Europe Insurance Technology Market Size 2026-2030

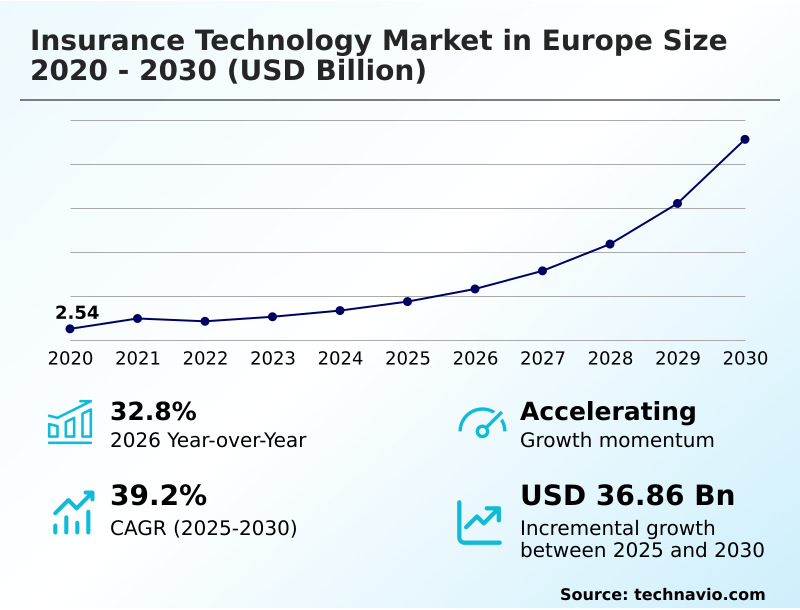

The europe insurance technology market size is valued to increase by USD 36.86 billion, at a CAGR of 39.2% from 2025 to 2030. Surge in personalized, data-driven insurance products will drive the europe insurance technology market.

