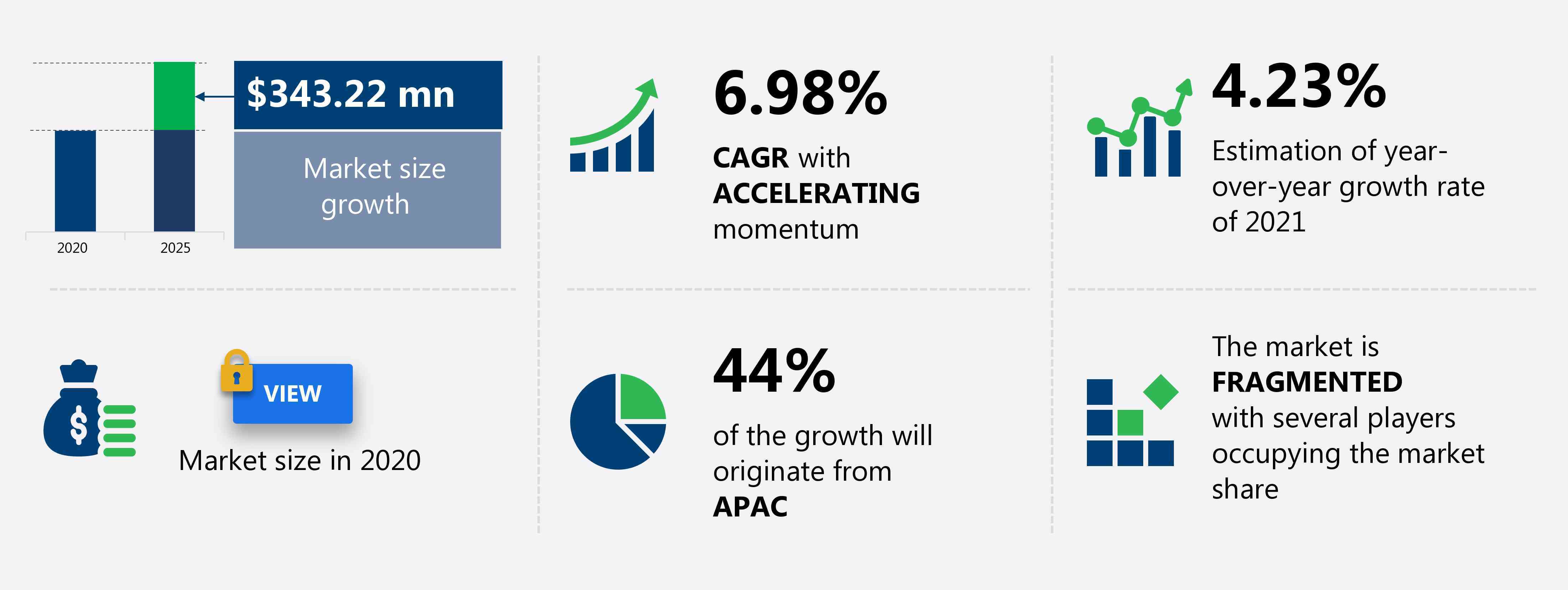

The interface ip market share is expected to increase by USD 343.22 million from 2020 to 2025, and the market’s growth momentum will accelerate at a CAGR of 6.98%.

This interface ip market research report provides valuable insights on the post COVID-19 impact on the market, which will help companies evaluate their business approaches. Furthermore, this report extensively covers interface ip market segmentations by end-user (fabless semiconductor company, idms, and foundries), type (USB, DDRn, PCIe, ethernet, and others), and geography (APAC, North America, Europe, South America, and MEA). The interface ip market report also offers information on several market vendors, including Achronix Semiconductor Corp., Cadence Design Systems Inc., CEVA Inc., eMemory Technology Inc., Lattice Semiconductor Corp., Marvell Technology Group Ltd., Rambus Inc., SoftBank Group Corp., Synopsys Inc., and Xilinx Inc. among others.

What will the Interface IP Market Size be During the Forecast Period?

