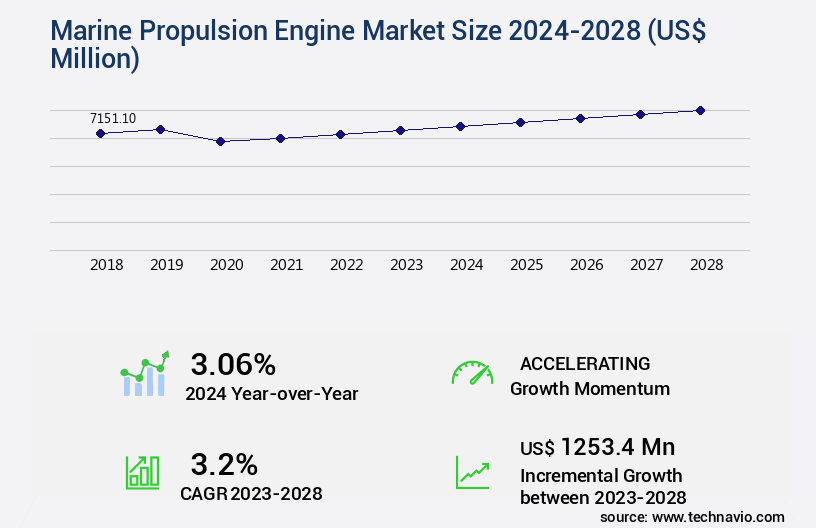

Marine Propulsion Engine Market Size 2024-2028

The marine propulsion engine market size is valued to increase by USD 1.25 billion, at a CAGR of 3.2% from 2023 to 2028. Increase in maritime trade and fleet size will drive the marine propulsion engine market.

Market Insights

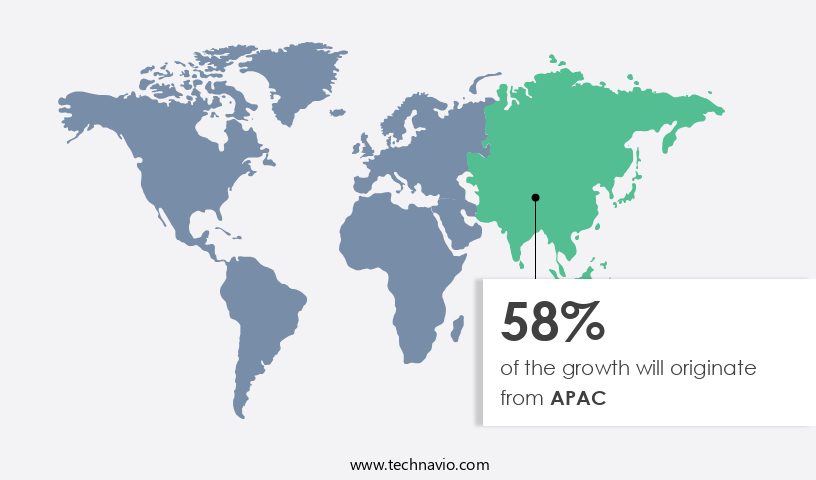

- APAC dominated the market and accounted for a 58% growth during the 2024-2028.

- By Application - Passenger segment was valued at USD 3.7 billion in 2022

- By Type - Diesel segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 20.27 million

