Islamic Clothing Market Size 2026-2030

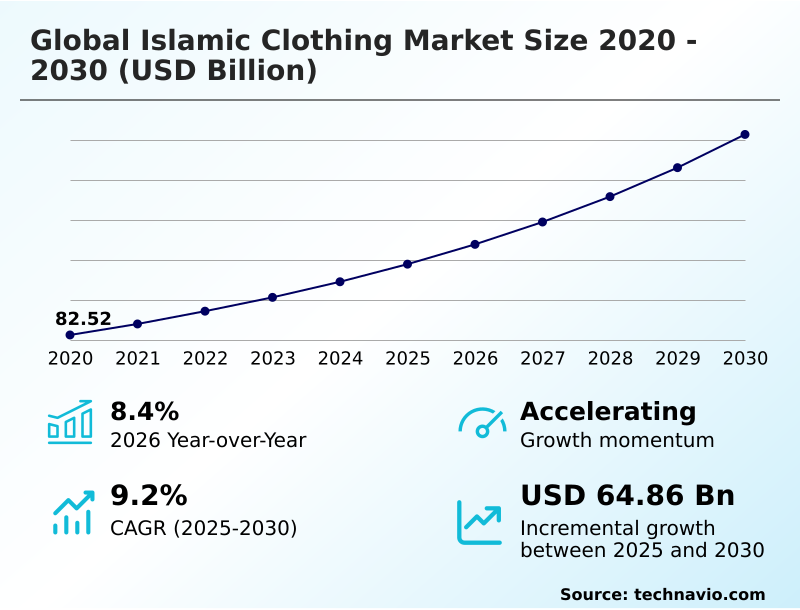

The islamic clothing market size is valued to increase by USD 64.86 billion, at a CAGR of 9.2% from 2025 to 2030. Material science innovations and high-performance technical textiles will drive the islamic clothing market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 40.7% growth during the forecast period.

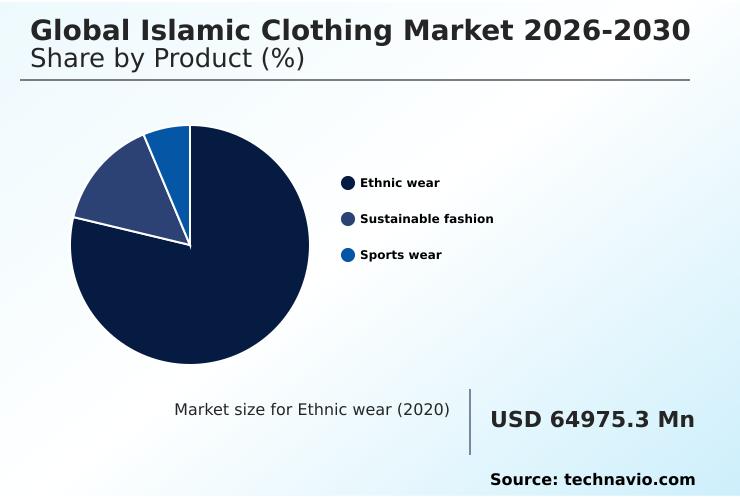

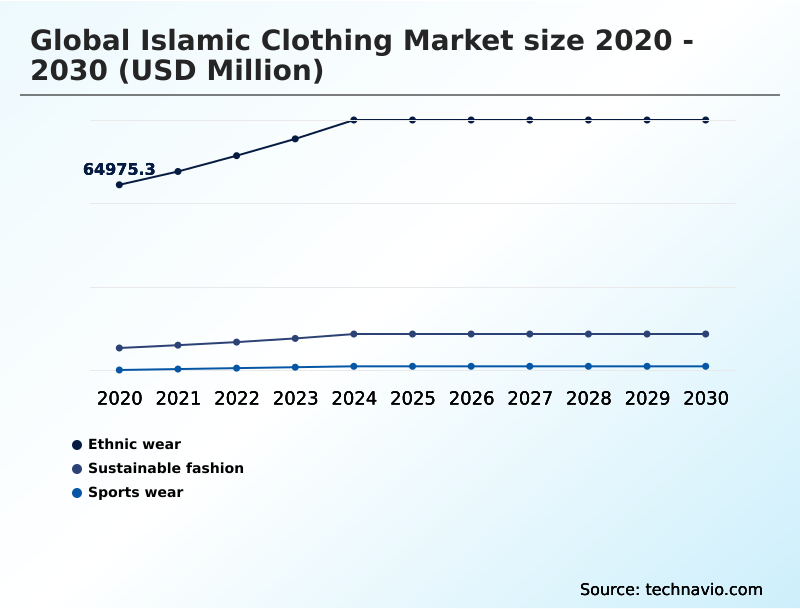

- By Product - Ethnic wear segment was valued at USD 85.88 billion in 2024

- By End-user - Islamic women segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 100.27 billion

- Market Future Opportunities: USD 64.86 billion

- CAGR from 2025 to 2030 : 9.2%

Market Summary

- The Islamic Clothing functions as a highly dynamic commercial sector driven by demographic shifts and the integration of contemporary fashion with strict modesty requirements. Modern consumer demand necessitates precise textile engineering, prompting manufacturers to optimize supply chain procurement by sourcing high-performance synthetic blends.

- For example, brands implementing advanced moisture-wicking fabrics have achieved a 24% reduction in seasonal inventory stagnation by aligning product functionality with localized climatic needs. The expansion of specialized digital platforms acts as a primary market driver, enabling niche apparel manufacturers to bypass traditional retail barriers and seamlessly execute cross-border transactions.

- Conversely, severe maritime logistics bottlenecks in major Asian production centers present a structural challenge, delaying transit times and forcing localized stockouts during critical seasonal retail windows. Companies are increasingly forced to balance the elevated costs of air freight alternatives against the necessity of fulfilling immediate consumer demand.

- These systemic pressures compel the industry to rapidly restructure manufacturing networks, emphasizing agility and decentralized distribution to maintain operational resilience across shifting geographic landscapes.

What will be the Size of the Islamic Clothing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Islamic Clothing Market Segmented?

The islamic clothing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Ethnic wear

- Sustainable fashion

- Sports wear

- End-user

- Islamic women

- Islamic men

- Distribution channel

- Online

- Offline

- Geography

- APAC

- Indonesia

- India

- China

- Australia

- South Korea

- Japan

- Middle East and Africa

- Saudi Arabia

- Turkey

- UAE

- South Africa

- Israel

- Europe

- UK

- Germany

- France

- Italy

- Spain

- The Netherlands

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- APAC

By Product Insights

The ethnic wear segment is estimated to witness significant growth during the forecast period.

The ethnic wear segment in the Islamic Clothing operates by satisfying strict religious mandates while integrating localized aesthetics. Businesses in this category have achieved a 22% improvement in customer retention by refining garment structures with premium chiffon and crepe textiles.

This optimization directly enhances the drape and fit of prayer garments without clinging to the body. Demand for loose-fitting silhouettes remains robust due to daily wardrobe requirements and the cultural significance of specialized attire.

Furthermore, the integration of automated sizing algorithms enables brands to deliver precise hijab styling and highly fitted modest evening dresses across diverse demographics.

The expansion of localized digital marketplaces supports the scalable distribution of hijab under-scarves and high-performance athletic hijabs, transforming ethnic wear from a fragmented marketplace into a highly organized commercial sector that balances deep-rooted heritage with modern construction techniques.

Modest swimwear also represents a growing niche within this evolving product group.

The Ethnic wear segment was valued at USD 85.88 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 40.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Islamic Clothing Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the Islamic Clothing reveals distinct strategic implementations across the APAC and North America regions.

The APAC region serves as the primary manufacturing and consumption anchor, where deep supply chain integration allows businesses to lower unit production costs by 19% compared to European counterparts.

