Mini Data Center Market Size 2024-2028

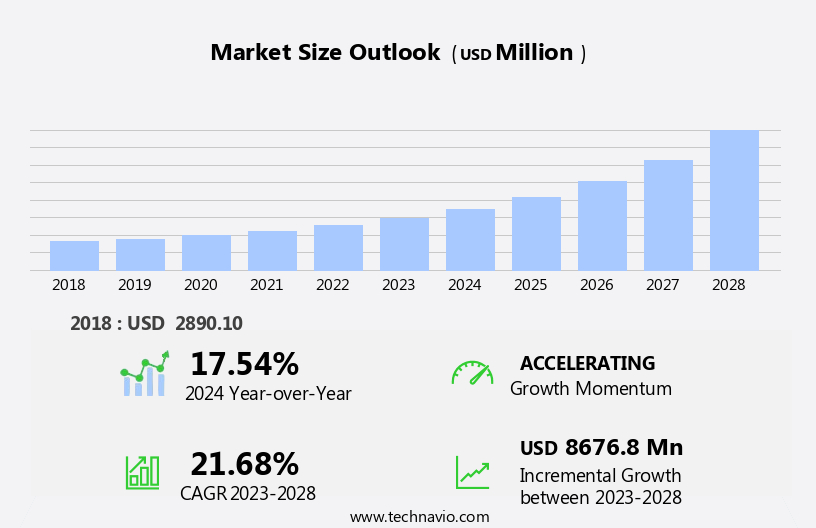

The mini data center market size is forecast to increase by USD 8.68 billion, at a CAGR of 21.68% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing demand from Small and Medium Enterprises (SMEs) for reliable and efficient data storage solutions. This trend is further fueled by the growing need for edge computing, which requires data processing to occur closer to the source, reducing latency and enhancing responsiveness. However, the market faces a notable challenge: the lack of awareness and understanding among businesses regarding the benefits and implementation of mini data centers. This obstacle presents an opportunity for market participants to educate potential clients and demonstrate the value proposition of mini data centers in addressing their specific data management needs.

- Companies that successfully navigate this challenge and effectively communicate the advantages of mini data centers will be well-positioned to capitalize on the market's potential for growth.

What will be the Size of the Mini Data Center Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the ever-increasing demand for reliable and efficient IT infrastructure. Businesses across various sectors are adopting modular data centers to address their unique requirements, from server consolidation and disaster recovery to network optimization and capacity planning. These data centers incorporate advanced technologies such as redundant power supplies, precision cooling, and remote monitoring, seamlessly integrated into their design. Mini data centers come in various forms, including micro data centers and edge data centers, catering to the diverse needs of organizations. Their modular design allows for easy deployment, scalability, and flexibility, making them an attractive option for businesses seeking to minimize their carbon footprint and optimize operational efficiency.

Data center construction and lifecycle management are crucial aspects of mini data center operations. From site selection and network infrastructure to HVAC systems and energy efficiency, every detail is meticulously planned and executed to ensure high availability and reliability. As the market continues to unfold, we see the integration of innovative technologies such as network virtualization, liquid cooling, and data center relocation services. These advancements enable businesses to optimize their IT infrastructure, reduce energy consumption, and enhance their overall IT infrastructure's performance and security. Maintenance services and support contracts are essential components of mini data center management, ensuring the seamless operation of these complex systems.

Capacity planning and space optimization are also critical considerations, as businesses look to maximize their investment in IT infrastructure while minimizing costs and ensuring business continuity. The market's continuous dynamism is reflected in its ongoing evolution, with new technologies and applications emerging regularly. From rackmount servers and blade servers to fiber optic cables and ethernet switches, the market's diverse offerings cater to the ever-changing needs of businesses in various sectors. In conclusion, the market's ongoing evolution is driven by the need for reliable, efficient, and flexible IT infrastructure. From server consolidation and disaster recovery to network optimization and capacity planning, mini data centers offer businesses a range of solutions to meet their unique requirements.

With a focus on energy efficiency, operational efficiency, and carbon footprint reduction, these data centers are an essential component of modern IT infrastructure.

How is this Mini Data Center Industry segmented?

