Industrial Heat Recovery Systems Market Size 2026-2030

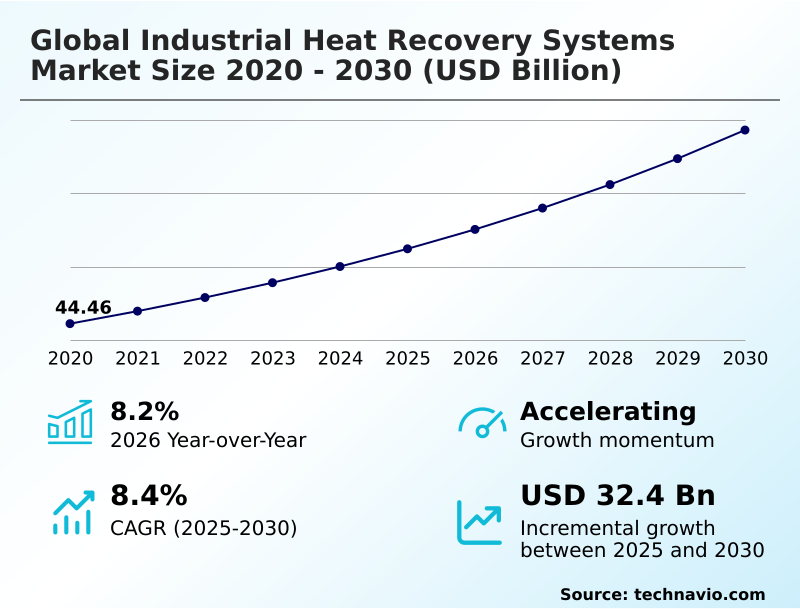

The industrial heat recovery systems market size is valued to increase by USD 32.40 billion, at a CAGR of 8.4% from 2025 to 2030. Accelerating decarbonization initiatives and regulatory compliance will drive the industrial heat recovery systems market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 47.1% growth during the forecast period.

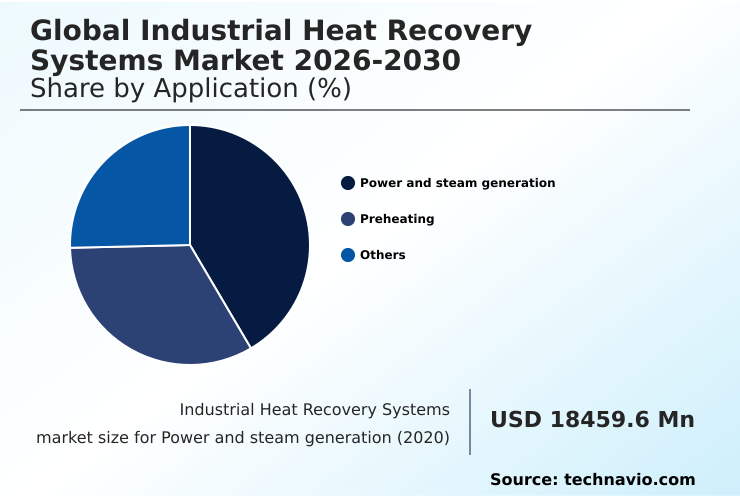

- By Application - Power and steam generation segment was valued at USD 25.81 billion in 2024

- By End-user - Energy generation segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 52.80 billion

- Market Future Opportunities: USD 32.40 billion

- CAGR from 2025 to 2030 : 8.4%

Market Summary

- The industrial heat recovery systems market is defined by a crucial shift toward thermal energy circularity and resource productivity. Organizations are increasingly adopting technologies for industrial decarbonization, moving beyond basic efficiency to integrated energy systems.

- A core focus is on waste heat to power applications, which utilize advanced methods like the organic rankine cycle and heat recovery steam generators to convert exhaust into usable electricity. This strategy enhances energy security and supports industrial electrification efforts.

- For instance, a chemical processing facility can deploy modular recovery units for preheating combustion air, directly lowering fuel consumption and contributing to net-zero emission targets. Innovations in high-temperature heat pumps and thermal storage systems are also expanding capabilities for low-grade heat recovery.

- The market's trajectory is shaped by the need for advanced thermal management ecosystems, driven by both economic incentives and stringent environmental mandates.

What will be the Size of the Industrial Heat Recovery Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Industrial Heat Recovery Systems Market Segmented?