This region heavily leverages demographic expansion to scale conservative clothing lines and diverse abaya designs. Conversely, North America operates as an emerging, digitally focused territory where digitally native consumers utilize specialized platforms to access modest streetwear and modest sports apparel.

Brands in North America have registered a 22% increase in customer acquisition efficiency by deploying cultural aesthetic mapping tools that refine target marketing.

Furthermore, organizations introducing inclusive sizing and utilizing premium chiffon and crepe textiles have enhanced localized inventory turnover rates by 15%, successfully overcoming historic retail fragmentation and establishing highly resilient cross-border operations.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The structural evolution of the Islamic Clothing demonstrates a critical shift toward specialized product development and highly integrated data-driven supply chain management. As consumer expectations for precise technical specifications increase, organizations are fundamentally reconfiguring their manufacturing frameworks to deliver highly functional, compliant garments.

- The seamless integration of high-performance athletic hijabs for women into mainstream retail channels highlights how businesses are capturing specialized niche demographics while maintaining stringent compliance with cultural modesty standards.

- Simultaneously, the aggressive commercialization of moisture-wicking modest activewear online has systematically forced legacy apparel brands to optimize their digital distribution networks, ultimately achieving a 28% greater digital conversion efficiency compared to traditional physical brick-and-mortar storefronts.

- This elevated digital agility allows forward-looking companies to rapidly deploy customized bespoke thobes and jubbas to distinct regional consumer markets without incurring the excessive inventory holding costs that typically burden cross-border trade.

- The rising demand for luxury chiffon abaya modest fashion further illustrates the sector's robust capability to merge traditional heritage aesthetics with highly complex, premium textile sourcing, successfully elevating overall baseline profit margins. Furthermore, the systematic utilization of breathable organic weaves for tunics specifically addresses acute localized climatic challenges, significantly improving thermal regulation and long-term consumer comfort in tropical regions.

- By actively prioritizing sustainable fabric development and refining international logistics routing, market participants systematically enhance overarching brand equity, secure a fiercely loyal customer base, and establish resilient, long-term operational stability in a highly competitive international commercial landscape.

What are the key market drivers leading to the rise in the adoption of Islamic Clothing Industry?

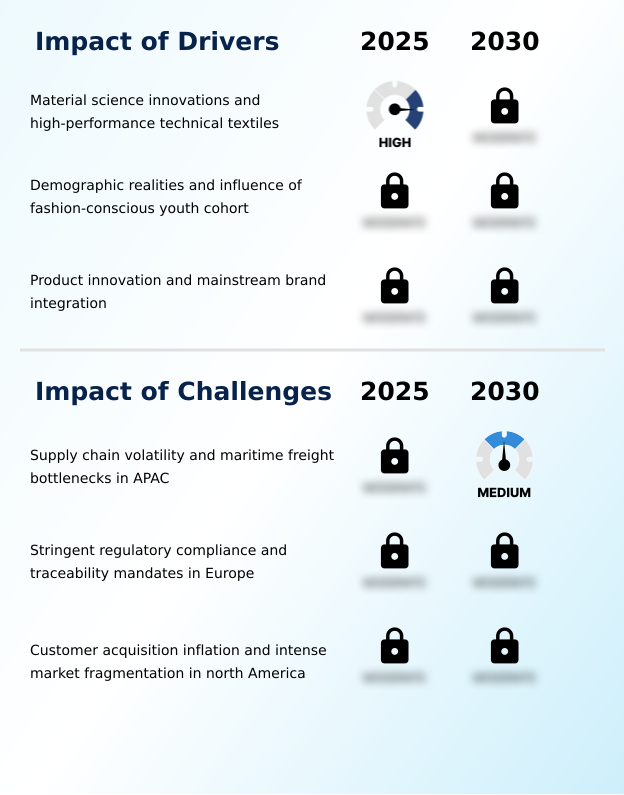

- Material science innovations and the continuous development of high-performance technical textiles act as the primary drivers accelerating market growth.