Download the Free Report Sample to Unlock the Interface IP Market Size for the Forecast Period and Other Important Statistics

Interface IP Market: Key Drivers, Trends, and Challenges

Based on our research output, there has been a neutral impact on the market growth during and post COVID-19 era. The increase in demand for modern soc chips is notably driving the interface ip market growth, although factors such as heavy investments driven by ip core design complexity may impede market growth. Our research analysts have studied the historical data and deduced the key market drivers and the COVID-19 pandemic impact on the interface ip industry. The holistic analysis of the drivers will help in deducing end goals and refining marketing strategies to gain a competitive edge.

Key Interface IP Market Driver

The growing design complexity are one of the key factors driving the growth of the global Interface IP market. Electronic device manufacturers currently try to offer products that have better functionalities while offering power-packed performances in comparison to the previous offerings or the older generations of the same product. This has compelled semiconductor chip manufacturers to ensure that their IC designs are capable of offering high performance. This has catapulted the product development process in the semiconductor industry. Vendors are pitting against each other in terms of the timely delivery of offerings while ensuring high-performing and multi-functional devices. To deliver such high-end multi-functional products, semiconductor device manufacturers have come up with the new and complex architecture and designs of semiconductor ICs. For instance, 3D ICs are compact in size and are more efficient in performance. In addition, they consume less power and have a complex design and manufacturing process. This design complexity will generally hamper the overall productivity of the industry as the number of manufacturing processes has increased considerably. The comparison of the product designing complexity and manufacturing indicates that the designing complexity is growing at a rate of 5% more than the manufacturing productivity.

Key Interface IP Market Trend

The growth of in-vehicle networks will fuel the global Interface IP market growth. The exponential increase in the deployment of advanced electronics, such as actuators, microcontrollers, and sensors, to enable in-vehicle communication is driving the growth of automotive communication protocols. Consumers are demanding smart features in automotive vehicles for convenience, entertainment, and safety. Thus, automotive OEMs are incorporating smart features, such as advanced driver-assistance systems (ADAS), antilock braking systems, automatic transmissions, central locking, and engine management systems, in vehicles. Moreover, the growing demand for higher bandwidth applications and the exponential increase in the number of electronic control modules in vehicles is expected to escalate the number of nodes connected by serial bus protocols. Growth in the number of connected nodes in vehicles will increase the demand for SoCs integrated with automotive communication protocols. The number of connected cars is expected to increase further because of the growing demand for safety features in automotive vehicles and the tightening of vehicle safety regulations. This is expected to accelerate the development of new SoC designs by incorporating advanced IP blocks, which will result in the rapid growth of the global interface IP market during the forecast period.

Key Interface IP Market Challenge

The heavy investments driven by IP core design complexity is a major challenge for the global Interface IP market growth. The design and developmental costs of semiconductor IPs are getting increasingly complex and expensive. This is because semiconductor IP vendors need to invest additional time and money to develop complex algorithms for addressing the growing needs of customers. In addition, heavy investments in R&D by semiconductor IP vendors are resulting in a high price per license and high royalty charges. Moreover, apart from the high cost of R&D investment, there are other cost-related factors involved in the semiconductor IP core development process. The cost of hard IPs is expected to increase at lesser nodes (at 20 nanometers) as a result of the transformation of original transistor devices. However, the same does not occur in the case of soft IPs unless the IP vendor is wholeheartedly involved in the development of the IP. This can be illustrated by taking the example of unconventional complementary metal-oxide-semiconductor (CMOS) processes such as the FinFET tool, which will indirectly increase the cost of soft IPs.

This interface ip market analysis report also provides detailed information on other upcoming trends and challenges that will have a far-reaching effect on the market growth. The actionable insights on the trends and challenges will help companies evaluate and develop growth strategies for 2021-2025.

Parent Market Analysis

Technavio categorizes the global interface IP market as a part of the global semiconductor market, within the overall global semiconductors and semiconductor equipment market. Our research report has extensively covered external factors influencing the parent market growth potential in the coming years, which will determine the levels of growth of the interface ip market during the forecast period.