The industrial heat recovery systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

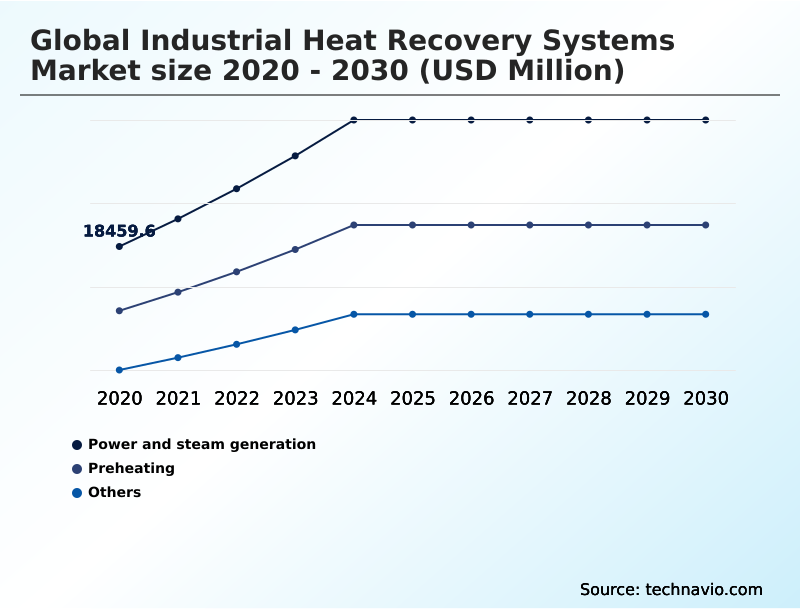

- Application

- Power and steam generation

- Preheating

- Others

- End-user

- Energy generation

- Petroleum refining

- Chemical and petrochemical

- Cement

- Others

- Type

- Medium temperature

- Low temperature

- High temperature

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Italy

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The power and steam generation segment is estimated to witness significant growth during the forecast period.

The power and steam generation segment is fundamental to industrial energy optimization, where thermal energy repurposing is a key strategy. This approach focuses on converting thermal waste from manufacturing into high-value utilities, such as on-site power generation.

Technologies like waste heat to power systems, often using an organic rankine cycle, enable industrial facilities to generate their own electricity from excess thermal energy.

This is especially critical for energy-intensive sectors where flue gas temperatures are high enough to drive turbines. By implementing process steam generation and thermal conversion efficiency, manufacturers can reduce their dependency on external electrical grids.

These smart thermal management systems achieve an operational cost reduction of up to 25%, insulating businesses from volatile utility prices and supporting sustainable manufacturing practices.

The Power and steam generation segment was valued at USD 25.81 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Industrial Heat Recovery Systems Market Demand is Rising in APAC Request Free Sample

The geographic landscape of the market is led by APAC, which is projected to grow at a rate approximately 19% faster than North America.

This growth is driven by aggressive industrial decarbonization policies and a focus on industrial energy optimization in countries like China and India.

The region's dense concentration of energy-intensive sectors provides a vast field for thermal energy repurposing and the deployment of advanced refrigerant development.

In contrast, North America and Europe are focusing on industrial electrification and the integration of high-temperature heat pumps to meet net-zero emission targets. The emphasis on district heating integration and cross-sector energy collaboration is particularly strong in Europe.

Firms in these mature markets are leveraging advanced materials science to enhance the durability of systems, ensuring a better lifecycle cost assessment. These regional differences highlight a global push toward more sustainable manufacturing practices.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the industrial heat recovery systems market are increasingly shaped by detailed evaluations of specific technologies and applications. For example, when comparing industrial heat pump efficiency, decision-makers are finding that newer systems can upgrade low-temperature waste heat valorization with greater effectiveness than older models.

- The cost-benefit of ORC systems continues to improve, making them a viable option for a wider range of facilities. However, challenges persist, particularly in the complexities of retrofitting heat exchangers in refineries, where space and process integration are major concerns.

- The roi of waste heat to power remains a critical metric, especially for large-scale waste heat recovery in cement production, where energy costs constitute a significant portion of operational expenses. Emerging opportunities in data center cooling heat reuse and heat recovery for green hydrogen are creating new avenues for growth, driving innovation in both technology and business models.

- These applications, along with the decarbonizing industrial process heat, are pushing the industry toward more specialized solutions. For example, advancements in thermal management in chemical plants now allow for more precise control over process temperatures.

- Optimizing steam generation from waste heat has also become a priority, as has the use of a digital twin for thermal system design to model performance before installation. The adoption of preheating systems for fuel savings is now standard in many industries. Addressing the challenges of integrating heat recovery is crucial for maximizing its benefits.