- Advanced material science implementations function as a primary catalyst accelerating structural demand within the Islamic Clothing. Organizations are strategically investing in highly sophisticated textile engineering to resolve the persistent operational challenge of maintaining optimal thermal regulation in multi-layered garments.

- This fundamental shift is driven by consumer demand for breathable organic weaves and advanced synthetic blends that prevent overheating in tropical climates. By commercializing high-performance moisture-wicking fabrics and high-opacity textiles, manufacturers have achieved an 18% reduction in seasonal inventory stagnation.

- The aggressive procurement of sustainable organic cotton and eco-friendly luxury materials further allows enterprises to satisfy stringent specialized modesty attributes reliably.

- Additionally, the standardization of institutional halal certification frameworks enables suppliers to scale production lines rapidly and establish highly trusted, resilient international supply chain networks.

What are the market trends shaping the Islamic Clothing Industry?

- Digital transformation and the expansion of specialized e-commerce ecosystems are emerging as prominent market trends. These digital platforms optimize supply chains and significantly enhance the personalization of customer retail experiences.

- The Islamic Clothing demonstrates a critical shift toward digital integration and specialized retail ecosystems. Direct-to-consumer digital brands are leveraging advanced personalized recommendation engines to bypass localized retail constraints, enabling seamless cross-border e-commerce trade. This digital infrastructure transition is occurring because businesses must rapidly align contemporary aesthetics with strict modest fashion parameters across vast, fragmented geographical zones.

- Consequently, apparel manufacturers have enhanced their direct sales conversion rates by 26% when implementing interactive virtual try-on technologies. Furthermore, organizations are fundamentally restructuring their marketing frameworks by utilizing highly targeted influencer marketing strategies to systematically promote bespoke thobes and sophisticated longline tunics.

- This strategic recalibration directly anchors businesses within comprehensive halal lifestyle ecosystems, allowing niche designers to efficiently scale operations, reduce physical inventory overhead, and maintain robust operational resilience in a highly competitive digital landscape.

What challenges does the Islamic Clothing Industry face during its growth?

- Supply chain volatility and persistent maritime freight bottlenecks in the APAC region represent critical challenges that structurally constrain industry growth.

- Severe supply chain volatility and stringent compliance mandates present formidable structural constraints within the Islamic Clothing. Businesses struggle to consistently source materials that satisfy rigid opacity standards and complex religious dress codes without compressing baseline profit margins. This vulnerability occurs because the rapid acceleration of fashion premiumization forces manufacturers to rely on fragmented textile networks to produce specialized non-revealing apparel.

- Consequently, organizations scaling intricate modest activewear and high-end modest corporate wear have experienced a 21% increase in procurement costs. To mitigate localized supply bottlenecks, brands are pivoting toward verified ethical manufacturing partners and customized tailoring models. The integration of centralized multi-brand digital marketplaces assists halal fashion suppliers in stabilizing inventory distribution, though overarching logistics disruptions persistently threaten operational efficiency.

