Immunoglobulin Products Market Size 2024-2028

The immunoglobulin products market size is forecast to increase by USD 9.7 billion at a CAGR of 10.11% between 2023 and 2028.

- The market is experiencing significant growth driven by advancements in biotechnology and manufacturing processes, enabling the production of more effective and targeted therapies. However, this market is not without challenges, primarily the high cost of immunoglobulin therapies, which limits accessibility for many patients and presents a significant barrier to entry for new market entrants. These high costs are due to the complex production processes and the need for large-scale facilities, which require substantial investments. Despite these challenges, the market presents numerous opportunities for companies seeking to capitalize on the growing demand for immunoglobulin therapies.

- The increasing prevalence of chronic diseases, such as primary immunodeficiency disorders and autoimmune diseases, is driving the need for more effective and accessible therapies. Additionally, the development of biosimilars and the entry of new market players are expected to increase competition and drive down prices, making therapies more accessible to a broader patient population. Companies that can effectively navigate the challenges of high production costs and regulatory requirements while delivering innovative and cost-effective solutions will be well-positioned to capitalize on the growing demand for immunoglobulin therapies.

What will be the Size of the Immunoglobulin Products Market during the forecast period?

- The market encompasses a range of therapeutic areas, including multiple sclerosis, health outcomes research, and digital health. Patient safety is a significant focus, with applications in immune thrombocytopenia, human immunodeficiency virus, and clinical trial endpoints. Kawasaki disease, hepatitis B, Crohn's disease, ulcerative colitis, rheumatoid arthritis, and patient-centered care are other key areas. Biosimilar approval pathways, remote patient monitoring, and value-based healthcare are driving market trends. Immunoglobulin M, immune deficiency disorders, immunoglobulin D, x-linked agammaglobulinemia, antibody deficiency, myasthenia gravis, antiviral therapy, infective endocarditis, anti-infective therapy, biosimilar development, genetic engineering, anti-fungal therapy, and the biopharmaceutical industry are integral components of this dynamic market.

- Drug safety, clinical trial design, targeted drug delivery, systemic lupus erythematosus, and various immune disorders continue to shape market evolution. Immunoglobulin G, guillain-barré syndrome, post-transplant immunosuppression, antibody-drug conjugates, and hepatitis C are also significant areas of interest. The market is underpinned by advancements in technology, regulatory frameworks, and scientific research.

How is this Immunoglobulin Products Industry segmented?

The immunoglobulin products industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- IgG

- IgA

- IgM

- IgD

- IgE

- Route Of Administration

- Intravenous (IV)

- Subcutaneous (SC)

- Intramuscular (IM)

- Geography

- North America

- US

- Europe

- Germany

- UK

- Middle East and Africa

- APAC

- China

- Japan

- South America

- Rest of World (ROW)

- North America

By Product Insights

The igg segment is estimated to witness significant growth during the forecast period.

The market is significantly influenced by the IgG product segment, which accounts for a substantial share due to the widespread application of IgG-based therapies in treating various immune-related disorders. IgG, the most abundant antibody isotype in the human body, plays a vital role in immune response and defense against pathogens. Derived from pooled plasma donations, IgG products are available in intravenous (IV), subcutaneous (SC), and intramuscular (IM) preparations. These therapies find utility in the treatment of primary immunodeficiencies, autoimmune diseases, neurological disorders, and certain infectious diseases. Key entities in this segment include prominent pharmaceutical companies such as CSL Ltd.

And others, who contribute to the development and production of these essential treatments. Health economics, patient advocacy, and healthcare professionals play a crucial role in disease management and patient care, influencing the market dynamics and trends. Immune modulation, quality control, clinical trials, and regulatory approvals are essential aspects of the drug development process, ensuring the safety and efficacy of these therapies. Disease management, secondary immunodeficiency, chronic inflammatory diseases, replacement therapy, dosage forms, and administration routes further expand the application scope of IgG products. Protein engineering, antibody engineering, and polyclonal antibodies are emerging technologies that offer potential advancements in the field, addressing the unmet needs and evolving patient requirements.