Who are the Major Interface IP Market Vendors?

The report analyzes the market’s competitive landscape and offers information on several market vendors, including:

- Achronix Semiconductor Corp.

- Cadence Design Systems Inc.

- CEVA Inc.

- eMemory Technology Inc.

- Lattice Semiconductor Corp.

- Marvell Technology Group Ltd.

- Rambus Inc.

- SoftBank Group Corp.

- Synopsys Inc.

- Xilinx Inc.

This statistical study of the interface ip market encompasses successful business strategies deployed by the key vendors. The interface ip market is fragmented and the vendors are deploying growth strategies such as price, quality, technology, brand identity, and distribution to compete in the market.

Product Insights and News

- Achronix Semiconductor Corp. - The company offers interface IP such as Speedcore eFPGA IP.

To make the most of the opportunities and recover from post COVID-19 impact, market vendors should focus more on the growth prospects in the fast-growing segments, while maintaining their positions in the slow-growing segments.

The interface ip market forecast report offers in-depth insights into key vendor profiles. The profiles include information on the production, sustainability, and prospects of the leading companies.

Interface IP Market Value Chain Analysis

Our report provides extensive information on the value chain analysis for the interface ip market, which vendors can leverage to gain a competitive advantage during the forecast period. The end-to-end understanding of the value chain is essential in profit margin optimization and evaluation of business strategies. The data available in our value chain analysis segment can help vendors drive costs and enhance customer services during the forecast period.

The value chain of the global semiconductor market includes the following core components:

- Inputs

- Inbound logistics

- Operations

- Outbound logistics

- Marketing and sales

- Service

- Support activities

- Innovation

The report has further elucidated on other innovative approaches being followed by service providers to ensure a sustainable market presence.

Which are the Key Regions for Interface IP Market?

For more insights on the market share of various regions Request for a FREE sample now!

44% of the market’s growth will originate from APAC during the forecast period. China, and Japan are the key markets for the interface ip market in APAC. Market growth in this region will be faster than the growth of the market in regions.

The growing design complexity will facilitate the interface ip market growth in APAC over the forecast period. This market research report entails detailed information on the competitive intelligence, marketing gaps, and regional opportunities in store for vendors, which will assist in creating efficient business plans.

COVID Impact and Recovery Analysis

The interface IP market in APAC witnessed certain challenges in 2020, owing to the COVID-19 outbreak. The outbreak affected many countries in the region, such as China, India, South Korea, and Japan. Since early 2020, many countries have been imposing nationwide lockdowns to prevent the community's spread of the disease. The outbreak affected the economy, supply chains, and the industrial and commercial sectors in the region. However, in 2021, the initiation of large-scale vaccination drives has lifted the lockdown and travel restrictions, which led to the resumption of supply chain activities. Such factors are expected to drive the market during the forecast period.

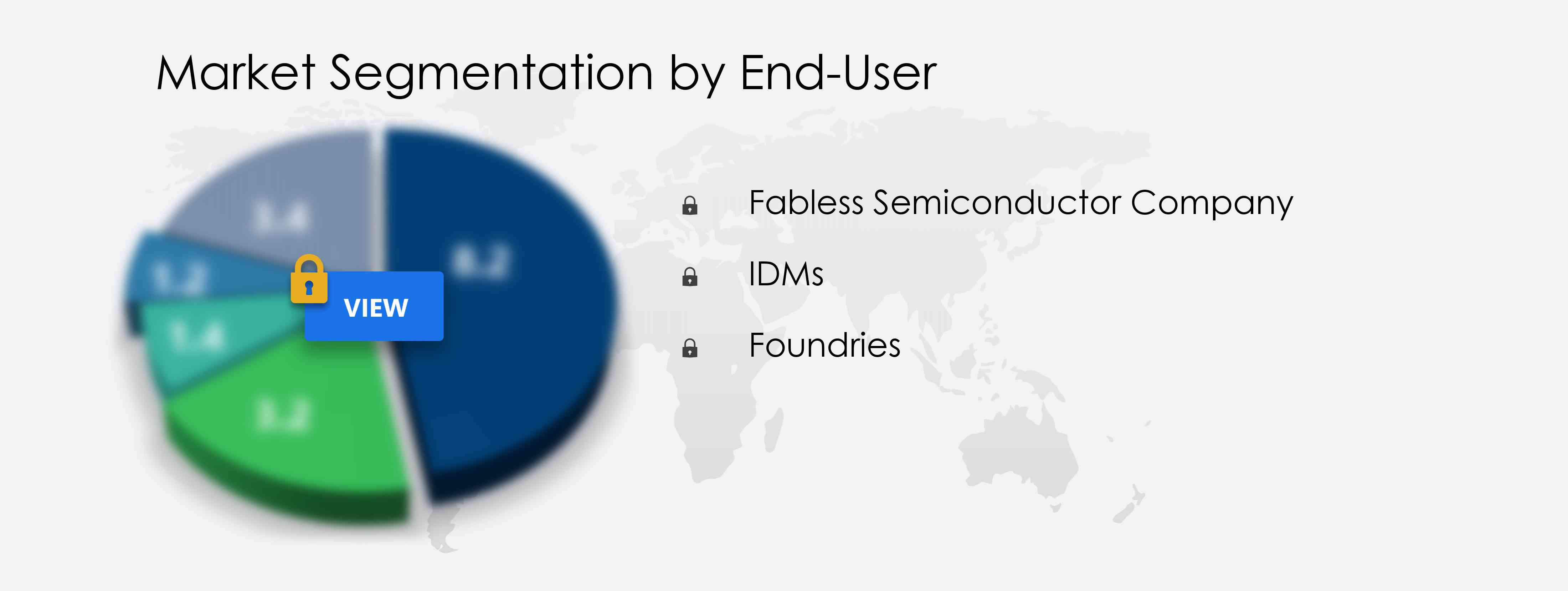

What are the Revenue-generating End-User Segments in the Interface IP Market?

To gain further insights on the market contribution of various segments Request for a FREE sample

The interface ip market share growth by the fabless semiconductor company segment will be significant during the forecast period. Fabless semiconductor companies only consider the design aspect of the semiconductor device. The main reason for this is to reduce the overhead expenses related to maintaining manufacturing units.

This report provides an accurate prediction of the contribution of all the segments to the growth of the interface ip market size and actionable market insights on post COVID-19 impact on each segment.

|

Interface IP Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

120 |

|

Base year |

2020 |

|

Forecast period |

2021-2025 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.98% |

|

Market growth 2021-2025 |

$ 343.22 million |

|

Market structure |

Fragmented |

|

YoY growth (%) |

4.23 |

|

Regional analysis |

APAC, North America, Europe, South America, and MEA |

|

Performing market contribution |

APAC at 44% |

|

Key consumer countries |

US, China, South Korea (Republic of Korea), Japan, and Germany |

|

Competitive landscape |

Leading companies, Competitive strategies, Consumer engagement scope |

|

Key companies profiled |

Achronix Semiconductor Corp., Cadence Design Systems Inc., CEVA Inc., eMemory Technology Inc., Lattice Semiconductor Corp., Marvell Technology Group Ltd., Rambus Inc., SoftBank Group Corp., Synopsys Inc., and Xilinx Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Interface IP Market Report?

- CAGR of the market during the forecast period 2021-2025

- Detailed information on factors that will drive interface ip market growth during the next five years

- Precise estimation of the interface ip market size and its contribution to the parent market

- Accurate predictions on upcoming trends and changes in consumer behavior

- The growth of the interface ip industry across APAC, North America, Europe, South America, and MEA

- A thorough analysis of the market’s competitive landscape and detailed information on vendors

- Comprehensive details of factors that will challenge the growth of interface ip market vendors

We can help! Our analysts can customize this report to meet your requirements. Get in touch

RIA -

RIA -