The mini data center industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

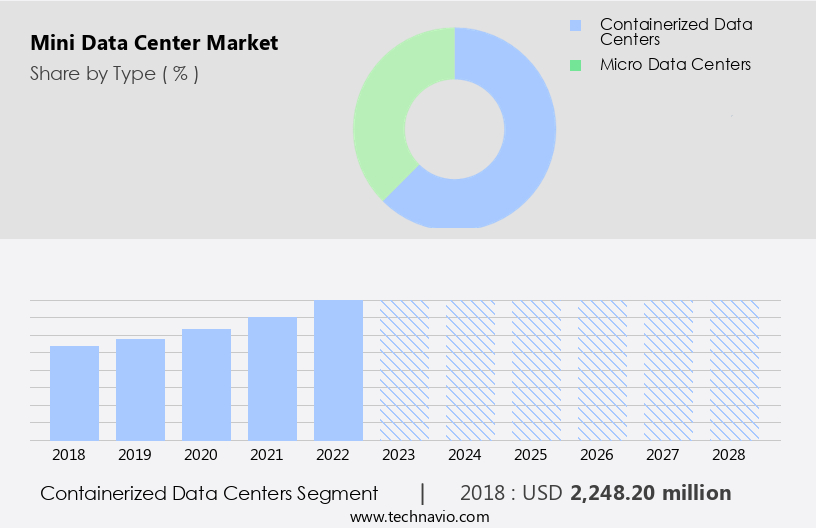

- Containerized data centers

- Micro data centers

- Business Segment

- SMEs

- Large enterprises

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Type Insights

The containerized data centers segment is estimated to witness significant growth during the forecast period.

Containerized modular data centers are gaining prominence in the business landscape, serving as crucial infrastructure for edge computing and disaster recovery applications. As companies strive for operational efficiency and expansion, the demand for reliable data centers with robust storage and processing capacities is escalating. With the increasing number of digital devices generating vast amounts of data, such as the rise from 7.13 billion mobile cellular subscriptions in 2015 to 8.36 billion in 2022, the need for advanced data center solutions becomes even more pressing. Data center migration and consolidation are essential strategies for businesses seeking to optimize their IT infrastructure and reduce energy consumption.

High-availability clusters and redundant power supplies ensure business continuity, while precision cooling, network virtualization, and server consolidation contribute to operational efficiency. Additionally, the adoption of green data centers and energy-efficient cooling systems, such as free air cooling and liquid cooling, minimizes the carbon footprint. Data center design, including modular and remote monitoring, plays a significant role in ensuring optimal network infrastructure and space utilization. Maintenance services, capacity planning, and disaster recovery plans further enhance the reliability and longevity of these critical systems. Furthermore, the integration of HVAC systems, ethernet switches, fiber optic cables, and deployment services streamlines the data center construction process.

Micro data centers and edge data centers cater to the growing demand for distributed computing, offering reduced latency and improved response times. Lifecycle management and it asset management are essential aspects of maintaining these data centers, ensuring the longevity and optimal performance of the IT infrastructure. In conclusion, the data center market is evolving to accommodate the increasing demand for reliable, efficient, and scalable IT infrastructure. Companies are investing in advanced technologies, such as containerized modular data centers, to meet the needs of their businesses and support the growing digital economy.

The Containerized data centers segment was valued at USD 2.25 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

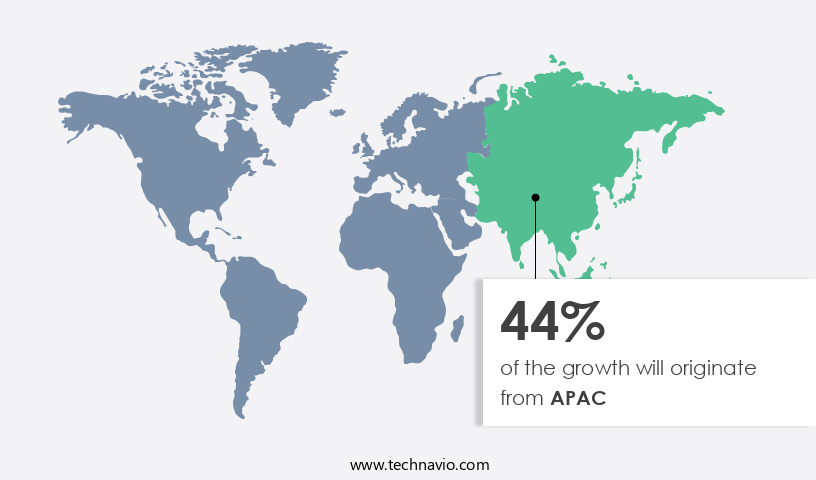

APAC is estimated to contribute 44% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The US market for mini data centers is experiencing significant growth, driven by the increasing adoption of these facilities in various industry verticals. Originally popularized by government agencies, mini data centers are now being utilized by healthcare, education, and the BFSI sector. These compact, modular data center solutions offer advantages such as energy efficiency, physical security, and remote monitoring. Business continuity is a key consideration, leading to the integration of disaster recovery and redundant power supplies. Data center migration and consolidation are ongoing trends, with mini data centers providing an optimal solution for space optimization and network infrastructure.

