovery drink is expanding beyond athletes, with adoption rates among general wellness consumers increasing by over 20% in some demographics. This is driving innovation in formats such as the ready-to-drink protein shake and protein bar formulation.

- Foodservice providers incorporating protein fortification ingredient options into menus have reported a 15% rise in sales of specific health-oriented dishes. Furthermore, the development of specialized products for medical nutrition therapy and geriatric nutrition food is creating new high-value segments, with formulations optimized for specific health outcomes showing a 2:1 preference over unfortified alternatives in clinical settings.

We can help! Our analysts can customize this high protein-based food market research report to meet your requirements.

RIA -

RIA -