Kosher Foods Market Size 2026-2030

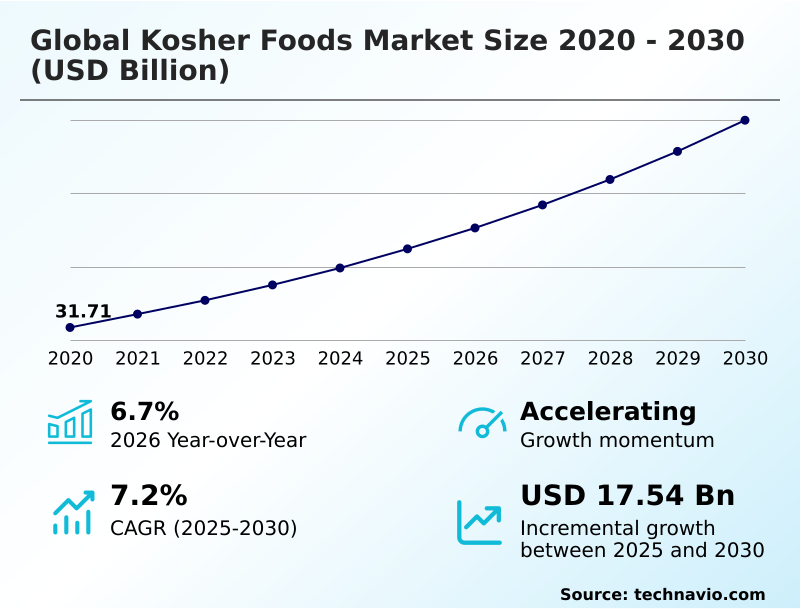

The kosher foods market size is valued to increase by USD 17.54 billion, at a CAGR of 7.2% from 2025 to 2030. Expanding health consciousness and quality assurance will drive the kosher foods market.

Major Market Trends & Insights

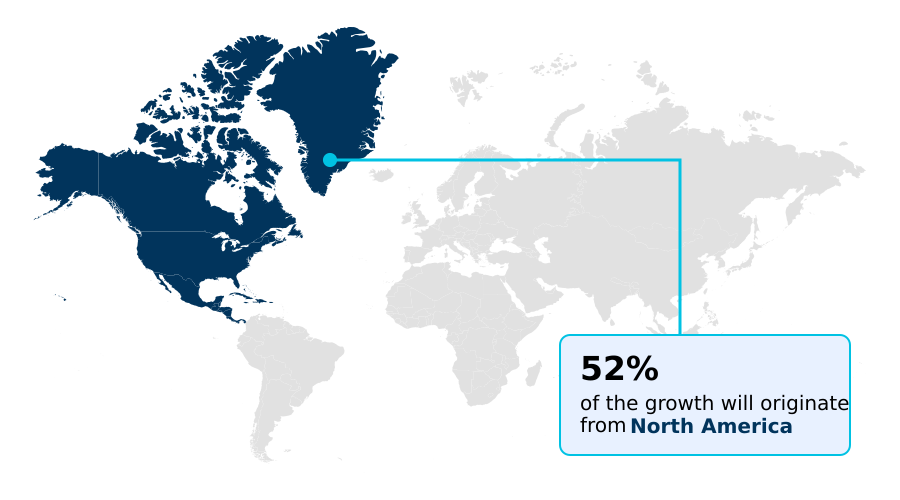

- North America dominated the market and accounted for a 51.9% growth during the forecast period.

