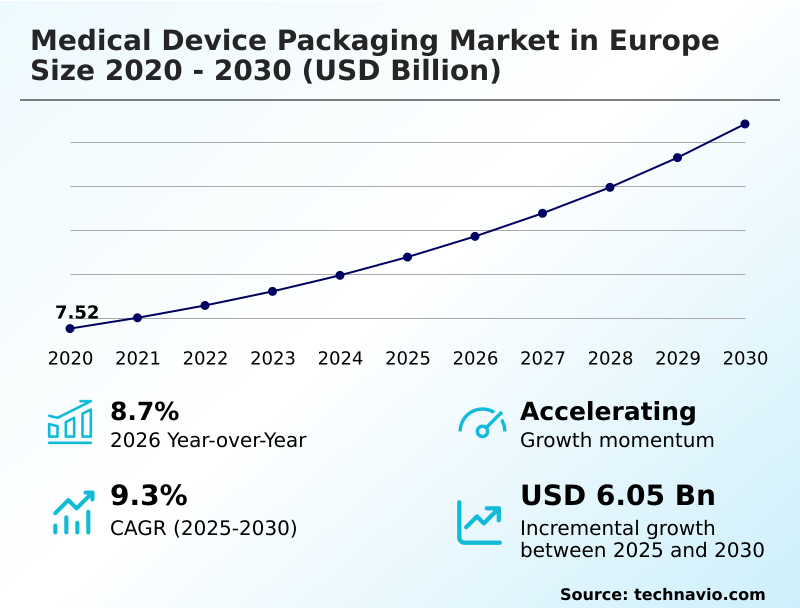

Europe Medical Device Packaging Market Size 2026-2030

The europe medical device packaging market size is valued to increase by USD 6.05 billion, at a CAGR of 9.3% from 2025 to 2030. Legislative mandates for circular economy will drive the europe medical device packaging market.

Major Market Trends & Insights

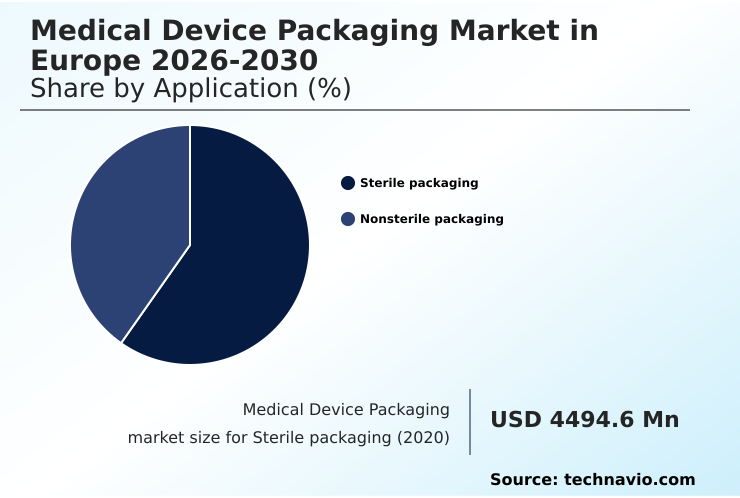

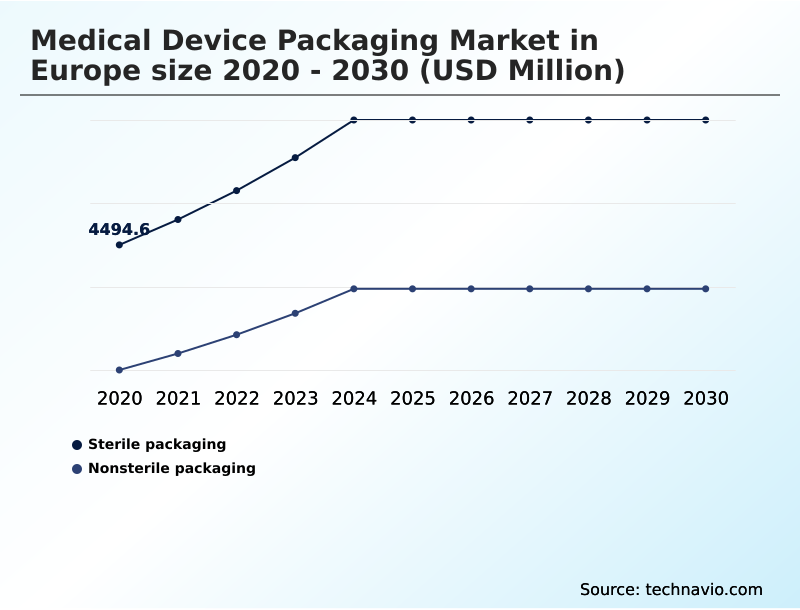

- By Application - Sterile packaging segment was valued at USD 5.96 billion in 2024

