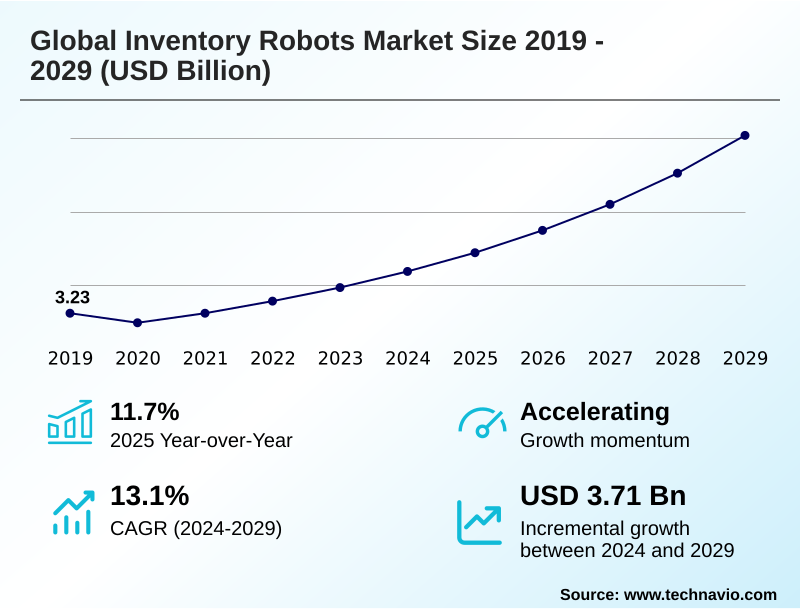

Inventory Robots Market Size 2025-2029

The inventory robots market size is valued to increase by USD 3.71 billion, at a CAGR of 13.1% from 2024 to 2029. Escalating labor shortages and rising labor costs will drive the inventory robots market.

Major Market Trends & Insights

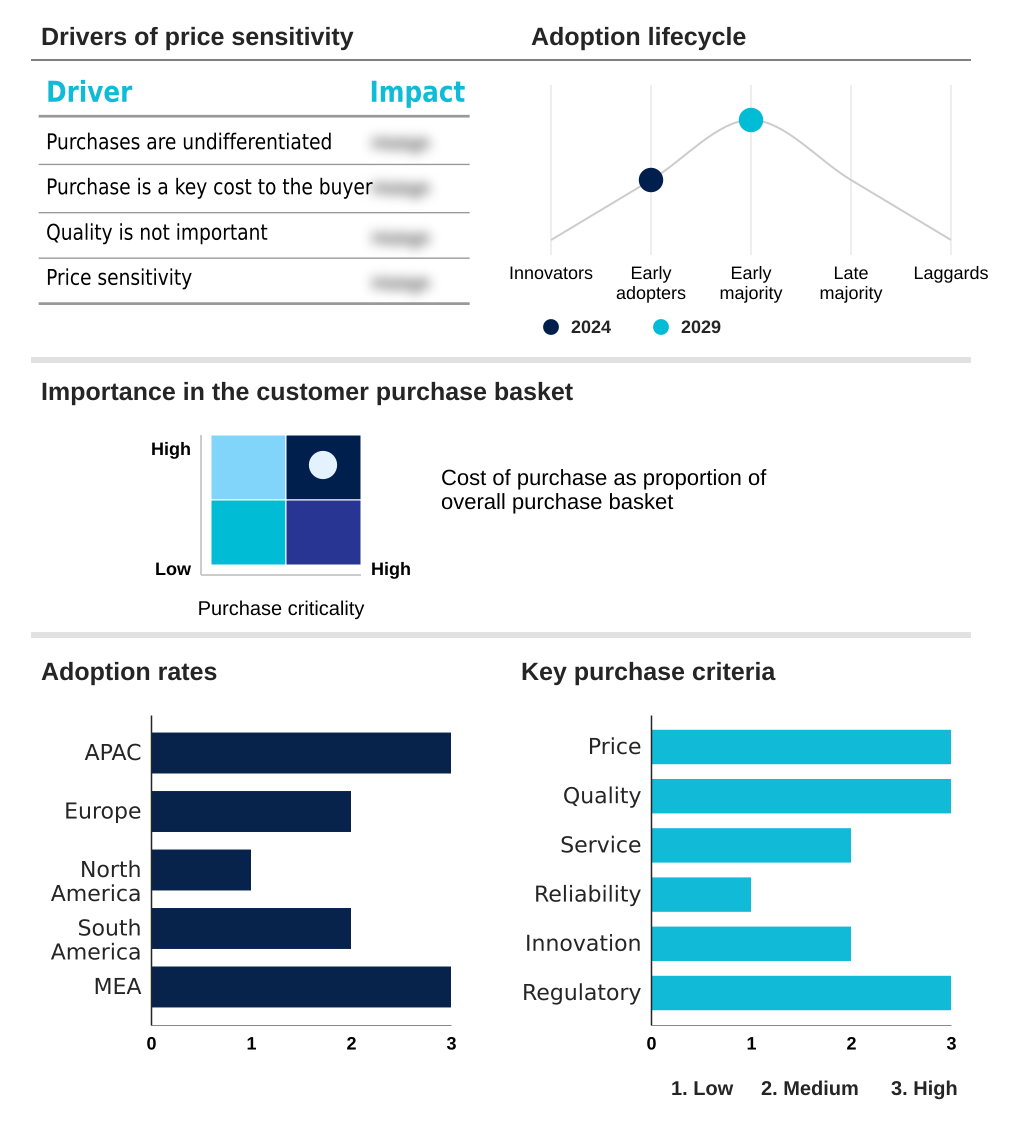

- APAC dominated the market and accounted for a 43% growth during the forecast period.

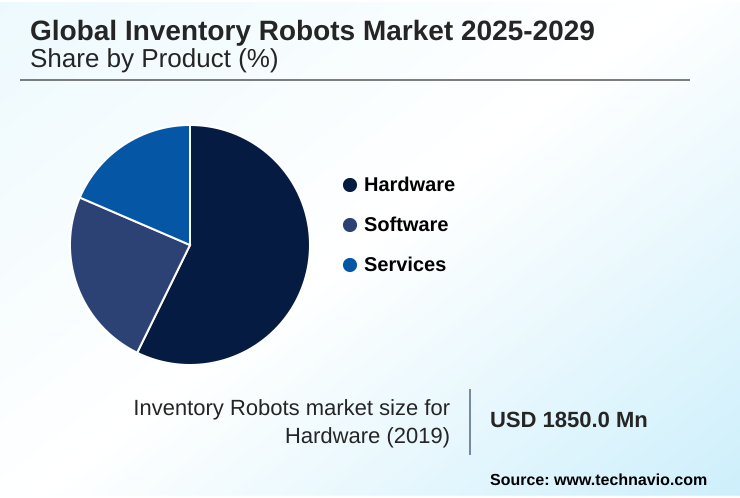

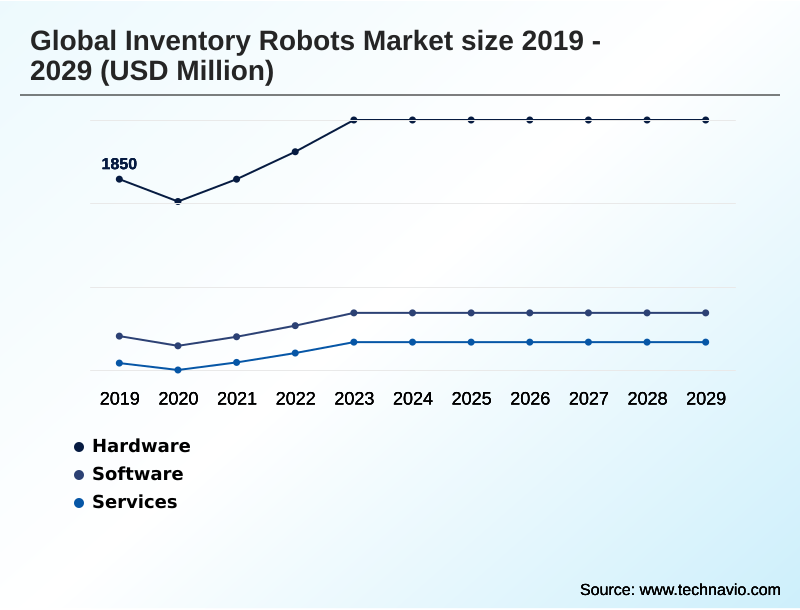

- By Product - Hardware segment was valued at USD 2.25 billion in 2023

- By Application - Warehousing segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 4.85 billion

- Market Future Opportunities: USD 3.71 billion

- CAGR from 2024 to 2029 : 13.1%

Market Summary

- The inventory robots market is undergoing a profound transformation, driven by the convergence of economic pressures and technological maturation. Persistent labor shortages and the escalating complexity of e-commerce fulfillment are compelling businesses to adopt automation for operational continuity and efficiency.

