Metal Material Based 3D Printing Market Size 2026-2030

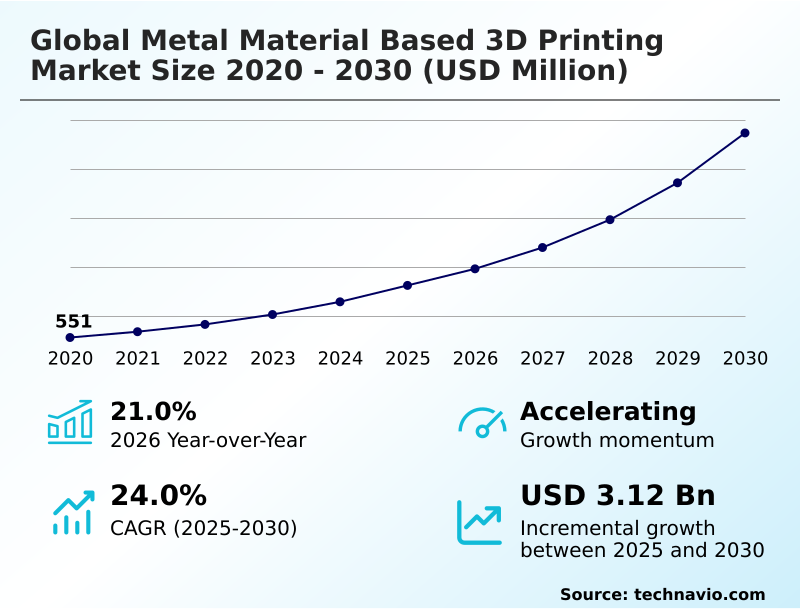

The metal material based 3d printing market size is valued to increase by USD 3.12 billion, at a CAGR of 24% from 2025 to 2030. Accelerated industrialization within aerospace and defense supply chains will drive the metal material based 3d printing market.

Major Market Trends & Insights

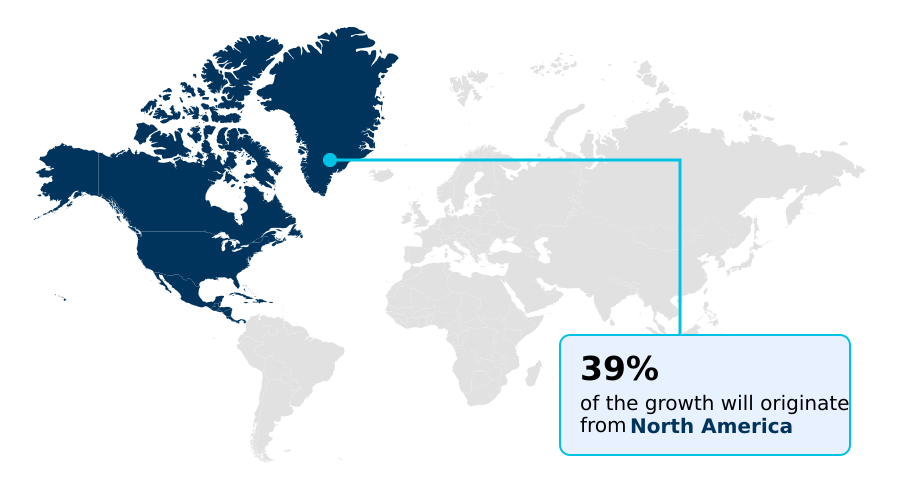

- North America dominated the market and accounted for a 39.1% growth during the forecast period.

