Immunohistochemistry Market Size 2024-2028

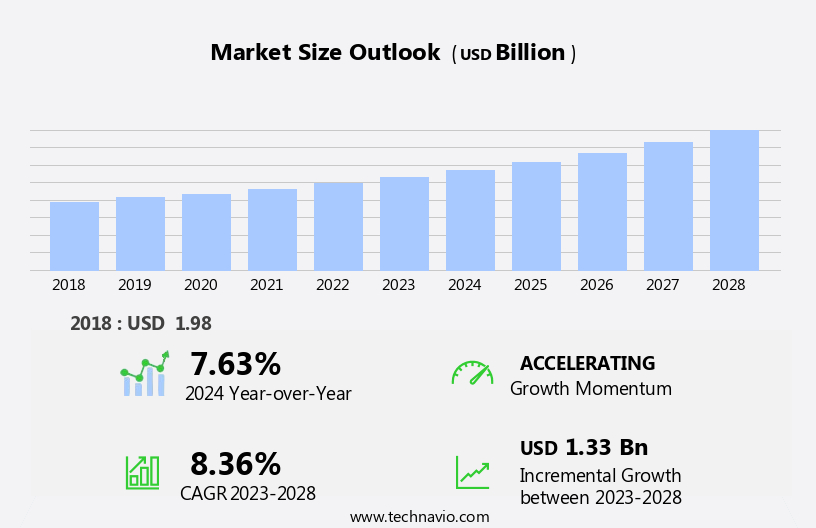

The immunohistochemistry market size is forecast to increase by USD 1.33 billion at a CAGR of 8.36% between 2023 and 2028.

What will be the Size of the Immunohistochemistry Market During the Forecast Period?

How is this Immunohistochemistry Industry segmented and which is the largest segment?

The immunohistochemistry industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Diagnostic application

- Research application

- Forensic application

- End-user

- Hospitals and diagnostic laboratories

- Academic and research institutes

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- France

- Asia

- China

- Rest of World (ROW)

- North America

By Application Insights

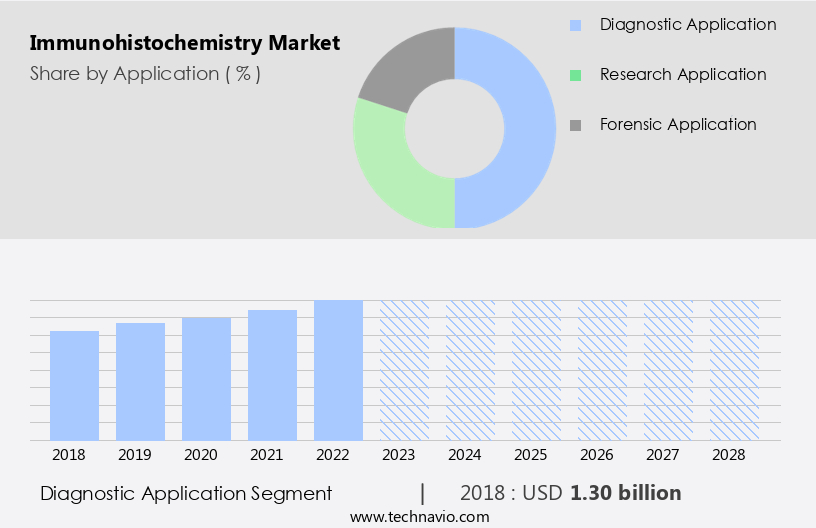

- The diagnostic application segment is estimated to witness significant growth during the forecast period.

Immunohistochemistry (IHC) is a vital diagnostic technique in pathology and molecular biology, enabling the identification and localization of specific proteins or antigens in tissue sections. This process utilizes antibodies that bind to the antigens, offering insights into disease mechanisms and biomarker discovery. IHC is particularly significant in oncology, where it assists in cancer diagnosis and therapy selection. With the growing understanding of various cancer types, including breast, colon, and lung cancer, the demand for IHC tests intensifies. Digital pathology and in vitro diagnostic (IVD) equipment facilitate automation and standardization, enhancing diagnostic accuracy. Key players In the market include Leica Biosystems, Akoya Biosciences, Roche, and others.