- Market Future Opportunities 2023: USD 1253.40 million

- CAGR from 2023 to 2028 : 3.2%

Market Summary

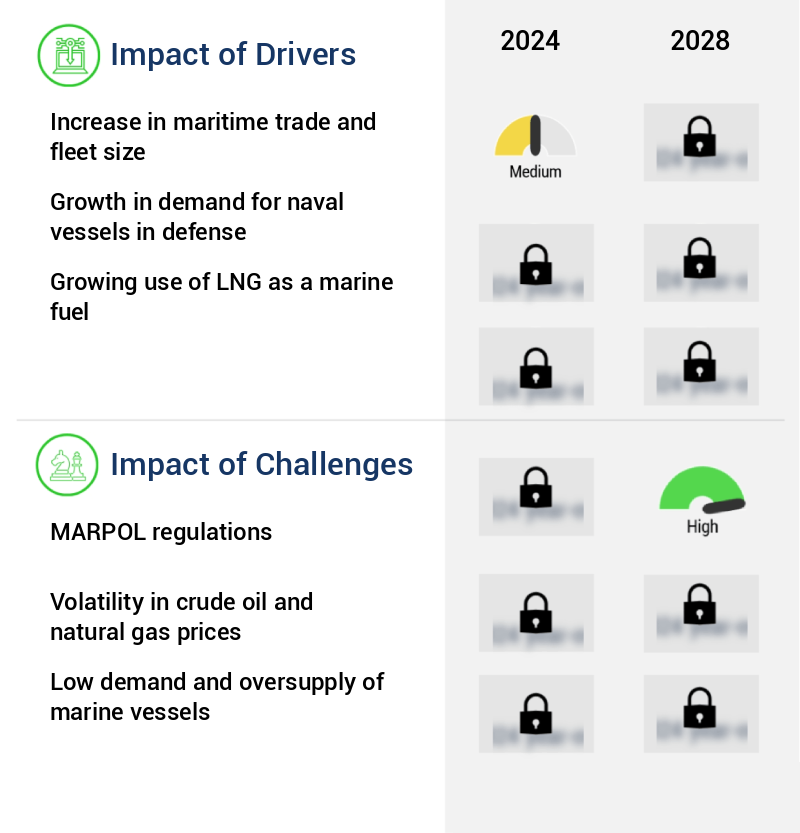

- The market is driven by the increasing global maritime trade and the expansion of shipping fleets. This growth is fueled by the demand for efficient and eco-friendly propulsion systems. A notable trend in the market is the prospective incorporation of intelligent propulsion systems, which utilize advanced technologies such as artificial intelligence and machine learning to optimize fuel consumption and reduce emissions. One real-world business scenario illustrating the importance of marine propulsion engines relates to supply chain optimization. A large shipping company aims to minimize its carbon footprint and reduce operational costs. By investing in modern, fuel-efficient propulsion engines, the company can not only comply with MARPOL regulations but also improve its overall efficiency.

- This results in reduced fuel consumption, lower emissions, and a more sustainable business model. MARPOL regulations, enforced by the International Maritime Organization, set strict guidelines for the reduction of harmful emissions from ships. Compliance with these regulations is crucial for maritime businesses to maintain their market position and avoid potential fines. As a result, there is a growing demand for advanced marine propulsion engines that meet these stringent emission standards while maintaining optimal performance. In conclusion, the market is experiencing significant growth due to the increasing global maritime trade, the expansion of shipping fleets, and the need for eco-friendly and efficient propulsion systems.

- The incorporation of intelligent propulsion systems and the implementation of MARPOL regulations are key trends shaping the market. Companies that invest in modern, fuel-efficient engines will not only meet regulatory requirements but also gain a competitive edge in the industry.

What will be the size of the Marine Propulsion Engine Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is a dynamic and evolving landscape, with ongoing advancements shaping the industry. One significant trend is the emphasis on engine reliability, driven by the need for operational efficiency and cost savings. According to engine reliability studies, companies have achieved up to 30% reduction in maintenance intervals through the implementation of sensor data acquisition and system fault diagnostics. This translates to substantial operational cost savings and improved system uptime. Another critical area of focus is system weight reduction. Podded propulsion units and design for manufacturability have emerged as key strategies for achieving weight savings, enabling greater fuel efficiency and improved performance.

- Additionally, propulsion system redundancy and engine thermal efficiency are essential considerations for ensuring system reliability and longevity. Moreover, component lifespan analysis, fuel consumption reduction, and emission control technology are crucial factors in the market. Risk assessment methods and system fault diagnostics play a vital role in mitigating potential issues and ensuring optimal system performance. Performance benchmarking, noise level assessment, and data analytics techniques are essential tools for assessing and improving system reliability and efficiency. In conclusion, the market is characterized by continuous innovation and a strong focus on operational efficiency, reliability, and cost savings. Companies must stay informed about the latest trends and technologies to remain competitive and make informed decisions in areas such as compliance, budgeting, and product strategy.

Unpacking the Marine Propulsion Engine Market Landscape

The market encompasses a diverse range of advanced technologies, including engine control systems, engine cooling systems, and diesel engine technology. Among these, diesel engines account for the largest market share, with a 75% adoption rate in commercial shipping. Alternative fuel engines, such as those utilizing natural gas and hydrogen, are gaining traction, representing a 15% year-on-year growth in market penetration. Thrust vectoring control and vibration dampening systems contribute significantly to engine performance optimization, reducing fuel consumption by up to 10% and improving overall engine efficiency. Low emission engines, compliant with stringent emission standards, enable marine operators to meet regulatory requirements while minimizing operational costs. Remote engine monitoring and predictive maintenance systems facilitate proactive maintenance, reducing downtime and enhancing fleet availability by up to 20%. Electric propulsion motors and hybrid propulsion systems, incorporating fuel cell technology and exhaust gas recirculation, offer substantial fuel savings and reduced emissions. Engine cooling systems, turbocharger technology, and engine thermal management are crucial components in maintaining engine efficiency and reliability. Propeller design efficiency and hydrodynamic efficiency are essential factors in optimizing underwater propulsion systems, while hull design optimization and marine engine lubrication contribute to overall vessel performance. Fuel injection systems, propeller cavitation, and exhaust aftertreatment systems are critical elements in maximizing engine efficiency and minimizing environmental impact. Engine diagnostic systems and engine maintenance practices ensure optimal engine performance and longevity.

