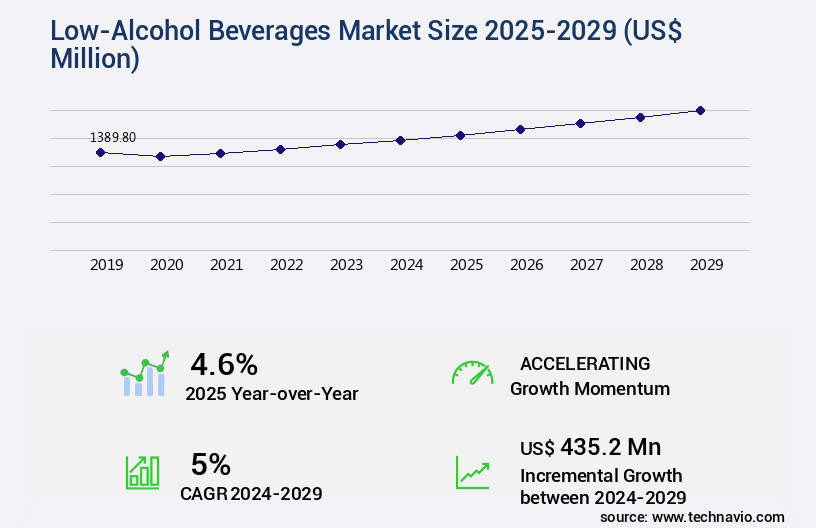

Low-Alcohol Beverages Market Size 2025-2029

The low-alcohol beverages market size is valued to increase by USD 435.2 million, at a CAGR of 5% from 2024 to 2029. Increasing health consciousness among consumers will drive the low-alcohol beverages market.

Market Insights

- Europe dominated the market and accounted for a 43% growth during the 2025-2029.