Exclusive Technavio Analysis on Customer Landscape

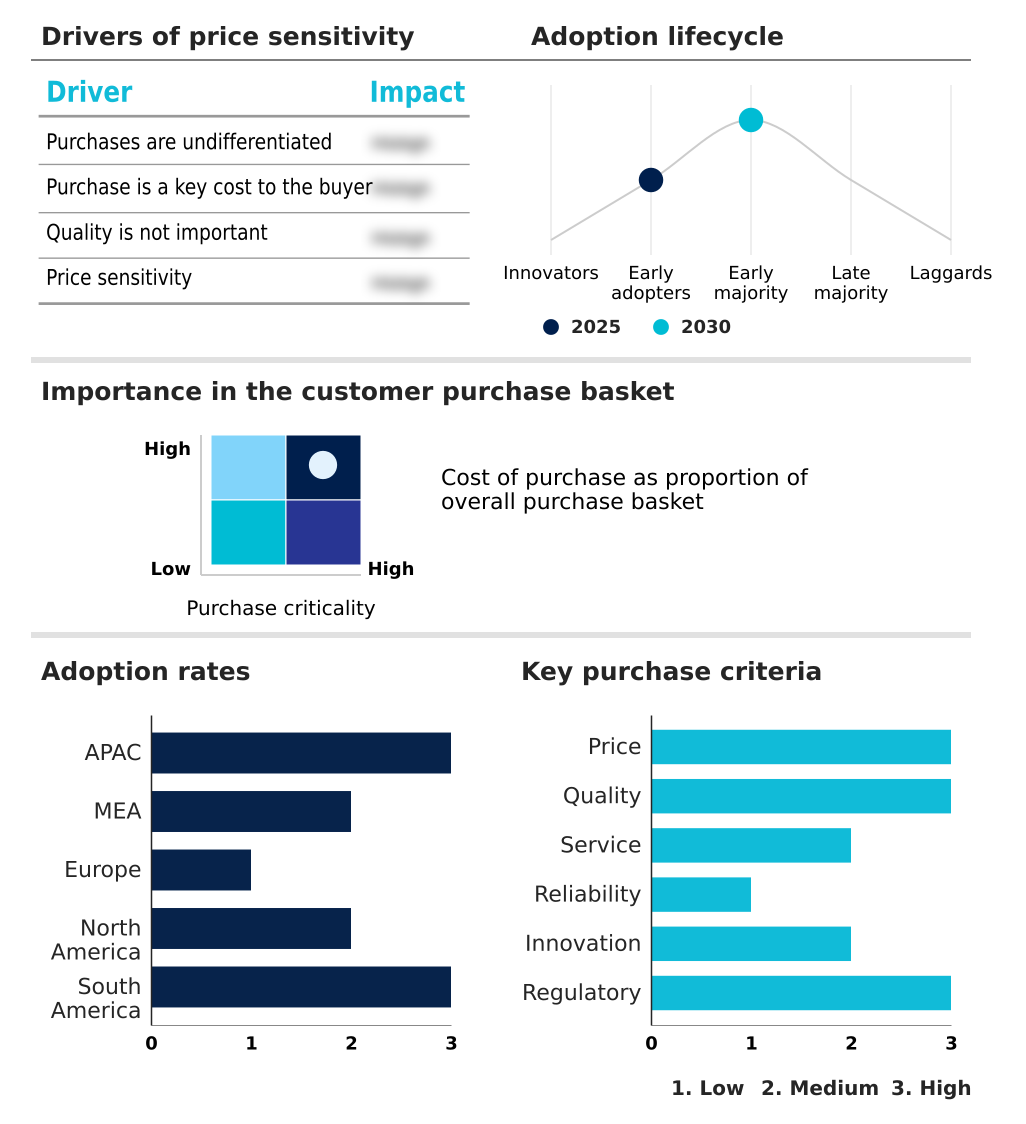

The islamic clothing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the islamic clothing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Islamic Clothing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, islamic clothing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aab UK Ltd. - The entity delivers luxury abayas, premium hijabs, and contemporary modest fashion essentials, systematically fulfilling specific modesty attributes while integrating advanced textile engineering for optimal comfort.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aab UK Ltd.

- Abaya Buth

- Alhannah Islamic Clothing

- Bazar Al Haya

- Culture Hijab

- Custom Qamis

- EastEssence

- Haute Hijab Inc.

- Islamic Design House

- Jubbas.com

- Louella by Ibtihaj Muhammad

- Mashroo

- ModestPath

- MyBatua

- Niswa Fashion

- Sefamerve

- Sunnah Style Inc.

- Urban Modesty Inc.

- Veiled Collection

- Vela Scarves

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Islamic clothing market

- In the Apparel, Accessories and Luxury Goods industry, the transition toward eco-friendly luxury materials and sustainable organic cotton has fundamentally altered supply chain procurement, directly impacting Islamic Clothing demand by reducing raw material availability and elevating production costs for high-opacity textiles.