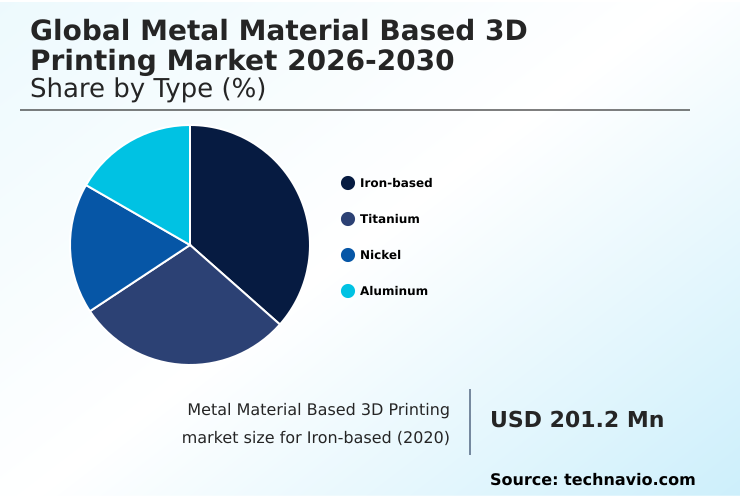

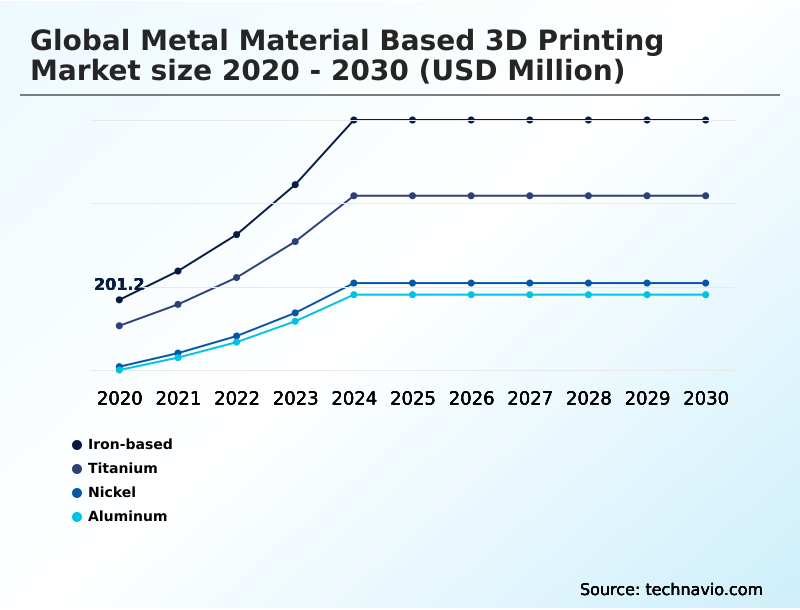

- By Type - Iron-based segment was valued at USD 481.3 million in 2024

- By End-user - Healthcare segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.18 billion

- Market Future Opportunities: USD 3.12 billion

- CAGR from 2025 to 2030 : 24%

Market Summary

- The metal material based 3D printing market is transitioning from a specialized prototyping tool to a mainstream manufacturing process for serial production. This evolution is driven by the demand for high-performance, lightweight components in sectors such as aerospace and healthcare.

- The technology enables the creation of parts with complex geometries, such as lattice structures and internal cooling channels, which are unachievable with traditional subtractive methods. Organizations are adopting metal additive manufacturing to improve supply chain resilience, reduce material waste, and create on-demand parts, aligning with sustainability goals.

- For instance, an aerospace supplier can consolidate a multi-part assembly into a single, 3D-printed component, reducing weight and potential points of failure while streamlining production. However, widespread adoption is tempered by the high costs of equipment and specialized metal powders, alongside the need for standardized quality assurance protocols.

- Advancements in real-time process monitoring and the development of new alloys are critical to overcoming these hurdles and unlocking the technology's full industrial potential.

What will be the Size of the Metal Material Based 3D Printing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Metal Material Based 3D Printing Market Segmented?

The metal material based 3d printing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Iron-based

- Titanium

- Nickel

- Aluminum

- End-user

- Healthcare

- Automotive

- Aerospace and defense

- Tool and mold making

- Others

- Technology

- PBF

- DED

- Binder jetting

- Metal extrusion

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The iron-based segment is estimated to witness significant growth during the forecast period.

