Military Laser Systems Market Size 2026-2030

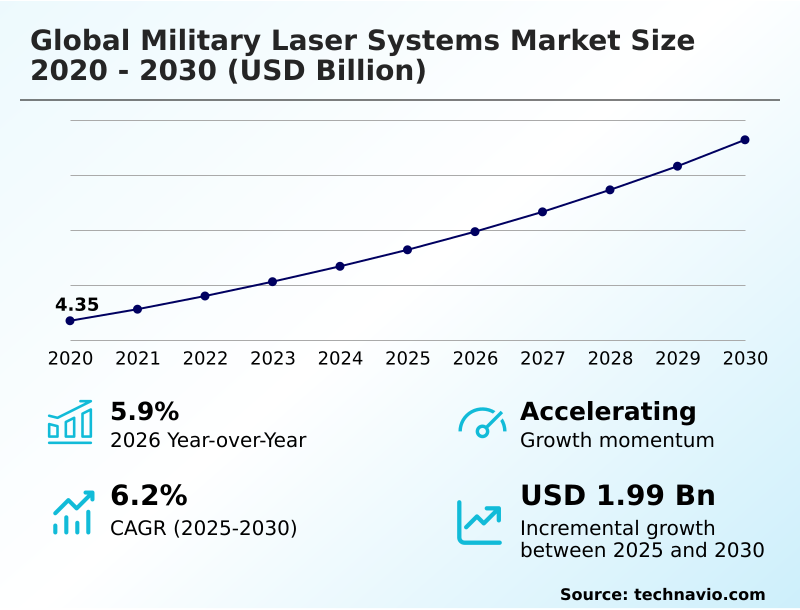

The military laser systems market size is valued to increase by USD 1.99 billion, at a CAGR of 6.2% from 2025 to 2030. Favorable cost-exchange ratio compared to kinetic interceptors will drive the military laser systems market.

Major Market Trends & Insights

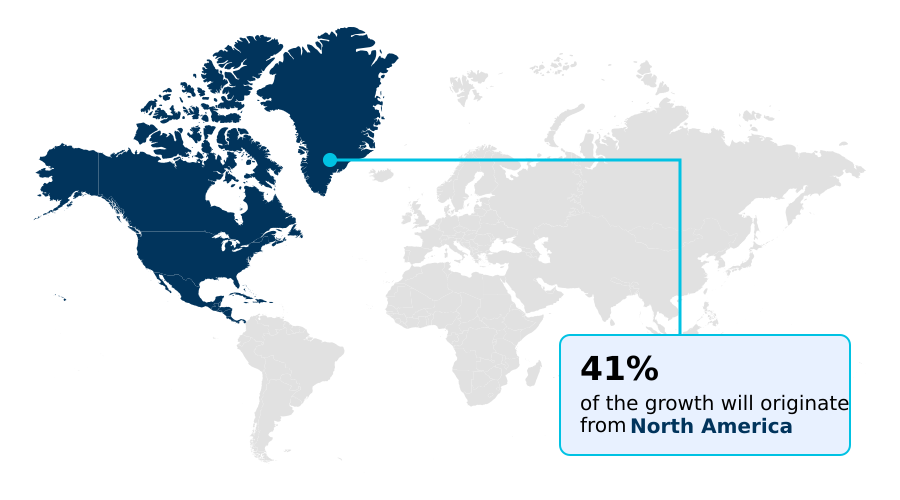

- North America dominated the market and accounted for a 41.3% growth during the forecast period.