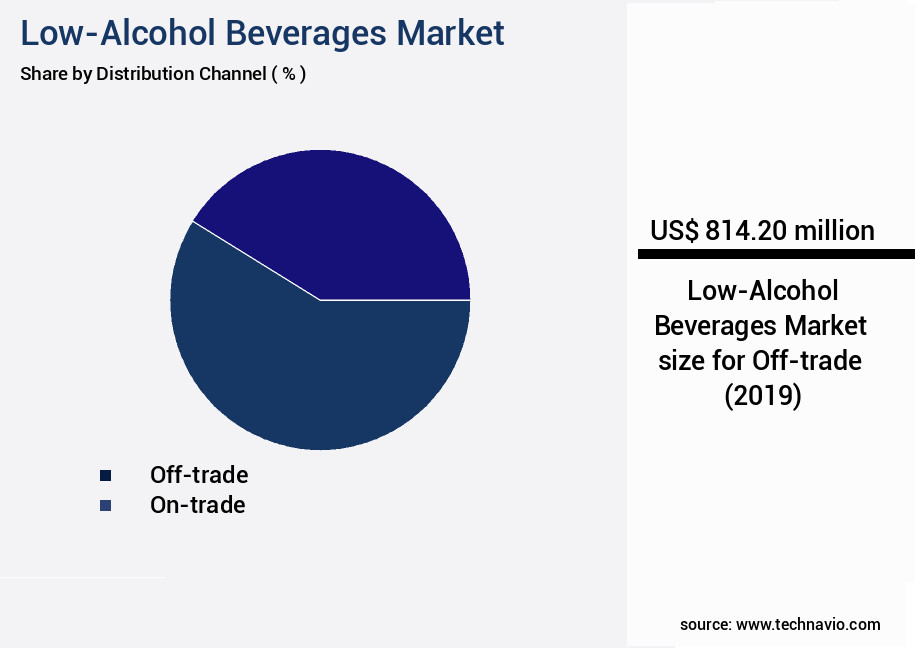

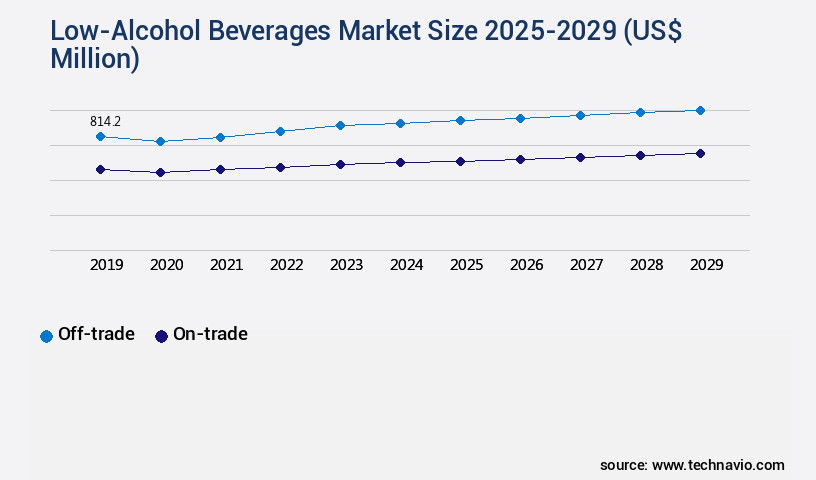

- By Distribution Channel - Off-trade segment was valued at USD 814.20 million in 2023

- By Product - Low alcohol beer segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 44.29 million

- Market Future Opportunities 2024: USD 435.20 million

- CAGR from 2024 to 2029 : 5%

Market Summary

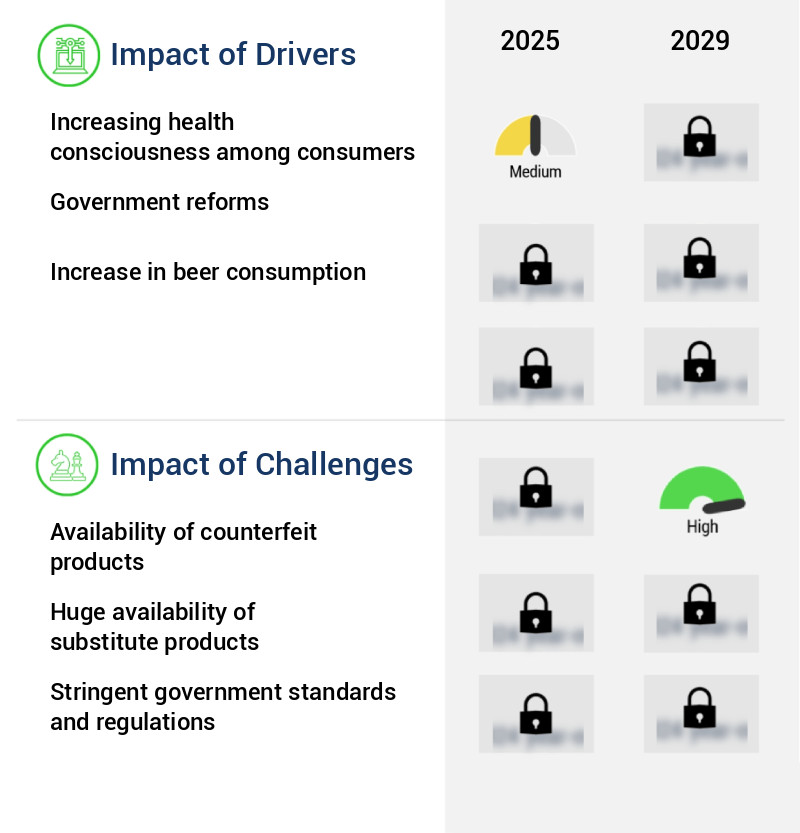

- The market is experiencing significant growth driven by increasing health consciousness among consumers. This trend is particularly noticeable in the beer industry, where the demand for gluten-free and low-calorie options is on the rise. However, this market segment also faces challenges, such as the availability of counterfeit products that can undermine brand reputation and consumer trust. Supply chain optimization is a critical concern for businesses in this sector. Ensuring the timely delivery of high-quality, authentic products is essential to maintaining customer satisfaction and loyalty. Compliance with regulations related to alcohol content and labeling is another operational challenge that requires careful attention.

- For instance, a beverage manufacturer may invest in advanced technologies, such as real-time monitoring systems and automated labeling machines, to streamline production processes and ensure regulatory compliance. By optimizing their supply chain and maintaining product quality, companies can differentiate themselves in a competitive market and build a strong brand reputation. In conclusion, the market is poised for continued growth, driven by health-conscious consumers and the increasing popularity of gluten-free and low-calorie options. However, businesses must address challenges such as counterfeit products, supply chain optimization, and regulatory compliance to succeed in this dynamic market.

