IT Workflow Automation Platforms (non-itsm) Market Size 2026-2030

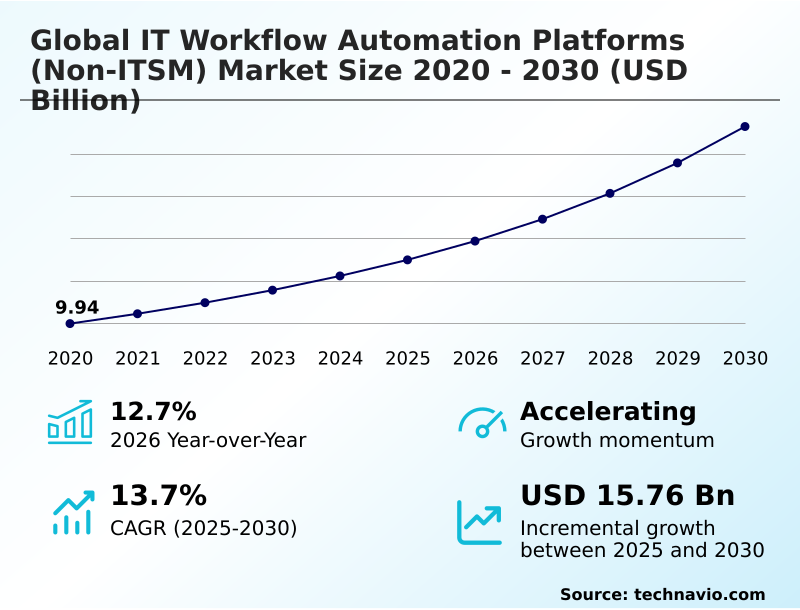

The it workflow automation platforms (non-itsm) market size is valued to increase by USD 15.76 billion, at a CAGR of 13.7% from 2025 to 2030. Escalating complexity of multi-cloud and hybrid infrastructure environments will drive the it workflow automation platforms (non-itsm) market.

Major Market Trends & Insights

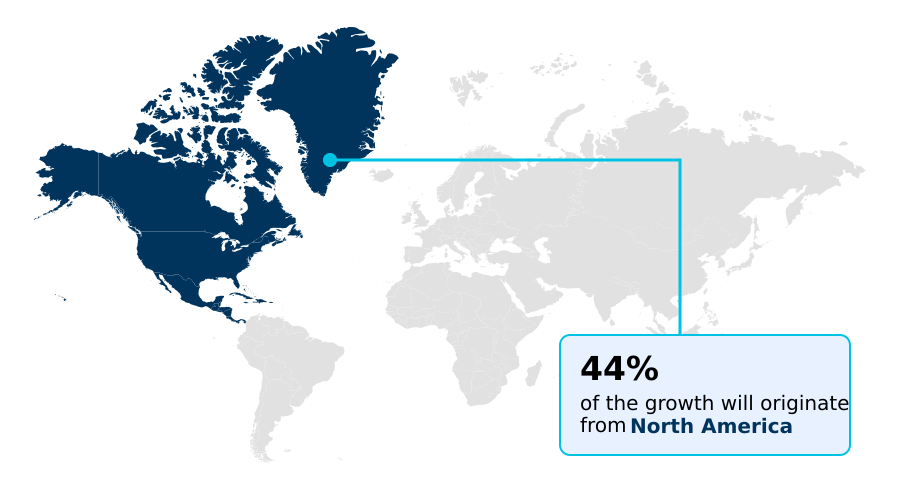

- North America dominated the market and accounted for a 43.9% growth during the forecast period.