- Innovations in advanced materials for heat exchangers are extending equipment life in corrosive environments, while the growth of high-temperature heat pump applications is enabling electrification. The trend toward modular heat recovery unit installation is reducing downtime, and the use of industrial cooling with absorption chillers is gaining traction.

- Finally, specialized applications like heat recovery in food processing and district heating from industrial waste heat are expanding the market's reach.

What are the key market drivers leading to the rise in the adoption of Industrial Heat Recovery Systems Industry?

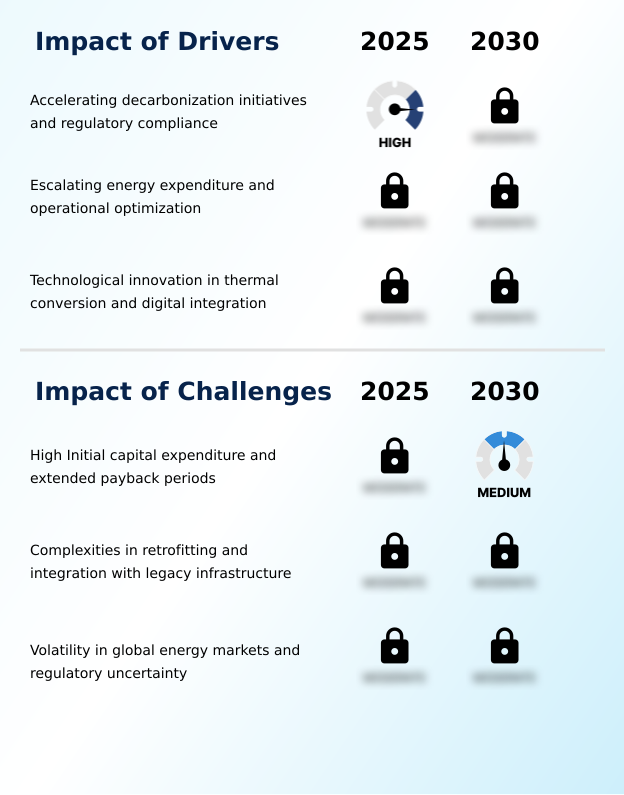

- Accelerating decarbonization initiatives and the need for regulatory compliance are key drivers for market growth.

- Market growth is significantly driven by accelerating industrial decarbonization initiatives and the need to meet net-zero emission targets. Escalating energy costs are compelling firms to prioritize industrial energy transition, leading to a focus on operational cost reduction.

- Facilities adopting modern heat recovery technologies report an average 15% decrease in annual energy expenditures. Technological innovations, including liquid-to-liquid heat exchangers and exhaust gas economizers, are expanding the scope of thermal conversion efficiency.

- The integration of digital platforms for asset performance management and predictive maintenance ensures that systems operate at peak performance, maximizing fuel consumption reduction.

- Furthermore, the global push toward a circular economy, coupled with energy efficiency audits, is solidifying the business case for investing in these systems and advancing supply chain modernization.

What are the market trends shaping the Industrial Heat Recovery Systems Industry?

- The integration of artificial intelligence and digital twin technology is an emerging trend, revolutionizing thermal management in industrial settings.

- Key market trends are centered on the rapid adoption of thermal management ecosystems and the use of digital twin technology to optimize performance. The proliferation of high-temperature heat pumps is enabling industrial electrification, allowing facilities to achieve a 20% improvement in thermal efficiency by upgrading low-grade heat.

- The expansion into new sectors like green hydrogen heat capture and data center heat reuse is diversifying market applications, with some projects reducing cooling energy demand by up to 35%. Technologies enabling this shift include advanced refrigerant development and oil-free centrifugal compressors, which are crucial for sustainable manufacturing practices.

- This move toward smart thermal management, supported by a clear regulatory compliance framework and integrated energy systems, is redefining how industries approach energy consumption and carbon footprint reduction.

What challenges does the Industrial Heat Recovery Systems Industry face during its growth?

- High initial capital expenditure and extended payback periods present a significant challenge to industry growth.

- A primary market challenge is the high initial capital expenditure planning required, which often involves payback periods extending beyond five years, posing a hurdle for firms with tight budgets. Integrating new systems with legacy infrastructure presents another significant barrier, with retrofitting projects increasing installation costs by as much as 30% due to unforeseen structural modifications.

- The volatility of global energy markets and inconsistent government policies create uncertainty, impacting the return on investment analysis. The lack of standardized financial models for quantifying secondary benefits like industrial water conservation makes it difficult to secure project approvals.