The iron-based segment is foundational to industrial additive manufacturing, utilizing materials like stainless steel and tool steels for automotive and machinery applications. Organizations leverage stainless steel grades for corrosion-resistant components and tool steels for durable molds featuring conformal cooling channels.

This segment's growth is driven by binder jetting technologies, enabling high-throughput production that competes with metal injection molding.

By employing predictive analytics in the build process, manufacturers achieve enhanced repeatability and have reported up to a 15% reduction in component rejection rates.

This data-driven approach to metal powder management ensures structural integrity, making iron-based additive manufacturing a scalable and cost-effective choice for industrial components, particularly in applications requiring thermal management and high-purity metal powders.

The Iron-based segment was valued at USD 481.3 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Metal Material Based 3D Printing Market Demand is Rising in North America Get Free Sample

The geographic landscape of the global metal material based 3D printing market is shaped by regional industrial priorities.

North America, which accounts for 39.1% of the market's incremental growth, leads due to heavy investment from its aerospace and defense sectors, focusing on advanced powder bed fusion and directed energy deposition systems.

Europe remains a strong contender, driven by its advanced manufacturing ecosystem, particularly in Germany and the UK. Meanwhile, APAC is projected to exhibit the highest regional growth rate at 25.0%, fueled by expanding industrialization and government support for additive manufacturing.

This region's adoption of hybrid manufacturing and metal extrusion techniques is growing.

The ability to perform advanced thermal analysis and utilize refractory metals is becoming a key differentiator across all regions, enabling the production of flight-critical components and specialized industrial machinery parts.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global metal material based 3D printing market is advancing through specialized applications and technological refinements. For instance, large-format metal 3d printing applications are crucial for industries requiring sizable components, while advancements in metal powder production for additive manufacturing ensure the quality and consistency needed for mission-critical parts.

- The use of electron beam melting for aerospace components delivers superior strength and heat resistance, a key advantage over traditional methods. Meanwhile, binder jetting for high-volume production is becoming a cost-effective alternative for serial manufacturing, challenging conventional techniques.

- Companies are increasingly offering directed energy deposition repair services to extend the life of high-value industrial assets, a market segment showing growth over 20% faster than new part production in some areas. The qualification of metal 3d printed parts for medical implants is driven by stringent regulatory standards, ensuring patient safety.

- Furthermore, process monitoring for metal additive manufacturing is essential for quality assurance, just as post-processing of 3d printed metal parts is critical for achieving final specifications. The development of high-performance superalloys for 3d printing and the optimization of multi-laser powder bed fusion systems are pushing the boundaries of what is possible in industrial production.

What are the key market drivers leading to the rise in the adoption of Metal Material Based 3D Printing Industry?