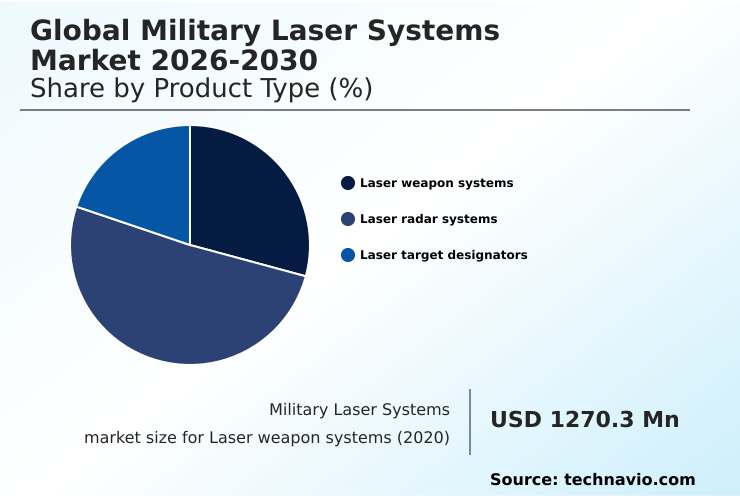

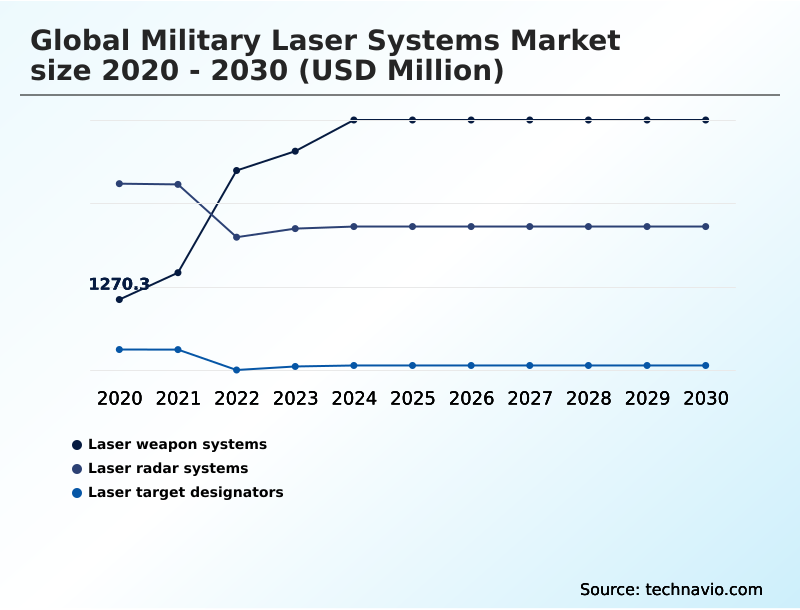

- By Product Type - Laser weapon systems segment was valued at USD 2.74 billion in 2024

- By Application - Non-weapons segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.29 billion

- Market Future Opportunities: USD 1.99 billion

- CAGR from 2025 to 2030 : 6.2%

Market Summary

- The Military Laser Systems Market is undergoing a strategic transformation, pivoting from traditional kinetic interceptors to directed energy solutions. This shift is motivated by the need to counter asymmetric threats, such as unmanned aerial systems and mortar projectiles, in a more financially sustainable manner. The core appeal lies in the low cost-per-shot and deep magazine capacity inherent to laser technology.

- Key advancements in solid-state and fiber lasers, coupled with innovations in beam combining and thermal management, are enabling the development of more compact, powerful, and ruggedized systems. Consequently, high-energy lasers are being integrated into a variety of platforms, including naval vessels, armored vehicles, and aircraft.

- However, operational deployment faces hurdles such as atmospheric interference and the immense power and cooling requirements for high-power systems. For instance, a defense contractor must now balance R&D investments between scaling laser power and perfecting AI-driven adaptive optics to ensure beam quality remains effective over tactical distances, directly impacting their long-term product viability and supply chain strategy.

What will be the Size of the Military Laser Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Military Laser Systems Market Segmented?

The military laser systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product type

- Laser weapon systems

- Laser radar systems

- Laser target designators

- Application

- Non-weapons

- Weapons

- Power output

- 10 kW TO 100 kW

- More than 100 kW

- 10 kW

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Israel

- Saudi Arabia

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Product Type Insights

The laser weapon systems segment is estimated to witness significant growth during the forecast period.