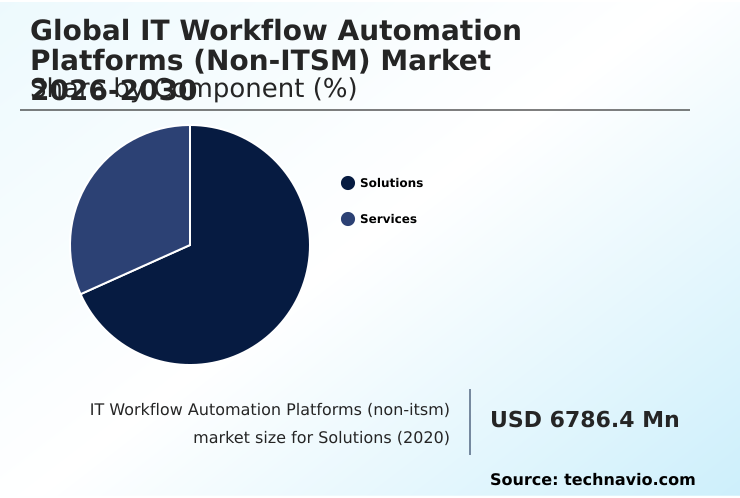

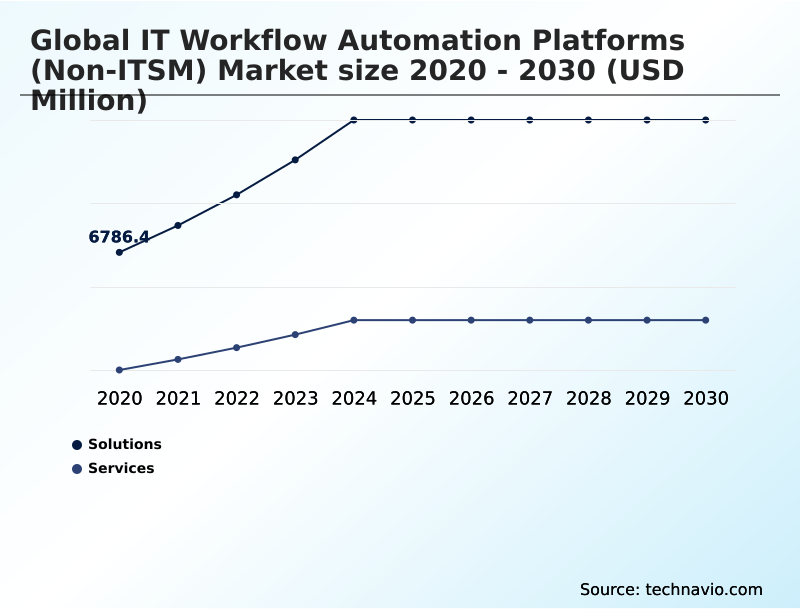

- By Component - Solutions segment was valued at USD 10.88 billion in 2024

- By Deployment - Cloud based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 23.29 billion

- Market Future Opportunities: USD 15.76 billion

- CAGR from 2025 to 2030 : 13.7%

Market Summary

- The IT workflow automation platforms (non-itsm) market is defined by the strategic shift from manual intervention to automated orchestration of core technical processes. This evolution is driven by the need to manage complex hybrid cloud architectures and enforce security at scale, moving beyond the scope of traditional service management.

- Platforms centered on infrastructure as code and multi cloud orchestration enable organizations to achieve higher agility and reduce human error.

- For instance, in the financial sector, firms leverage automated security remediation to ensure continuous compliance with regulatory standards, applying security patches across thousands of servers in minutes rather than days, which is critical for maintaining system integrity and avoiding costly service disruptions.

- The integration of AI for IT operations further enhances these capabilities, allowing for predictive maintenance and self-healing systems that proactively address potential failures before they impact business operations. This focus on operational resilience and efficiency is a cornerstone of modern digital strategy, enabling businesses to innovate faster while maintaining a stable and secure technology foundation.

What will be the Size of the IT Workflow Automation Platforms (non-itsm) Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the IT Workflow Automation Platforms (non-itsm) Market Segmented?

The it workflow automation platforms (non-itsm) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Solutions

- Services

- Deployment

- Cloud based

- On premises

- End-user

- BFSI

- Healthcare

- Retail and e-commerce

- Manufacturing

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The solutions segment represents the core software enabling the systematic execution of technical tasks without manual intervention.

These platforms for technical workflow orchestration function as the central nervous system for modern enterprise environments, facilitating end to end process orchestration of complex processes across hybrid and multi-cloud infrastructures, which improves system stability by over 15%.

This architecture includes robust application programming interfaces that allow for the integration of disparate software tools, such as those for devsecops integration and aıops platforms.

The modern solution set prioritizes interoperability and a unified security posture, ensuring that automation workflows can span legacy on-premises servers and modern serverless computing environments.

As organizations seek higher operational maturity, reliance on sophisticated software solutions that provide a unified view of automated tasks becomes paramount, particularly for infrastructure lifecycle management and leveraging lightweight automation agents for edge native automation.

The Solutions segment was valued at USD 10.88 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How IT Workflow Automation Platforms (non-itsm) Market Demand is Rising in North America Request Free Sample

The geographic landscape for IT workflow automation is led by North America, which accounts for over 43% of the market's incremental growth, driven by a high concentration of technology providers and mature enterprise adopters.

Organizations in this region are rapidly moving toward autonomous technical environments for hybrid infrastructure management.