- Technical complexities related to handling diverse waste streams demand specialized corrosion-resistant alloys and waste heat recovery boilers, further escalating costs and complicating lifecycle cost assessment and carbon pricing impact.

Exclusive Technavio Analysis on Customer Landscape

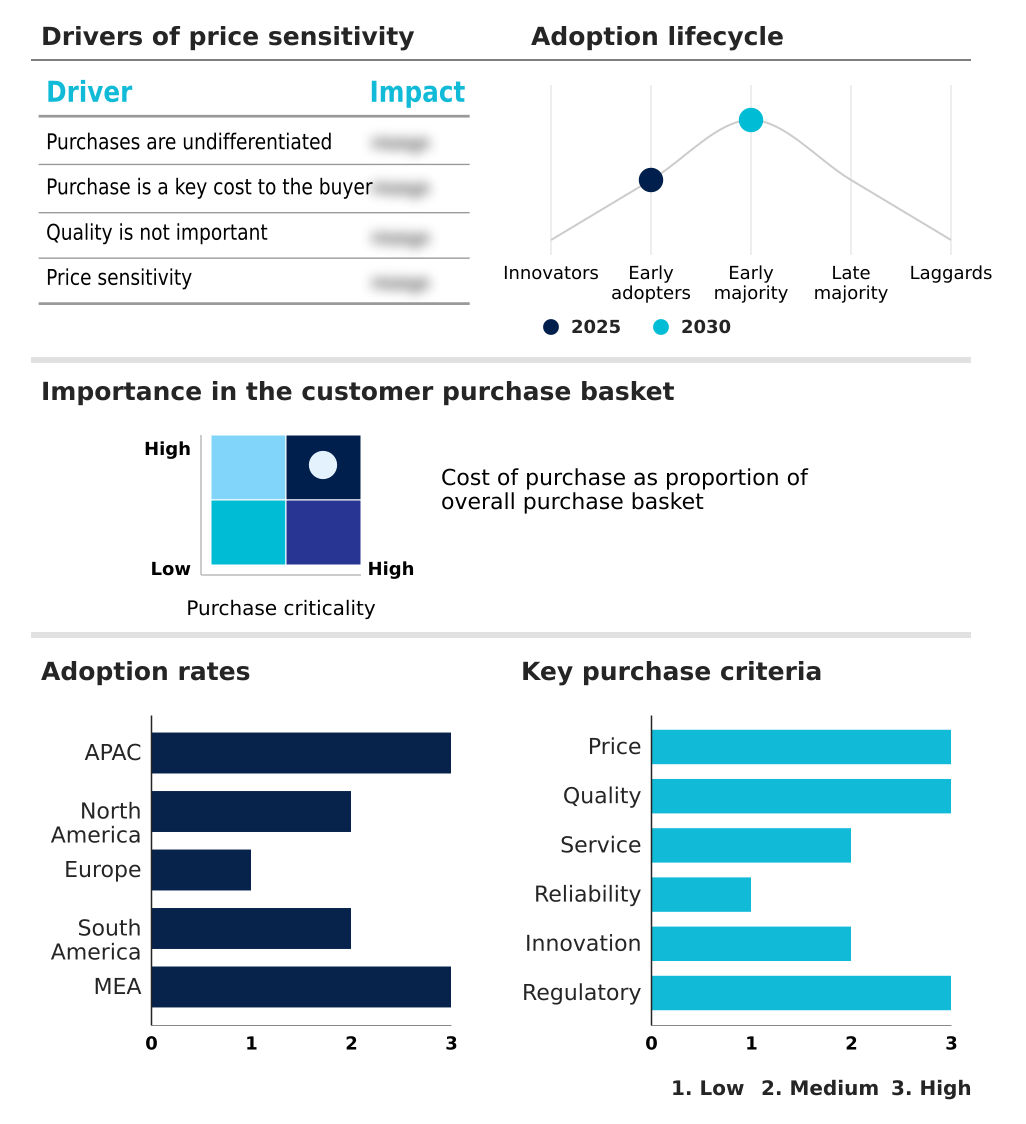

The industrial heat recovery systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial heat recovery systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Industrial Heat Recovery Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, industrial heat recovery systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Expertise in industrial heat recovery systems includes waste heat recovery for power generation and integrated solutions for low-temperature waste heat utilization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Alfa Laval AB

- Atlas Copco AB

- Danfoss AS

- Eastman Chemical Co.

- Emerson Electric Co.

