North America Directional Drilling Market Size 2024-2028

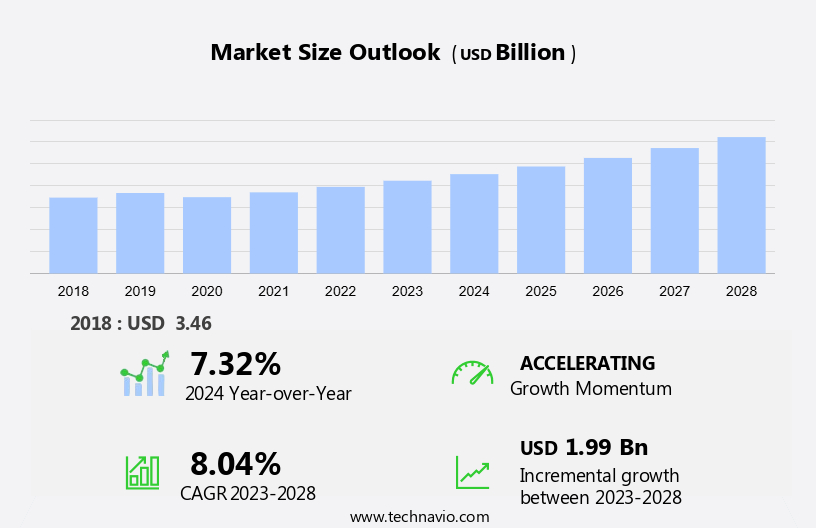

The North America directional drilling market size is forecast to increase by USD 1.99 billion at a CAGR of 8.04% between 2023 and 2028.

- In North America, the directional drilling market is experiencing significant growth due to increased investments in the upstream oil and gas sector. The emergence of automation in directional drilling is a major trend, leading to increased efficiency and accuracy in drilling operations. Additionally, the adoption of alternative energy sources is driving the market, as directional drilling is used to access hard-to-reach reserves of natural gas and oil. Construction equipment, such as drilling rigs, is being upgraded to accommodate maximum length and diameter specifications to tackle challenging soil conditions. Crypto-asset exchanges and trading fees have not significantly impacted the market at this time.

What will be the size of the market during the forecast period?

- The market is witnessing significant advancements driven by the increasing demand for hydrocarbon extraction and the adoption of modern techniques in drilling operations. This market caters to the exploration and production sectors of the oil and gas industry, focusing on minimizing surface disturbance and enhancing drilling efficiency. Environmental regulations are a crucial factor influencing the market. Stringent regulations aimed at reducing the environmental impact of drilling operations have led to the widespread adoption of directional drilling techniques. By drilling horizontally or at non-vertical angles, companies can minimize the number of wells required, thereby reducing the overall surface disturbance.

- The market is characterized by the use of advanced technologies such as hydraulic jets and drill bits. These technologies enable efficient and reliable drilling in various formations, including shale, sandstone, and coal seams. The market is also witnessing the integration of real-time adjustment systems, which allow drill operators to optimize drilling parameters based on real-time data from GPS signals. The oil and gas industry's reliance on directional drilling is increasing due to the potential for exploring geothermal energy and renewable energy production. In the case of geothermal energy exploration, directional drilling enables the tapping of deep reservoirs that were previously inaccessible.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Onshore

- Offshore

- Technique

- Rotary steerable system

- Conventional methods

- Geography

- North America

- Canada

- Mexico

- US

- North America

By Application Insights

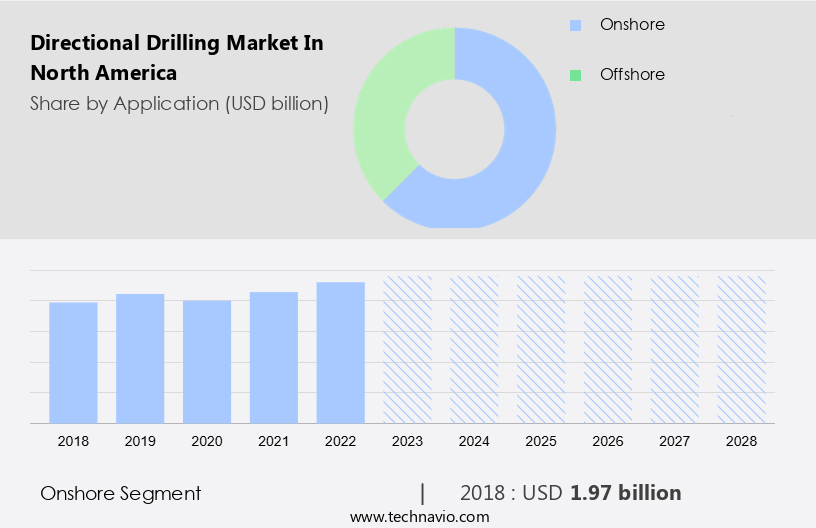

- The onshore segment is estimated to witness significant growth during the forecast period.

The market is experiencing notable expansion, with onshore drilling projects being a key driver. On-land drilling involves the drilling of wells on property or land. This technique's affordability and accessibility make it an allure for oil and gas firms. The United States is a significant contributor to the growth of the North American onshore directional drilling market. The shale revolution has instigated an increase in onshore drilling activities, primarily in regions like the Permian Basin and the Bakken Formation. Major corporations have made substantial investments in onshore drilling projects to capitalize on the extensive shale reserves in these areas.