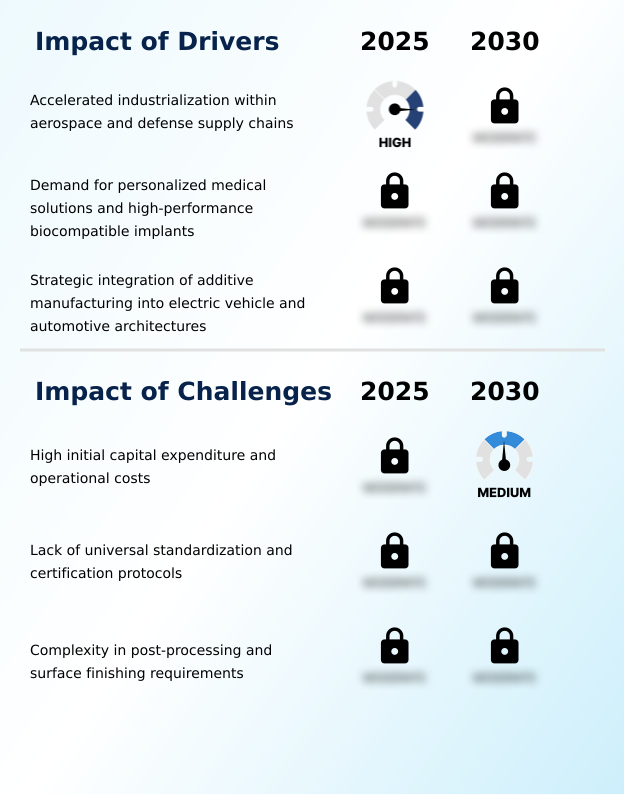

- Accelerated industrialization within aerospace and defense supply chains represents a key driver for the market.

- A significant driver for the global metal material based 3D printing market is the accelerated adoption of additive manufacturing for flight-critical components in the aerospace and defense sectors.

- The need to improve fuel efficiency by lightweighting, with some programs achieving mass reductions of over 30%, propels the use of topology optimization and complex lattice structures.

- These technologies enable the production of parts from high-performance superalloys and custom metal alloys.

- The defense industry leverages metal 3D printing to manufacture obsolete spare parts on demand, ensuring operational readiness and reducing inventory costs by as much as 50% for certain legacy systems.

- This strategic shift towards localized production of high-value metallic parts mitigates supply chain disruptions. The development of refractory metals and advanced metal powders is also expanding the operational capabilities for mission-critical applications.

What are the market trends shaping the Metal Material Based 3D Printing Industry?

- The integration of AI and machine learning for advanced process monitoring is an emerging trend. This development is enhancing manufacturing reliability and efficiency across the industry.

- A primary trend influencing the metal material based 3D printing market is the integration of AI and machine learning for enhanced process control. Stakeholders are deploying sophisticated sensor arrays for in-situ monitoring, allowing for immediate detection of anomalies like porosity, which has been shown to reduce part rejection rates by up to 20%.

- This shift towards a data-driven discipline enables the use of predictive analytics and digital twinning to ensure structural integrity and high repeatability. As organizations adopt these software solutions, a global standardization of digital quality protocols is emerging.

- The focus is on creating a continuous improvement loop where historical build data from multi-laser systems refines future print parameters, making the transition to industrial-scale serial production more viable. This trend is particularly evident in the production of complex components requiring topology optimization and advanced thermal management.

What challenges does the Metal Material Based 3D Printing Industry face during its growth?

- High initial capital expenditure and significant operational costs present a key challenge affecting industry growth.

- A major challenge restraining the global metal material based 3D printing market is the significant capital investment required for industrial-scale facilities. High-end powder bed fusion or directed energy deposition systems, combined with ancillary equipment, create a substantial financial barrier.

- Operational costs, driven by expensive specialized metal powders and high energy consumption, add further pressure, with utility expenses representing up to 15% of the total cost per part in some cases. The need for a highly skilled workforce with expertise in material science and additive design principles increases labor costs.

- The complexity of post-processing, including surface finishing and heat treatment, also adds considerable time and expense, sometimes doubling the initial print time. These economic factors limit the democratization of metal 3D printing, especially for small and medium-sized enterprises seeking a justifiable short-term ROI.

Exclusive Technavio Analysis on Customer Landscape

The metal material based 3d printing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the metal material based 3d printing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Metal Material Based 3D Printing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, metal material based 3d printing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - Key offerings include direct metal printing technologies, enabling the production of complex, industrial-grade metal components for high-stakes aerospace, healthcare, and automotive applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- AddUp

- Carpenter Technology Corp.

- Colibrium Additive

- Desktop Metal Inc.

- DMG MORI CO. LTD.

- EOS GmbH

- Eplus 3D

- GKN Sinter Metals Engineering GmbH

- Hoganas AB

- HP Inc.

- Markforged Holding Corp.

- OC Oerlikon Corp.

- Optomec Inc.

- Renishaw Plc

- Sandvik AB

- Sciaky Inc.