Companion diagnostics and immunotherapy trials further emphasize the therapeutic significance of IHC. Chronic diseases, such as cardiovascular diseases (e.G., ischemic heart disease, stroke), and infectious diseases (e.G., monkeypox, viral epidemics) also benefit from IHC. Monoclonal antibodies, antibody fragments, and diagnostic kits are essential laboratory consumables. Healthcare professionals and research organizations leverage IHC for diagnostic testing and personalized medicine. Immunofluorescence assay is a related technique. Cancer incidence, antigen-antibody interactions, geriatric population, reimbursement policies, and chronic diseases influence market growth.

Get a glance at the Immunohistochemistry Industry report of share of various segments Request Free Sample

The Diagnostic application segment was valued at USD 1.30 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

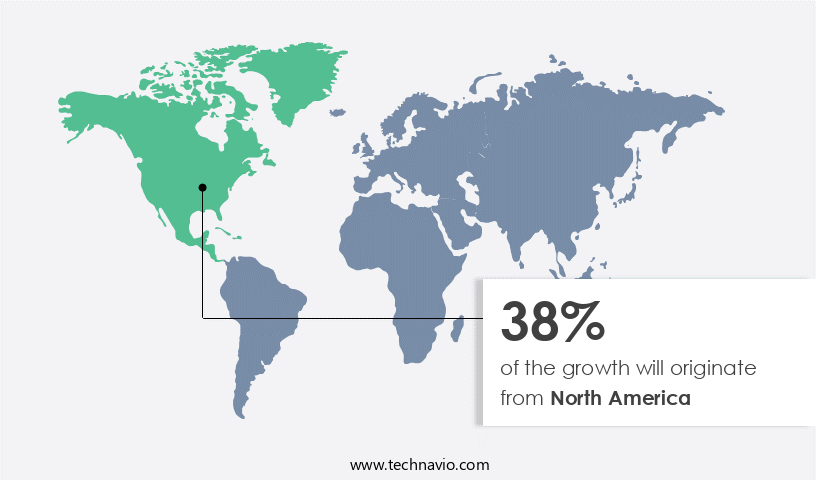

- North America is estimated to contribute 38% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

Immunohistochemistry (IHC) plays a pivotal role in diagnosing and understanding various cancer diseases, chronic conditions, and infectious diseases. In North America, the high adoption of IHC tests can be attributed to advanced healthcare infrastructure, research capabilities, and a commitment to personalized medicine. With numerous hospitals, research institutes, and clinics In the US and Canada, sophisticated diagnostic tests like IHC are routinely performed. These facilities are at the forefront of medical innovation, collaborating with academic and research organizations to develop new diagnostic techniques and therapeutic strategies. IHC is an essential tool in cancer research, aiding In the identification of specific antigens and antibodies, and contributing to the development of companion diagnostics and immunotherapy trials.

Digital pathology, IVD equipment, and laboratory consumables are integral components of IHC testing. Companies such as Leica Biosystems, Akoya Biosciences, Roche, and others provide solutions for IHC, digital immunohistochemistry, and multiplex immunohistochemistry. Standardization and automation are critical to ensuring diagnostic accuracy and consistency. IHC is also used In the diagnosis and monitoring of cardiovascular diseases, such as ischemic heart disease and stroke, and In the detection of viral epidemics, including monkeypox. The geriatric population and chronic diseases further drive the demand for IHC testing due to the increased prevalence of these conditions. Reimbursement policies and healthcare professional education are essential factors influencing the market growth.

In summary, IHC is a vital diagnostic tool In the US and Canadian healthcare systems, driving research, innovation, and precision medicine.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Immunohistochemistry Industry?

Increasing number of cancer patients globally is the key driver of the market.

What are the market trends shaping the Immunohistochemistry Industry?

Automation and technological advancements in immunohistochemistry processes is the upcoming market trend.

