Implantable Medical Devices Market Size 2025-2029

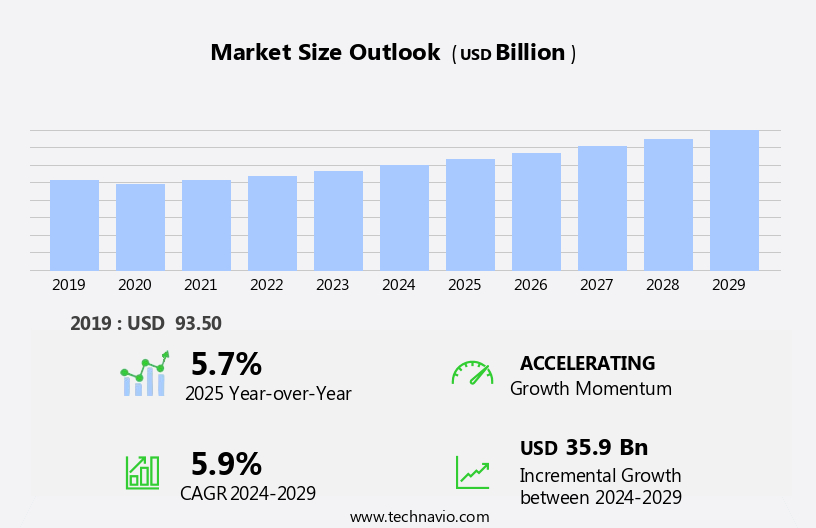

The implantable medical devices market size is forecast to increase by USD 35.9 billion at a CAGR of 5.9% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing prevalence of chronic illnesses and advancements in technology, particularly the adoption of 3D printing for implantable devices. However, this market faces notable challenges that require strategic navigation for companies seeking to capitalize on its potential. Regulatory hurdles, including stringent approval processes and compliance requirements, impact adoption and increase costs for manufacturers. Furthermore, high surgery costs associated with implant procedures can limit accessibility for patients, despite the benefits of these advanced medical solutions. These devices, which include insulin pumps, cosmetic implants, orthopedic implants such as knee replacements and spinal implants, ventricular assist devices, neurostimulation devices, dental implants, and implantable MRI systems, are transforming healthcare services.

- To succeed in this market, companies must focus on addressing these challenges through innovative strategies, such as streamlining regulatory approvals and collaborating with healthcare providers to offer affordable financing options for patients. By staying abreast of market trends and addressing these challenges effectively, companies can capitalize on the significant growth opportunities presented by the market.

What will be the Size of the Implantable Medical Devices Market during the forecast period?

- The market is experiencing significant advancements, driven by the integration of technology and biocompatible materials to enhance patient care and improve surgical precision. Informed consent processes are being augmented through digital platforms, enabling more transparent communication between healthcare providers and patients. Biocompatible coatings and bioabsorbable materials are revolutionizing device development, making implants more personalized and aligned with outcomes-based reimbursement. Precision surgery is being advanced through image-guided procedures and augmented reality, while remote diagnostics and haptic feedback facilitate connected healthcare. Value-based care and regulatory affairs are shaping the industry, driving innovation in areas such as tissue engineering, stem cell therapy, and gene therapy. Additionally, the increasing prevalence of chronic diseases like diabetes and cardiovascular conditions necessitates the development of more advanced and cost-effective implantable medical devices for chronic disease management. The market is expected to witness significant growth in the coming years, particularly in areas such as extremities, cardiac pacemakers, and insulin pumps.

- Device tracking and supply chain management are becoming essential components of the healthcare ecosystem, ensuring patient safety and efficient delivery of care. Wearable technology, mobile health apps, and smart implants are transforming patient portal access and remote patient management, enabling a more proactive and personalized approach to healthcare. Industry consolidation continues to shape the landscape, with companies focusing on technology adoption, clinical research, and additive manufacturing to stay competitive. Biometric monitoring and cognitive enhancement are also emerging trends, as healthcare moves towards a more holistic and patient-centric approach. The future of implantable medical devices lies in the intersection of technology, biomaterials science, and healthcare policy, as we strive to deliver safer, more effective, and more accessible healthcare solutions.

How is this Implantable Medical Devices Industry segmented?

The implantable medical devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

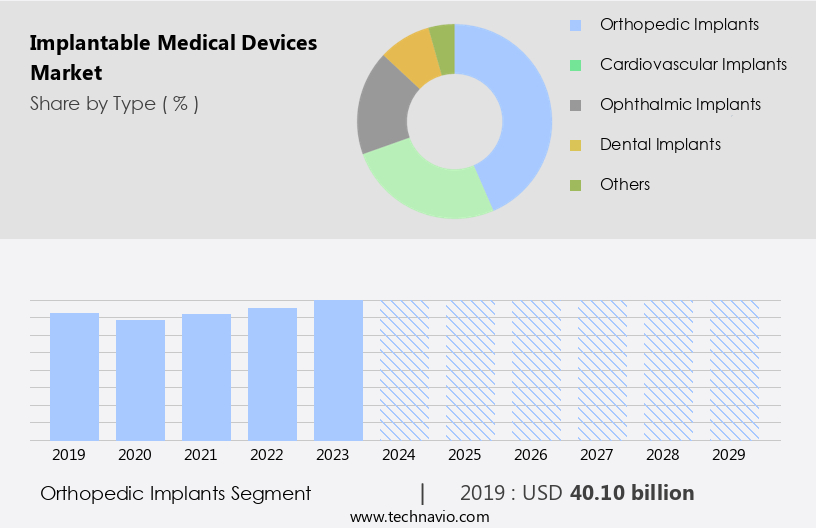

- Orthopedic implants

- Cardiovascular implants

- Ophthalmic implants

- Dental implants

- Others

- End-user

- Hospitals

- Clinics

- Others

- Material

- Metallic

- Ceramic

- Natural

- Polymeric

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The orthopedic implants segment is estimated to witness significant growth during the forecast period. Implantable devices, including medical implants and orthopedic implants, are transforming healthcare through advances in digital health, precision medicine, and biocompatible materials. Orthopedic implants, such as joint replacements, are essential for treating various conditions, including knee injuries, hip fractures, spinal injuries, joint disorders, and craniomaxillofacial defects. These implants come in different forms, including pins, wires, staples, plating systems, pedicle screws, cages, rods, plates, pedicle screw systems, hip and shoulder arthroplasty, and intramedullary nailing systems. Classified into joint reconstruction implants, spinal implants, and craniomaxillofacial implants, orthopedic devices are revolutionizing surgical procedures. Joint reconstruction implants are utilized for knee and hip replacement, trauma, and extremities. Devices include implantable cardiac pacemakers, implantable cardioverter defibrillators, implantable hearing devices, implantable shock absorbers, neurostimulators, and ventricular assist devices.

Machine learning and data privacy are vital for improving patient care and maintaining data security. Cardiac implants, insulin pumps, drug eluting stents, and spinal cord stimulation devices are other types of implantable devices that significantly impact healthcare. The integration of artificial intelligence and robotics in medical implants is leading to minimally invasive surgery and advanced patient care. The future of implantable devices lies in personalized medicine, regenerative medicine, and 3D printing, offering innovative solutions for improving quality of life.

The Orthopedic implants segment was valued at USD 40.10 billion in 2019 and showed a gradual increase during the forecast period. Spinal implants cater to the treatment of spinal disorders, such as spinal deformities, spondylolisthesis, and scoliosis. Wireless communication and telemetry systems enable remote monitoring and post-operative care, ensuring long-term efficacy and patient engagement. Clinical trials and data analytics are crucial for clinical performance evaluation and regulatory approval. Patient education and consent are essential components of the implantation process, ensuring device safety and addressing surgical risks. Healthcare systems, insurance companies, and government agencies collaborate to develop reimbursement models and infection control protocols. Device maintenance, biocompatibility testing, and sensor technology are essential for ensuring device lifespan and patient outcomes. Neurostimulation devices, including neurostimulators, provide relief for individuals with Parkinson's disease and epilepsy.

Regional Analysis

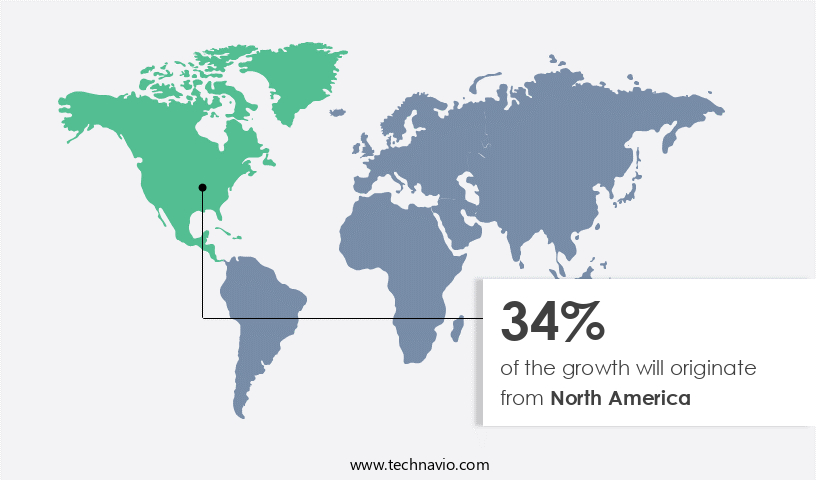

North America is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing steady growth, driven by several factors. The increasing prevalence of orthopedic and cardiovascular diseases and conditions, such as arthritis, osteoporosis, spinal disorders, and knee injuries, is fueling the demand for orthopedic implants. According to the Centers for Disease Control and Prevention (CDC), arthritis prevalence in the US is projected to rise in the coming years. New product launches, favorable reimbursements for implant surgeries, and initiatives by governments and non-profit organizations to raise awareness about various healthcare conditions are also contributing to market growth. Advancements in digital health, regenerative medicine, and precision medicine are leading to the development of innovative implantable devices. Orthopedic implants, such as those used for knee replacement and hip fractures, are another growing segment of the market.

These include drug eluting stents, insulin pumps, spinal cord stimulation systems, and cardiac implants. Wireless communication, telemetry systems, and remote monitoring enable real-time data analytics and patient engagement, improving clinical performance and long-term efficacy. Minimally invasive surgery, robotic surgery, and 3D printing are transforming surgical procedures, reducing surgical risk and improving patient outcomes. Biocompatible materials, machine learning, and infection control are essential considerations for ensuring device safety and longevity. Reimbursement models, healthcare systems, and insurance companies are adapting to accommodate the integration of these advanced implantable devices. Regulatory approval processes, clinical trials, and post-operative care are crucial aspects of the market.

Patient consent, data privacy, and quality of life are key concerns for patients and healthcare providers. The market also encompasses dental implants, joint replacements, and drug delivery systems. Bioengineered tissues and personalized medicine are emerging trends, offering potential for significant advancements in implantable devices. Despite these opportunities, challenges remain, including device failure, device replacement, and device integration complexities. Government agencies and healthcare providers are working to address these challenges and ensure the safety and effectiveness of implantable devices. Overall, the North American the market is poised for continued growth, driven by technological advancements, changing healthcare landscapes, and evolving patient needs.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Implantable Medical Devices market drivers leading to the rise in the adoption of Industry?

- The increasing prevalence of chronic illnesses among the population serves as the primary market driver. The market in the US is driven by the increasing prevalence of orthopedic conditions, such as osteoporosis, arthritis, hip and knee injuries, and bone deformities. According to the Centers for Disease Control and Prevention (CDC), approximately 53 million adults in the US are diagnosed with arthritis in 2023. Osteoarthritis, a common joint disorder, is a significant contributor to this number. The aging population and the resulting rise in orthopedic conditions are leading to a high volume of knee and hip replacement surgeries, with over 700,000 procedures performed annually in the US (American Academy of Orthopaedic Surgeons). Advancements in medical technology are also fueling market growth. For instance, sensor technology, biocompatibility testing, and 3D printing are revolutionizing implantable medical devices. Minimally invasive surgery and patient engagement are other trends gaining traction. Long-term efficacy and device failure are critical factors influencing market dynamics. Government agencies and reimbursement models play a crucial role in market regulation and financing. Sensor technology, such as that used in insulin pumps and deep brain stimulation devices, enables real-time monitoring and analysis of patient health data. Biocompatibility testing ensures the safety and effectiveness of implantable devices. Minimally invasive surgery reduces recovery time and minimizes post-operative complications.

- Patient engagement through mobile applications and telehealth services enhances the patient experience and improves long-term outcomes. The market faces challenges, including the high cost of devices and the risk of device failure. Regulatory agencies, such as the Food and Drug Administration (FDA), enforce stringent regulations to ensure the safety and efficacy of implantable medical devices. Reimbursement models, such as bundled payments and value-based pricing, are evolving to address the high cost of these devices. In summary, the market in the US is experiencing significant growth due to the increasing prevalence of orthopedic conditions, advancements in technology, and regulatory and reimbursement trends.

- Sensor technology, biocompatibility testing, minimally invasive surgery, patient engagement, long-term efficacy, and device failure are key market dynamics. Government agencies and reimbursement models play a critical role in market regulation and financing.

What are the Implantable Medical Devices market trends shaping the Industry?

- Implantable medical devices are increasingly being produced via 3D printing, representing a significant market trend in the healthcare industry. This advanced manufacturing technique enables the creation of customized, complex designs for medical implants, enhancing patient outcomes and surgical precision. Implantable medical devices, including dental implants and drug delivery systems, have seen significant advancements due to the adoption of 3D printing technology. This technology offers advantages such as high precision, complex structure fabrication, and efficient material utilization, making it ideal for manufacturing intricate implantable devices. For instance, in joint replacement surgery, 3D-printed implants are being used by surgeons at Yale Medicine to expedite recovery and minimize patient pain. Patient consent and surgical risk are critical factors in the implementation of implantable medical devices. Healthcare providers and insurance companies play a significant role in ensuring the integration of these devices into patient care.