Get a glance at the market report of share of various segments Request Free Sample

The IgG segment was valued at USD 8.98 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

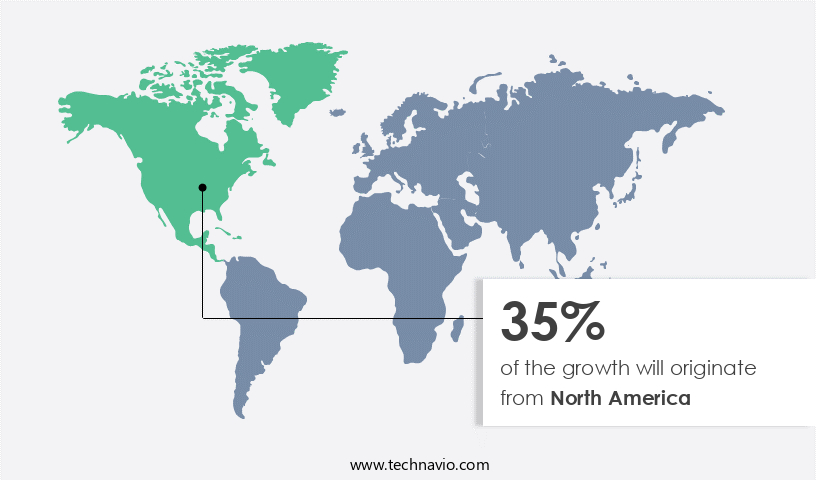

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in North America is experiencing significant growth, driven by the increasing prevalence of various diseases, including cancer, autoimmune diseases, metabolic diseases, musculoskeletal disorders, central nervous system disorders, and blood disorders. The global rise in the prevalence of cardiovascular disease and cancer further fuels market expansion. In the US, healthcare reforms have led to an increase in healthcare services utilized by both insured and uninsured populations, providing additional impetus for market growth. Population growth and economic stability in the region offer promising opportunities for the market. Immunomodulatory therapies, such as monoclonal antibodies, are increasingly being used in precision medicine and targeted therapies for various diseases, including neurological disorders, hematologic disorders, chronic inflammatory diseases, and infectious diseases.

Patient advocacy groups and healthcare professionals are playing a crucial role in raising awareness and driving the adoption of these therapies. Drug development companies are focusing on personalized medicine and patient management strategies to improve disease management and optimize dosage forms for various immunoglobulin products. Regulatory approvals for new therapeutic antibodies and replacement therapies are expected to further boost market growth. Infusion therapy, including home infusion and intravenous immunoglobulin, is a significant administration route for immunoglobulin products. Advancements in infusion therapy technologies and the convenience they offer to patients are expected to increase their adoption. Protein engineering and antibody engineering are key areas of research in the market, with the potential to offer more effective and targeted therapies for various diseases.

Polyclonal antibodies and primary immunodeficiency treatments are also gaining attention due to their potential to address unmet medical needs. Quality control and clinical trials are essential components of the market, ensuring the safety and efficacy of these therapies. Health economics and disease management are also critical factors influencing market growth, as payers and providers seek cost-effective solutions for managing various diseases.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Immunoglobulin Products Industry?

- Recent immunoglobulin product developments is the key driver of the market.

- The market experiences growth due to the continuous introduction of new formulations, delivery methods, and indications by pharmaceutical companies. These innovations expand treatment options and cater to unmet medical needs for various patient populations. For instance, in January 2024, Takeda Pharmaceutical Co. Ltd. Secured US FDA approval for GAMMAGARD Liquid, an intravenous immunoglobulin therapy, for treating chronic inflammatory demyelinating polyneuropathy (CIDP) in adults.

- Simultaneously, CSL Ltd. Launched a subcutaneous immunoglobulin, Hizentra, in the form of a prefilled syringe, for the treatment of CIDP and primary immunodeficiency. These developments underscore the dynamic nature of the market and the commitment of companies to addressing diverse patient requirements.

What are the market trends shaping the Immunoglobulin Products Industry?

- Advancements in biotechnology and manufacturing processes is the upcoming market trend.

- The market is experiencing significant growth, driven by advancements in biotechnology and manufacturing processes. These innovations enable the creation of safer, more effective, and higher-quality therapies. Recombinant DNA technology and protein engineering are revolutionizing the production of immunoglobulin products, leading to the development of next-generation therapies with enhanced potency, specificity, and reduced immunogenicity. Leading biopharmaceutical companies, such as CSL Ltd., Takeda Pharmaceutical Co.