The laser weapon systems segment is shifting from demonstration units to operationally deployed systems. These hard-kill defensive systems utilize a high-energy laser to neutralize threats, offering a superior cost-exchange ratio compared to kinetic interceptors.

A primary driver is the ability to engage unmanned aerial systems and cruise missiles effectively. Technological advances in scalable laser architecture and laser power scaling allow for outputs exceeding 300 kilowatts, essential for hardened targets.

Defense agencies are integrating these systems onto diverse platforms, including naval laser weapon system and ground-based air defense vehicles. This operational pivot reduces engagement costs by over 95% in certain scenarios.

Key technologies include LIDAR systems and electro-optical/infrared sensors, which are crucial for the target acquisition system. Progress in this area is a focus of naval laser defense integration and airborne laser weapon development.

The Laser weapon systems segment was valued at USD 2.74 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Military Laser Systems Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Military Laser Systems Market is led by North America, which is projected to contribute over 41% of the market's incremental growth, driven by substantial US investment in short-range air defense programs using directed energy weapons.

Concurrently, APAC is experiencing rapid expansion due to geopolitical tensions, with nations focusing on indigenous research into airborne laser systems and laser radar.

Europe is advancing through collaborative programs focused on creating sovereign capabilities, with a strong emphasis on naval applications and laser jamming technologies.

The successful deployment of Israel's Iron Beam system has demonstrated an operational cost reduction of over 98% for certain interception scenarios, setting a new benchmark for cost-exchange ratio analysis. Such hybrid kinetic-laser defense models are influencing global procurement.

The market is also seeing advances in space-based laser technology and shipboard laser weapon integration.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

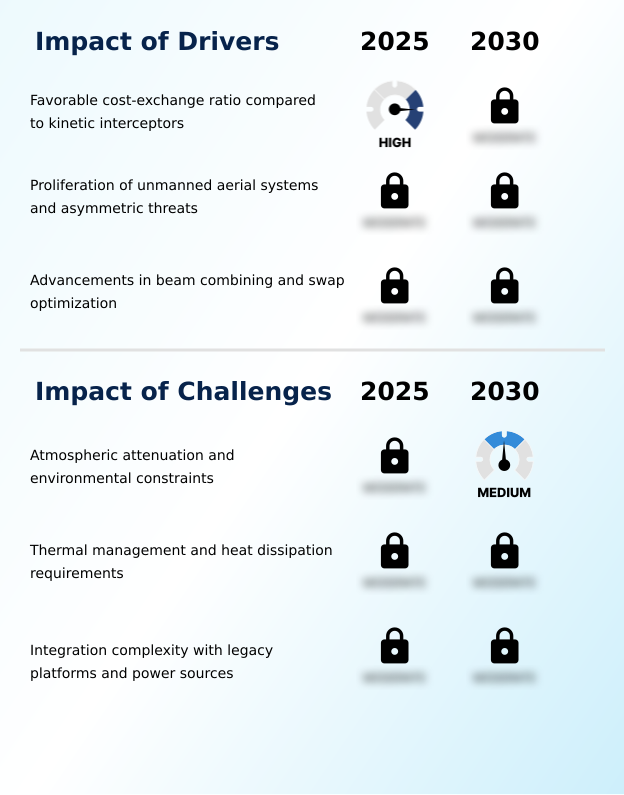

- The strategic calculus for adopting directed energy is increasingly shaped by a detailed analysis of the cost-exchange ratio of laser weapons compared to legacy munitions. This financial driver is compelling military planners to prioritize SWaP optimization for mobile laser systems, enabling deployment on a wider range of tactical platforms.

- However, the laser effectiveness in adverse weather conditions remains a significant technical hurdle, prompting a strategic move toward layered defense with kinetic and laser systems to ensure all-weather capability. A critical element in improving performance is the use of AI algorithms in advanced laser targeting, which compensates for atmospheric turbulence and enhances precision.