What challenges does the Immunohistochemistry Industry face during its growth?

High cost associated with immunohistochemistry is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The immunohistochemistry market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the immunohistochemistry market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, immunohistochemistry market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Agilent Technologies Inc. - The company's immunohistochemistry portfolio is a comprehensive solution, prioritizing quality and service to streamline workflows, minimize variation, and reduce potential staining imperfections. This portfolio caters to the diagnostic and research markets, offering a range of validated antibodies and assays for various applications. By focusing on consistency and accuracy, the company aims to provide reliable results, ensuring confidence in research and diagnostic outcomes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agilent Technologies Inc.

- Bio Rad Laboratories Inc.

- Bio SB

- Bio Techne Corp.

- Biocare Medical LLC

- BioGenex Laboratories Inc.

- CANDOR Bioscience GmbH

- Cell Signaling Technology Inc.

- Danaher Corp.

- Eagle Biosciences Inc.

- Elabscience Biotechnology Inc.

- F. Hoffmann La Roche Ltd.

- Lunaphore Technologies SA

- Merck KGaA

- Miltenyi Biotec B.V. and Co. KG

- PerkinElmer Inc

- PHC Holdings Corp.

- SAKURA SEIKI Co. Ltd.

- Takara Holdings Inc.

- Thermo Fisher Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Immunohistochemistry (IHC) is a vital technique used In the field of pathology and research to identify specific proteins or antigens in cells and tissues. This method has been instrumental in advancing our understanding of various diseases, including cancer and infectious diseases, and In the development of personalized medicine and therapeutic interventions. The global market for IHC is driven by several factors, including the increasing incidence of chronic diseases such as cancer and cardiovascular diseases. The geriatric population, which is more susceptible to these diseases, also contributes to the growth of the market. The need for accurate and reliable diagnostic tests to aid In the early detection and treatment of diseases is another significant factor.

Automation and digitalization are key trends In the IHC market. Digital pathology, which involves the digitization of glass slides and the analysis of images using computer algorithms, is gaining popularity due to its efficiency and accuracy. Digital IHC, which combines digital pathology with IHC, offers several advantages, including faster turnaround time, improved reproducibility, and the ability to perform multiplex IHC, which allows for the detection of multiple markers in a single test. The use of IHC in research organizations and academic institutions is also driving market growth. Researchers In the field of immunology and infectious diseases are utilizing IHC to gain insights into disease mechanisms and to develop new therapeutic interventions.

Companion diagnostics, which are tests that are used in conjunction with therapeutic drugs to identify patients who are most likely to respond to treatment, are also gaining traction In the market. The standardization of IHC protocols and the availability of high-quality antibodies and kits are crucial for the consistent and reliable performance of IHC tests. Laboratory consumables, such as slides and buffers, also play a critical role in ensuring the success of IHC experiments. The use of IHC In the diagnosis of infectious diseases, such as monkeypox and viral epidemics, is another area of growth. IHC is a valuable tool for identifying the presence of specific viral antigens in clinical samples, which can aid In the diagnosis and treatment of these diseases.

Reimbursement policies and regulatory approvals are important considerations for the market. The availability of reimbursement for IHC tests and the regulatory approval of new IHC-based diagnostic tests can significantly impact market growth. In conclusion, the global market for IHC is driven by the increasing incidence of chronic diseases, the need for accurate and reliable diagnostic tests, and the trends towards automation and digitalization. The use of IHC in research, personalized medicine, and infectious disease diagnosis is also contributing to market growth. Standardization, the availability of high-quality antibodies and kits, and regulatory approvals are crucial factors for the success of the market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

168 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.36% |

|

Market growth 2024-2028 |

USD 1.33 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.63 |

|

Key countries |

US, Germany, France, UK, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Immunohistochemistry Market Research and Growth Report?

- CAGR of the Immunohistochemistry industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the immunohistochemistry market growth of industry companies

We can help! Our analysts can customize this immunohistochemistry market research report to meet your requirements.

RIA -

RIA -