Furthermore, the cost-effective nature of onshore drilling, coupled with the abundance of resources, makes it a strategic choice for energy production in North America. The market's growth is influenced by the price trends of renewable energy, crude oil, and natural gas, as well as the exploitation of marine resources.

Get a glance at the market share of various segments Request Free Sample

The onshore segment was valued at USD 1.97 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the North American directional Drilling Market?

Rising investments in the upstream oil and gas sector is the key driver of the market.

- In response to the growing energy demands and the depletion of conventional oil and gas resources, there is a heightened focus on extracting reserves from underground reservoirs in North America. This approach is essential for securing energy supplies and increasing revenue for oil and gas operators. The drilling industry is evolving to meet these needs through the adoption of directional drilling technology. Directional drilling is a technique that enables the drilling of boreholes at precise angles, enabling access to previously inaccessible reservoirs. This method reduces the need for multiple well sites and minimizes the impact on groundwater and ecosystems.

- It also enhances site safety by reducing the risk of gas ruptures and operational complications. The North American directional drilling market is witnessing significant growth due to the increasing investment in upstream oil and gas projects. In 2021, global upstream oil and gas investment increased by 9-10%, with three new drilling rigs added. This trend is expected to continue as companies prioritize the optimization of existing oilfields and the exploration of new resources. As the industry advances, it is crucial to prioritize environmental concerns and ensure the protection of groundwater and ecosystems. The use of directional drilling technology contributes to these efforts by reducing the number of well sites and minimizing the impact on the environment.

What are the market trends shaping the North America Directional Drilling Market?

The emergence of automation in directional drilling is the upcoming trend in the market.

- In the oil and gas sector, directional drilling is transforming automation. Advanced technologies are increasingly being adopted by drilling companies to enhance efficiency, precision, and safety. One significant aspect of this automation is the implementation of robotic drilling systems. These systems incorporate sensors, cameras, and artificial intelligence algorithms, enabling them to make real-time adjustments during drilling processes.

- For instance, Precision Drilling Corporation's RigSense system can identify downhole conditions and modify drilling parameters accordingly, eliminating the need for manual intervention. This results in quicker and more precise drilling. Automation in directional drilling is a game-changer in the industry, streamlining operations and improving overall productivity.

What challenges does the North American directional Drilling Market face during its growth?

Adoption of alternative energy sources is a key challenge affecting the market growth.

- In North America, the directional drilling market is experiencing significant growth due to various factors. The increasing demand for energy and the implementation of clean energy initiatives are key drivers. Renewable energy sources, such as solar, wind, and hydropower, are becoming increasingly popular due to their clean and inexhaustible nature. Governments are taking steps to reduce greenhouse gas emissions by shifting focus from conventional fuels to renewables. The use of drilling rigs and construction equipment in the energy sector is essential for extracting resources. However, the soil conditions in North America can be challenging, requiring specialized drilling techniques. Directional drilling is a cost-effective solution for drilling in complex geological formations.

- Moreover, the rise of crypto-asset exchanges and the associated trading fees have led to an increased focus on reducing operational costs in the energy sector. Directional drilling offers cost savings by minimizing the number of drilling sites required to extract resources. In conclusion, the market is expected to continue growing due to the increasing energy demand, the shift towards renewable energy sources, and the need to reduce operational costs. The use of drilling rigs and construction equipment in this sector will remain crucial for extracting resources efficiently, especially in challenging soil conditions.

Exclusive North America Directional Drilling Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- APA Corp.

- Baker Hughes Co.

- Cathedral Energy Services

- Chevron Corp.

- Direct Horizontal Drilling

- Granite Construction Inc.

- Halliburton Co.

- Intrepid

- Laney Drilling

- LEAM Drilling Services

- Nabors Industries Ltd.

- NOV Inc.

- RPB Industries Group

- Scientific Drilling International

- Stryker Directional

- Terra Contracting

- Texas Directional Boring

- Texas Roc Contracting

- Vermeer Corp.

- Weatherford International Plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth due to the increasing demand for hydrocarbons, particularly oil and natural gas. This modern drilling technique allows for the efficient and cost-effective extraction of resources from oil fields and underground reservoirs, with minimal surface disturbance. The horizontal digging method, which is a popular directional drilling technique, enables drilling operations to reach oil and gas deposits located in complex formations and hard-to-reach areas. Environmental regulations are a crucial factor influencing the market. The use of modern techniques, such as real-time adjustment through GPS signals, ensures the protection of marine resources and ecosystems during offshore drilling.

Furthermore, the industry is also focusing on the exploration of geothermal energy and renewable energy production to reduce reliance on hydrocarbons. Drill operators rely on advanced drill bits and hydraulic jets to drill through various soil conditions and rock formations, ensuring maximum efficiency and reliability. Crude oil prices and natural gas prices significantly impact heating costs, electricity generation, and the construction of underground works, including vertical wells and utility pipelines. The market is also witnessing the adoption of non-vertical angle drilling, which reduces the risk of groundwater pollution and site safety concerns. The cost-effective nature of directional drilling, coupled with the ability to operate wells in various locations, makes it a preferred choice for oil and gas companies and utility pipeline construction.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

136 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.04% |

|

Market Growth 2024-2028 |

USD 1.99 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.32 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -