In-game Advertising (IGA) Market Size 2026-2030

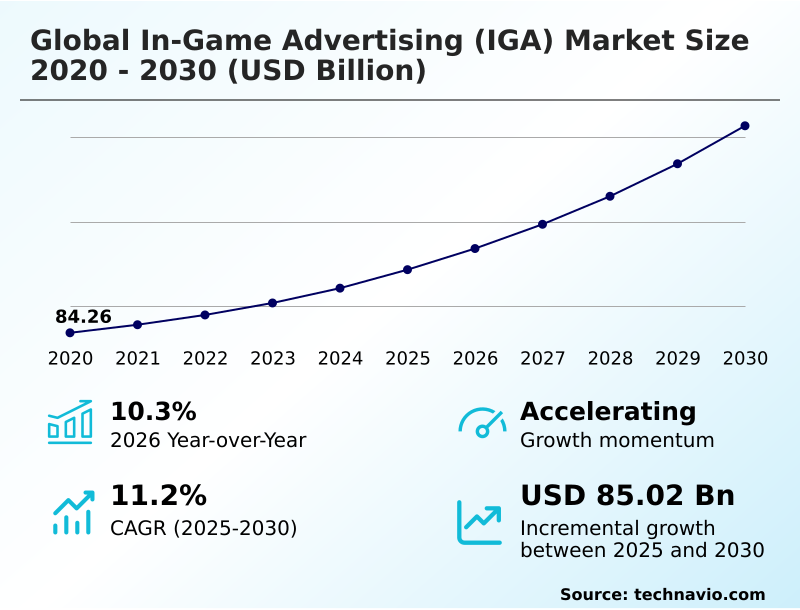

The in-game advertising (iga) market size is valued to increase by USD 85.02 billion, at a CAGR of 11.2% from 2025 to 2030. Proliferation of intrinsic and non-intrusive advertising formats will drive the in-game advertising (iga) market.

Major Market Trends & Insights

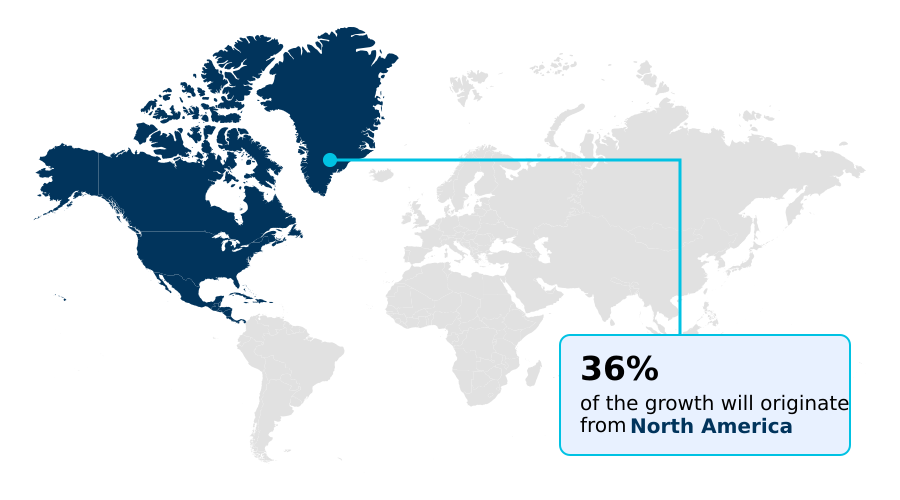

- North America dominated the market and accounted for a 35.6% growth during the forecast period.

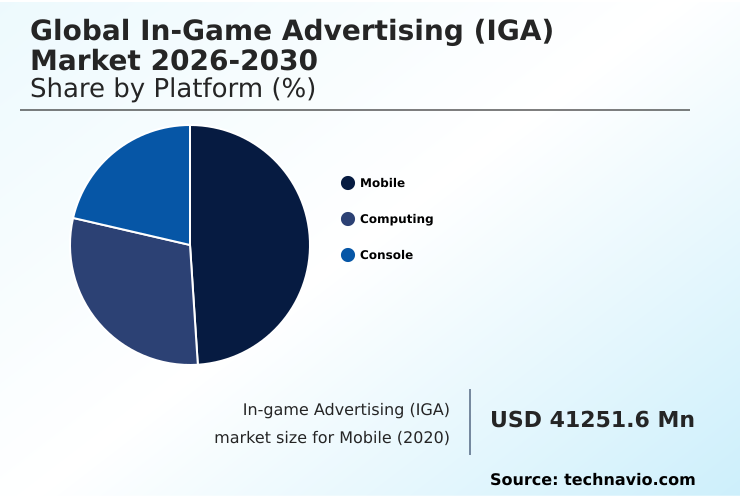

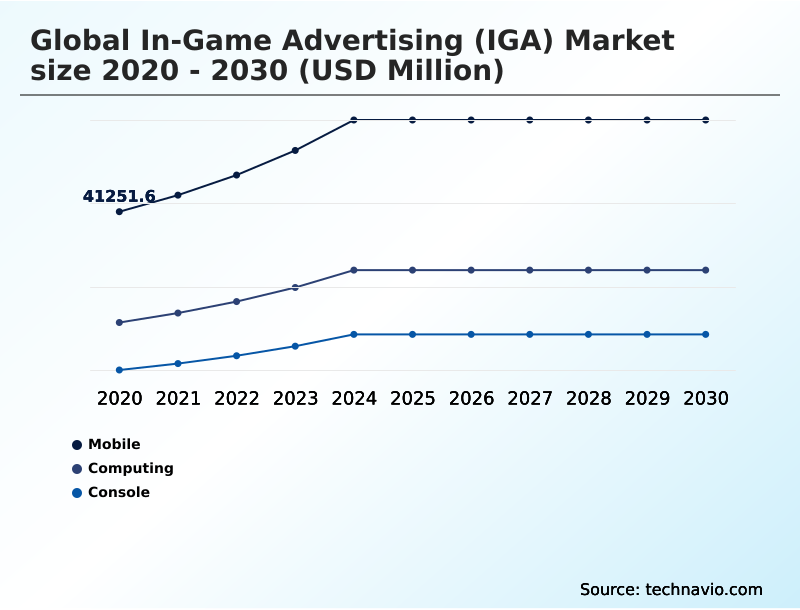

- By Platform - Mobile segment was valued at USD 54.71 billion in 2024

- By Type - Static ads segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 122.32 billion

- Market Future Opportunities: USD 85.02 billion

- CAGR from 2025 to 2030 : 11.2%

Market Summary

- The In-game Advertising (IGA) market is undergoing a significant transformation, moving beyond simple banners to sophisticated, integrated brand experiences. A core driver is the adoption of intrinsic ad placements and rewarded video ads, which respect player immersion standards while offering effective monetization.

- This shift is enabled by programmatic buying through advanced ad mediation platforms, which automate the purchasing of inventory across mobile, console, and PC environments. Key trends include the expansion of metaverse brand integration and the use of dynamic ad insertion in the burgeoning esports sector.

- For instance, a consumer goods company can leverage real-time bidding to place virtual product placements in a popular racing game, with ad creative personalized using generative AI to match player demographics, ensuring contextual relevance. However, the industry faces challenges in establishing unified cross-platform measurement and navigating complex data privacy compliance regulations.

- Success depends on balancing monetization with user experience, mitigating ad fatigue, and ensuring robust brand safety protocols are in place across all interactive ad units and software development kits.

What will be the Size of the In-game Advertising (IGA) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the In-game Advertising (IGA) Market Segmented?

The in-game advertising (iga) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Platform

- Mobile

- Computing

- Console

- Type

- Static ads

- Dynamic ads

- Advergaming

- Pricing scheme

- Cost per mille

- Hybrid or outcome-based

- Cost per completed view

- Cost per click

- Cost per action

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- UK

- France

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Platform Insights

The mobile segment is estimated to witness significant growth during the forecast period.

The mobile segment is the largest and most dynamic platform, driven by the low barrier to entry for casual gaming and widespread smartphone use.

This sector relies on diverse ad monetization strategies, including rewarded video ads and playable ad demonstrations, which provide a clear value exchange for users. Advertisers favor mobile due to sophisticated data for granular, real-time performance tracking and click-through rate optimization.

The prevalence of the free-to-play model necessitates robust ad mediation platforms to sustain developer revenue. As hardware improves, the capacity for high-fidelity, intrinsic ad placements is increasing, with some implementations boosting ad impressions by 20% year-over-year.

This evolution supports deeper brand safety protocols and more immersive user experiences.

The Mobile segment was valued at USD 54.71 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How In-game Advertising (IGA) Market Demand is Rising in North America Get Free Sample

The market's geographic composition is dynamic, with North America leading in monetization maturity, contributing 35.6% of the incremental growth, while the APAC region is the fastest-growing market, with an expansion rate of 11.5%.

In North America, the focus is on programmatic ad delivery within console and PC gaming, leveraging sophisticated demand-side platform integration. In contrast, APAC's growth is fueled by mobile gaming, where value-exchange advertising models and interactive ad units are paramount.

Europe prioritizes non-intrusive advertising and strict data privacy compliance. Emerging regions like South America and the Middle East are rapidly adopting mobile-first ad monetization strategies, creating new opportunities for cloud gaming ad solutions and in-game storefronts as digital infrastructure improves.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Successfully navigating the in-game advertising landscape requires a deep understanding of its evolving mechanics, moving beyond simple ad placements to strategic ecosystem integration. Key considerations include measuring the ROI of in-game advertising, which remains a complex task due to challenges in attribution for cross-platform gaming.

- For mobile-first strategies, integrating programmatic ads in mobile games is essential for scalability, but best practices for non-disruptive advertising must be followed to maintain engagement. This involves balancing monetization with the player experience to reduce ad fatigue in hyper-casual games. For premium environments, dynamic ad insertion in esports broadcasts and implementing intrinsic ads in console games offer high-impact visibility.

- Advergaming strategies for brand engagement and metaverse advertising are creating new frontiers, tying into virtual economies and user-generated content, though this raises concerns about brand safety. The role of DSPs in in-game ad buying is to streamline access to inventory, while publishers focus on optimizing ad fill rates with mediation.

- A critical shift is leveraging first-party data for targeting, a direct response to privacy compliance for in-game ad targeting. This pivot away from third-party cookies is compelling studios to build direct user relationships. Technologically, the focus is on refining viewability standards for 3D environments and using generative AI for ad personalization to improve the effectiveness of rewarded video ad formats.

- Firms that automate inventory purchasing through such programmatic pipelines have been shown to reduce campaign launch times by over 40% compared to manual direct-sales models, showcasing a clear operational advantage.

What are the key market drivers leading to the rise in the adoption of In-game Advertising (IGA) Industry?

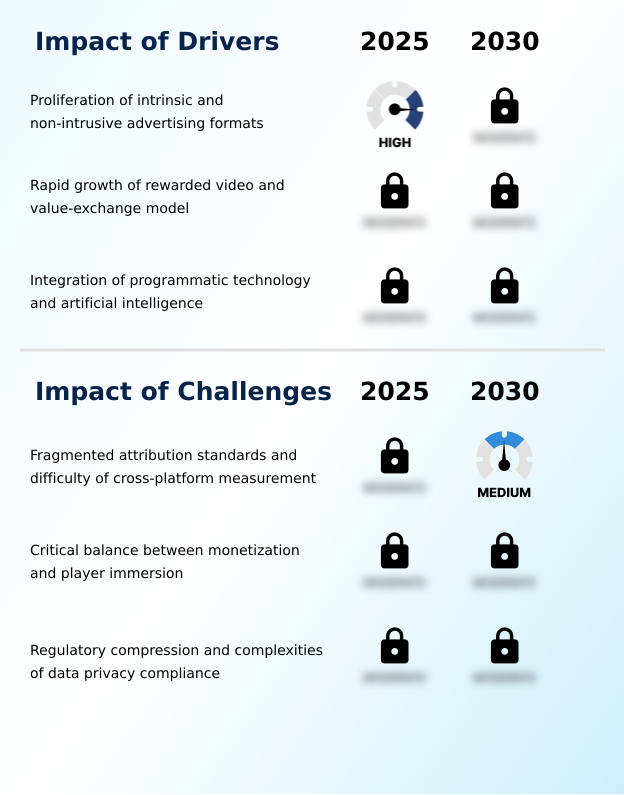

- A key market driver is the proliferation of intrinsic and non-intrusive advertising formats designed to enhance player immersion rather than disrupt gameplay.

- Market growth is fundamentally driven by the adoption of more sophisticated and player-friendly monetization models. The proliferation of intrinsic ad placements that blend into gameplay is reducing player churn, as these non-intrusive advertising formats are preferred over disruptive interstitials.

- Simultaneously, the value-exchange advertising model, particularly rewarded video ads, has become a core revenue driver, with some mobile-first markets seeing up to a 25% increase in average revenue per daily active user.

- The integration of programmatic buying and AI-powered real-time ad personalization is streamlining ad delivery. This ad-tech stack consolidation allows for highly effective contextual ad targeting, improving return on investment for cost per action campaigns and other performance-based initiatives.

What are the market trends shaping the In-game Advertising (IGA) Industry?

- The ascent of programmatic in-game advertising, driven by automated real-time bidding, is an emerging market trend. This shift signals a move toward more efficient, data-driven ad purchasing within virtual environments.

- Key market trends are centered on technological automation and deeper immersion. The expansion of programmatic in-game ad exchanges is pivotal, with programmatic ad delivery now enabling real-time bidding for dynamic ad insertion across platforms. This trend toward automated ad auctions has resulted in a 20% surge in total ad impressions for some publishers.

- Concurrently, metaverse brand integration is moving from concept to reality, with brands creating persistent virtual environment advertising. Esports advertising formats are also maturing, becoming a premium channel for brands.

- This is complemented by the use of generative AI for ad creative, which has accelerated marketing asset production and contributed to a 10% year-on-year increase in paid install share as competition for player visibility intensifies globally.

What challenges does the In-game Advertising (IGA) Industry face during its growth?

- A key challenge affecting industry growth is the difficulty of cross-platform measurement, compounded by fragmented attribution standards across gaming ecosystems.

- The market faces significant operational and regulatory headwinds. A primary challenge is the lack of unified cross-platform measurement and attribution modeling techniques, which complicates ROI analysis for advertisers. Poorly implemented intrusive ads can elevate player churn rates by over 15% in the first month, underscoring the critical need to balance monetization and player immersion.

- Furthermore, tightening data privacy compliance, such as GDPR and other regional mandates, restricts traditional user acquisition funnels. Failure to secure user consent properly for data collection can result in fines representing up to 4% of annual global turnover. This forces a strategic shift toward first-party data strategies and on-device processing to ensure user consent management.

Exclusive Technavio Analysis on Customer Landscape

The in-game advertising (iga) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the in-game advertising (iga) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of In-game Advertising (IGA) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, in-game advertising (iga) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Activision Blizzard Inc. - Expertise in patented in-play platforms enables seamless ad integration within interactive game environments, enhancing brand presence without disrupting user experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Activision Blizzard Inc.

- AdInMo Ltd.

- AdMaven

- Adverty AB

- Alphabet Inc.

- Anzu Virtual Reality Ltd.

- AppLovin Corp.

- AppsFlyer Ltd.

- Azerion Group N.V

- Bidstack Ltd.

- Chartboost Inc.

- Frameplay

- Gadsme

- InMobi Pte. Ltd.

- Liftoff Inc.

- Mistplay Inc.

- PubScale

- Unity Technologies Inc.

- Verve Group SE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in In-game advertising (iga) market

- In February, 2025, JBL launched an official branded world on the Roblox platform, allowing millions of players to explore a themed environment and collect virtual currency for branded cosmetic items, showcasing a significant move in advergaming.