- By Product - Pouches segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.30 billion

- Market Future Opportunities: USD 6.05 billion

- CAGR from 2025 to 2030 : 9.3%

Market Summary

- The medical device packaging market in Europe is navigating a complex period of transformation, defined by the convergence of stringent safety regulations and ambitious sustainability goals. The central dynamic involves harmonizing the unyielding requirements of the medical device regulation, which prioritizes patient safety through proven materials, with new environmental laws that penalize non-recyclable formats.

- This has catalyzed a market-wide pivot toward innovation in mono-material structures and high-barrier paper systems that can maintain a sterile barrier system while supporting a circular economy. Concurrently, the push for supply chain localization is reshaping manufacturing footprints, with investment flowing into regional cleanroom capacities to mitigate geopolitical risks and shorten lead times.

- For instance, a mid-sized device manufacturer faces the challenge of re-validating its entire packaging portfolio to align with new eco-design mandates. This requires significant capital investment not only in new medical-grade polymers but also in the testing and documentation needed to prove ISO 11607 compliance, all while ensuring continuous supply to clinical end-users.

- This environment favors providers who offer pre-validated packaging systems and comprehensive regulatory support, reducing the burden on device OEMs and accelerating their transition to compliant, sustainable solutions.

What will be the Size of the Europe Medical Device Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Medical Device Packaging Market Segmented?

The europe medical device packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Sterile packaging

- Nonsterile packaging

- Product

- Pouches

- Trays

- Clamshells

- Others

- Material

- Plastic

- Paper and paperboard

- Metal

- Others

- Geography

- Europe

- Germany

- UK

- France

- Europe

By Application Insights

The sterile packaging segment is estimated to witness significant growth during the forecast period.

The sterile packaging segment is governed by the absolute necessity of maintaining a sterile barrier system from manufacturing to the point of aseptic presentation. This requires strict adherence to the medical device regulation and robust heat-sealing techniques to prevent contamination.

Market activity is defined by a dual focus on sustainable sterile packaging and supply chain security, driving demand for near-shore packaging supply.

Material science focuses on ensuring superior microbial barrier properties and minimizing particulate matter generation, especially for devices undergoing gas sterilization modalities.

Innovations aim to achieve delamination risk prevention in complex materials while also simplifying the overall system to support a circular economy.

The Sterile packaging segment was valued at USD 5.96 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the current landscape requires a sophisticated approach to combining mdr and ppwr packaging requirements, pushing engineers toward a mono-material design for sterile packaging. This pivot necessitates the difficult process of validating new materials under mdr, a challenge compounded by the urgent search for pfas replacement in medical grade paper.

- The goal is to develop solutions like a recyclable blister pack for pharmaceuticals that do not compromise safety. This extends to complex devices, where finding appropriate packaging solutions for orthopedic implants is critical. To enhance efficiency and security, rfid integration in medical device packaging is becoming essential for tracking high-value assets.

- This is particularly vital for temperature monitoring for cold chain biologics, a process often managed with smart labels for clinical trial supplies. Such technologies are crucial for advanced polymer vials for gene therapies, which have stringent storage needs. Optimizing the entire system involves improving aseptic presentation with no-touch design and refining processes like optimizing packaging for ethylene oxide sterilization.

- Many OEMS now consider outsourcing sterile packaging and validation to specialized partners to manage costs and complexity. The industry is also exploring novel solutions like laser-cleaning technology for reusable trays and non-woven wraps for autoclave sterilization, all while advancing high-barrier films for oxygen-sensitive devices and developing better antimicrobial coatings for medical pouches.

- These efforts collectively address the core challenge of ensuring circular economy compliance for medical packaging while simultaneously improving supply chain resilience in healthcare packaging and reducing plastic volume in thermoformed trays.