- Biocompatible materials and personalized medicine are essential considerations for improving patient outcomes. Hospital infrastructure and device integration are also essential aspects of the market. The use of 3D-printed implants, bioengineered tissues, and drug delivery systems can significantly enhance the quality of life for patients. The potential for customized solutions and the continuous development of new materials and technologies will continue to drive the growth of this market.

How does Implantable Medical Devices market faces challenges face during its growth?

- The escalating costs linked to implant surgeries represent a significant challenge to the industry's growth trajectory. The market encompasses a range of advanced technologies, including machine learning, remote monitoring, and robotic surgery, that significantly enhance post-operative care for patients. Implantable devices, such as cardiac implants and orthopedic implants, employ precision medicine and artificial intelligence to improve patient outcomes and extend device lifespan. However, the high cost of implant surgeries and related procedures remains a significant challenge. For instance, orthopedic implants, which are used to treat various injuries and conditions, can range from USD900 to USD1,000 per pedicle screw and exhibit a considerable increase in cost across the value chain, up to 150%.

- Ensuring regulatory approval, maintaining patient data privacy, and addressing data security concerns are other critical factors influencing market dynamics.

Exclusive Customer Landscape

The implantable medical devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the implantable medical devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, implantable medical devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company specializes in the development and commercialization of advanced implantable medical devices.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AbbVie Inc.

- B.Braun SE

- BIOTRONIK SE and Co. KG

- Boston Scientific Corp.

- Cardinal Health Inc.

- Conmed Corp.

- Global Consolidated Aesthetics Ltd.

- Globus Medical Inc.

- Ideal Implant Inc.

- Institut Straumann AG

- Johnson and Johnson Services Inc.

- LivaNova PLC

- Medtronic Plc

- NuVasive Inc.

- Orthofix Medical Inc.

- Osstem

- Smith and Nephew plc

- Stryker Corp.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Implantable Medical Devices Market

- In February 2024, Medtronic, a leading medical technology company, announced the FDA approval of its new MiniMed⢠MiniMed Sync 3Hm System, an advanced insulin pump system for diabetes management (Medtronic Press Release, 2024). This approval marks a significant technological advancement in implantable medical devices, offering improved glucose sensing and insulin delivery capabilities.

- In July 2025, Stryker and Boston Scientific, two major players in the market, entered into a definitive agreement to merge their neurotechnology businesses (Stryker Press Release, 2025). This strategic partnership aims to create a leading neurotechnology company, combining Stryker's Neuro and Spine division with Boston Scientific's Neuromodulation business.

- In September 2024, Abbott Laboratories secured EU approval for its FreeStyle Libre 3 System, a next-generation continuous glucose monitoring system (Abbott Press Release, 2024). This approval signifies a key regulatory milestone, allowing the company to expand its market presence in Europe and further strengthen its position in the implantable medical devices sector.

- In March 2025, Janssen Pharmaceuticals, a Johnson & Johnson subsidiary, and Google announced a collaboration to develop a digital therapeutic platform for neurodegenerative diseases using implantable medical devices (Google Blog, 2025). This partnership represents a significant strategic move, combining Janssen's expertise in neuroscience research with Google's advanced technology to create innovative solutions for treating neurodegenerative diseases.

Research Analyst Overview

The market continues to evolve, driven by advancements in technology and the growing demand for minimally invasive surgical procedures and personalized healthcare solutions. These devices, which include artificial organs, insulin pumps, cardiac implants, and orthopedic implants, among others, are integral to post-operative care and improving patient outcomes. Machine learning and artificial intelligence are increasingly being integrated into implantable devices, enabling remote monitoring, predictive analytics, and real-time intervention. Precision medicine and personalized care are also gaining traction, with biocompatible materials and drug delivery systems tailored to individual patient needs. Regulatory approval processes remain a critical factor in the market, with government agencies and insurance companies requiring rigorous testing for device safety, biocompatibility, and clinical performance.

Telemetry systems and wireless communication enable seamless data transfer and analysis, while digital health and patient engagement initiatives promote long-term efficacy and quality of life. However, challenges persist, including device failure, infection control, and patient consent. Device maintenance and replacement are ongoing concerns, with 3D printing and robotic surgery offering potential solutions for minimizing surgical risk and improving hospital infrastructure. Data privacy and security are also crucial considerations, with patient data requiring robust protection to ensure confidentiality and compliance with regulatory requirements. Ongoing clinical trials and biomedical research continue to push the boundaries of what is possible in the market, with new applications and innovations emerging constantly.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Implantable Medical Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

236 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.9% |

|

Market growth 2025-2029 |

USD 35.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.7 |

|

Key countries |

US, Canada, Germany, China, UK, France, Italy, Japan, India, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Implantable Medical Devices Market Research and Growth Report?

- CAGR of the Implantable Medical Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the implantable medical devices market growth of industry companies

We can help! Our analysts can customize this implantable medical devices market research report to meet your requirements.

RIA -

RIA -