North America Vegetable Oil Market Size 2024-2028

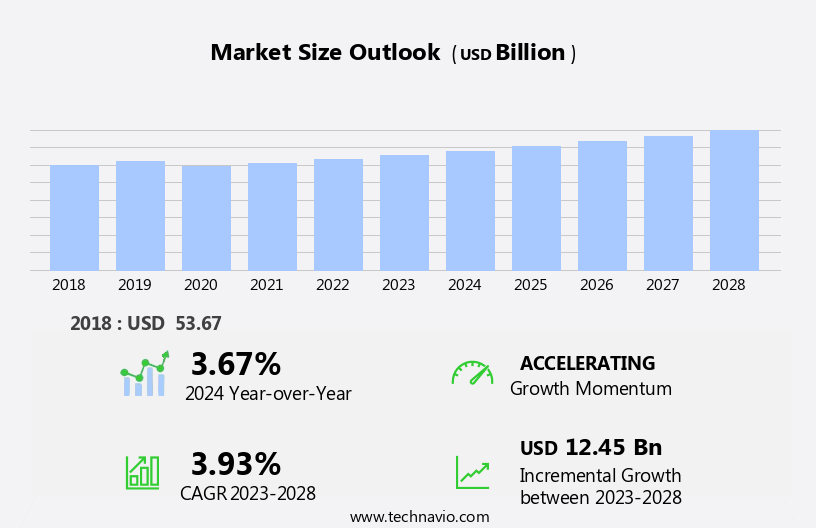

The north america vegetable oil market size is forecast to increase by USD 12.45 billion at a CAGR of 3.93% between 2023 and 2028.

What will be the size of the North America Vegetable Oil Market during the forecast period?

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Distribution Channel

- Offline

- Online

- Type

- Palm oil

- Soybean oil

- Canola oil

- Sunflower oil

- Others

- Geography

- North America

- Canada

- Mexico

- US

- North America

By Distribution Channel Insights

- The offline segment is estimated to witness significant growth during the forecast period.

In the North American vegetable oils market, traditional retail channels dominate distribution. Supermarkets and hypermarkets serve as primary outlets, providing a wide selection of vegetable oils and sizes. Convenience is a key factor, as consumers value the variety and accessibility these retailers offer. Convenience stores also play a significant role, particularly in urban and suburban areas, catering to the quick needs of consumers. Traditional grocery stores remain prominent, maintaining their status as go-to destinations for vegetable oils within local communities. Wholesale clubs cater to both household consumers and businesses, offering bulk purchasing options for vegetable oils. Vegetable oils, derived from plant sources such as soybean, corn, sunflower, canola, and others, serve various purposes.

They are used for cooking and baking, as heat transfer mediums, flavor enhancers, and moisture agents. In addition, they are used In the production of soaps, skincare products, biodiesel, and essential fatty acids. Vegetable oils are also rich in unsaturated fats, particularly monounsaturated and omega-3 fatty acids, making them heart-healthy options. The health consciousness trend and increasing household incomes contribute to the growing demand for vegetable oils. Key players In the market include soybean oil, corn oil, sunflower oil, canola oil, and others. Vegetable oils are also used In the pharmaceutical, cosmetics, animal feed, and retail/household industries. E-commerce platforms are emerging as a distribution channel, offering convenience and competitive pricing.

The nutritional value and health benefits of vegetable oils make them an essential component of food production.

Get a glance at the market share of various segments Request Free Sample

The Offline segment was valued at USD 40.58 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of North America Vegetable Oil Market?

Increasing use of vegetable oils in non-food applications is the key driver of the market.

What are the market trends shaping the North America Vegetable Oil Market?

Demand for clean-label vegetable oil products is the upcoming trend In the market.

What challenges does North America Vegetable Oil Market face during the growth?

Increasing threats from other cooking oils and fats is a key challenge affecting the market growth.

Exclusive North America Vegetable Oil Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Archer Daniels Midland Co.

- Azelis SA

- Bulk Apothecary

- Bunge Ltd.

- Cargill Inc.

- CHS Inc.

- ELIXENS GROUP

- Fuji Oil Co. Ltd.

- Jedwards International Inc.

- Louis Dreyfus Co. BV

- Olam Group Ltd.

- Ravago Chemicals

- The Clorox Co.

- Unilever PLC

- Wilmar International Ltd.

- Cheryls Herbs

- Hybco USA

- The Procter and Gamble Co.

- Welch Holme and Clark Co. Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Vegetable oils have long been a staple in North American food production and consumption, serving various purposes beyond culinary applications. These plant-derived triglycerides offer a wide range of benefits, making them essential in various industries, including food, pharmaceuticals, cosmetics, animal feed, and even as biofuels. The vegetable oils market in North America is driven by several factors, including the health benefits associated with unsaturated fats and the increasing health consciousness of consumers. Vegetable oils, rich in monounsaturated and polyunsaturated fats, are considered heart-healthy alternatives to saturated fats. As a result, their demand continues to rise, particularly In the retail/household sector.

Vegetable oils, derived from plant sources such as soybean, corn, sunflower, canola, olive, avocado, and others, offer unique characteristics that cater to diverse applications. For instance, sunflower oil is known for its high smoke point, making it suitable for deep-frying and heat transfer medium applications. Canola oil, on the other hand, is popular for its neutral taste and high stability, making it an excellent choice for baking and salad dressings. Beyond their culinary uses, vegetable oils find applications in various industries. In the pharmaceutical sector, they are used as emulsifiers and stabilizers in drug formulations. In cosmetics, they are used in soaps, skincare products, and as a base for various lotions and creams.

In the animal feed industry, vegetable oils are used as a source of energy and essential fatty acids. The vegetable oils market in North America is also influenced by the growing demand for biodiesel as an alternative fuel source. Vegetable oils, particularly palm oil, soybean oil, and corn oil, are used to produce biodiesel, which is a renewable, cleaner-burning fuel that reduces greenhouse gas emissions. The increasing health consciousness of consumers and the rising prevalence of micronutrient deficiencies have led to the fortification of vegetable oils with essential nutrients such as Vitamin D. Cooking oil fortification and food fortification are becoming increasingly common practices In the food industry to address these deficiencies and improve overall health.

The vegetable oils market in North America is expected to continue growing, driven by the increasing demand for heart-healthy oils, the growing popularity of plant-based diets, and the expanding applications of vegetable oils in various industries. However, factors such as price volatility, supply chain disruptions, and regulatory challenges may pose challenges to market growth. In conclusion, the vegetable oils market in North America is a dynamic and diverse market, driven by various factors, including health benefits, increasing health consciousness, and expanding applications in various industries. The market is expected to continue growing, offering opportunities for businesses and investors alike.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

145 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.93% |

|

Market growth 2024-2028 |

USD 12.45 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.67 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -