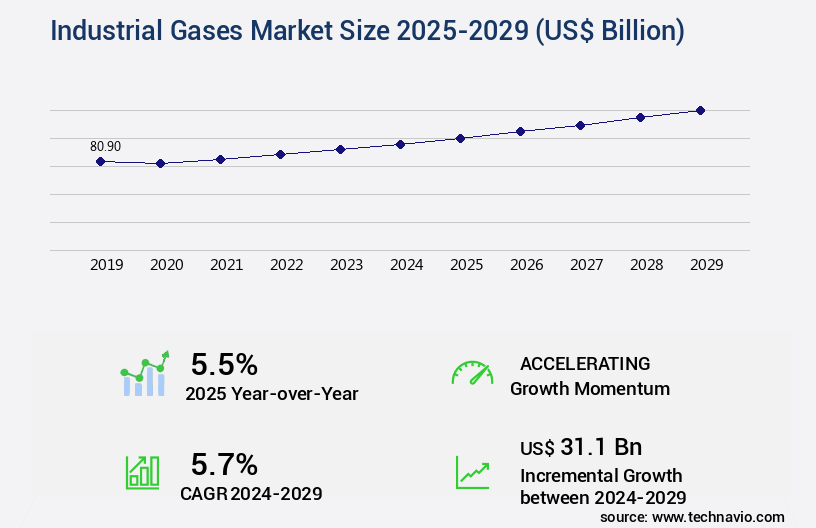

Industrial Gases Market Size 2025-2029

The industrial gases market size is valued to increase USD 31.1 billion, at a CAGR of 5.7% from 2024 to 2029. Facility expansion strategies by industrial gases vendors will drive the industrial gases market.

Major Market Trends & Insights

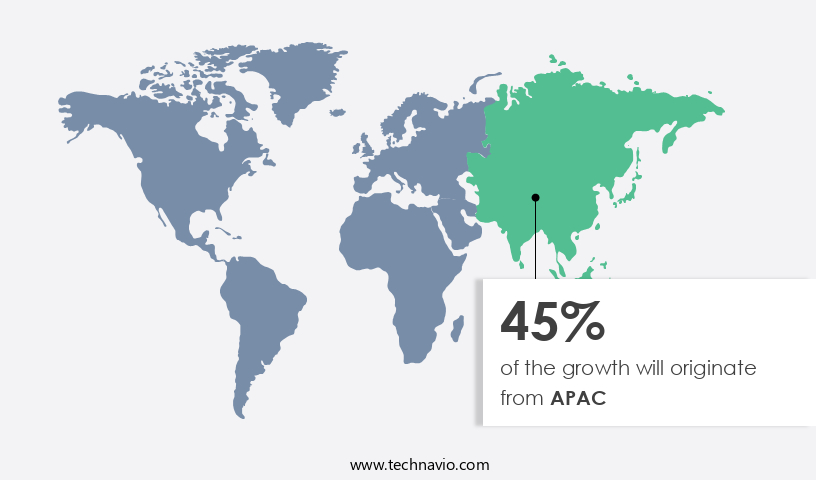

- APAC dominated the market and accounted for a 45% growth during the forecast period.

- By End-user - Manufacturing segment was valued at USD 23.00 billion in 2023

- By Type - Hydrogen segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 58.22 billion

- Market Future Opportunities: USD 31.10 billion

- CAGR from 2024 to 2029 : 5.7%

Market Summary

- The market encompasses the production, distribution, and application of various gases used in various industries. This dynamic market is driven by core technologies and applications, including welding, refrigeration, and chemical processing. Notable trends include the increasing adoption of advanced technologies, such as hydrogen fuel cells and carbon capture, utilization, and storage (CCUS). Service types and product categories, such as bulk gases, cylinders, and tonnage gases, continue to evolve, with an emphasis on sustainability and efficiency. Regulations play a crucial role in shaping the market, with stricter emission norms and safety standards driving innovation. Facility expansion strategies by industrial gases companies and the increasing number of mergers and acquisitions among market players are key developments.

- Criticalities in gas distribution and gas handling systems, such as ensuring safety, reliability, and efficiency, remain a significant challenge. According to a recent study, the market is expected to account for over 20% of the global hydrogen market by 2027.

What will be the Size of the Industrial Gases Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Industrial Gases Market Segmented ?

The industrial gases industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Manufacturing

- Chemical processing

- Metal fabrication

- Energy

- Others

- Type

- Hydrogen

- Oxygen

- Nitrogen

- Carbon dioxide

- Others

- Application

- Manufacturing

- Healthcare

- Food and Beverage

- Metallurgy

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The manufacturing segment is estimated to witness significant growth during the forecast period.

Industrial gases play a pivotal role in various manufacturing sectors, including aerospace, automotive, glass, ceramics, pulp and paper, shipbuilding, and railways coach and wagon manufacturing. These gases, such as oxygen, nitrogen, hydrogen, and carbon dioxide, are indispensable for numerous processes like welding, cutting, brazing, heat treating, purging, and annealing. In the automotive industry, they are utilized extensively in automobile parts and body manufacturing, as well as in repairs. In the aerospace sector, industrial gases are essential for fueling rockets and maintaining cabin pressure. In the glass industry, they are used for float glass production and tempering. In the ceramics sector, they aid in the sintering process.

In the pulp and paper industry, they are employed for pulp bleaching and paper coating. In shipbuilding, they are utilized for welding and cutting steel. In railways coach and wagon manufacturing, they are essential for welding and brazing. The market for industrial gases is currently thriving, with oxygen generation systems witnessing a significant increase in demand due to their extensive usage in various industries. For instance, argon purification is a crucial process in the steel industry, where it is used to protect the molten steel from oxidation during the production process. Membrane separation, a gas separation technique, is gaining popularity due to its energy efficiency and cost-effectiveness.

Furthermore, the market for industrial gases is expected to grow substantially in the coming years. For instance, the demand for nitrogen generation systems is projected to rise due to their increasing use in the food and beverage industry for food preservation. The market for hydrogen production is also expected to expand due to its growing usage in fuel cells and as a reducing agent in various industries. Process control systems, heat exchanger design, refrigeration cycles, and pressure swing adsorption are some of the key technologies driving the growth of the market. Temperature monitoring, safety systems, and pipeline transportation are essential components of the market infrastructure.

In terms of market size, the market was valued at approximately 150 billion USD in 2020, and it is projected to reach over 200 billion USD by 2026. The market's growth is attributed to the increasing demand for industrial gases in various sectors, advancements in technology, and regulatory compliance. The market for industrial gases is continuously evolving, with ongoing research and development in areas like gas liquefaction, carbon dioxide capture, and adsorbent materials. Additionally, there is a growing focus on emission reduction, which is leading to the adoption of cleaner production methods and the development of more efficient and sustainable industrial gas production technologies.

Gas handling equipment, compressor technology, and purification membranes are some of the key components of the industrial gas production process. Cryogenic distillation is a widely used process for separating and purifying gases based on their different boiling points. Pressure sensors and safety systems are essential components of the industrial gas infrastructure, ensuring safe and efficient production and transportation of gases. In conclusion, the market is a dynamic and evolving industry, with a wide range of applications across various sectors. The market is expected to grow substantially in the coming years, driven by technological advancements, regulatory compliance, and increasing demand for industrial gases in various industries.

The Manufacturing segment was valued at USD 23.00 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Industrial Gases Market Demand is Rising in APAC Request Free Sample

In the dynamic industrial landscape of 2024, APAC emerged as the leading consumer of industrial gases, accounting for a significant market share. This dominance can be attributed to the region's robust industrialization and the surging demand from sectors like metals and metal fabrication, chemical and petrochemical, and food and beverage. The rapid expansion of infrastructure in APAC necessitates the production of large volumes of steel, thereby driving the demand for industrial gases.

Furthermore, the region's industrial sector is witnessing a shift towards alternate sources of energy, leading to the proliferation of gasification plants, gas-to-liquids, coal-to-liquids, and coal-to-chemical plants. These facilities significantly contribute to the increasing consumption of industrial gases in APAC.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a diverse range of applications, from cryogenic distillation column design for producing oxygen and nitrogen to pressure swing adsorption cycle optimization for enhancing nitrogen generation efficiency. One significant trend driving market growth is the continuous pursuit of membrane separation efficiency improvement to meet stringent industrial gas purity specifications. Helium recovery from natural gas and oxygen generation system safety protocols are essential aspects of this market, with safety regulations increasingly stringent to ensure optimal performance and minimal risk. Carbon dioxide capture technology advancements and hydrogen production from electrolysis are other critical areas of focus, as emission reduction strategies gain traction in response to environmental concerns.

Gas blending system calibration procedures and pipeline transportation safety regulations are essential for maintaining the integrity of industrial gas supply chains. Gas handling equipment maintenance and process control system integration are also crucial for ensuring operational efficiency and reliability. The energy efficiency in gas liquefaction and refrigeration cycle improvements are essential for reducing operational costs and enhancing overall market competitiveness. In terms of technology advancements, compressor technology and heat exchanger design optimization are key areas of investment. Moreover, purification membrane selection criteria and adsorbent material regeneration are essential considerations for optimizing industrial gas production processes. A notable comparison within the market involves the adoption rates of different separation technologies, with membrane-based methods gaining significant ground against traditional distillation processes due to their energy efficiency and flexibility.

In conclusion, the market is a dynamic and evolving landscape, driven by technological advancements, regulatory requirements, and the pursuit of operational efficiency and cost savings. Companies investing in R&D for cryogenic distillation column design, pressure swing adsorption cycle optimization, membrane separation efficiency improvement, and other related areas are well-positioned to capitalize on the market's growth opportunities.

What are the key market drivers leading to the rise in the adoption of Industrial Gases Industry?

- Industrial gases companies' strategies for facility expansion are the primary catalysts fueling market growth.

- The global industrial gas market is witnessing significant expansion as companies invest in new production facilities to cater to various sectors, including healthcare, electronics, and manufacturing. Air Liquide SA, for instance, recently established a new platform for producing low-carbon gases in Quebec's new energy transition valley. This move is part of the company's strategy to increase its manufacturing footprint and support industries such as healthcare, chemicals, and metals. Other companies are adopting similar approaches to enhance efficiency and sustainability in their operations.

- The growing demand for industrial gases in these sectors is driving the market's continuous evolution. For example, the healthcare industry relies on medical gases like oxygen and nitrous oxide, while electronics manufacturing requires gases like nitrogen and hydrogen. The manufacturing sector, too, utilizes industrial gases extensively for processes like steelmaking and refining. These trends underscore the dynamic nature of the industrial gas market and its diverse applications.

What are the market trends shaping the Industrial Gases Industry?

- The increasing trend in the market is characterized by an escalating number of mergers and acquisitions among market players. (Or) Mergers and acquisitions are on the rise, becoming an increasingly prevalent trend in the market.

- The market is characterized by a fragmented landscape, with a multitude of small and medium-sized businesses operating regionally. To expand their market presence and achieve operational efficiencies, larger industrial gases companies are engaging in mergers and acquisitions (M&A). These strategic moves enable the consolidation of market share, economies of scale, and the acquisition of complementary businesses and technologies. For instance, in May 2023, Air Products announced an investment agreement with the Government of the Republic of Uzbekistan and Uzbekneftegaz JSC to acquire and manage a natural gas-to-syngas processing facility in Qashqadaryo Province, Uzbekistan, for a significant investment.

- This acquisition underscores the ongoing trend of industrial gases companies expanding their product portfolios and diversifying their offerings to cater to the evolving needs of industries worldwide. Moreover, M&A activities facilitate the enhancement of capabilities and market reach, as demonstrated by the growing number of strategic alliances and collaborations in the sector. These partnerships enable companies to broaden their geographical presence and strengthen their competitive positions. The dynamic nature of the market necessitates continuous adaptation and innovation, making M&A an essential tool for businesses seeking growth and expansion.

What challenges does the Industrial Gases Industry face during its growth?

- The growth of the industry is significantly impacted by the complexities and criticalities in the design, implementation, and management of gas distribution and handling systems. Ensuring the reliable and efficient operation of these systems is a key priority for industry professionals.

- Industrial gases are essential components in various sectors, including manufacturing, processing, and packaging. Ensuring the safe and efficient distribution of these gases is crucial for maintaining process quality. In the food and beverage and healthcare industries, stringent standards apply due to the sensitive nature of the applications. Industrial gases are transported in trolleys or cylinders, necessitating frequent refilling and dispatch. Alternative distribution methods include pipelines and bulk transport via ships and trucks. The distribution systems for industrial gases must maintain precise control over impurities, which can significantly impact processes. For instance, in the food and beverage industry, even minor impurities can lead to product recalls or quality issues.

- In the healthcare sector, impurities can compromise the efficacy of therapeutic gases. The choice of distribution method depends on several factors, including the volume of gas required, the distance to the point of use, and the specific gas application. Trolleys and cylinders offer flexibility for small-scale or remote applications, while pipelines and bulk transport are more suitable for large-scale industrial processes. Regardless of the chosen method, the focus remains on ensuring the safety, reliability, and efficiency of the industrial gas distribution network.

Exclusive Technavio Analysis on Customer Landscape

The industrial gases market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial gases market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Industrial Gases Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, industrial gases market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Air Liquide - This industrial gas provider caters to the refining, petrochemical, and metal industries with a comprehensive range of offerings. Gases include oxygen, nitrogen, hydrogen, argon, carbon dioxide, helium, acetylene, and specialty gases. These essential elements fuel various industrial processes, driving efficiency and productivity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Liquide

- Air Products and Chemicals

- Asia Technical Gas Co.

- BASF SE

- Buzwair Holding

- Coregas

- Gulf Cryo

- INOX Air Products

- Iwatani Corporation

- Lincoln Electric

- Linde plc

- Messer Group

- Nippon Sanso Holdings

- NovaGas Technologies

- Praxair

- SABIC

- SOL Group

- Taiyo Nippon Sanso

- Welsco Inc.

- Yingde Gases

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial Gases Market

- In January 2024, Linde plc, a leading industrial gases provider, announced the launch of its new hydrogen fueling station in Germany, marking a significant expansion of its alternative fuel infrastructure (Linde press release). This station, part of Linde's H2 Mobility joint venture, is expected to increase the availability of hydrogen fuel for commercial vehicles in Europe.

- In March 2024, Air Products and Chemicals, Inc. Entered into a strategic collaboration with Siemens Energy to develop and commercialize carbon capture, utilization, and storage (CCUS) technologies (Air Products press release). This partnership aims to reduce greenhouse gas emissions in the industrial sector by utilizing industrial gases for carbon capture and utilization.

- In May 2024, Praxair, a leading industrial gases company, completed the acquisition of INEOS's US nitrogen business, expanding its presence in the North American market (Praxair press release). The acquisition added approximately 1.3 billion cubic feet per day of nitrogen production capacity to Praxair's portfolio.