- Ltd., Grifols SA, and Octapharma AG, are at the forefront of leveraging these advancements to advance the field of immunoglobulin therapy. By utilizing these technologies, they are able to offer greater therapeutic benefits to patients. The continuous research and development in this area will further propel the growth of the market.

What challenges does the Immunoglobulin Products Industry face during its growth?

- High cost of immunoglobulin therapies is a key challenge affecting the industry growth.

- The market faces a substantial challenge due to the high cost of therapies, which affects both patients and healthcare systems. The average price for an intravenous immunoglobulin (IVIG) product ranges from USD50 to USD100 per gram, and patients often require multiple grams per infusion session. For instance, a typical IVIG infusion for a patient with a primary immunodeficiency disorder may necessitate doses of 400-800 milligrams per kilogram of body weight every 3-4 weeks.

- This translates into substantial treatment expenses, especially for those requiring long-term therapy. Subcutaneous immunoglobulin (SCIG) therapies, though generally less expensive than IVIG, still carry considerable costs. These high expenses can limit patient access to these essential treatments and put a strain on healthcare budgets.

Exclusive Customer Landscape

The immunoglobulin products market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the immunoglobulin products market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, immunoglobulin products market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ADMA Biologics Inc. - The company specializes in the production of Immune Globulin Intravenous (IGIV), specifically Bivigam, a 10% liquid product. Indicated for primary humoral immunodeficiency patients, Bivigam is an essential treatment option. This human immune globulin product is designed to address the immune system's deficiencies, ensuring optimal health and well-being for affected individuals. The company's commitment to innovation and quality is reflected in its comprehensive range of immunoglobulin solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ADMA Biologics Inc.

- Bio Products Laboratory Ltd.

- Biocon Ltd.

- CSL Ltd.

- GC Biopharma corp.Â

- Grifols SA

- Kedrion S.p.A

- LFB SA

- Novartis AG

- Octapharma AG

- Pfizer Inc.

- Serum Institute of India Pvt. Ltd.

- Shanghai RAAS Blood Products Co. Ltd.

- Taibang Biological Group Co. Ltd.

- Taj Pharmaceuticals Ltd.

- Takeda Pharmaceutical Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a diverse range of therapeutic offerings that cater to various medical conditions, particularly those related to immunodeficiencies and inflammatory diseases. Precision medicine and targeted therapies have emerged as key trends in this domain, with monoclonal antibodies representing a significant portion of the market's growth. Patient advocacy and health economics continue to influence the immunoglobulin market, as stakeholders seek to optimize treatment outcomes while managing costs. Neurological disorders, hematologic disorders, and chronic inflammatory diseases are among the primary indications for immunoglobulin use. Advancements in antibody engineering and immune modulation have led to the development of novel dosage forms and administration routes, including subcutaneous immunoglobulin and home infusion.

Clinical trials and regulatory approvals remain crucial components of the drug development process, ensuring the safety and efficacy of these therapeutic solutions. Healthcare professionals play a pivotal role in patient management, as they collaborate with patients and their caregivers to determine the most appropriate treatment regimens. Personalized medicine and disease management strategies are increasingly being adopted to address the unique needs of individual patients. Secondary immunodeficiency and autoimmune diseases are also significant indications for immunoglobulin therapy. Infectious diseases, including those caused by viruses and bacteria, continue to drive demand for these products. Protein engineering and polyclonal antibodies are other areas of innovation within the immunoglobulin market.

Quality control and infusion therapy administration routes are essential considerations in the delivery of immunoglobulin products. Intravenous immunoglobulin and therapeutic antibodies remain popular choices for treating various conditions, while replacement therapy remains a critical aspect of managing primary immunodeficiencies. The evolving landscape of the immunoglobulin market reflects the ongoing efforts to address unmet medical needs and improve patient outcomes. As research and development continue to advance, the market is expected to expand, offering new opportunities for innovation and growth.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.11% |

|

Market growth 2024-2028 |

USD 9699.84 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

8.65 |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Immunoglobulin Products Market Research and Growth Report?

- CAGR of the Immunoglobulin Products industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the immunoglobulin products market growth of industry companies

We can help! Our analysts can customize this immunoglobulin products market research report to meet your requirements.

RIA -

RIA -