- Development efforts are also targeting high-energy laser for counter-hypersonic threats, pushing the boundaries of power and beam control. Addressing thermal management challenges in HEL systems is paramount, as inefficient cooling can severely limit operational endurance. To achieve higher outputs, engineers rely on spectral beam combining for power scaling, a complex but essential technique.

- The difficulty of integrating laser weapons on legacy platforms, which often lack sufficient power and cooling, remains a major logistical challenge. The focus on solid-state laser reliability in combat underscores the demand for robust, field-tested solutions.

- Meanwhile, applications for a non-lethal laser dazzler for crowd control and improving laser rangefinder accuracy for artillery continue to expand the technology's utility beyond hard-kill missions.

What are the key market drivers leading to the rise in the adoption of Military Laser Systems Industry?

- The market's growth is primarily driven by the favorable cost-exchange ratio that military laser systems offer when compared to traditional kinetic interceptors.

- The primary market driver remains the unparalleled cost-exchange ratio, as a directed energy weapon can neutralize low-cost aerial threats for less than 1% of the cost of a traditional missile interceptor. This economic advantage is fueling directed energy weapon proliferation.

- A second major driver is the need to counter asymmetric threats like drone swarms, which has accelerated investment in counter-UAS laser effectiveness. Technological maturity, particularly in size, weight, and power (SWaP) optimization, is a critical enabler.

- Recent efforts in developing compact laser weapon systems have reduced the physical footprint of mobile units by over 50%, enabling integration onto a wider array of tactical vehicles.

- This facilitates the deployment of mobile laser air defense platforms and supports future soldier laser systems with ruggedized military optronics.

What are the market trends shaping the Military Laser Systems Industry?

- A key trend influencing the market is the integration of artificial intelligence for advanced beam control and targeting. This development is reshaping the technological landscape of military laser systems.

- The market is experiencing a structural shift toward modular, open-system architectures, a trend that is projected to reduce system upgrade costs by up to 40% over a platform's lifecycle. This approach, driven by the need for a tactical laser that can be easily adapted, facilitates rapid technology insertion and simplifies logistics.

- Another key trend is the integration of AI, where AI-driven laser targeting has demonstrated the ability to decrease target engagement time by 30%. This is critical for countering drone swarms. The development of hybrid layered air defense network combining high-power microwave weapons with kinetic interceptors optimizes defense economics.

- Innovations in free-space optical communications and optical dazzler technologies are also expanding the utility of laser-based systems beyond destructive applications, with a focus on laser communication security.

What challenges does the Military Laser Systems Industry face during its growth?

- A significant challenge affecting the market is atmospheric attenuation, where environmental factors can degrade the performance and effective range of laser systems.

- A fundamental challenge is laser system atmospheric propagation, as environmental factors like fog and dust can reduce a laser's effective range by over 80%. This limitation necessitates maintaining redundant kinetic systems, complicating logistics. Another significant engineering hurdle is thermal management.

- Current solid-state lasers convert up to 60% of their input power into waste heat, requiring cooling systems that can double the total system volume and weight, a critical issue for laser weapon system SWaP. Integration with legacy platforms, which often lack the requisite electrical power generation and structural support, poses further difficulties.

- These technical constraints temper the pace of widespread adoption, especially for high-power laser for missile defense applications. The development of anti-satellite laser weapons faces similar physics-based constraints.

Exclusive Technavio Analysis on Customer Landscape

The military laser systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the military laser systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Military Laser Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, military laser systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BAE Systems Plc - Offerings include integrated laser-guided rockets and advanced 3D LIDAR mapping solutions, alongside the development of high-energy laser effectors for modern military applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BAE Systems Plc

- Coherent Corp.

- Elbit Systems Ltd.

- General Atomics

- Israel Aerospace Ltd.

- Kratos Defense and Security Inc.

- L3Harris Technologies Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- MBDA

- MKS Instruments Inc.

- Newport Corp.

- Northrop Grumman Corp.

- QinetiQ Ltd.