- TRUMPF SE Co. KG

- Velo3D Inc.

- Xjet Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Metal material based 3d printing market

- In August 2025, 3D Systems Corp. received a $7.5 million contract from the U.S. Air Force for its Large-format Metal 3D Printer Advanced Technology Demonstrator, supporting the development of large-scale industrial metal additive manufacturing for high-speed flight applications.

- In October 2025, EOS GmbH expanded its portfolio with four new metal additive manufacturing materials, including EOS FeNi36 and EOS NickelAlloy C22, optimized for laser powder bed fusion systems to serve the aerospace, energy, and automotive industries.

- In March 2025, Backflip AI introduced a new 3D artificial intelligence foundation model designed to automate the creation of high-fidelity digital files from 3D scans, streamlining the production of replacement parts and reducing industrial downtime.

- In April 2025, Nano Dimension completed its acquisition of Desktop Metal, creating a global leader in digital manufacturing solutions by combining complementary technologies in systems, software, and materials for advanced additive manufacturing at scale.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Metal Material Based 3D Printing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24% |

| Market growth 2026-2030 | USD 3118.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 21.0% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The metal material based 3D printing market is undergoing a crucial maturation phase, shifting from prototyping to industrial-scale serial production. This transition influences boardroom decisions on capital expenditure and supply chain strategy, as organizations integrate technologies like powder bed fusion and directed energy deposition into their core operations.

- The adoption of metal injection molding principles within binder jetting processes is a key development. The demand for biocompatible implants and patient-specific medical devices drives innovation in materials and regulatory compliance. Similarly, the aerospace sector's focus on topology optimization and lightweighting for fuel efficiency propels the use of advanced systems.

- Achieving a certified manufacturing process is paramount, with some firms reporting a 25% reduction in qualification time by leveraging integrated software and hardware platforms. The market's evolution is further characterized by the development of custom metal alloys and a focus on creating functional end-use parts that meet stringent industry standards for performance and reliability.

What are the Key Data Covered in this Metal Material Based 3D Printing Market Research and Growth Report?

-

What is the expected growth of the Metal Material Based 3D Printing Market between 2026 and 2030?

-

USD 3.12 billion, at a CAGR of 24%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Iron-based, Titanium, Nickel, and Aluminum), End-user (Healthcare, Automotive, Aerospace and defense, Tool and mold making, and Others), Technology (PBF, DED, Binder jetting, and Metal extrusion) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerated industrialization within aerospace and defense supply chains, High initial capital expenditure and operational costs

-

-

Who are the major players in the Metal Material Based 3D Printing Market?

-

3D Systems Corp., AddUp, Carpenter Technology Corp., Colibrium Additive, Desktop Metal Inc., DMG MORI CO. LTD., EOS GmbH, Eplus 3D, GKN Sinter Metals Engineering GmbH, Hoganas AB, HP Inc., Markforged Holding Corp., OC Oerlikon Corp., Optomec Inc., Renishaw Plc, Sandvik AB, Sciaky Inc., TRUMPF SE Co. KG, Velo3D Inc. and Xjet Ltd.

-

Market Research Insights

- The metal material based 3D printing market is defined by a dynamic interplay of technological advancement and industrial application, where process optimization drives significant business outcomes. For instance, the use of topology optimization has enabled component lightweighting by over 40% in some aerospace applications, directly improving fuel efficiency.

- Simultaneously, the implementation of real-time melt pool monitoring has reduced part rejection rates by more than 25%, enhancing production yields. These efficiency gains are compelling, with some organizations reporting a return on investment within 24 months for high-volume production lines.

- The focus on developing a digital twin for each build allows for predictive analytics, further refining print parameters and ensuring consistent quality across global manufacturing sites. The expansion into new high-performance superalloys and advanced metal powders continues to broaden the technology's applicability in extreme environments.

We can help! Our analysts can customize this metal material based 3d printing market research report to meet your requirements.

RIA -

RIA -