Mechanical Ventilators Market Size 2024-2028

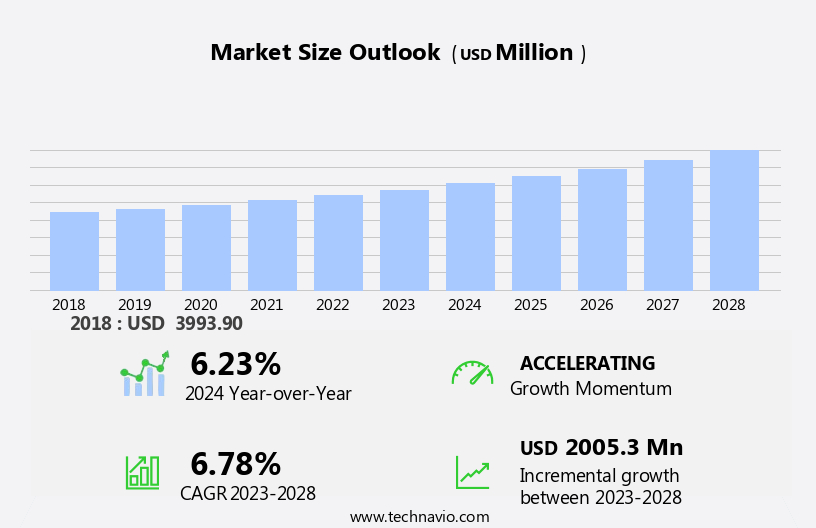

The mechanical ventilators market size is forecast to increase by USD 2.01 billion at a CAGR of 6.78% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing prevalence of respiratory diseases and technological advancements in ventilator technology. The rising number of patients suffering from chronic obstructive pulmonary disease (COPD), asthma, and other respiratory disorders is driving the demand for mechanical ventilators. Moreover, technological advancements such as miniaturization, wireless connectivity, and integration of artificial intelligence (AI) in ventilators are enhancing their functionality and making them more patient-friendly. However, the use of mechanical ventilators also poses several risks, including ventilator-associated pneumonia, barotrauma, and vascular complications. These factors are expected to provide both opportunities and challenges to the market In the coming years.

What will be the Size of the Mechanical Ventilators Market During the Forecast Period?

- The mechanical ventilators market encompasses a range of respiratory devices designed to assist or replace the function of the human respiratory system in patients suffering from various acute and chronic respiratory conditions. These conditions include asthma, obstructive sleep apnea, exertional dyspnea, pulmonary embolism, and other respiratory interventions. They are essential for managing critical care cases, such as intensive care unit patients, neonates, and adults, as well as pediatric and adult cases requiring mobility.

- Moreover, disease management for chronic diseases like chronic obstructive pulmonary disease (COPD) and cystic fibrosis also relies heavily on them. Portable ventilators offer greater flexibility for patients with respiratory disorders, allowing for treatment outside of hospital settings. However, the risk of complications such as ventilator-associated pneumonia remains a concern. The market is expected to grow due to the increasing prevalence of respiratory disorders, the ongoing development of advanced ventilator technologies, and the ongoing vaccination programs aimed at preventing acute medical conditions.

How is this Mechanical Ventilators Industry segmented and which is the largest segment?

The mechanical ventilators industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Hospitals