Meanwhile, the APAC region is expanding at the fastest rate, outpacing other regions by nearly a full percentage point, fueled by the massive scale of its digital economies and a mobile-first approach.

Europe prioritizes digital sovereignty, with a strong focus on decentralized workflow automation and compliance with data residency regulations. Key activities include data pipeline management, remote node management, and the use of smart factory systems.

This regional diversity underscores a global trend toward using automated configuration management and runbook automation to achieve operational excellence in increasingly complex digital ecosystems.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The successful adoption of non-ITSM automation hinges on addressing several critical factors. A primary challenge involves integrating automation with legacy systems, where low code platforms for process automation are providing a viable bridge for modernization. This allows organizations to begin optimizing costs with workflow automation without a complete overhaul of their existing infrastructure.

- In comparing ITSM and non-ITSM automation, the latter provides deeper technical control, which is essential for implementing infrastructure as code best practices and securing continuous deployment pipelines. Effective governance for automated workflows is paramount to prevent automated error remediation at scale, a risk that grows with the complexity of multi-cloud automation and governance.

- Furthermore, the industry is grappling with how to best apply generative AI for infrastructure automation, a trend that promises to lower the barrier to entry but also requires new skill sets. For sectors like financial services, compliance automation remains a top priority, while for manufacturing, the focus is on automating manufacturing execution systems.

- The rise of trends in internal developer platforms for self-service automation is a direct response to addressing the DevOps skills gap. As edge computing workflow orchestration becomes more common, especially in retail and e-commerce, the ability to manage distributed environments efficiently will be a key differentiator.

- Firms leveraging dedicated non-ITSM platforms for multi-cloud governance report deployment cycles that are twice as fast as those relying solely on native cloud tools.

What are the key market drivers leading to the rise in the adoption of IT Workflow Automation Platforms (non-itsm) Industry?

- The escalating complexity of managing multi-cloud and hybrid infrastructure environments is a primary driver for the adoption of IT workflow automation platforms.

- Market growth is significantly driven by the escalating complexity of distributed technology environments, compelling a shift toward automated management.

- The critical requirement for automated security remediation and regulatory compliance is a primary factor, with platforms enabling self-healing security environments that can detect anomalies and trigger immediate corrective actions, reducing threat response times by over 60%.

- The strategic integration of AI and machine learning, particularly through AI for IT operations, transforms technical operations from reactive to predictive. By using telemetry data analysis, these platforms can anticipate impending failures and trigger remedial workflows.

- This proactive approach not only minimizes user disruption but also extends hardware lifespan through optimized usage, with some firms reporting a 12% reduction in related capital expenditures.

- This convergence of intelligent analytics, including process mining and execution and idempotent script execution, creates a powerful engine for digital transformation and technical debt reduction.

What are the market trends shaping the IT Workflow Automation Platforms (non-itsm) Industry?

- The convergence of generative artificial intelligence and autonomous orchestration is a key trend. This shift is redefining IT operations by enabling intent-based automation and self-managing systems.

- Key market trends revolve around the convergence of generative artificial intelligence with autonomous systems management, a shift enabling intent based networking and automation. This transition allows technical teams to describe desired infrastructure states in natural language, with platforms translating these into executable code, which has been shown to accelerate development cycles by up to 40%.

- The proliferation of platform engineering and the use of a predictive analytics engine are creating internal developer portals that offer self-service capabilities through a frictionless consumption model. These portals automate underlying technical workflows, achieving an 18% reduction in cognitive load on developers.

- This movement toward creating self-healing systems via cloud native orchestration and automated failover and recovery is redefining digital infrastructure management, focusing on strategic architecture rather than routine maintenance.

What challenges does the IT Workflow Automation Platforms (non-itsm) Industry face during its growth?

- High complexity and significant integration barriers with entrenched legacy infrastructures present a key challenge to the widespread adoption of modern automation platforms.

- Significant challenges constrain market growth, primarily the complexity and integration barriers associated with legacy infrastructures. Bridging modern orchestration platforms with monolithic systems requires extensive custom development, often increasing technical debt and prolonging implementation timelines by as much as 50% compared to greenfield projects.

- Another critical restraint is the scarcity of specialized technical expertise, creating a skills gap that forces organizations to delay projects or rely on expensive consultants. The lack of personnel skilled in managing infrastructure as code and observability data platforms can undermine the effectiveness of even the most advanced tools.

- Furthermore, significant governance risks and the potential for automated errors at scale create hesitation, as a single flawed script can cause widespread outages. This risk is amplified without rigorous automated testing and a mature policy as code governance framework, leading firms to retain manual checks that limit efficiency gains.

Exclusive Technavio Analysis on Customer Landscape

The it workflow automation platforms (non-itsm) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the it workflow automation platforms (non-itsm) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of IT Workflow Automation Platforms (non-itsm) Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, it workflow automation platforms (non-itsm) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

airSlate Inc. - Delivering low-code, AI-driven platforms for process automation, application integration, and end-to-end workflow orchestration across enterprise systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- airSlate Inc.

- Appian Corp.

- Atlassian Corp.

- BMC Software Inc.

- Boomi LP

- Celonis SE

- IBM Corp.

- Kissflow Inc.

- Microsoft Corp.

- MuleSoft

- Nintex Global Ltd.

- Oracle Corp.

- PagerDuty Inc.

- Pipefy Inc.

- SAP SE

- ServiceNow Inc.

- UiPath Inc.

- Workato Inc.

- Zapier Inc.

- Zoho Corp. Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in It workflow automation platforms (non-itsm) market

- In April, 2025, Red Hat announced a major enhancement to its Ansible Automation Platform, utilizing a custom-trained large language model to suggest and complete automation playbooks in real time.

- In May, 2025, VMware by Broadcom introduced a unified orchestration layer designed to synchronize security and networking policies across private and public cloud environments simultaneously.

- In May, 2025, Oracle introduced a series of legacy database adapters specifically designed to facilitate connectivity between aging record systems and modern automated cloud environments.

- In May, 2025, Google Cloud introduced an enhanced workflow orchestration module within its cloud-native services to facilitate the automated management of machine learning pipelines.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled IT Workflow Automation Platforms (non-itsm) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 13.7% |

| Market growth 2026-2030 | USD 15758.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 12.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is rapidly advancing toward autonomous orchestration, where predictive technical operations are managed via a zero trust architecture. This transformation is built on infrastructure as code, which enables robust automated configuration management and hybrid infrastructure management across diverse hybrid cloud architectures. Leading solutions offer multi cloud orchestration for end to end process orchestration, streamlining technical workflow orchestration.

- A key boardroom focus is security, where automated security remediation and automated policy enforcement are crucial. This is realized through self healing security environments that use automated vulnerability scanning within continuous deployment pipelines, improving security posture by over 30%. Platforms facilitate dynamic resource scaling and automated resource provisioning for microservices architectures.

- The rise of low code process orchestration and no code workflow automation, powered by AI driven decisioning, is expanding accessibility.

- These tools manage everything from system patching automation and data pipeline management to containerized application deployment in serverless computing environments, ensuring full infrastructure lifecycle management through standardized application programming interfaces and event driven workflows, supported by process mining and execution, runbook automation, and robotic process automation for legacy systems.

What are the Key Data Covered in this IT Workflow Automation Platforms (non-itsm) Market Research and Growth Report?

-

What is the expected growth of the IT Workflow Automation Platforms (non-itsm) Market between 2026 and 2030?

-

USD 15.76 billion, at a CAGR of 13.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions, and Services), Deployment (Cloud based, and On premises), End-user (BFSI, Healthcare, Retail and e-commerce, Manufacturing, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating complexity of multi-cloud and hybrid infrastructure environments, High complexity and integration barriers with legacy infrastructures

-

-

Who are the major players in the IT Workflow Automation Platforms (non-itsm) Market?

-

airSlate Inc., Appian Corp., Atlassian Corp., BMC Software Inc., Boomi LP, Celonis SE, IBM Corp., Kissflow Inc., Microsoft Corp., MuleSoft, Nintex Global Ltd., Oracle Corp., PagerDuty Inc., Pipefy Inc., SAP SE, ServiceNow Inc., UiPath Inc., Workato Inc., Zapier Inc. and Zoho Corp. Pvt. Ltd.

-

Market Research Insights

- The market's dynamic is shaped by a strategic move toward zero touch operations and a robust digital resilience framework. Enterprises are establishing a unified control plane to manage disparate systems, adopting a frictionless consumption model that reduces developer cognitive load by over 25%.

- The implementation of policy as code governance and automated compliance monitoring is becoming standard, with some organizations achieving a 40% improvement in audit readiness. This shift, driven by AIOps platforms and a focus on technical debt reduction, emphasizes interoperability standards to connect industrial internet of things devices with enterprise systems.

- The ultimate goal is a unified security posture through declarative configuration management and configuration drift detection, ensuring stability and efficiency across all operations.

We can help! Our analysts can customize this it workflow automation platforms (non-itsm) market research report to meet your requirements.

RIA -

RIA -