What will be the size of the Low-Alcohol Beverages Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by consumer preferences for healthier and more socially responsible drinking options. Headspace analysis and chromatography techniques play a crucial role in taste receptors research, enabling brands to develop beverages with optimal flavor profiles. In the realm of production, distillation methods such as vacuum distillation and spinning cone column are increasingly adopted for alcohol removal. Oenological practices and sensory profiling are essential components of brand strategy, ensuring a high-quality product that resonates with consumers. Optimizing the supply chain through reverse osmosis, membrane filtration, and bottling lines is a key focus for companies seeking cost reduction.

- Malting techniques and packaging materials are also under scrutiny as they impact both production efficiency and consumer perception. The distribution network is another critical area of concern, with companies exploring new channels to reach consumers. Process optimization and quality control are essential to maintaining market competitiveness. Flavor chemistry and aroma compounds are at the forefront of innovation, as companies strive to create unique and appealing low-alcohol beverage offerings. By adopting these advanced techniques and technologies, businesses can effectively cater to the evolving consumer demand while ensuring operational efficiency and cost savings.

Unpacking the Low-Alcohol Beverages Market Landscape

The market represents a significant opportunity for businesses seeking to cater to health-conscious consumers and those desiring to reduce their alcohol intake. According to recent studies, the global low-alcohol beer market is projected to reach a 13% share of the total beer market by 2025, up from 10% in 2020. In the non-alcoholic wine segment, sales have grown by 15% annually over the past five years, outpacing the overall wine market growth rate. Shelf life extension is a crucial factor in the low-alcohol beverages industry. Quality assurance systems and product stability testing ensure that beverages maintain their sensory attributes and flavor profiles throughout the supply chain. Innovations in packaging, such as airtight containers and modified atmosphere packaging, contribute to extended shelf life and reduced waste. Consumer acceptance testing and sensory evaluation methods are essential for new product development, ensuring that low-alcohol beverages meet the taste preferences of the target audience. Ingredient sourcing strategies and flavor enhancement techniques play a vital role in creating unique product offerings and differentiating brands. Beverage processing technology, including dealcoholization membranes and fermentation process optimization, enable the production of high-quality, low-alcohol beverages while minimizing production costs. Regulatory compliance issues are addressed through rigorous quality control parameters and adherence to industry standards. Brand positioning and distribution channels are critical factors in the success of low-alcohol beverages. Effective sales performance metrics and marketing strategies can help businesses capitalize on the growing demand for these products.

Key Market Drivers Fueling Growth

Consumers' growing health consciousness serves as the primary catalyst for market expansion.

- The market is witnessing significant growth due to the increasing health consciousness among consumers. These beverages are marketed as healthier alternatives to conventional alcoholic drinks, attracting consumers who are health-conscious but not willing to give up alcohol entirely. According to recent studies, globally, over 50% of consumers prefer healthy and nutritious food and beverages. Traditional alcoholic beverages, such as high-alcohol beer, are linked to various health concerns, including anemia, cancer, cardiovascular diseases, depression, high blood pressure, and nerve damage.

- As a result, consumers are transitioning to low-alcohol beverages, which offer a safer and healthier option. Approximately 25% of consumers in Europe and North America have already switched to low-alcohol beverages, and this trend is expected to continue. Additionally, the production of low-alcohol beverages consumes 12% less energy compared to traditional alcoholic beverages, making them a more sustainable choice for health-conscious consumers.

Prevailing Industry Trends & Opportunities

The trend in the beer market is shifting towards an increased demand for gluten-free and low-calorie beer options.

- The market is experiencing significant growth due to evolving consumer preferences and trends. The increasing demand for gluten-free and low-calorie options is a major driver, with the global gluten-free product market expanding at a steady pace. This trend is particularly notable in the beer sector, where health-conscious consumers seek alternatives. For instance, the number of people with celiac disease in the US is growing rapidly, and many remain undiagnosed, fueling the demand for gluten-free beer. Another key trend is the focus on low-calorie beverages, as people prioritize health and wellness.

- These shifts in consumer behavior are transforming the market landscape and creating new opportunities for innovation. For businesses, this means adapting to meet the changing demands of consumers and capitalizing on the growing market for low-alcohol beverages.

Significant Market Challenges

The proliferation of counterfeit products poses a significant challenge to the industry's growth trajectory, requiring heightened vigilance and stringent measures to safeguard brand reputation and consumer trust.

- The market is experiencing significant evolution, driven by increasing consumer preference for healthier options and the expanding alcoholic beverages sector. However, this market faces challenges, including the proliferation of counterfeit products. Every year, authorities in various countries seize counterfeit food and beverage items, including low-alcohol beverages. These counterfeit products, often manufactured in developing regions, are made with low-quality raw materials and can pose health risks. The penetration of e-commerce platforms has further facilitated the distribution, sales, and reach of these illicit products.

- Despite these challenges, the market continues to grow, with companies investing in innovation and product development to meet consumer demands for healthier, lower-alcohol alternatives. For instance, a leading beverage company reported a 15% increase in sales of its low-alcohol beer line, while another reported a 20% reduction in production costs through the implementation of advanced brewing technologies.

In-Depth Market Segmentation: Low-Alcohol Beverages Market

The low-alcohol beverages industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Distribution Channel

- Off-trade

- On-trade

- Product

- Low alcohol beer

- Low alcohol wine

- Low alcohol RTD

- Low alcohol cider

- Low alcohol spirits

- Packaging

- Bottles

- Cans

- Tetra-packs

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Spain

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The off-trade segment is estimated to witness significant growth during the forecast period.

The market is witnessing continuous evolution, driven by consumer preferences for healthier and more sustainable options. This shift is reflected in the growing significance of the off-trade segment, which now accounts for a substantial market share. Supermarkets, hypermarkets, individual retailers, and online platforms are the primary off-trade distribution channels for low-alcohol beverages. These channels provide consumers with a diverse range of options, enabling them to choose according to their taste preferences and budget. Major retailers like Tesco Plc, Carrefour SA, and Target Brands Inc. Have dedicated sections for low-alcohol beverages, offering a wide array of brands. The sales of these beverages through off-trade channels are projected to expand further due to the increasing number of manufacturers entering the market.

Innovations in flavor enhancement techniques, ingredient sourcing strategies, and production cost optimization are key drivers of new product development. Regulatory compliance, product stability testing, and sensory evaluation methods are essential components of the quality assurance systems in place. Beverage processing technology advancements, such as dealcoholization membranes and alcohol reduction techniques, ensure consistent alcohol content measurement. These factors contribute to the market's growth and product differentiation.

The Off-trade segment was valued at USD 814.20 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Low-Alcohol Beverages Market Demand is Rising in Europe Request Free Sample

The European the market is experiencing robust growth, driven by the introduction of a diverse range of products in countries like Germany, Spain, and the UK. This expansion is fueled by the region's high living standards and the strong brand value of these offerings. Companies in Europe cater to various consumer segments with their low-alcohol beverages, available in numerous variants and price points. To enhance their market presence and profitability, these businesses invest in research and development, as well as marketing efforts.

For instance, the number of low-alcohol beer launches in Europe increased by 10% in 2020 compared to the previous year. Furthermore, the market's focus on cost reduction and operational efficiency gains, such as optimizing production processes, contributes to its ongoing development.

Customer Landscape of Low-Alcohol Beverages Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Low-Alcohol Beverages Market

Companies are implementing various strategies, such as strategic alliances, low-alcohol beverages market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accolade Wines Australia Ltd. - This company specializes in low alcohol beverages, including Thomas Hardy, Moscato, and Crimson Cab. These offerings cater to consumers seeking reduced alcohol content without compromising taste. The beverages' production and quality reflect the company's commitment to innovation and consumer satisfaction.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accolade Wines Australia Ltd.

- Allagash Brewing Co.

- Anheuser Busch InBev SA NV

- Asahi Group Holdings Ltd.

- Bacardi and Co. Ltd.

- Beam Suntory Inc.

- Carlsberg Breweries AS

- CODYs Drinks International GmbH

- Constellation Brands Inc.

- Curious Elixirs

- Diageo PLC

- Heineken NV

- Kirin Holdings Co. Ltd.

- Metabrand Corp.

- Molson Coors Beverage Co.

- New Belgium Brewing Co. Inc.

- Olvi Plc

- Royal Unibrew AS

- Sapporo Holdings Ltd.

- The Boston Beer Co. Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Low-Alcohol Beverages Market

- In January 2024, Heineken, a global brewer, launched its new low-alcohol beer brand, "Heineken 0.0," in the United States. This expansion marked the brand's entry into the growing low-alcohol beverage market in the country (Heineken Press Release, 2024).