- Ambulatory surgery centers

- Home-care settings

- Product

- Critical care ventilators

- Portable ventilators

- Neonatal

- Technology

- Non-invasive

- Invasive

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

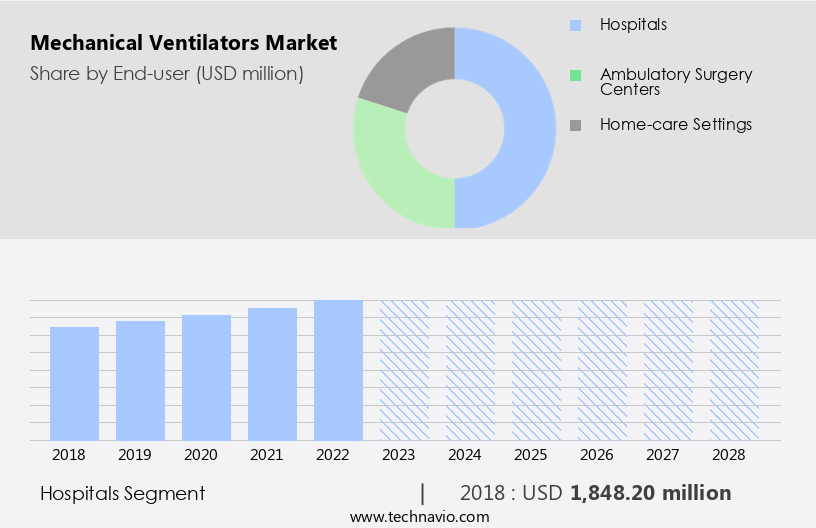

By End-user Insights

- The hospitals segment is estimated to witness significant growth during the forecast period.

The market is driven by the increasing prevalence of chronic respiratory conditions, such as asthma, obstructive sleep apnea, and exertional dyspnea, among other respiratory disorders. They are essential medical devices used to treat patients with acute or chronic respiratory failure, including pulmonary embolism and spinal cord injuries. These devices facilitate artificial breathing and provide oxygen to patients with compromised respiratory functions. Advanced technological developments, such as smart technology, digital sensors, and non-invasive ventilators, have significantly improved patient comfort and treatment outcomes. The geriatric population and lifestyle influences are significant factors contributing to the growth of this market. Healthcare reforms and regulatory standardization have increased the demand in-home care, ambulatory centers, hospitals, and skilled healthcare providers.

Moreover, the market caters to various patient populations, including pediatric and adult cases, with a focus on disease management and mobility. They are used to treat a range of acute medical conditions, such as ventilator-associated pneumonia and intensive care ventilators for neonates and adults. The market also includes portable ventilators for patients with mobility issues or those requiring respiratory support during transportation. In summary, The market is poised for growth due to the increasing prevalence of chronic diseases, technological advancements, and regulatory standardization. These devices are essential for treating various respiratory disorders, providing patient comfort, and improving treatment outcomes.

Get a glance at the Mechanical Ventilators Industry report of share of various segments Request Free Sample

The hospitals segment was valued at USD 1.85 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

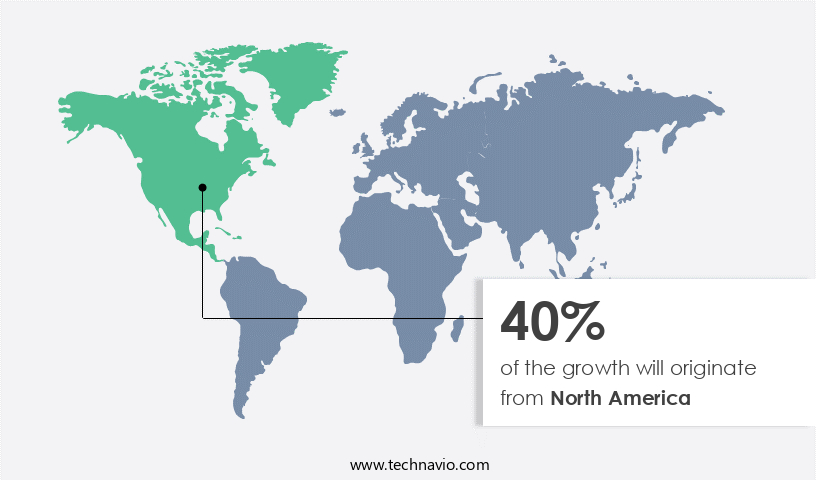

- North America is estimated to contribute 40% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in North America is experiencing significant growth due to the increasing prevalence of chronic respiratory conditions, such as asthma and obstructive sleep apnea, as well as the rising incidence of acute medical conditions, including exertional dyspnea, pulmonary embolism, and respiratory interventions for critical care patients. Additionally, the geriatric population's expansion, lifestyle influences, and healthcare reforms are contributing factors.

Moreover, advanced technologies, such as smart technology, digital sensors, and non-invasive ventilators, are improving patient comfort, efficacy, and treatment outcomes. These technological advancements are particularly important for managing chronic diseases, such as asthma and obstructive sleep apnea, and for home care, ambulatory centers, hospitals, and skilled healthcare providers. The market is further driven by the increasing prevalence of sleep apnea in pediatric and adult cases, mobility issues, and the need for disease management in patients. The global market is also influenced by regulatory standardization and the availability of portable ventilators for various respiratory disorders and acute medical conditions, including spinal cord injury and stroke.