Major Market Trends & Insights

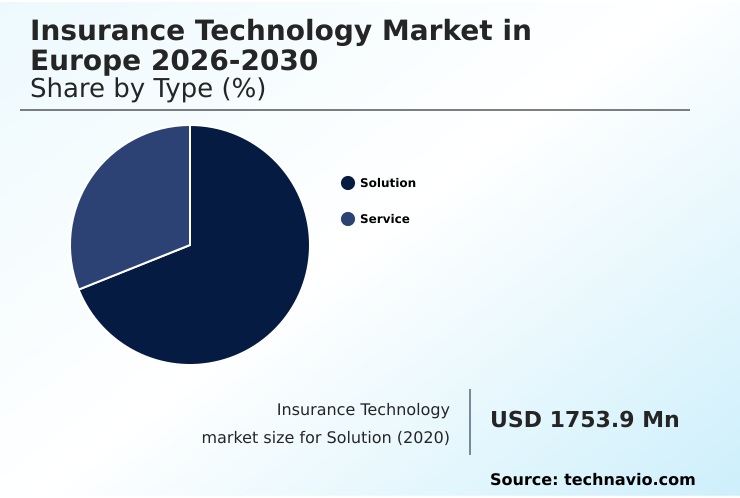

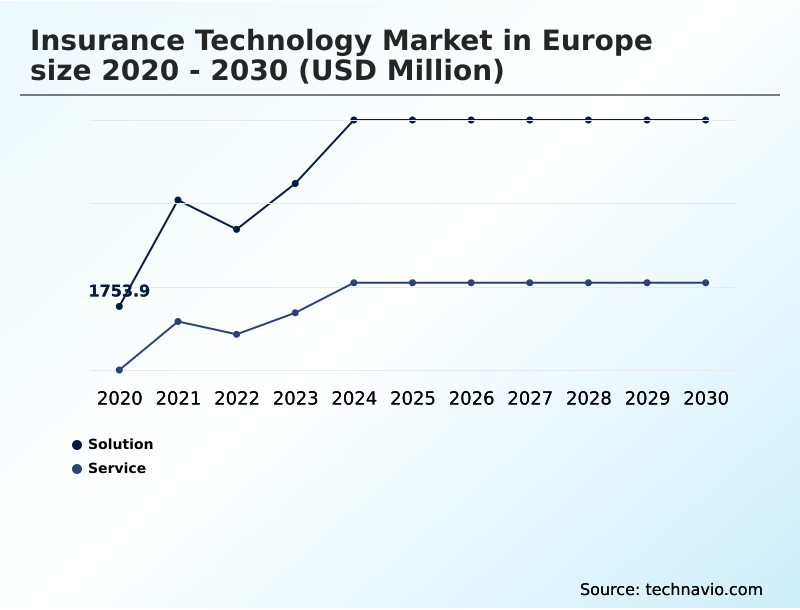

- By Type - Solution segment was valued at USD 4.58 billion in 2024

- By Technology - Cloud computing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 43.05 billion

- Market Future Opportunities: USD 36.86 billion

- CAGR from 2025 to 2030 : 39.2%

Market Summary

- The insurance technology market in Europe is undergoing a profound transformation, driven by the integration of advanced digital solutions into the traditional insurance value chain. This evolution is defined by the shift toward optimizing operational efficiency and refining risk assessment models through innovations like artificial intelligence, cloud computing, and IoT.

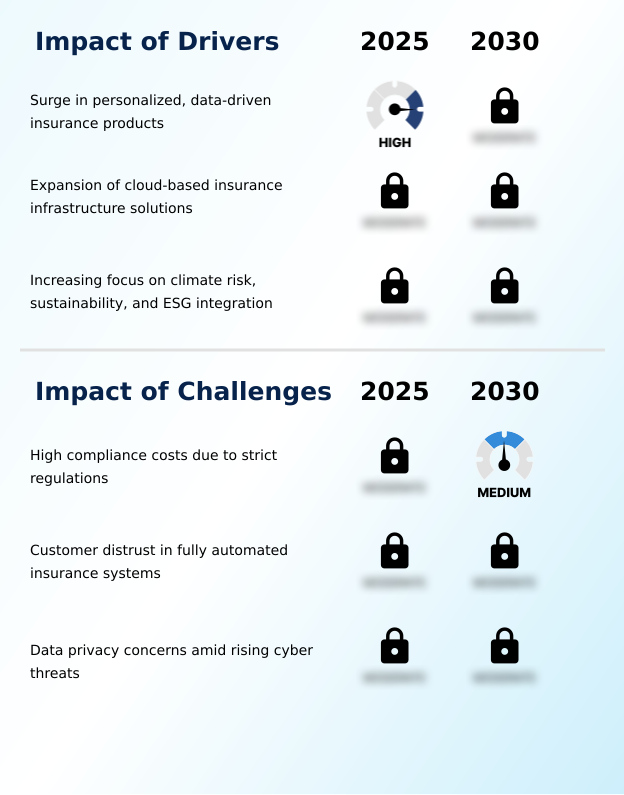

- A primary driver is the growing consumer demand for personalized, data-driven insurance products, compelling insurers to leverage predictive analytics for underwriting to offer hyper-customized policies. For example, a commercial fleet operator can now utilize telematics-based auto insurance to receive dynamic premiums based on real-time driving behavior, reducing costs and promoting safer practices.

- Key trends include rising partnerships between incumbent insurers and agile startups, which foster innovation in areas like automated claims processing and blockchain for fraud prevention.

- However, this progress is met with challenges such as high compliance costs due to strict regulations like GDPR and customer distrust in fully automated systems, requiring a delicate balance between technological advancement and maintaining consumer confidence.

What will be the Size of the Europe Insurance Technology Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Insurance Technology Market Segmented?

The europe insurance technology industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Solution

- Service

- Technology

- Cloud computing

- IoT

- Big data and business analytics

- Blockchain

- Others

- Application

- Policy administration and management

- Claims management

- Underwriting and risk assessment

- Fraud detection and prevention

- Others

- Geography

- Europe

- UK

- France

- Germany

- Europe

By Type Insights

The solution segment is estimated to witness significant growth during the forecast period.

The insurance technology market in Europe segmentation reflects a strategic shift from monolithic systems toward agile solutions and specialized services.