What are the key market drivers leading to the rise in the adoption of Europe Medical Device Packaging Industry?

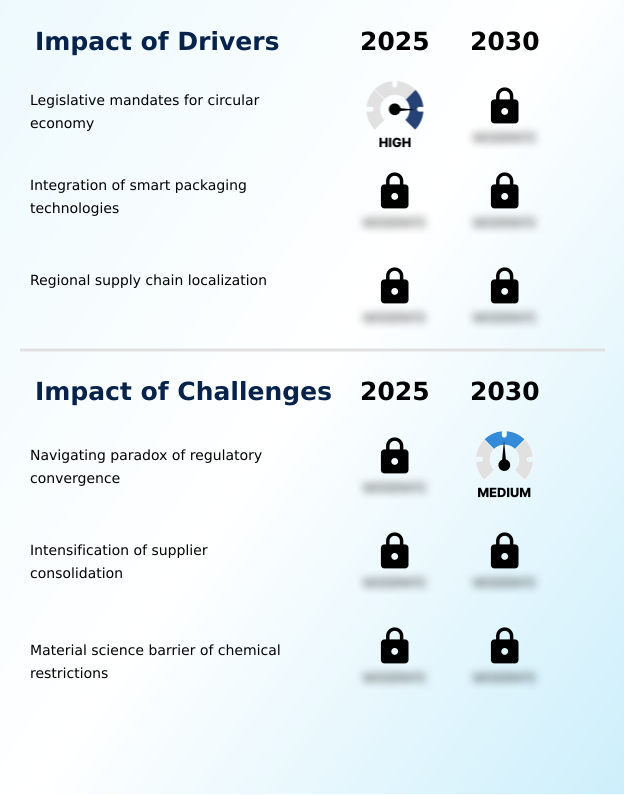

- Legislative mandates for a circular economy are a key driver influencing the market's trajectory.

- Legislative pressure and supply chain evolution are the primary market drivers. The packaging and packaging waste regulation, underpinned by circular economy principles, is forcing a strategic pivot in material sourcing.

- Adherence to extended producer responsibility schemes is now a primary factor in over 85% of material sourcing decisions, accelerating the adoption of bio-based plastics and high-performance films. The goal of polyvinyl chloride elimination is also gaining momentum.

- Concurrently, the imperative for supply chain localization has reduced logistics-related lead times by an average of 30%. This shift favors regional producers of high-clarity polymers.

- Digital mandates for unique device identification are also compelling manufacturers to adopt smarter, more traceable solutions, with many leveraging pre-validated packaging systems to expedite compliance.

What are the market trends shaping the Europe Medical Device Packaging Industry?

- A predominant trend is the market's accelerated shift toward sustainable material innovation. This includes a notable transition to mono-material structures to meet circularity goals.

- Key market trends are centered on the convergence of sustainability and digitalization. The industry is rapidly adopting mono-material structures and high-barrier paper systems to comply with stringent eco-design mandates. This transition toward a recyclable thermoform solution is critical, with adoption increasing recyclability rates by 40% in certain device categories. Parallel to material science, smart packaging integration is transforming supply chains.

- The deployment of technologies like an NFC temperature logger and other sensors has improved traceability by over 99%. These features, combined with tamper-evident features, enable robust anti-counterfeiting verification. This digitalization extends to the end-user through digital instructions for use, which streamline clinical workflows and support automated inventory management.

What challenges does the Europe Medical Device Packaging Industry face during its growth?

- A key challenge affecting industry growth is navigating the paradox of regulatory convergence.

- The market faces significant hurdles in balancing conflicting regulatory demands and material science limitations. Achieving ISO 11607 compliance with novel, sustainable materials is a primary challenge, with validation costs increasing by up to 50%. The search for effective pfas-free materials is intense, as alternatives must not compromise safety.

- This is especially critical for combination product packaging and packaging for advanced therapy medicinal products, where material interaction is a major concern. The logistical complexity of cold chain logistics for these biologics can represent over 60% of the product's distribution cost. Furthermore, while the industry explores reusable medical trays, the operational and sterilization challenges remain high.

- The rise of robotic surgery packaging demands highly customized solutions that are difficult to standardize, often requiring the specialized expertise of a contract development manufacturing organization.