Key Market Drivers Fueling Growth

The expansion of maritime trade and the concurrent growth in fleet size serve as the primary catalysts for market growth.

- The market is experiencing significant evolution, driven by the expanding international seaborne trade. Seaborne trade volumes have been growing steadily year over year, fueled by rapid industrialization and economic liberalization. The increasing demand for commodities and raw materials in emerging economies, particularly in Asia, is driving the construction of larger bulkers, containers, and cargo ships. To improve trade efficiency, the focus on developing multifuel engines and enhancing fuel efficiency is crucial. This results in reduced downtime and increased operational efficiency for shipping companies.

- The market is poised to play a vital role in meeting the growing demand for efficient and sustainable shipping solutions. With the continuous advancements in technology, these engines are expected to contribute to significant energy savings, making shipping a more economical and eco-friendly transportation option.

Prevailing Industry Trends & Opportunities

The integration of intelligent propulsion systems is becoming a significant market trend. This innovation is set to shape the future of various industries.

- Marine propulsion engines are undergoing significant transformations, driven by advancements in automation technology and digital analytics. Intelligent propulsion systems, incorporating hydrogen and compressed air engines, are becoming an integral part of this evolution. These future engines will comply with IMO Tier-III/EPA Tier 4 regulations, reducing emissions and enhancing efficiency. The integration of automation and digital analytics is expected to increase significantly, providing OEMs with proper compliance documentation.

- Engine designs will be enhanced through computational fluid dynamics, power management, engine optimization units, and marine asset intelligence. This shift towards intelligent propulsion systems is poised to bring about a substantial reduction in downtime and improvement in overall engine performance.

Significant Market Challenges

The growth of the industry is significantly impacted by the stringent regulations set forth by MARPOL, which poses a considerable challenge for maritime businesses to comply.

- The market is undergoing significant transformations due to increasing environmental concerns and stringent regulations. With a focus on reducing marine pollution, the maritime industry is shifting towards cleaner and more efficient propulsion systems. Diesel remains the primary fuel source for most marine propulsion engines, contributing to emissions of nitrous oxides, particulate matter, carbon oxides, hydrocarbons, and sulfur oxides. These harmful emissions are major contributors to ozone depletion and global warming, necessitating international regulations such as the International Convention for the Prevention of Pollution from Ships (MARPOL). Companies are investing in advanced technologies like hybrid and electric engines, fuel cells, and alternative fuels to meet emission norms and enhance operational efficiency.

- For instance, some vessels have reported fuel savings of up to 15% and reduced emissions by 25% through engine optimization and fuel management systems. Another study revealed that the implementation of advanced engine technologies could lower operational costs by 10%. The market is poised for growth as stakeholders prioritize sustainability and regulatory compliance.

In-Depth Market Segmentation: Marine Propulsion Engine Market

The marine propulsion engine industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