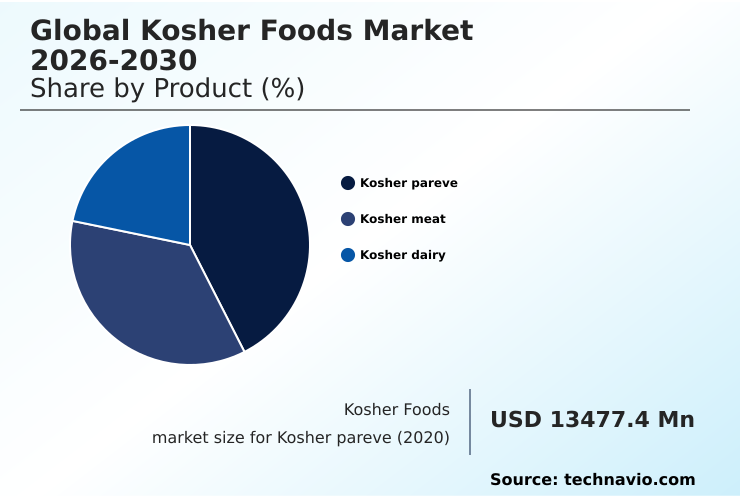

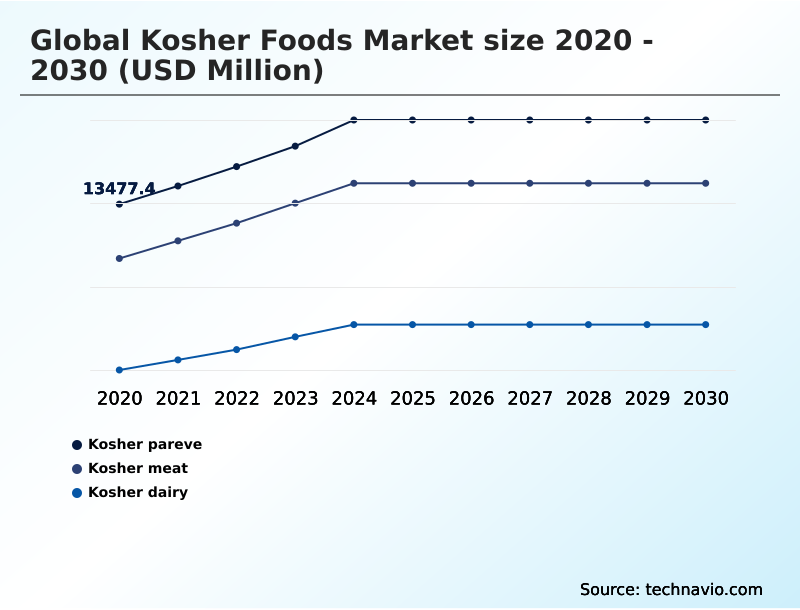

- By Product - Kosher pareve segment was valued at USD 16.81 billion in 2024

- By Distribution Channel - Supermarkets and hypermarkets segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 28.26 billion

- Market Future Opportunities: USD 17.54 billion

- CAGR from 2025 to 2030 : 7.2%

Market Summary

- The kosher foods market is undergoing a significant transformation, moving beyond its traditional religious demographic to appeal to a wider audience seeking verified quality and safety. This expansion is driven by a growing perception of the hechsher symbol as a hallmark of rigorous food safety assurance and clean label verification.

- Adherence to kashrut dietary laws, overseen by stringent mashgiach supervision, provides a level of transparency that resonates with health-conscious consumers, including those following vegan and allergen-free diets. Consequently, manufacturers are increasingly pursuing kosher certification standards for a diverse range of products, from everyday snacks to gourmet items.

- For instance, a food processor aiming to capture the specialty market for pas yisroel baked goods might implement blockchain technology to ensure complete supply chain traceability, from certified ingredient sourcing to final packaging. This not only guarantees compliance with kosher for passover foods regulations but also reinforces consumer trust.

- However, the industry faces challenges related to the higher costs of certified production and competition from other food certifications. The market’s trajectory is shaped by its ability to balance tradition with innovation, leveraging its reputation for quality while adapting to modern consumer values and technological advancements.

What will be the Size of the Kosher Foods Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Kosher Foods Market Segmented?

The kosher foods industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Kosher pareve

- Kosher meat

- Kosher dairy

- Distribution channel

- Supermarkets and hypermarkets

- Grocery stores

- Online stores

- End-user

- Household consumers

- Food service industry

- Food processing industry

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Middle East and Africa

- Israel

- South Africa

- UAE

- South America

- Brazil

- Argentina

- APAC

- Australia

- Japan

- India

- Rest of World (ROW)

- North America

By Product Insights

The kosher pareve segment is estimated to witness significant growth during the forecast period.

The kosher pareve segment is expanding beyond its traditional consumer base, increasingly serving as a reliable indicator for vegan and allergen-free diets. This category, which stringently enforces meat and dairy separation, undergoes rigorous mashgiach supervision to ensure religious dietary compliance.

Manufacturers are leveraging this classification, which mandates scrutiny of all food processing additives and requires intense quality control inspection, to appeal to a broader health-conscious demographic.

Adherence to rabbinical oversight in production facilities dedicated to pareve products has led to a 20% reduction in cross-contamination incidents compared to mixed-use lines.

The growing alignment with non-GMO food verification and the demand for enhanced food purity standards are positioning this segment as a significant driver of innovation.