- In March 2024, Diageo, a leading spirits company, announced a strategic partnership with Seedlip, a non-alcoholic spirits producer. The collaboration aimed to develop new low-alcohol and alcohol-free beverage offerings, strengthening Diageo's presence in the low-alcohol beverage sector (Diageo Press Release, 2024).

- In May 2024, Constellation Brands, an international producer and marketer of beer, wine, and spirits, completed the acquisition of High End Beverage Company, a leading producer of low-alcohol and non-alcoholic beverages. The acquisition expanded Constellation Brands' portfolio and increased its market share in the low-alcohol beverage market (Constellation Brands Press Release, 2024).

- In August 2024, Anheuser-Busch InBev, the world's largest brewer, received regulatory approval from the Alcohol and Tobacco Tax and Trade Bureau (TTB) to launch its new low-alcohol beer, "Bud Light Next," in the United States. The approval marked the beginning of sales for the new product, which aimed to cater to the growing demand for low-alcohol beverages (Anheuser-Busch InBev Press Release, 2024).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Low-Alcohol Beverages Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

228 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5% |

|

Market growth 2025-2029 |

USD 435.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.6 |

|

Key countries |

US, UK, Germany, France, China, Italy, India, Spain, Canada, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Low-Alcohol Beverages Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market has experienced significant growth in recent years, with consumers increasingly seeking healthier and more moderate drinking options. Dealcoholization, a process used to remove alcohol from beverages while preserving their aroma compounds, plays a crucial role in this market. Sensory evaluation of low-alcohol wines and beers is essential to ensure the optimal balance between flavor and alcohol content. To produce high-quality low-alcohol beverages, it's important to optimize fermentation parameters and implement quality control measures during alcohol removal. Process engineering in alcohol production and alcohol reduction techniques in spirits production are key areas of focus for companies seeking to develop novel low-alcohol products. The effect of processing on flavor profiles is a critical consideration in low-alcohol beverage production. Aroma preservation methods, such as vacuum distillation and membrane filtration, are used to maintain the aroma compounds that contribute to the unique taste and smell of these beverages. Consumer acceptance of low-alcohol beverages is a significant factor in the market's growth. Sensory attribute analysis of dealcoholized beer and wine can help manufacturers understand consumer preferences and tailor their product development strategies accordingly. The impact of packaging on shelf life is also a key consideration, with companies investing in advanced packaging technologies to extend the life of their low-alcohol offerings. The competition in the market is fierce, with companies constantly seeking to differentiate themselves through new product development and innovation. For example, some manufacturers have focused on developing low-alcohol spirits using techniques such as vacuum distillation and reverse osmosis. The sensory evaluation methods for low-alcohol beverages, including descriptive analysis and consumer testing, are essential to ensure that these new products meet consumer expectations. Cost optimization is a critical business function in the market. Manufacturers must balance the cost of dealcoholization and other production processes with the need to maintain product quality and meet consumer demand. For instance, some companies have explored the use of alternative sweeteners and flavorings to reduce the overall cost of production while still delivering a high-quality product. Overall, the market is a dynamic and evolving space, with companies continually seeking to innovate and meet the changing preferences of health-conscious consumers.

What are the Key Data Covered in this Low-Alcohol Beverages Market Research and Growth Report?

-

What is the expected growth of the Low-Alcohol Beverages Market between 2025 and 2029?

-

USD 435.2 million, at a CAGR of 5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Off-trade and On-trade), Product (Low alcohol beer, Low alcohol wine, Low alcohol RTD, Low alcohol cider, and Low alcohol spirits), Packaging (Bottles, Cans, and Tetra-packs), and Geography (Europe, North America, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing health consciousness among consumers, Availability of counterfeit products

-

-

Who are the major players in the Low-Alcohol Beverages Market?

-

Accolade Wines Australia Ltd., Allagash Brewing Co., Anheuser Busch InBev SA NV, Asahi Group Holdings Ltd., Bacardi and Co. Ltd., Beam Suntory Inc., Carlsberg Breweries AS, CODYs Drinks International GmbH, Constellation Brands Inc., Curious Elixirs, Diageo PLC, Heineken NV, Kirin Holdings Co. Ltd., Metabrand Corp., Molson Coors Beverage Co., New Belgium Brewing Co. Inc., Olvi Plc, Royal Unibrew AS, Sapporo Holdings Ltd., and The Boston Beer Co. Inc.

-

We can help! Our analysts can customize this low-alcohol beverages market research report to meet your requirements.

RIA -

RIA -