- A key trend is the integration of advanced artificial intelligence, evolving robots from simple automated guided vehicles to intelligent autonomous mobile robots capable of dynamic navigation and decision-making. For instance, an e-commerce fulfillment center can deploy a fleet of robots for goods-to-person picking, which not only increases throughput but also enhances order fulfillment accuracy by minimizing human error.

- These systems leverage computer vision and machine learning algorithms for precise item handling. However, significant challenges remain, including the high upfront capital investment and the technical complexities of integrating robotic fleets with legacy warehouse management systems.

- The growing availability of robotics-as-a-service (RaaS) models is helping to mitigate financial barriers, making advanced automation more accessible and allowing companies to scale their operations flexibly in response to market demands. The market is thus characterized by a strategic shift towards intelligent, data-driven automation as a cornerstone of resilient and competitive supply chain operations.

What will be the Size of the Inventory Robots Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Inventory Robots Market Segmented?

The inventory robots industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Hardware

- Software

- Services

- Application

- Warehousing

- Retail

- Manufacturing

- Type

- Autonomous mobile robots

- Automated guided vehicles

- Fixed robotics

- Geography

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- France

- Italy

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Product Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment, encompassing physical systems like autonomous mobile robots and automated guided vehicles, is foundational to improving warehouse operational efficiency.

Innovations in LiDAR sensor technology and 3D vision systems are enhancing navigational precision, while advancements in end-of-arm tooling expand task capabilities, directly addressing e-commerce fulfillment complexity.

These physical assets are critical for high-density storage retrieval and require careful robotic systems integration, especially in brownfield integration scenarios. Deployments are demonstrating significant operational throughput enhancement, with some achieving a 2-3x boost in productivity.

Strategic investment in this segment is driven by the need for greater supply chain resilience and is carefully weighed against the total cost of ownership.

The Hardware segment was valued at USD 2.25 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Inventory Robots Market Demand is Rising in APAC Get Free Sample

The geographic landscape is led by APAC, which accounts for 43% of the incremental growth, driven by massive e-commerce and manufacturing sectors demanding supply chain optimization.

North America follows, with a strong focus on data-driven logistics and omnichannel inventory management to serve its mature retail market.

In these advanced regions, technologies such as RFID-enabled autonomous systems and autonomous drone system are deployed for perpetual inventory scanning and inventory shrinkage control.

Innovations in simultaneous localization and mapping support complex navigation, while a focus on human-robot collaboration addresses labor dynamics. Europe emphasizes just-in-time production integration, using robotics for tasks like robotic piece-picking and ensuring planogram compliance monitoring.

Niche applications like cold storage logistics are also gaining traction globally.

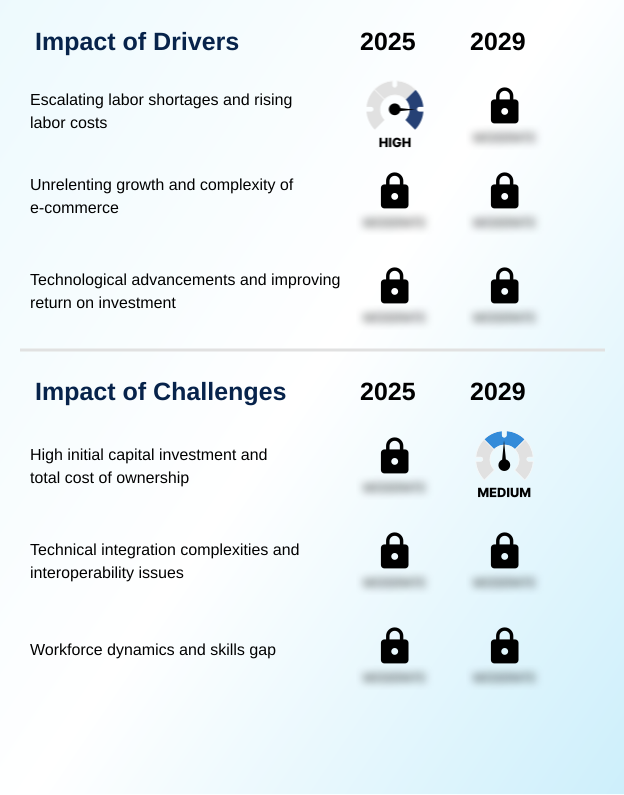

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of logistics is heavily influenced by the adoption of autonomous mobile robots for e-commerce fulfillment, which directly addresses the need for speed and accuracy. The success of these systems hinges on core technologies like SLAM technology for dynamic warehouse navigation, allowing robots to operate effectively in constantly changing environments.

- Further intelligence is added through AI-powered computer vision for item recognition, which is critical for handling diverse product catalogs. A major focus for operators is integrating AMRs with existing WMS platforms to create a unified data ecosystem for real-time decision-making. The business case is often proven by the strong ROI of goods-to-person robotic systems.

- However, enterprises must also navigate the challenges of robotic bin picking implementation for handling smaller, unstructured items. For large-scale inventory audits, many are now using drones for automated cycle counting, which can achieve accuracy levels over 99%, a significant improvement over manual methods that often hover below 95%.

- The financial accessibility is improving, with robotics-as-a-service pricing models explained as a viable OpEx alternative. In retail, improving planogram compliance with shelf-scanning robots is a key use case. All these connected systems demand robust cybersecurity protocols for autonomous robot fleets. As deployments grow, so does the importance of human-robot collaboration safety standards and optimizing fleet management for swarm robotics.

- Specialized applications, such as robotic automation in cold chain logistics, are also expanding, driven by tailored brownfield automation integration strategies. Looking ahead, using digital twins to simulate robot workflows will be standard practice for reducing order fulfillment errors with robotics.

- The debate over AMR vs AGV for manufacturing logistics continues, while innovation in robotic piece-picking for heterogeneous items and real-time inventory tracking with RFID robots advances. Finally, the full potential will be unlocked by the impact of 5G on warehouse robot connectivity.

What are the key market drivers leading to the rise in the adoption of Inventory Robots Industry?

- Escalating labor shortages and rising labor costs are a primary driver propelling the adoption of inventory robots across global supply chains.

- Persistent labor shortages and the increasing complexity of omnichannel retail fulfillment are primary market drivers. For labor shortage mitigation, businesses are deploying systems for automated case handling and line-side feeding automation.

- E-commerce demands for speed and order fulfillment accuracy are met by goods-to-person methodology and robotic sorting systems, which can increase pick rates by over 200% and reduce order cycle time reduction significantly.

- Technologies such as automated cycle counting and robotic palletizing depalletizing provide real-time inventory visibility, which is crucial for modern supply chains.

- The favorable return on investment calculation, driven by declining hardware costs and proven efficiency gains from goods-to-person picking, makes adoption a strategic imperative for competitive logistics operations.

What are the market trends shaping the Inventory Robots Industry?

- The market is witnessing a dominant trend where advanced artificial intelligence is being integrated into inventory robots, moving systems beyond simple automation toward cognitive capabilities for real-time adaptation.

- A dominant trend is the shift towards cognitive automation, powered by AI-powered data analytics and advanced computer vision systems. Intelligent orchestration software, often delivered via a cloud-based software platform, enables swarm intelligence algorithms for superior coordination, while digital twin simulation optimizes workflows before deployment. This facilitates real-time data analytics, improving forecast accuracy by over 15% and enabling predictive maintenance alerts.

- The proliferation of subscription-based robotics models and flexible deployment models is lowering entry barriers, making niche application specialization for tasks like cold storage feasible for more businesses. These fleet management software advancements are accelerating the path toward lights-out warehouse automation, where facilities achieve continuous operation with minimal human oversight.

What challenges does the Inventory Robots Industry face during its growth?

- The high initial capital investment and total cost of ownership present a primary challenge affecting widespread market adoption and industry growth.

- Significant challenges hinder widespread adoption, led by technical integration complexities. Achieving seamless warehouse management system integration with warehouse execution systems is a major hurdle, with nearly 40% of projects facing delays due to interoperability issues.

- The lack of universal system interoperability standards complicates the deployment of mixed fleets, including AI-enabled autonomous systems like autonomous shelf-scanning units and a mobile RFID robot. The technical sophistication required for tasks like robotic bin picking demands advanced machine learning algorithms and robust cybersecurity for robotic systems.

- Furthermore, the human element presents a dual challenge, requiring effective change management strategies to ease workforce anxieties and comprehensive workforce upskilling programs to fill critical technical roles, which is essential for stock-out prevention and inventory distortion reduction.

Exclusive Technavio Analysis on Customer Landscape

The inventory robots market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the inventory robots market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Inventory Robots Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, inventory robots market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Badger Technologies LLC - Delivering highly mobile robotic systems for automated data capture and complex case handling in dynamic logistics environments, enhancing operational visibility and material flow.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Badger Technologies LLC

- Bastian Solutions LLC

- Bossa Nova Robotics

- Boston Dynamics Inc.

- Brain Corp.

- Clearpath Robotics Inc.

- Corvus Robotics Inc.

- Dexory Ltd.

- Grey Orange Pte. Ltd.

- inVia Robotics Inc.

- Jabil Inc.

- Keonn Technologies

- KION GROUP AG

- Locus Robotics Corp.

- MetraLabs GmbH

- PAL Robotics

- RightHand Robotics Inc.

- Simbe Robotics Inc.

- Vecna Robotics Inc.

- Zebra Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Inventory robots market

- In April 2025, Locus Robotics Corp. announced it surpassed 5 billion units picked using its AMR fleet, achieving the latest billion picks just 24 weeks after the previous milestone in October 2024.

- In March 2025, Boston Dynamics Inc. announced a strategic partnership with a leading logistics provider to deploy its Stretch robot for autonomous trailer unloading across a network of 50 distribution centers.

- In December 2024, Grey Orange Pte. Ltd. secured a significant Series D funding round of $150 million to accelerate the global expansion of its AI-driven fulfillment platform and enhance R&D in robotic piece-picking.

- In September 2024, Zebra Technologies Corp. launched its new suite of RFID-enabled autonomous inventory scanning robots, designed to provide retailers with 99.9% inventory accuracy through daily autonomous cycle counts.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Inventory Robots Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 13.1% |

| Market growth 2025-2029 | USD 3708.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 11.7% |

| Key countries | China, Japan, South Korea, India, Taiwan, Indonesia, Germany, France, Italy, UK, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The inventory robots market is evolving from basic material transport to intelligent, data-driven operations. Core platforms include autonomous mobile robots and automated guided vehicles, orchestrated by fleet management software and intelligent orchestration software. Navigation relies on simultaneous localization and mapping with LiDAR sensor technology.

- Onboard computer vision systems and 3D vision systems, powered by machine learning algorithms and AI-powered data analytics, enable complex tasks. A key trend impacting boardroom strategy is the shift to specialized applications, with deployments showing productivity boosts of over 200%. This includes robotic piece-picking using advanced end-of-arm tooling, goods-to-person methodology, robotic bin picking, and automated case handling.

- For large-scale movement, robotic palletizing depalletizing and robotic sorting systems are critical. Achieving real-time inventory visibility is a primary goal, accomplished through perpetual inventory scanning, automated cycle counting via an autonomous drone system, autonomous shelf-scanning units, or a mobile RFID robot as part of RFID-enabled autonomous systems.

- Seamless warehouse management system integration with warehouse execution systems is paramount for success, facilitated by a cloud-based software platform. This ecosystem also supports line-side feeding automation, high-density storage retrieval, and planogram compliance monitoring, all while emphasizing human-robot collaboration and leveraging swarm intelligence algorithms in these AI-enabled autonomous systems.

What are the Key Data Covered in this Inventory Robots Market Research and Growth Report?

-

What is the expected growth of the Inventory Robots Market between 2025 and 2029?

-

USD 3.71 billion, at a CAGR of 13.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Hardware, Software, and Services), Application (Warehousing, Retail, and Manufacturing), Type (Autonomous mobile robots, Automated guided vehicles, and Fixed robotics) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating labor shortages and rising labor costs, High initial capital investment and total cost of ownership

-

-

Who are the major players in the Inventory Robots Market?

-

Badger Technologies LLC, Bastian Solutions LLC, Bossa Nova Robotics, Boston Dynamics Inc., Brain Corp., Clearpath Robotics Inc., Corvus Robotics Inc., Dexory Ltd., Grey Orange Pte. Ltd., inVia Robotics Inc., Jabil Inc., Keonn Technologies, KION GROUP AG, Locus Robotics Corp., MetraLabs GmbH, PAL Robotics, RightHand Robotics Inc., Simbe Robotics Inc., Vecna Robotics Inc. and Zebra Technologies Corp.

-

Market Research Insights

- The market's dynamics are shaped by a strategic push for warehouse operational efficiency and greater supply chain resilience. The adoption of robotics addresses critical challenges like labor shortage mitigation and e-commerce fulfillment complexity. Flexible and scalable automation delivers measurable business outcomes, with deployments demonstrating a 2-3x increase in productivity and reducing order picking errors by up to 60%.

- This significantly improves order fulfillment accuracy and strengthens the return on investment calculation. As companies increasingly focus on data-driven logistics and supply chain optimization, they are turning to advanced systems that support omnichannel inventory management. The availability of flexible deployment models further accelerates adoption, enabling businesses to enhance their competitive posture in a rapidly evolving landscape.

We can help! Our analysts can customize this inventory robots market research report to meet your requirements.

RIA -

RIA -