HVAC systems, cooling technologies like water and liquid cooling, and precision cooling are essential components of these facilities. Ethernet switches, fiber optic cables, and deployment services are integral to their network optimization. Mini data centers are also being integrated with cloud computing and edge data centers for improved operational efficiency. Lifecycle management, server consolidation, and network virtualization are crucial aspects of their design and maintenance. Cooling systems, such as free air cooling and energy-efficient cooling, are essential for minimizing energy consumption and reducing the carbon footprint. Mini data centers are increasingly being adopted for their environmental monitoring capabilities and IT asset management.

Security systems, including fire suppression, are integrated to ensure business continuity and protect IT infrastructure. Support contracts and maintenance services are essential for ensuring the ongoing operational efficiency of these facilities. Blade servers and rackmount servers are commonly used to maximize space and power efficiency.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Mini Data Center Industry?

- The significant increase in demand from small and medium-sized enterprises (SMEs) serves as the primary driver for market growth.

- Mini data centers have gained significant traction among enterprises as an affordable and flexible alternative to traditional data center facilities. With the increasing demand for business continuity and high-availability clusters, the market for mini data centers has witnessed notable growth. These compact data centers, which can house rackmount servers, offer energy efficiency, physical security, and network optimization. Technological advancements have expanded the capabilities of mini data centers from single racks to modular systems consisting of multiple racks, suitable for installation in existing offices and commercial spaces. Mini data centers are particularly beneficial for small and medium-sized enterprises (SMEs) that cannot afford the substantial investments required for constructing a traditional data center.

- The cost of establishing a traditional data center can reach up to USD6 million for a 1MW facility. In contrast, mini data centers offer cost savings, scalability, and ease of deployment. Additionally, mini data centers facilitate data center migration and consolidation, making them an attractive option for businesses seeking to optimize their IT infrastructure. Lifecycle management of these data centers is also simplified due to their compact size and standardized components.

What are the market trends shaping the Mini Data Center Industry?

- The growing requirement for edge computing represents a significant market trend in the technology industry. This shift towards decentralized processing and data analysis at the edge of networks is becoming increasingly necessary for efficient and timely data processing.

- The edge data center market is experiencing significant growth due to the increasing number of Internet-of-Things (IoT) devices, which generate vast amounts of data that need to be processed in real-time. This architectural model processes data at the edge of the network, typically near the source, reducing latency and bandwidth requirements. The concept of edge computing was popularized by the use of RFID sensors in logistics and warehouses in the late 1990s. The growing popularity of connected cars, homes, health, and cities further accelerates the demand for edge data centers. To effectively manage this data, advanced technologies such as HVAC systems, ethernet switches, storage optimization, network virtualization, water cooling, and fiber optic cables are being adopted.

- Deployment services and data center relocation are also crucial to ensure seamless integration and minimal downtime. Fire suppression systems and liquid cooling are essential safety measures in data center design. Site selection plays a vital role in ensuring optimal performance and energy efficiency. Companies are investing in research and development to improve these technologies and make them more cost-effective. Overall, the edge data center market is expected to continue growing as the world becomes increasingly connected.

What challenges does the Mini Data Center Industry face during its growth?

- The absence of awareness is a significant obstacle impeding industry expansion.

- Mini data centers, also known as micro data centers, have gained traction in the market as an alternative to traditional data center facilities. Introduced by pure-play companies a few years ago, these data centers offer organizations an efficient and cost-effective solution for their in-house computing requirements. Despite their benefits, awareness and adoption remain low among some organizations, particularly in developing countries. Mini data centers are designed with modularity in mind, enabling space optimization and energy efficiency. They can be used to build entire data centers or supplement existing ones. These facilities are suitable for organizations with budget constraints and can be particularly beneficial for industries like banking, retail, and manufacturing that utilize IoT.

- These data centers offer several advantages, including server consolidation, disaster recovery, and redundant power supplies. Remote monitoring capabilities allow for efficient maintenance services and capacity planning. Precision cooling systems ensure optimal temperature control, while network infrastructure is designed for high availability and reliability. Additionally, some mini data centers employ free air cooling, further reducing energy consumption. Mini data centers offer organizations a cost-effective and efficient solution for their IT infrastructure needs. Their modular design allows for easy expansion and customization, making them an attractive option for businesses looking to streamline their operations and reduce costs.

Exclusive Customer Landscape

The mini data center market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the mini data center market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, mini data center market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

CANCOM SE - The company specializes in mini data center solutions, including the innovative All-in-One Container Data Center (AIO BOX).

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- CANCOM SE

- Cannon Technologies Ltd.

- Canovate Group

- Dataracks

- Dell Technologies Inc.

- Eaton Corp. Plc

- Gardner DC Solutions Ltd

- Hanley Energy Ltd.

- Hewlett Packard Enterprise Co.

- Huawei Technologies Co. Ltd.