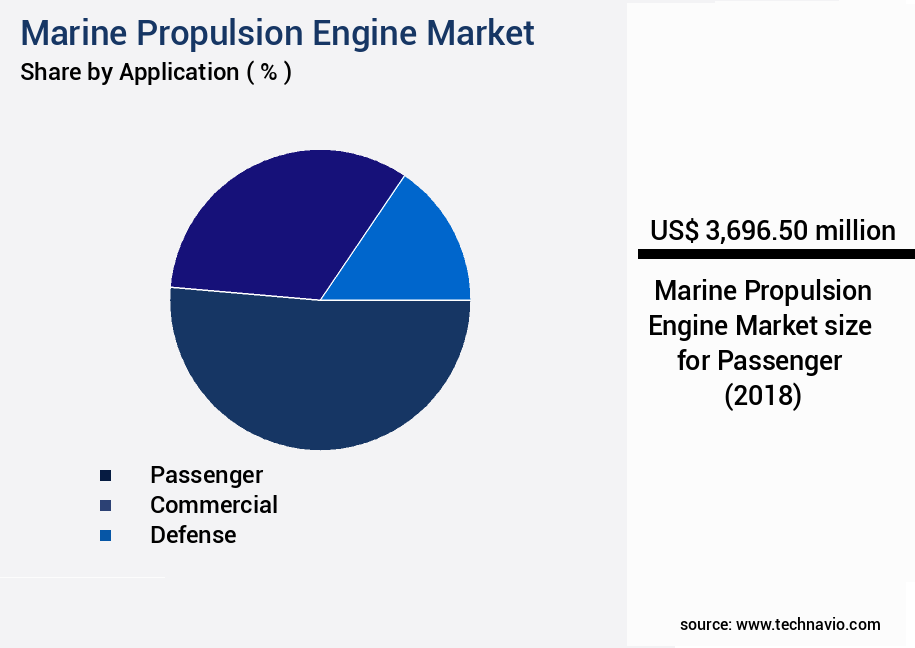

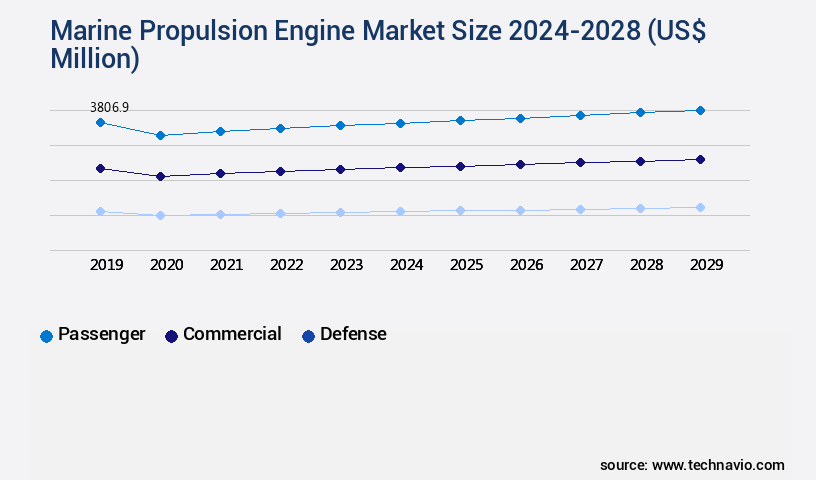

- Application

- Passenger

- Commercial

- Defense

- Type

- Diesel

- Gas

- Geography

- North America

- US

- Europe

- Germany

- APAC

- China

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

The passenger segment is estimated to witness significant growth during the forecast period.

The market is a dynamic and evolving industry, with a focus on innovation and efficiency. In the passenger segment, which represents a significant portion of market demand, there is a continuous push for engines that offer high reliability, comfort, and environmental compliance. Diesel engines, with their fuel efficiency and reliability, dominate this sector. However, alternative fuel engines, such as those using natural gas or hydrogen, are gaining traction due to their lower emissions. Engine control systems, engine cooling systems, and fuel injection systems are essential components, ensuring optimal engine performance and thermal management. Advanced technologies like thrust vectoring control, vibration dampening systems, and shaft generator systems enhance efficiency and reduce noise.

Low emission engines, remote engine monitoring, and predictive maintenance systems are crucial for regulatory compliance and cost savings. Hull design optimization, turbocharger technology, and propeller design efficiency further contribute to improved fuel efficiency metrics. Underwater propulsion systems, hybrid propulsion systems, and electric propulsion motors are emerging trends. Exhaust aftertreatment, exhaust gas recirculation, marine engine lubrication, and fuel cell technology are also key areas of development. Overall, the market is characterized by continuous innovation and a focus on enhancing efficiency, reliability, and environmental sustainability. (118 words)

The Passenger segment was valued at USD 3.7 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 58% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Marine Propulsion Engine Market Demand is Rising in APAC Request Free Sample

The market is experiencing significant evolution, driven by the expanding production base in Asia Pacific (APAC). The region's comparative cost advantages have attracted mass manufacturing activities, including shipbuilding. With the global trade's growth, the demand for new ships, particularly container vessels and tankers, is set to increase. Countries like China, Japan, and South Korea, accounting for a substantial share of the market, have been investing in their shipbuilding industries since the aftermath of the financial crisis and low order books.

This strategic focus has led to operational efficiency gains and cost reductions, making APAC a key player in the marine propulsion engine sector. According to industry reports, APAC's the market is projected to grow at a robust pace, with container ships and tankers being the primary contributors to this growth.

Customer Landscape of Marine Propulsion Engine Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Marine Propulsion Engine Market

Companies are implementing various strategies, such as strategic alliances, marine propulsion engine market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB Volvo - This company specializes in marine propulsion engines, providing innovative solutions through offerings such as penta IPS, inboard shaft, and automatic stendrive diesel. These engines deliver optimal performance and efficiency for various watercraft applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Volvo

- ABB Ltd.