The solution segment, encompassing everything from a cloud-native insurance platform to an automated underwriting platform, dominates as carriers pursue legacy system modernization. Insurers are adopting AI-powered advisory platforms and tools for AI-driven health insights to enhance customer experience automation.

The service segment complements this by providing the expertise for implementation and digital transformation in insurance.

This comprehensive insurance technology ecosystem enables carriers to meet stringent insurtech regulatory compliance while improving operational efficiency, with some achieving a 30% reduction in administrative overhead through new platform adoption and even offering parametric climate risk insurance.

The Solution segment was valued at USD 4.58 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the European insurtech sector now hinges on a detailed cost-benefit analysis of smart contract settlement and comparing cloud-native vs legacy insurance platforms. Businesses are actively implementing AI for automated underwriting decisions and leveraging blockchain for transparent claims processing to gain a competitive edge.

- The benefits of telematics in usage-based insurance are becoming increasingly clear, as is the role of IoT sensors in property insurance for proactive risk mitigation. Insurers are using predictive analytics for dynamic risk pricing to offer more competitive and accurate rates. The impact of low-code platforms on policy administration is significant, streamlining workflows and reducing reliance on specialized IT teams.

- Furthermore, generative AI applications in insurance customer service are improving customer engagement with digital platforms. However, companies face challenges of insurtech regulatory compliance in europe and must develop clear strategies for modernizing core insurance systems. Developing API-driven embedded insurance products and integrating voice biometrics for policyholder security are key priorities.

- The optimization of claims management with computer vision has shown to improve accuracy by more than 15% over manual methods, while best practices for insurance fraud detection AI and real-time claims payment processing benefits are reshaping risk management. Building a resilient insurance technology ecosystem requires addressing data privacy considerations in AI risk modeling and automating policy lifecycle management for efficiency.

What are the key market drivers leading to the rise in the adoption of Europe Insurance Technology Industry?

- A key market driver is the surge in personalized, data-driven insurance products, reflecting a fundamental shift in consumer expectations and industry capabilities.

- The demand for insurance product personalization is a primary driver, pushing carriers to adopt technologies that enable dynamic risk assessment and customized offerings.

- This is accelerating the use of predictive analytics for underwriting and underwriting decision automation through various digital distribution channels.

- Insurers are investing in a digital insurance marketplace to streamline automated claims processing and enable straight-through claims processing for simple cases, reducing settlement times from days to hours. The adoption of smart contract settlement further enhances efficiency.

- Advanced fraud prevention analytics are also becoming critical, with some platforms improving detection accuracy by over 25%, directly impacting profitability and operational agility across the market.

What are the market trends shaping the Europe Insurance Technology Industry?

- A prominent market trend is the rise of strategic partnerships between traditional insurers and technology startups, aimed at accelerating digital transformation and enhancing customer experience.

- Strategic partnerships are fueling innovation across the insurance value chain optimization, enabling the integration of sophisticated technologies. A key trend is the deployment of API-driven insurance services, which facilitate the seamless integration of embedded insurance solutions at the point of sale. This approach supports the creation of data-driven insurance products, including telematics-based auto insurance.

- Insurers are also enhancing operational resilience in insurance through advanced AI fraud detection and blockchain for fraud prevention, with some firms achieving a 40% reduction in fraudulent claims processing. The focus on core insurance system replacement is accelerating the adoption of platforms capable of delivering real-time claims payments, meeting heightened consumer expectations for speed and transparency.

What challenges does the Europe Insurance Technology Industry face during its growth?

- A significant challenge restraining market growth is the high cost of compliance associated with navigating Europe's stringent and complex regulatory frameworks.

- Navigating data privacy and customer trust remains a central challenge, particularly with the expansion of usage-based insurance models and sophisticated AI-driven risk modeling. As carriers implement advanced policy administration systems and claims management automation, the need for transparent risk assessment models becomes critical. Integrating claims adjudication software that is both efficient and explainable is key to building consumer confidence.

- Furthermore, the deployment of generative AI for customer service and improvements in policy lifecycle management must be balanced with robust security protocols. Poorly managed customer engagement platforms can erode trust, with data showing that over 60% of consumers are wary of fully automated insurance pricing automation.

Exclusive Technavio Analysis on Customer Landscape

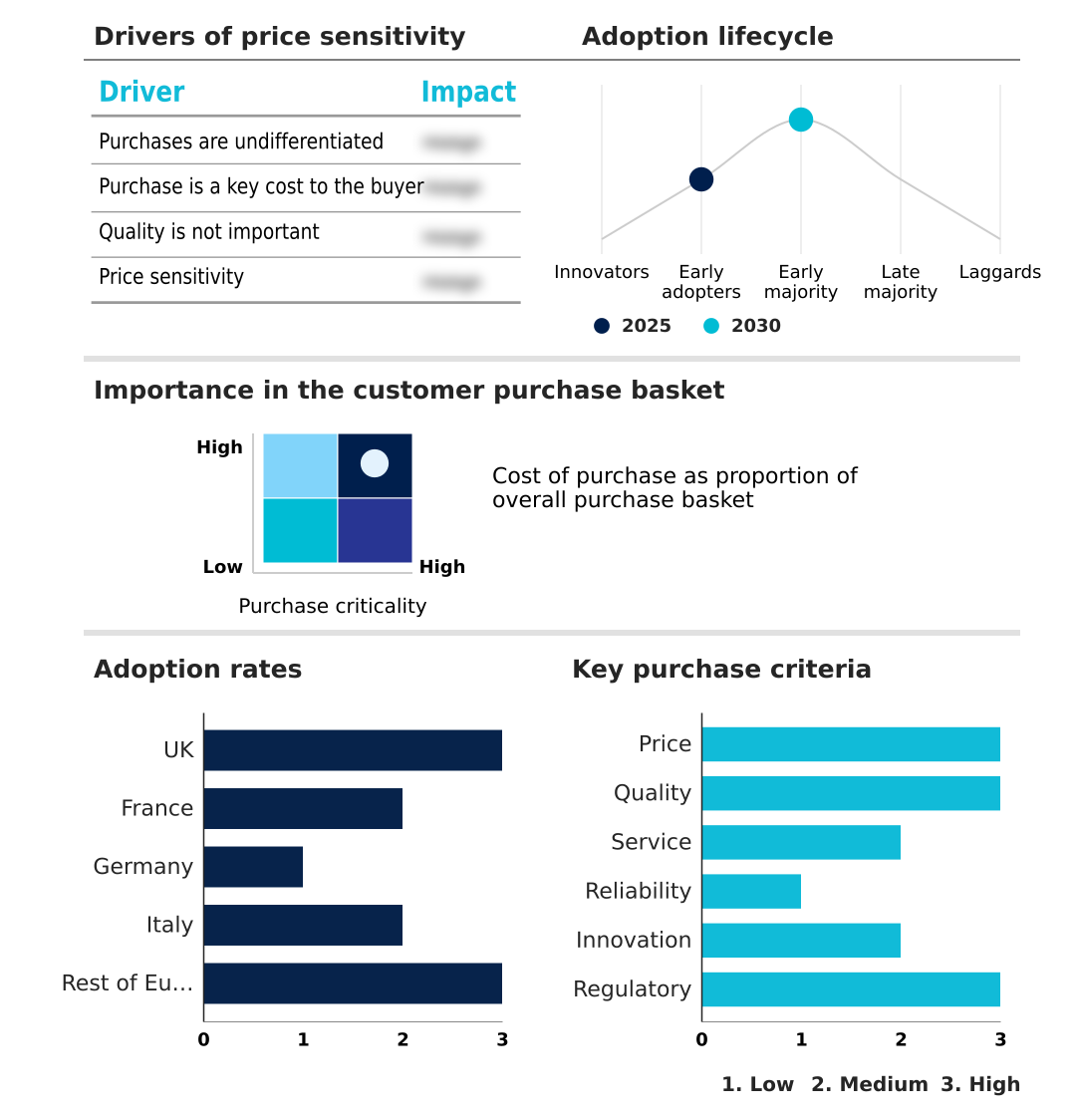

The europe insurance technology market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe insurance technology market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Insurance Technology Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe insurance technology market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alan SA - Delivers parametric insurance solutions for climate and catastrophe risks, leveraging data analytics for rapid, trigger-based payouts and enhanced portfolio resilience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alan SA

- Anorak Technologies Ltd.

- CFC Underwriting Ltd

- Charles Taylor Ltd.

- Cover Genius

- Damco Group

- Descartes Underwriting SAS

- Duck Creek Technologies LLC

- FRISS

- Getsafe Digital GmbH

- Guidewire Software Inc.

- INZMO Europe GmbH

- Majesco

- Powszechny Zaklad Ubezpieczen

- Shift Technology

- simplesurance GmbH

- wefox Holding AG

- Xempus AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe insurance technology market

- In August 2024, Duck Creek Technologies announced the general availability of Policy with Active Delivery, a cloud-native solution designed to eliminate the need for traditional software upgrades for property and casualty insurers.

- In October 2024, Allianz established a new European technology hub in Lisbon to centralize technical operations and leverage local talent to support its entities across the continent.

- In January 2025, Generali announced a research partnership with the Massachusetts Institute of Technology to explore the application of artificial intelligence in complex risk modeling and smart underwriting.

- In March 2025, Allianz UK confirmed a significant investment program to deploy new digital platforms designed to simplify trading for brokers and enhance pricing accuracy.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Insurance Technology Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 213 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 39.2% |

| Market growth 2026-2030 | USD 36861.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 32.8% |

| Key countries | UK, France, Germany, Italy and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The European insurtech landscape is rapidly maturing, driven by the adoption of advanced technologies designed to overhaul legacy operations. The move to a cloud-native insurance platform is foundational, enabling the deployment of an automated underwriting platform and AI-powered advisory platform that deliver AI-driven health insights.

- We are seeing a diversification of products, including parametric climate risk insurance and specialized telematics-based auto insurance. Key operational enhancements include automated claims processing and real-time claims payments, often facilitated by smart contract settlement and computer vision for damage assessment. The rise of embedded insurance solutions within a digital insurance marketplace is changing distribution.

- At a strategic level, boardrooms are prioritizing investments that deliver measurable efficiency gains; for instance, the integration of predictive analytics for underwriting has reduced policy issuance times by over 30%. Technologies like AI fraud detection, blockchain for fraud prevention, natural language processing for documents, and voice biometrics for security are now critical for dynamic risk assessment and claims management automation.

- This evolution is supported by generative AI for customer service, low-code development platforms, and sophisticated AI-driven risk modeling, all managed through modernized policy administration systems that support dynamic usage-based insurance models.

What are the Key Data Covered in this Europe Insurance Technology Market Research and Growth Report?

-

What is the expected growth of the Europe Insurance Technology Market between 2026 and 2030?

-

USD 36.86 billion, at a CAGR of 39.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Solution, and Service), Technology (Cloud computing, IoT, Big data and business analytics, Blockchain, and Others), Application (Policy administration and management, Claims management, Underwriting and risk assessment, Fraud detection and prevention, and Others) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Surge in personalized, data-driven insurance products, High compliance costs due to strict regulations

-

-

Who are the major players in the Europe Insurance Technology Market?

-

Alan SA, Anorak Technologies Ltd., CFC Underwriting Ltd, Charles Taylor Ltd., Cover Genius, Damco Group, Descartes Underwriting SAS, Duck Creek Technologies LLC, FRISS, Getsafe Digital GmbH, Guidewire Software Inc., INZMO Europe GmbH, Majesco, Powszechny Zaklad Ubezpieczen, Shift Technology, simplesurance GmbH, wefox Holding AG and Xempus AG

-

Market Research Insights

- The insurance technology ecosystem is defined by a rapid push toward legacy system modernization and customer experience automation. This digital transformation in insurance is enabling operational resilience in insurance, with firms that adopt API-driven insurance services reporting a 30% reduction in product development timelines compared to traditional methods.

- The optimization of the insurance value chain through data-driven insurance products has led to significant efficiency gains, such as a 40% decrease in call center volume through AI-powered customer service. As insurers navigate complex insurtech regulatory compliance, the focus remains on leveraging technology for both growth and risk management.

We can help! Our analysts can customize this europe insurance technology market research report to meet your requirements.

RIA -

RIA -