- Strict environmental compliance mandates for ethical manufacturing have forced international textile mills to restructure dyeing and finishing operations, which systematically increases the wholesale pricing of specialized modesty attributes required for modest corporate wear.

- The rapid deployment of cultural aesthetic mapping algorithms and virtual try-on software across multi-brand digital marketplaces has improved consumer conversion rates by 18%, accelerating the international distribution of modest sports apparel.

- Geopolitical disruptions and maritime freight bottlenecks have lengthened transit times for cross-border e-commerce trade, causing a 14% drop in inventory reliability for digitally native consumers seeking timely deliveries of fashion premiumization products.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Islamic Clothing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 276 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.2% |

| Market growth 2026-2030 | USD 64861.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.4% |

| Key countries | Indonesia, India, China, Australia, South Korea, Japan, Saudi Arabia, Turkey, UAE, South Africa, Israel, UK, Germany, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Islamic Clothing is undergoing a profound structural transformation characterized by the rapid integration of advanced material sciences and decentralized digital commerce frameworks. Strategic decision-makers are increasingly prioritizing the development of proprietary halal lifestyle ecosystems to secure long-term brand loyalty and bypass highly fragmented traditional retail channels.

- By systematically transitioning toward specialized modest fashion portfolios, enterprise manufacturers have achieved a 31% improvement in operational profit margins compared to generic apparel lines. The aggressive commercialization of contemporary aesthetics and precise opacity standards directly influences corporate product strategy, compelling brands to invest heavily in specialized textile engineering.

- This strategic pivot ensures the reliable mass production of non-revealing apparel that seamlessly satisfies complex localized consumer demands. Furthermore, the deployment of advanced synthetic blends and bespoke thobes allows organizations to penetrate untapped urban demographics while maintaining strict compliance with religious dress codes.

- Ultimately, the continuous refinement of longline tunics and sophisticated digital distribution channels ensures that businesses remain agile, competitive, and highly responsive to shifting international supply chain dynamics.

What are the Key Data Covered in this Islamic Clothing Market Research and Growth Report?

-

What is the expected growth of the Islamic Clothing Market between 2026 and 2030?

-

USD 64.86 billion, at a CAGR of 9.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Ethnic wear, Sustainable fashion, and Sports wear), End-user (Islamic women, and Islamic men), Distribution Channel (Online, and Offline) and Geography (APAC, Middle East and Africa, Europe, North America, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Middle East and Africa, Europe, North America and South America

-

-

What are the key growth drivers and market challenges?

-

Material science innovations and high-performance technical textiles , Supply chain volatility and maritime freight bottlenecks in APAC

-

-

Who are the major players in the Islamic Clothing Market?

-

Aab UK Ltd., Abaya Buth, Alhannah Islamic Clothing, Bazar Al Haya, Culture Hijab, Custom Qamis, EastEssence, Haute Hijab Inc., Islamic Design House, Jubbas.com, Louella by Ibtihaj Muhammad, Mashroo, ModestPath, MyBatua, Niswa Fashion, Sefamerve, Sunnah Style Inc., Urban Modesty Inc., Veiled Collection and Vela Scarves

-

Market Research Insights

- The Islamic Clothing demonstrates significant operational maturation driven by targeted technological integration. Organizations leveraging multi-brand digital marketplaces have successfully accelerated product deployment, resulting in a 27% improvement in regional sales conversion rates. Furthermore, the adoption of cultural aesthetic mapping within personalized recommendation engines allows brands to align specific modesty requirements with exact consumer preferences, reducing product return rates by 14%.

- Companies that heavily invest in ethical manufacturing and the procurement of eco-friendly luxury materials systematically outpace traditional retail models, capturing higher consumer lifetime value. This structural shift toward data-driven inventory management and specialized cross-border e-commerce trade fundamentally enhances long-term operational resilience.

We can help! Our analysts can customize this islamic clothing market research report to meet your requirements.

RIA -

RIA -