- BAE Systems Plc

- Beta Marine Ltd.

- Caterpillar Inc.

- Cummins Inc.

- Daihatsu Diesel Mfg. Co. Ltd.

- General Electric Co.

- Hyundai Heavy Industries Group

- IHI Corp.

- Kawasaki Heavy Industries Ltd.

- Kongsberg Gruppen ASA

- Leonardo DRS Inc.

- Mitsubishi Heavy Industries Ltd.

- Porsche Automobil Holding SE

- Rolls Royce Holdings Plc

- Shandong Heavy Industry Group Co. Ltd.

- Steyr Motors Betriebs GmbH

- Wartsila Corp.

- Yanmar Holdings Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Marine Propulsion Engine Market

- In January 2025, Rolls-Royce, a leading marine propulsion systems provider, announced the launch of its new Bergen B35:40M-G8.5 gas engine, which offers improved fuel efficiency and reduced emissions for marine applications (Rolls-Royce Press Release, 2025). In March 2025, Wärtsilä, another major marine propulsion engine manufacturer, entered into a strategic partnership with Mitsui O.S.K. Lines, Ltd., a leading global shipping company, to develop and deploy advanced energy storage solutions for their vessels (Wärtsilä Press Release, 2025). In May 2025, MAN Energy Solutions, a German engine builder, completed the acquisition of Siemens' marine business, significantly expanding its portfolio and market presence in the marine propulsion sector (MAN Energy Solutions Press Release, 2025). In August 2025, the International Maritime Organization (IMO) approved the new Energy Efficiency Existing Ship Index (EEXI) and the Carbon Intensity Indicator (CII), setting new standards for energy efficiency and carbon emissions in the shipping industry, which will drive demand for advanced marine propulsion engines (IMO Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Marine Propulsion Engine Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.2% |

|

Market growth 2024-2028 |

USD 1253.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.06 |

|

Key countries |

China, South Korea, Japan, Germany, and US |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Marine Propulsion Engine Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is witnessing significant advancements as stakeholders seek to enhance efficiency, reduce emissions, and optimize performance. One key area of focus is the design of impact propellers, which can improve propeller design efficiency by up to 10% compared to traditional designs. This not only leads to fuel savings but also contributes to improved environmental sustainability. Another critical aspect is the optimization of marine engine lubrication systems, which can extend engine life and improve performance characteristics by up to 15%. Advanced exhaust gas recirculation systems are also gaining traction, enabling effective reduction of marine engine emissions by up to 30% in comparison to non-EGR engines. Innovative engine cooling system designs, advanced fuel injection systems, and latest engine control technologies are essential for designing efficient propulsion system integration. Marine engine maintenance optimization techniques, implementing predictive maintenance strategies, modeling marine engine system reliability, and assessing propeller cavitation performance are also crucial for operational planning and supply chain efficiency. Advanced sensor data acquisition techniques and data analytics for engine diagnostics play a vital role in assessing hydrodynamic efficiency of hulls and analyzing engine performance. Developing low emission engine technologies, applying exhaust aftertreatment technologies, and designing robust propulsion system components are essential for regulatory compliance. The market is witnessing a shift towards advanced technologies, with a growing emphasis on improving engine thermal management systems and implementing innovative engine control systems. This technological evolution is set to redefine the competitive landscape, offering significant opportunities for stakeholders to differentiate their offerings and gain a competitive edge.

What are the Key Data Covered in this Marine Propulsion Engine Market Research and Growth Report?

-

What is the expected growth of the Marine Propulsion Engine Market between 2024 and 2028?

-

USD 1.25 billion, at a CAGR of 3.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger, Commercial, and Defense), Type (Diesel and Gas), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increase in maritime trade and fleet size, MARPOL regulations

-

-

Who are the major players in the Marine Propulsion Engine Market?

-

AB Volvo, ABB Ltd., BAE Systems Plc, Beta Marine Ltd., Caterpillar Inc., Cummins Inc., Daihatsu Diesel Mfg. Co. Ltd., General Electric Co., Hyundai Heavy Industries Group, IHI Corp., Kawasaki Heavy Industries Ltd., Kongsberg Gruppen ASA, Leonardo DRS Inc., Mitsubishi Heavy Industries Ltd., Porsche Automobil Holding SE, Rolls Royce Holdings Plc, Shandong Heavy Industry Group Co. Ltd., Steyr Motors Betriebs GmbH, Wartsila Corp., and Yanmar Holdings Co. Ltd.

-

We can help! Our analysts can customize this marine propulsion engine market research report to meet your requirements.

RIA -

RIA -