Market Dynamics

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Mechanical Ventilators Industry?

Increasing prevalence of respiratory diseases is the key driver of the market.

- The mechanical ventilator market is experiencing notable growth due to the expanding healthcare infrastructure In the US. This growth can be attributed to the increasing demand for advanced respiratory interventions to manage chronic respiratory conditions such as asthma, obstructive sleep apnea, and exertional dyspnea. Additionally, the geriatric population, with its higher prevalence of chronic diseases and respiratory disorders, is a significant market driver. Technological advancements, including smart technology, digital sensors, and portable devices, are improving patient comfort and efficacy, leading to better treatment outcomes.

- Moreover, healthcare reforms and regulatory standardization are also fostering market growth. The market caters to various settings, including hospitals, ambulatory centers, home care, and skilled healthcare providers. These are essential in treating acute medical conditions such as pulmonary embolism, spinal cord injury, and stroke. The market encompasses various types, including non-invasive ventilators, intensive care ventilators, and portable ventilators, catering to pediatric and adult cases. Disease management programs, vaccination programs, and home healthcare services are also contributing to the market's expansion. However, the risk of ventilator-associated pneumonia remains a concern, necessitating continuous research and innovation in mechanical ventilator technology.

What are the market trends shaping the Industry?

Technological advancements are the upcoming market trend.

- The market is experiencing significant growth due to the increasing prevalence of chronic respiratory conditions, such as asthma, obstructive sleep apnea, and exertional dyspnea, In the US population. Technological advancements are playing a crucial role in this expansion, as these devices become more sophisticated and effective in treating various respiratory interventions. The geriatric population, with its higher susceptibility to chronic diseases and respiratory disorders, is a key target demographic for these advanced ventilators. Smart technology, digital sensors, and personalized ventilation modes are some of the features that are increasingly being incorporated to improve patient comfort, efficacy, and treatment outcomes. These technological innovations are particularly important for managing complex respiratory conditions, such as pulmonary embolism, spinal cord injury, and stroke. The market is diverse, with applications ranging from intensive care units in hospitals to home care and ambulatory centers. Skilled healthcare providers, including physicians, nurses, and respiratory therapists, are the primary users of these devices. The growing trend towards healthcare reforms and regulatory standardization is also driving the demand, particularly In the areas of non-invasive ventilators and home healthcare.

- Moreover, the market is not limited to adults but also includes pediatric cases and neonates. Portable ventilators are gaining popularity due to their mobility and convenience, making them ideal for treating patients with respiratory disorders in various settings. The market is also witnessing an increasing focus on disease management, with vaccination programs and chronic disease initiatives playing a crucial role in reducing the incidence and prevalence of acute medical conditions. Despite the numerous benefits, there are challenges associated with their use, such as the risk of ventilator-associated pneumonia and the need for ongoing maintenance and calibration. However, the potential benefits of these devices in improving patient outcomes and enhancing clinical efficiency far outweigh these challenges. Overall, the market is poised for continued growth, driven by the increasing prevalence of respiratory disorders, technological advancements, and the changing healthcare landscape.

What challenges does the Mechanical Ventilators Industry face during its growth?

Several risks associated with the use of mechanical ventilators are key challenges affecting the industry growth.

- Mechanical ventilators are essential respiratory interventions used to manage various acute and chronic respiratory conditions, including asthma, obstructive sleep apnea, exertional dyspnea, pulmonary embolism, and other respiratory disorders. These devices provide artificial breathing to patients who cannot breathe adequately on their own due to illness or injury. The mechanical ventilator market caters to diverse patient populations, including geriatric patients, pediatric cases, and adults, with technological advanced devices offering enhanced patient comfort and efficacy. Chronic respiratory conditions, such as asthma and obstructive sleep apnea, are prevalent among the aging populations, influenced by lifestyle factors and healthcare reforms. Mechanical ventilators are employed in ambulatory centers, hospitals, and home care settings, with the increasing popularity of non-invasive ventilators enabling home healthcare.