The Kosher pareve segment was valued at USD 16.81 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 51.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Kosher Foods Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is led by North America, which accounts for 51.9% of incremental growth, driven by a mature consumer base that values transparent food labeling.

This region is a major importer of glatt kosher meat, where every stage of the kosher slaughtering method, including bedikah internal inspection and nikur deveining process, is scrutinized.

In contrast, APAC is the fastest-growing region, with a 9% CAGR, as it becomes a critical hub for certified ingredient sourcing.

The demand here is not just for finished goods like chalav yisrael products but for raw materials that meet global standards.

The integrity of the international supply chain relies on technologies that ensure food fraud prevention and complete supply chain traceability, validating ethical food production claims across continents.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the kosher foods market is increasingly influenced by specific consumer needs and technological advancements. The synergy between kosher pareve for vegan consumers and the broader trend of plant-based diets is a significant growth area, with kosher certification for plant-based foods becoming a key differentiator.

- This has led to a focus on kosher pareve as a dairy-free indicator, reinforcing consumer trust in kosher certification. However, challenges in kosher ingredient sourcing and complex supply chain logistics for kosher meat persist. In response, firms are adopting blockchain for kosher supply chain management and other kosher food traceability technology, which helps address kosher meat export regulations.

- The market is also seeing a growth of artisanal kosher products and innovation in kosher for passover products. As producers navigate the kosher certification cost for manufacturers and the nuances of kosher dairy production standards, they are also exploring integrating kosher and organic certifications.

- Companies that successfully achieve this dual status have demonstrated market penetration rates in specialty health stores nearly twice those of singly certified brands. This shift underscores the importance of effective marketing strategies for kosher foods to non-jewish consumers, leveraging the appeal of rabbinical supervision in food processing and the perceived high standards of the shechita process and animal welfare.

- The expansion of online retail for kosher products is further widening market access, changing the competitive landscape.

What are the key market drivers leading to the rise in the adoption of Kosher Foods Industry?

- Expanding health consciousness among consumers and a growing demand for quality assurance are key drivers propelling market growth.

- The market's expansion is fundamentally driven by the growing perception of the hechsher symbol as a benchmark for food safety assurance and quality.

- The stringent kashrut dietary laws and the detailed shechita process provide a level of clean label verification that resonates beyond religious observers.

- The pareve designation is increasingly used by consumers as a reliable proxy for plant-based diet compatibility, a crossover that has broadened the consumer base by over 30% in some categories.

- This is reinforced by the rigorous nature of the third-party food audit inherent in obtaining kosher certification standards.

- As a result, the certification serves as one of the most powerful consumer trust indicators in the food industry, driving both loyalty and new customer acquisition.

- Firms that highlight their compliance in marketing materials see an average 10% uplift in engagement.

What are the market trends shaping the Kosher Foods Industry?

- The kosher sector is experiencing a notable trend toward premiumization, marked by a surge in artisanal product offerings that cater to evolving consumer preferences for high-quality, specialized goods.

- The market is witnessing a significant trend toward premiumization, with a notable rise in artisanal food production. This shift is driven by consumer demand for gourmet food certification and products with high-quality attributes, expanding the specialty food market. Companies focusing on this niche report that achieving premium food certification can increase profit margins by up to 15%.

- This trend is particularly evident in categories like pas yisroel baked goods and specialty kosher for passover foods. Innovation in ingredients, such as the development of a kosher gelatin alternative and the careful sourcing of animal-derived enzymes, is enabling this growth. Furthermore, the alignment with other certifications, particularly organic food alignment and dairy-free certification, is creating new opportunities.

- Retailers have noted a 20% increase in sales velocity for products that carry both kosher and organic labels.

What challenges does the Kosher Foods Industry face during its growth?

- Escalating production costs, coupled with inherent supply chain vulnerabilities, present a key challenge to the industry's growth trajectory.

- Key challenges in the market stem from the operational complexities and costs associated with strict manufacturing protocol adherence. The kashering process and the bishul yisrael requirement add significant overhead, impacting price competitiveness. For instance, maintaining separate production lines for treif contamination prevention can increase capital expenditures by up to 25%.

- The need for specific tools like a shechita knife specifications and ingredients like kosher salt properties also constrains the supply chain. Moreover, the market faces intense competition from other labels, where the dual-certification benefits of kosher are not always clearly communicated.