- Rafael Advanced Defense Ltd.

- Rheinmetall AG

- RTX Corp.

- Saab AB

- Safran SA

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Military laser systems market

- In August 2025, RTX Corp. announced the delivery of an enhanced 50-kilowatt class High Energy Laser Weapon System to the US Army, featuring upgraded beam control software to decrease the time required to defeat maneuvering drone threats.

- In January 2025, Lockheed Martin Corp. confirmed the delivery of another battery of 300-kilowatt class laser weapon systems to the United States Army, significantly expanding the operational footprint of the IFPC-HEL program.

- In March 2025, Northrop Grumman Corp. reported the successful fielding of an upgraded lightweight laser target designator module, which provides extended battery life and improved beam stability for dismounted infantry units.

- In April 2025, Rheinmetall AG announced the successful integration and live-fire testing of a new high-energy laser effector on its Skyranger 30 mobile air defense vehicle, proving its capability to neutralize multiple drone threats in rapid succession.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Military Laser Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.2% |

| Market growth 2026-2030 | USD 1994.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.9% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Israel, Saudi Arabia, UAE, Turkey, South Africa, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Military Laser Systems Market is defined by a rapid transition toward advanced directed energy weapon platforms. The underlying technology has evolved from chemical lasers to more efficient and compact fiber laser technology and solid-state laser designs. Central to their effectiveness are sophisticated beam control systems and adaptive optics, which mitigate atmospheric distortion and thermal blooming compensation.

- As systems scale in power, thermal management solutions become critical. Innovations like spectral beam combining enable laser power scaling to hundreds of kilowatts, making high-energy laser effectors viable for short-range air defense and counter-rocket, artillery, and mortar roles. The integration of directed infrared countermeasures has improved aircraft survivability against heat-seeking missiles by over 75%.

- This trend toward intelligent systems is forcing boardroom-level decisions on R&D budgets, shifting focus from raw power to AI-driven targeting, which uses pulse repetition frequency coding for precision. This impacts everything from the development of a laser guidance kit to a full naval laser weapon system or airborne laser systems.

What are the Key Data Covered in this Military Laser Systems Market Research and Growth Report?

-

What is the expected growth of the Military Laser Systems Market between 2026 and 2030?

-

USD 1.99 billion, at a CAGR of 6.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Laser weapon systems, Laser radar systems, and Laser target designators), Application (Non-weapons, and Weapons), Power Output (10 kW TO 100 kW, More than 100 kW, and 10 kW) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Favorable cost-exchange ratio compared to kinetic interceptors, Atmospheric attenuation and environmental constraints

-

-

Who are the major players in the Military Laser Systems Market?

-

BAE Systems Plc, Coherent Corp., Elbit Systems Ltd., General Atomics, Israel Aerospace Ltd., Kratos Defense and Security Inc., L3Harris Technologies Inc., Leonardo S.p.A., Lockheed Martin Corp., MBDA, MKS Instruments Inc., Newport Corp., Northrop Grumman Corp., QinetiQ Ltd., Rafael Advanced Defense Ltd., Rheinmetall AG, RTX Corp., Saab AB, Safran SA, Thales Group and The Boeing Co.

-

Market Research Insights

- The strategic dynamics of the Military Laser Systems Market are shaped by the proliferation of directed energy weapons and the pursuit of cost-effective defense. The adoption of counter-UAS laser effectiveness has shown a 90% reduction in engagement costs against certain threats, compelling investment in mobile laser air defense platforms.

- Furthermore, integrating AI-driven laser targeting has improved tracking accuracy against maneuvering targets by up to 40%, a crucial factor in complex combat scenarios. This move toward ruggedized military optronics and tactical high-energy laser applications is central to modern force structures.

- Development is also focused on non-lethal laser deterrents and ensuring laser communication security, which are vital for future soldier laser systems and maintaining information superiority on the battlefield.

We can help! Our analysts can customize this military laser systems market research report to meet your requirements.

RIA -

RIA -