- International Business Machines Corp.

- Inspur Group

- Legrand

- Minkels B.V.

- Panduit Corp.

- Rahi

- Rittal GmbH and Co. KG

- ScaleMatrix Holdings Inc.

- Schneider Electric SE

- Vertiv Holdings Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Mini Data Center Market

- In January 2024, Schneider Electric, a global energy management and automation company, announced the launch of its new prefabricated micro data center solution, 'MicroDataCenter 100,' designed for edge computing applications. This product expansion aims to cater to the growing demand for smaller, more distributed data centers (Schneider Electric Press Release).

- In March 2024, Vertiv, a global provider of critical infrastructure solutions for data centers, entered into a strategic partnership with Microsoft to offer integrated IT and power solutions for Microsoft Azure data centers. This collaboration will help Vertiv expand its market reach and strengthen its position in the data center industry (Vertiv Press Release).

- In May 2024, NTT Ltd., a global digital infrastructure and IT services provider, acquired the data center business of e-Shelter, a leading data center operator in Europe. This acquisition will enable NTT to expand its European data center footprint and enhance its capabilities in the colocation market (NTT Ltd. Press Release).

- In April 2025, IBM and Google Cloud announced a significant collaboration to offer joint solutions for hybrid multicloud environments. This partnership includes the integration of IBM's Power Systems and Google Cloud's Anthos, allowing customers to run workloads seamlessly across both on-premises and cloud environments (IBM Press Release).

Research Analyst Overview

- The market encompasses various solutions, including colocation facilities, hyperscale data centers, and containerized data centers, among others. Thermal management and capacity management are crucial aspects of this market, ensuring optimal performance and energy efficiency. Load balancing and AI integration are trending technologies, enabling improved resource utilization and enhanced user experience. Vulnerability assessments and security audits are essential for safeguarding data privacy and ensuring compliance with regulatory requirements. HPC, deep learning, and machine learning applications demand high-performance computing and robust fault tolerance. 5G networks and IoT integration are transforming data processing, necessitating edge computing and serverless computing for real-time data analysis.

- Cloud connectivity, data analytics, and performance monitoring are integral components of modern data management strategies. AI and ML are increasingly integrated into data centers for predictive maintenance, risk management, and dynamic voltage scaling. Data security and penetration testing are paramount for mitigating cyber threats and ensuring business continuity. Capacity management and failover mechanisms are essential for ensuring uninterrupted operations and minimizing downtime. AI and ML are also utilized for predictive maintenance, enhancing overall efficiency and reliability. In the realm of high-tech applications, such as HPC, deep learning, and big data analytics, data centers must provide advanced security features and robust performance.

- Thermal management, load balancing, and capacity management are crucial for maintaining optimal conditions and ensuring seamless operations. AI and ML are revolutionizing data center management, enabling predictive maintenance, real-time performance monitoring, and advanced risk management. Thermal management, capacity management, and security audits remain essential for maintaining optimal conditions and ensuring data privacy and compliance. The integration of AI, ML, and IoT is transforming data centers, necessitating advanced thermal management, capacity management, and security measures. Hyperscale data centers and edge computing are key trends, with containerized data centers and serverless computing gaining popularity for their flexibility and scalability.

- Capacity management, thermal management, and security audits are essential components of data center operations, ensuring optimal performance, energy efficiency, and data privacy. AI and ML are transforming data center management, enabling predictive maintenance, real-time performance monitoring, and advanced risk management. The market is characterized by advanced technologies, including AI, ML, and IoT integration, hyperscale data centers, and edge computing. Thermal management, capacity management, and security audits remain essential for maintaining optimal conditions and ensuring data privacy and compliance. In the ever-evolving data center landscape, thermal management, capacity management, and security audits are essential for maintaining optimal conditions and ensuring data privacy and compliance.

- AI and ML are transforming data center management, enabling predictive maintenance, real-time performance monitoring, and advanced risk management. The market is witnessing a shift towards advanced technologies, such as AI, ML, and IoT integration, hyperscale data centers, and edge computing. Thermal management, capacity management, and security audits remain crucial for maintaining optimal conditions and ensuring data privacy and compliance. In the dynamic world of data centers, thermal management, capacity management, and security audits are essential for maintaining optimal conditions and ensuring data privacy and compliance. AI and ML are transforming data center management, enabling predictive maintenance, real-time performance monitoring, and advanced risk management.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Mini Data Center Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 21.68% |

|

Market growth 2024-2028 |

USD 8676.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

17.54 |

|

Key countries |

US, China, Japan, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Mini Data Center Market Research and Growth Report?

- CAGR of the Mini Data Center industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the mini data center market growth of industry companies

We can help! Our analysts can customize this mini data center market research report to meet your requirements.

RIA -

RIA -