- While the certification provides clear allergen-free labeling advantages, its value proposition in a crowded market that includes a strong halal food comparison requires constant reinforcement to prevent cross-contamination avoidance from becoming the sole perceived benefit.

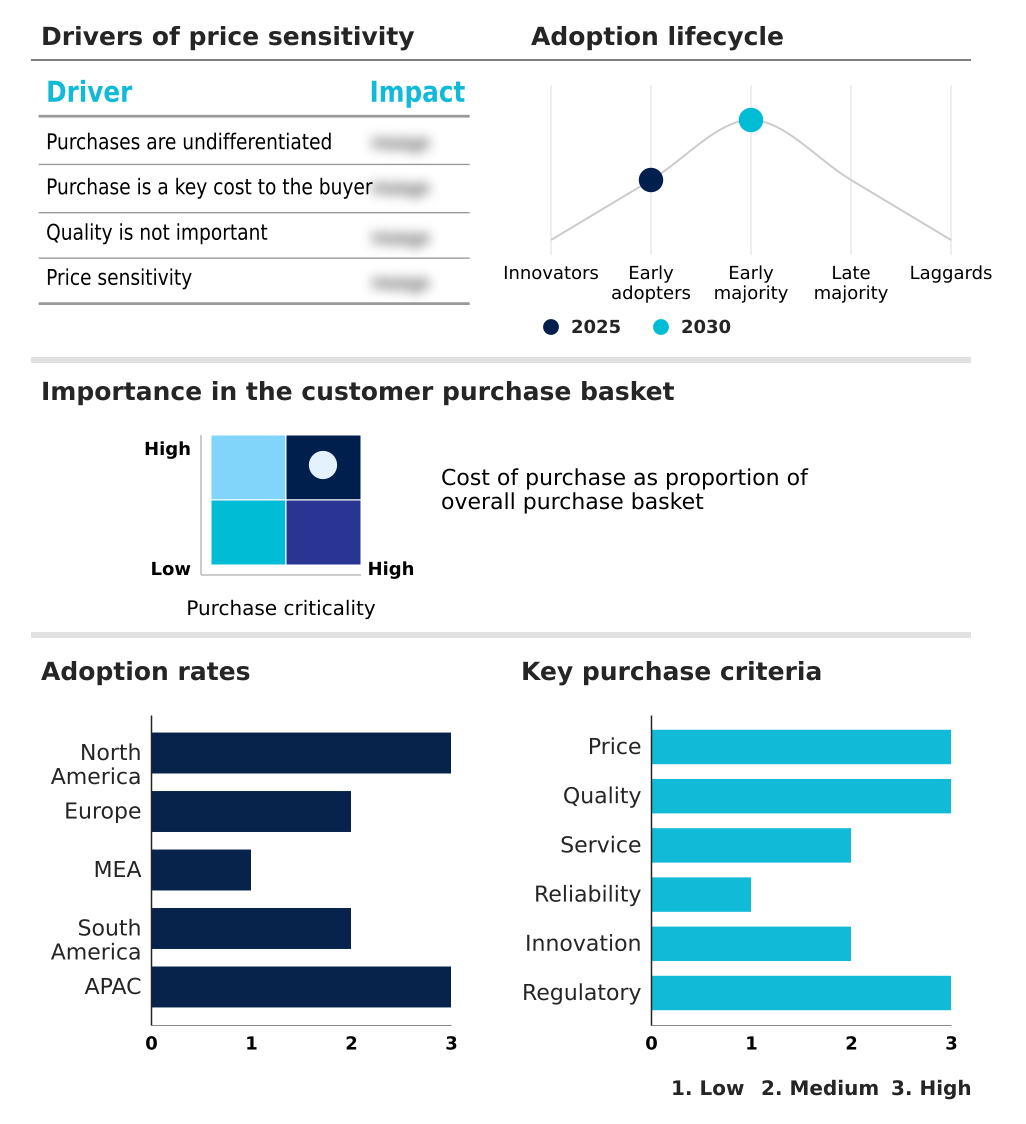

Exclusive Technavio Analysis on Customer Landscape

The kosher foods market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the kosher foods market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Kosher Foods Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, kosher foods market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGRANA Beteiligungs AG - Analysis indicates a focus on providing specialized kosher-certified ingredients, including fruit preparations and starches, for the bakery and dairy food processing sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGRANA Beteiligungs AG

- Archer Daniels Midland Co.

- Aron Streit Inc.

- BASF SE

- Bobs Red Mill Natural Foods

- Cargill Inc.