- In January, 2025, Konami revealed a new suite of immersive AI-driven game design tools that enable more natural and contextual placement of brands within its sports and action titles, enhancing dynamic ad insertion capabilities.

- In November, 2024, a leading US-based advertising platform announced the acquisition of a specialized in-game ad technology provider to strengthen its programmatic delivery capabilities for intrinsic ads across console and PC games.

- In September, 2024, Google India implemented a strict policy update that banned advertising for certain real-money gaming categories from its ecosystem, highlighting the growing regulatory scrutiny and challenges related to brand safety and content relevance in the market.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled In-game Advertising (IGA) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.2% |

| Market growth 2026-2030 | USD 85016.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.3% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Indonesia, Australia, Germany, UK, France, Italy, Spain, The Netherlands, South Africa, Saudi Arabia, UAE, Egypt, Nigeria, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The in-game advertising market is defined by a strategic shift toward preserving the user experience while maximizing monetization. A core pillar of this evolution is the widespread adoption of programmatic buying and real-time bidding, which streamline access to inventory through sophisticated ad mediation platforms.

- These systems facilitate the use of diverse immersive ad formats, including intrinsic ad placements and rewarded video ads, which are becoming standard. The rise of metaverse brand integration and dynamic ad insertion within esports are creating new high-value opportunities.

- Technology providers are offering advanced software development kits that enable everything from virtual product placement to interactive ad units and playable ad demonstrations. However, this progress is tempered by the critical need for robust brand safety protocols and clear player immersion standards to mitigate ad fatigue.

- For instance, developers leveraging non-intrusive ad formats have seen partner revenue increases of up to 30%. Navigating this landscape requires a focus on contextual ad targeting using first-party data strategies to comply with privacy regulations, moving away from less transparent user acquisition funnels.

- The complexity of cross-platform measurement remains a significant hurdle, pushing the industry toward unified standards for in-game ad exchanges. Ultimately, success hinges on the seamless convergence of demand-side platform integration and supply-side platform monetization to create a sustainable and engaging ecosystem for brands and players alike.

What are the Key Data Covered in this In-game Advertising (IGA) Market Research and Growth Report?

-

What is the expected growth of the In-game Advertising (IGA) Market between 2026 and 2030?

-

USD 85.02 billion, at a CAGR of 11.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Platform (Mobile, Computing, and Console), Type (Static ads, Dynamic ads, and Advergaming), Pricing Scheme (Cost per mille, Hybrid or outcome-based, Cost per completed view, Cost per click, and Cost per action) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of intrinsic and non-intrusive advertising formats, Fragmented attribution standards and difficulty of cross-platform measurement

-

-

Who are the major players in the In-game Advertising (IGA) Market?

-

Activision Blizzard Inc., AdInMo Ltd., AdMaven, Adverty AB, Alphabet Inc., Anzu Virtual Reality Ltd., AppLovin Corp., AppsFlyer Ltd., Azerion Group N.V, Bidstack Ltd., Chartboost Inc., Frameplay, Gadsme, InMobi Pte. Ltd., Liftoff Inc., Mistplay Inc., PubScale, Unity Technologies Inc. and Verve Group SE

-

Market Research Insights

- The market's momentum is increasingly tied to the adoption of advanced ad monetization strategies. For example, implementing value-exchange advertising models has been shown to improve player retention metrics by over 15% in certain genres.

- The consolidation of the ad-tech stack is also critical, with some platforms reporting up to a 30% revenue increase for developers who adopt seamless in-play advertising solutions. This push for efficiency is reshaping how ad inventory management and automated ad auctions are handled, with a focus on real-time ad personalization.

- These data-driven approaches, which include sophisticated attribution modeling techniques and viewability measurement standards, are essential for brands seeking measurable returns and a positive association within virtual environment advertising.

We can help! Our analysts can customize this in-game advertising (iga) market research report to meet your requirements.

RIA -

RIA -