Exclusive Technavio Analysis on Customer Landscape

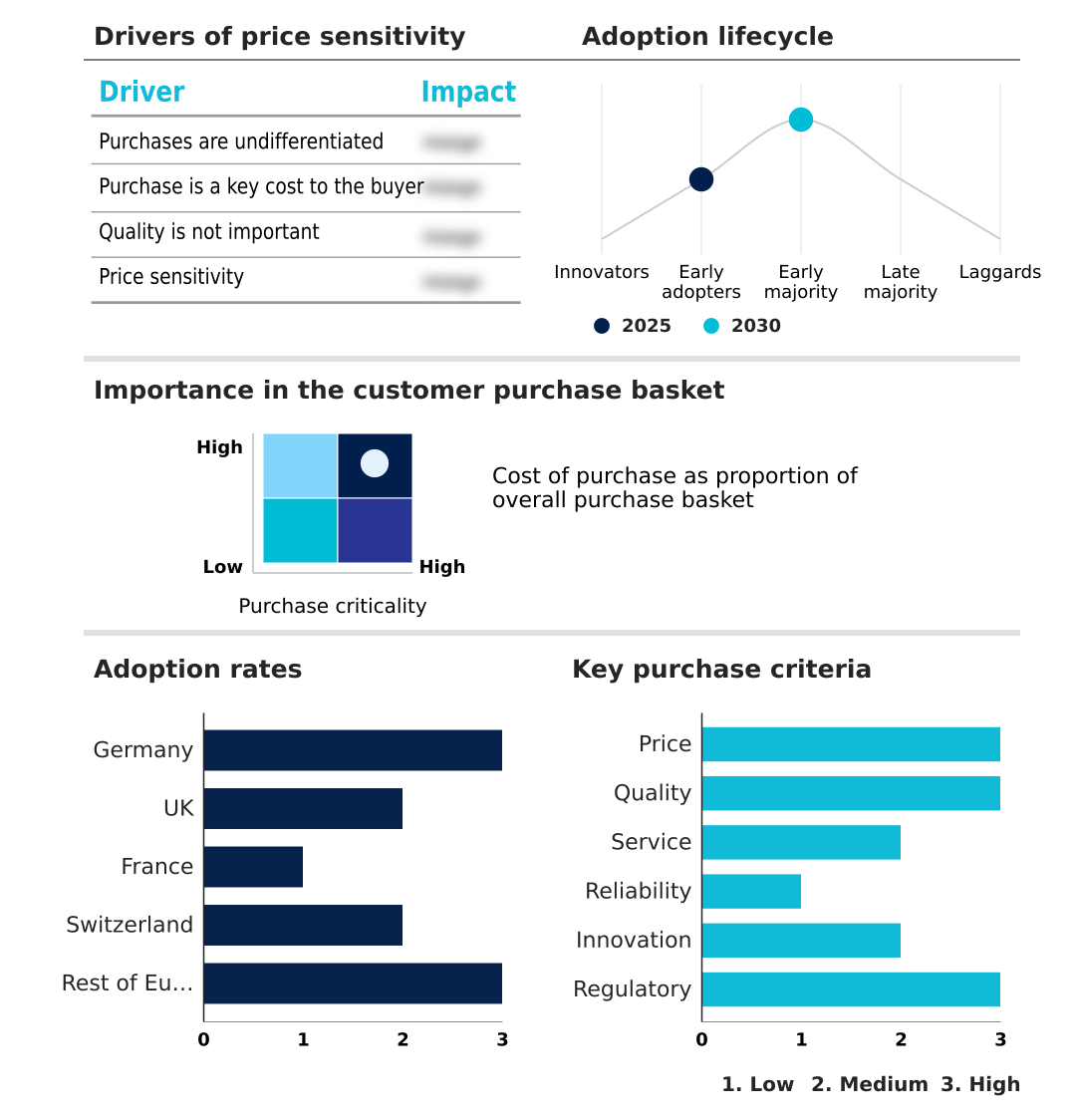

The europe medical device packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe medical device packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Medical Device Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe medical device packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aluflexpack AG - Analysis indicates a focus on advanced barrier materials and integrated packaging systems designed for stringent regulatory compliance and product integrity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aluflexpack AG

- Amcor Plc

- Berry Global Inc.