- Conagra Brands Inc.

- Dairy Farmers of America Inc.

- Eden Foods Inc.

- Empire Kosher Poultry LLC

- General Mills Inc.

- Kayco Co.

- Kellanova

- Nestle SA

- PepsiCo Inc.

- Taja Beverages

- The Kraft Heinz Co.

- Unilever PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Kosher foods market

- In August 2025, IBM Food Trust entered into a landmark partnership with the Orthodox Union to implement blockchain technology across several major kosher meat processing facilities in Europe and South America.

- In May 2025, Vitasoy International Holdings Limited achieved a significant milestone by obtaining kosher certification for its entire premium beverage line throughout its operations in the Asia Pacific.

- In March 2025, the popular Asia Pacific food technology startup ZENB, known for its innovative plant based snacks, achieved Certified B Corporation status, creating new competitive pressure for kosher brands.

- In February 2025, Whole Foods Market introduced an exclusive partnership with several boutique kosher bakeries in the North American region to stock high end seasonal pastries.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Kosher Foods Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.2% |

| Market growth 2026-2030 | USD 17539.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, Israel, South Africa, UAE, Turkey, Saudi Arabia, Brazil, Argentina, Chile, Australia, Japan, India, China, Singapore and South Korea |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The operational framework of the kosher foods market is built upon strict adherence to kashrut dietary laws, a complex system governed by rigorous kosher certification standards. Central to this is the shechita process, a specific kosher slaughtering method requiring a specialized shechita knife and subsequent bedikah internal inspection to ensure compliance.

- The integrity of products like glatt kosher meat depends on meticulous procedures such as the nikur deveining process. Constant rabbinical oversight and on-site mashgiach supervision are non-negotiable for validating the hechsher symbol, which signifies compliance. This extends to specialized categories, including chalav yisrael products, pas yisroel baked goods, and foods prepared under the bishul yisrael requirement.

- The industry invests heavily in treif contamination prevention, employing a thorough kashering process and specific kosher salt properties for sanitation. Facilities implementing rigorous protocols for meat and dairy separation have achieved a 40% reduction in cross-contamination incidents.

- Furthermore, innovation is evident in the development of kosher gelatin alternatives and the careful screening of animal-derived enzymes and food processing additives to maintain the pareve designation and dairy-free certification, ensuring products like kosher for passover foods meet all requirements for ritual slaughter compliance.

What are the Key Data Covered in this Kosher Foods Market Research and Growth Report?

-

What is the expected growth of the Kosher Foods Market between 2026 and 2030?

-

USD 17.54 billion, at a CAGR of 7.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Kosher pareve, Kosher meat, and Kosher dairy), Distribution Channel (Supermarkets and hypermarkets, Grocery stores, and Online stores), End-user (Household consumers, Food service industry, and Food processing industry) and Geography (North America, Europe, Middle East and Africa, South America, APAC)

-

-

Which regions are analyzed in the report?

-

North America, Europe, Middle East and Africa, South America and APAC

-

-

What are the key growth drivers and market challenges?

-

Expanding health consciousness and quality assurance, Escalating production costs and supply chain vulnerabilities

-

-

Who are the major players in the Kosher Foods Market?

-

AGRANA Beteiligungs AG, Archer Daniels Midland Co., Aron Streit Inc., BASF SE, Bobs Red Mill Natural Foods, Cargill Inc., Conagra Brands Inc., Dairy Farmers of America Inc., Eden Foods Inc., Empire Kosher Poultry LLC, General Mills Inc., Kayco Co., Kellanova, Nestle SA, PepsiCo Inc., Taja Beverages, The Kraft Heinz Co. and Unilever PLC

-

Market Research Insights

- The market dynamics are increasingly shaped by consumer demand for transparency, where third-party food audit results and clear consumer trust indicators directly influence purchasing decisions. The pursuit of premium food certification is driving growth in the artisanal food production segment, with some brands achieving a 15% price premium over non-certified counterparts.

- Strategic alignment with other lifestyle diets, highlighting dual-certification benefits, has become a key differentiator, particularly when compared to the halal food comparison. Businesses that successfully integrate robust protocols for food fraud prevention into their supply chains report a 25% higher consumer retention rate.

- This shift underscores a move from niche compliance to a broad-based strategy centered on verifiable quality and ethical production standards.

We can help! Our analysts can customize this kosher foods market research report to meet your requirements.

RIA -

RIA -