- Moreover, smart technology and digital sensors are integrated into modern mechanical ventilators to optimize treatment outcomes, monitor patient status, and facilitate disease management. Technological advancements in mechanical ventilators have led to the development of portable ventilators, enabling mobility and flexibility in patient care. Regulatory standardization and vaccination programs aim to reduce the risk of ventilator-associated pneumonia and other complications. Mechanical ventilators are also used In the treatment of acute medical conditions, such as spinal cord injury and stroke. The market for mechanical ventilators continues to grow, driven by the increasing prevalence of chronic diseases and the need for effective respiratory devices.

Exclusive Customer Landscape

The mechanical ventilators market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the mechanical ventilators market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, mechanical ventilators market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry. The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Liquide SA

- Allied Healthcare Products Inc.

- Asahi Kasei Corp.

- Boston Scientific Corp.

- Dragerwerk AG and Co. KGaA

- Fisher and Paykel Healthcare Corp. Ltd.

- General Electric Co.

- Getinge AB

- Hamilton Co.

- ICU Medical Inc.

- Koninklijke Philips N.V.

- Medtronic Plc

- MicroPort Scientific Corp.

- Nihon Kohden Corp.

- ResMed Inc.

- SCHILLER AG

- Shenzhen Mindray BioMedical Electronics Co. Ltd

- Smiths Group Plc

- Stryker Corp.

- Vyaire Medical Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Mechanical ventilators have emerged as essential medical devices in managing various respiratory conditions. These conditions include chronic respiratory diseases such as asthma, obstructive sleep apnea, and exertional dyspnea, as well as acute medical situations like pulmonary embolism. The market for mechanical ventilators has witnessed significant growth due to the increasing prevalence of these conditions, particularly In the aging population. Technological advancements have played a pivotal role In the evolution of mechanical ventilators. Smart technology and digital sensors have enabled the development of more efficient and patient-friendly devices. These technological innovations aim to enhance patient comfort and improve treatment outcomes. The prevalence of chronic respiratory conditions is on the rise due to lifestyle influences and aging populations. Chronic diseases like asthma and obstructive sleep apnea affect millions of adults and children In the United States. According to the American Lung Association, over 25 million Americans have asthma, and more than 22 million Americans have sleep apnea. The geriatric population, in particular, is at a higher risk of developing respiratory conditions.

As per the Centers for Disease Control and Prevention (CDC), over 60% of adults aged 65 and older have chronic lung disease. Moreover, respiratory interventions have become increasingly common in intensive care units (ICUs) and hospitals, further driving the demand for mechanical ventilators. Healthcare reforms and regulatory standardization have also contributed to the growth of the mechanical ventilator market. For instance, the Affordable Care Act (ACA) has expanded healthcare coverage for millions of Americans, leading to increased demand for medical devices like mechanical ventilators. Additionally, regulatory bodies like the Food and Drug Administration (FDA) have set stringent standards for the manufacturing and distribution of mechanical ventilators, ensuring their safety and efficacy. The market for mechanical ventilators is diverse, catering to various end-users, including skilled healthcare providers, home care, ambulatory centers, and hospitals. Non-invasive ventilators have gained popularity in home healthcare settings due to their portability and ease of use.

Thus, these devices allow patients to receive treatment In the comfort of their homes, reducing the need for hospitalization. Mechanical ventilators are also used in treating pediatric and adult cases of respiratory disorders. For instance, neonates with respiratory distress syndrome and adults with spinal cord injuries or stroke require mechanical ventilation to breathe. Moreover, mechanical ventilators play a crucial role in managing ventilator-associated pneumonia (VAP), a common complication in patients receiving prolonged mechanical ventilation. In summary, the market for mechanical ventilators is driven by the increasing prevalence of respiratory conditions, technological advancements, healthcare reforms, and regulatory standardization. These devices are essential in managing various respiratory conditions, from chronic diseases to acute medical situations. The market caters to diverse end-users, including hospitals, skilled healthcare providers, home care, and ambulatory centers. As the population ages and the prevalence of respiratory conditions continues to rise, the demand for mechanical ventilators is expected to grow.

|

Mechanical Ventilators Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

192 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.78% |

|

Market growth 2024-2028 |

USD 2.01 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.23 |

|

Key countries |

US, UK, Germany, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Mechanical Ventilators Market Research and Growth Report?

- CAGR of the Mechanical Ventilators industry during the forecast period

- Detailed information on factors that will drive the Mechanical Ventilators growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the mechanical ventilators market growth of industry companies

We can help! Our analysts can customize this mechanical ventilators market research report to meet your requirements.

RIA -

RIA -