- Constantia Flexibles GmbH

- Coveris Management GmbH

- Daklapack Group

- DuPont de Nemours Inc.

- Gerresheimer AG

- Huhtamaki Oyj

- KP Holding GmbH and Co. KG

- Mondi Plc

- Oliver Healthcare Packaging

- RENOLIT SE

- Sonoco Products Co.

- SUDPACK Holding GmbH

- Technipaq Inc.

- Wihuri International Oy

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe medical device packaging market

- In August, 2024, Oliver Healthcare Packaging joined the Healthcare Plastics Recycling Council, a global consortium focused on designing and implementing viable recycling streams for clinical plastics.

- In November, 2024, Amcor announced a definitive agreement to acquire Berry Global in an all-stock transaction, a move poised to create a global packaging leader with extensive healthcare sector expertise.

- In January, 2025, Huhtamaki received the Eco-Design Award at Pharmapack Europe for its Omnilock Ultra PAPER solution, a fully recyclable, paper-based flexible packaging innovation with high-barrier properties.

- In March, 2025, West Pharmaceutical Services completed a major capacity expansion at its manufacturing facility in Dublin, Ireland, adding cleanroom space and advanced equipment to meet growing regional demand.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Medical Device Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 216 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.3% |

| Market growth 2026-2030 | USD 6045.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.7% |

| Key countries | Germany, UK, France, Switzerland and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The European market is defined by a fundamental redesign of the sterile barrier system, driven by the dual pressures of regulatory compliance and sustainability. This requires a shift toward innovative medical-grade polymers and mono-material structures that satisfy both ISO 11607 compliance and circular economy principles.

- Boardroom decisions are increasingly focused on the capital expenditure needed for cleanroom class 7 upgrades and R&D for next-generation materials. The successful integration of technologies supporting unique device identification and supply chain localization is now a key differentiator.

- The process of aseptic presentation is being re-evaluated to minimize particulate matter generation, while sterilization compatibility, covering both gamma radiation and ethylene oxide sterilization, remains a primary concern. The adoption of pre-validated packaging systems has become a key strategy, with some firms achieving a 30% reduction in time-to-market for new devices.

- As the industry moves away from legacy materials, polyvinyl chloride elimination and the development of recyclable thermoform solutions are paramount. This complex environment creates opportunities for the contract development manufacturing organization sector, which offers specialized expertise in navigating these technical and regulatory hurdles.

What are the Key Data Covered in this Europe Medical Device Packaging Market Research and Growth Report?

-

What is the expected growth of the Europe Medical Device Packaging Market between 2026 and 2030?

-

USD 6.05 billion, at a CAGR of 9.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Sterile packaging, and Nonsterile packaging), Product (Pouches, Trays, Clamshells, and Others), Material (Plastic, Paper and paperboard, Metal, and Others) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Legislative mandates for circular economy, Navigating paradox of regulatory convergence

-

-

Who are the major players in the Europe Medical Device Packaging Market?

-

Aluflexpack AG, Amcor Plc, Berry Global Inc., Constantia Flexibles GmbH, Coveris Management GmbH, Daklapack Group, DuPont de Nemours Inc., Gerresheimer AG, Huhtamaki Oyj, KP Holding GmbH and Co. KG, Mondi Plc, Oliver Healthcare Packaging, RENOLIT SE, Sonoco Products Co., SUDPACK Holding GmbH, Technipaq Inc. and Wihuri International Oy

-

Market Research Insights

- Market dynamics are increasingly shaped by the dual imperatives of sustainability and digitalization. The push for pfas-free materials and bio-based plastics is accelerating, with firms adopting such solutions reporting a 20% improvement in alignment with forthcoming environmental regulations. Concurrently, smart packaging integration is becoming standard for high-value devices.

- Systems incorporating anti-counterfeiting verification and automated inventory management have been shown to reduce stock discrepancies in hospital settings by up to 35%. The need for specialized combination product packaging and solutions for advanced therapy medicinal products further drives innovation in high-performance films and high-clarity polymers that ensure product stability and safety.

- These shifts require significant R&D investment but create high-value opportunities.

We can help! Our analysts can customize this europe medical device packaging market research report to meet your requirements.

RIA -

RIA -