- Forbes Marshall Pvt. Ltd.

- GEA Group AG

- Ingersoll Rand Inc.

- Johnson Controls International

- Kelvion Holding GmbH

- Mitsubishi Heavy Industries

- Pentair Plc

- Robert Bosch GmbH

- Shanghai Shenglin Technology Ltd.

- SPX FLOW Inc.

- SUEZ SA

- Sulzer Ltd.

- Thermax Ltd.

- Turboden SpA

- Viessmann Generations GmbH and Co

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial heat recovery systems market

- In May 2025, Johnson Controls finalized a landmark project in Northern Europe that successfully integrated the waste heat recovery system of a large-scale data center with a municipal district heating grid, demonstrating the potential for cross-sector collaboration.

- In August 2025, a large-scale textile manufacturing plant in Vietnam reported significant technical difficulties when attempting to install a condensing economizer system, as the existing exhaust stacks could not support the new equipment's weight.

- In September 2025, a major steel production facility in the United States completed the installation of a comprehensive waste heat to power system to stabilize its internal power supply against rising local electricity tariffs.

- In October 2025, Alfa Laval introduced a digital monitoring platform designed to enhance the heat transfer efficiency of plate heat exchangers by using predictive maintenance algorithms to prevent fouling and scaling.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Heat Recovery Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.4% |

| Market growth 2026-2030 | USD 32395.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.2% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, Italy, France, UK, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The industrial heat recovery systems market is advancing through sophisticated technological integration and a strategic focus on thermal energy circularity. The adoption of advanced thermal management ecosystems is no longer optional but a core component of competitive manufacturing, directly impacting boardroom decisions on capital expenditure and compliance.

- Key technologies such as high-temperature heat pumps, plate heat exchangers, and the organic rankine cycle are enabling unprecedented levels of thermal conversion efficiency. For example, facilities implementing comprehensive waste heat to power systems have reported up to a 40% reduction in reliance on grid electricity. Innovations in condensing economizer systems and modular recovery units are simplifying brownfield retrofits.

- The use of specialized thermal fluids and corrosion-resistant alloys extends equipment lifespan, while digital twin technology and predictive maintenance algorithms optimize performance. This shift toward industrial decarbonization is supported by energy performance contracting and the broader move to industrial electrification, with applications like preheating combustion air and process steam generation becoming standard.

- The ability to capture value from previously wasted resources through low-grade heat recovery, thermal storage systems, and heat recovery steam generators is reshaping industrial economics.

What are the Key Data Covered in this Industrial Heat Recovery Systems Market Research and Growth Report?

-

What is the expected growth of the Industrial Heat Recovery Systems Market between 2026 and 2030?

-

USD 32.40 billion, at a CAGR of 8.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Power and steam generation, Preheating, and Others), End-user (Energy generation, Petroleum refining, Chemical and petrochemical, Cement, and Others), Type (Medium temperature, Low temperature, and High temperature) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerating decarbonization initiatives and regulatory compliance, High Initial capital expenditure and extended payback periods

-

-

Who are the major players in the Industrial Heat Recovery Systems Market?

-

ABB Ltd., Alfa Laval AB, Atlas Copco AB, Danfoss AS, Eastman Chemical Co., Emerson Electric Co., Forbes Marshall Pvt. Ltd., GEA Group AG, Ingersoll Rand Inc., Johnson Controls International, Kelvion Holding GmbH, Mitsubishi Heavy Industries, Pentair Plc, Robert Bosch GmbH, Shanghai Shenglin Technology Ltd., SPX FLOW Inc., SUEZ SA, Sulzer Ltd., Thermax Ltd., Turboden SpA and Viessmann Generations GmbH and Co

-

Market Research Insights

- The market dynamics for industrial heat recovery systems are shaped by a strong focus on industrial energy optimization and enhancing asset performance management. The strategic implementation of these systems leads to measurable business outcomes, with some facilities achieving a 30% reduction in fuel consumption through efficient thermal load management.

- This directly improves return on investment analysis, making capital expenditure planning more attractive. Furthermore, alignment with circular economy principles and a stringent regulatory compliance framework is driving adoption, as companies in energy-intensive sectors seek to lower their carbon footprint.

- The integration of smart factory technologies with heat recovery hardware has improved thermal efficiency by over 15% in certain brownfield project retrofitting scenarios, showcasing the value of supply chain modernization and industrial water conservation.

We can help! Our analysts can customize this industrial heat recovery systems market research report to meet your requirements.

RIA -

RIA -