- In April 2025, Air Liquide, a global leader in gases, technologies, and services, secured regulatory approval for its proposed USD13.6 billion acquisition of Airgas, Inc. (Air Liquide press release). This acquisition will significantly expand Air Liquide's presence in the US market and strengthen its position as a leading industrial gases provider worldwide.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Gases Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

220 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.7% |

|

Market growth 2025-2029 |

USD 31.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.5 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving the market, various processes and techniques play a pivotal role in ensuring the production and purification of gases for diverse applications. Gas purification processes, such as membrane separation and cryogenic distillation, are continually advancing to enhance energy efficiency and improve gas separation techniques. Refrigeration cycles, a crucial aspect of gas liquefaction, are increasingly being optimized to minimize energy consumption. Process control systems, including pressure sensors and temperature monitoring, are integral to maintaining industrial gas purity and ensuring consistent quality. Argon purification, a significant application of gas separation technologies, is essential for various industries, including welding and metal fabrication.

- Heat exchanger design and compressor technology also contribute to the efficiency of gas handling equipment and oxygen generation systems. Gas analysis methods, employing advanced sensors and spectroscopic techniques, enable real-time monitoring of gas compositions and facilitate process optimization. Regulatory compliance and safety systems are integral components of industrial gas production and handling, ensuring emission reduction and adherence to environmental standards. Bulk storage tanks, designed with pressure swing adsorption technology, facilitate the safe and efficient storage of gases. Helium recovery and nitrogen generation systems are essential for numerous applications, including medical, industrial, and scientific sectors.

- Carbon dioxide capture and hydrogen production are emerging trends in the market, driven by the growing demand for sustainable energy solutions and emission reduction strategies. Gas blending systems and flow rate measurement techniques enable precise control over gas mixtures, enhancing overall process efficiency. Purification membranes, an essential component of many gas separation processes, are continually evolving to improve gas separation and energy efficiency. The ongoing development of compressor technology and pipeline transportation systems further expands the capabilities of the market, enabling the delivery of clean, high-purity gases to a wide range of industries.

What are the Key Data Covered in this Industrial Gases Market Research and Growth Report?

-

What is the expected growth of the Industrial Gases Market between 2025 and 2029?

-

USD 31.1 billion, at a CAGR of 5.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Manufacturing, Chemical processing, Metal fabrication, Energy, and Others), Type (Hydrogen, Oxygen, Nitrogen, Carbon dioxide, and Others), Geography (APAC, Europe, North America, South America, and Middle East and Africa), and Application (Manufacturing, Healthcare, Food and Beverage, and Metallurgy)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Facility expansion strategies by industrial gases vendors, Criticalities in gas distribution and gas handling systems

-

-

Who are the major players in the Industrial Gases Market?

-

Air Liquide, Air Products and Chemicals, Asia Technical Gas Co., BASF SE, Buzwair Holding, Coregas, Gulf Cryo, INOX Air Products, Iwatani Corporation, Lincoln Electric, Linde plc, Messer Group, Nippon Sanso Holdings, NovaGas Technologies, Praxair, SABIC, SOL Group, Taiyo Nippon Sanso, Welsco Inc., and Yingde Gases

-

Market Research Insights

- The market encompasses a diverse range of applications, including heat treatment, welding processes, medical diagnostics, energy production, electronics manufacturing, automotive manufacturing, gas distribution networks, leak detection, aerospace applications, wastewater treatment, petroleum refining, laser cutting, remote monitoring, gas metering systems, pipeline integrity management, fault detection, data acquisition systems, cryogenic freezing, industrial gas applications, predictive maintenance, process automation, food packaging atmosphere, metal fabrication processes, chemical synthesis, pharmaceutical manufacturing, medical gas supply, semiconductor manufacturing, and power generation. According to industry estimates, the market for industrial gases reached a value of USD200 billion in 2020, with an annual growth rate of 3.5%.

- In comparison, the market for medical gases, a subset of the market, was valued at USD50 billion in the same year, expanding at a CAGR of 5.2%. These figures underscore the significant role industrial gases play in various industries and the continuous demand for innovative solutions in this evolving market.

We can help! Our analysts can customize this industrial gases market research report to meet your requirements.

RIA -

RIA -