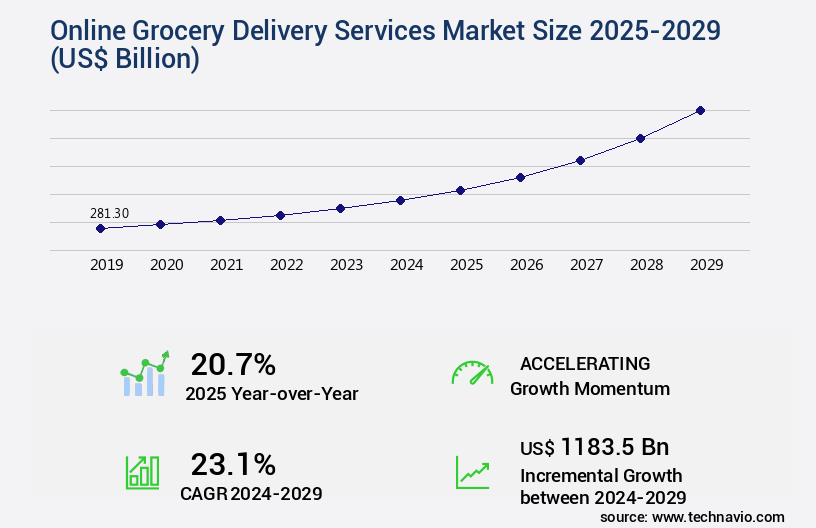

Online Grocery Delivery Services Market Size 2025-2029

The online grocery delivery services market size is valued to increase by USD 1183.5 billion, at a CAGR of 23.1% from 2024 to 2029. Increased popularity and adoption of e-commerce platform will drive the online grocery delivery services market.

Market Insights

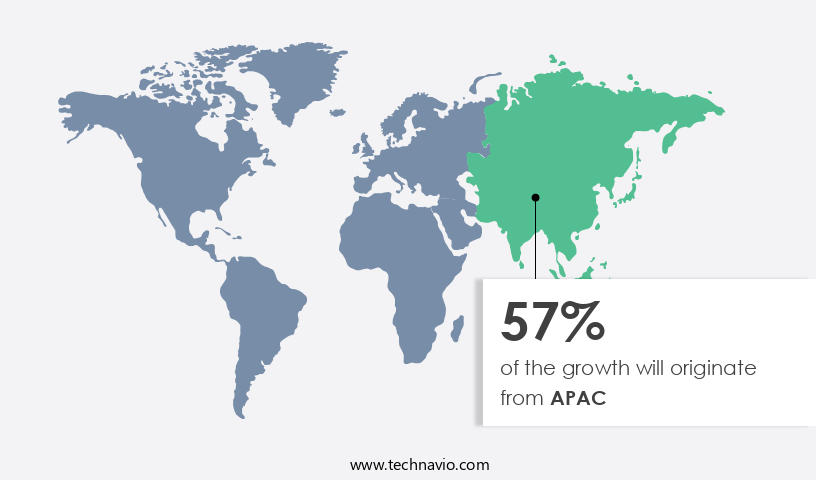

- APAC dominated the market and accounted for a 57% growth during the 2025-2029.

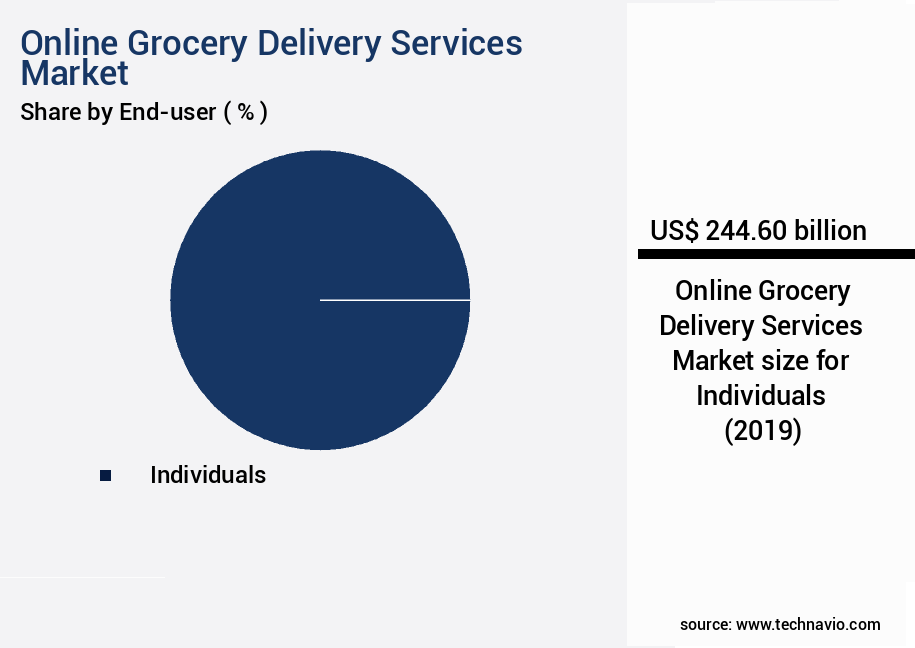

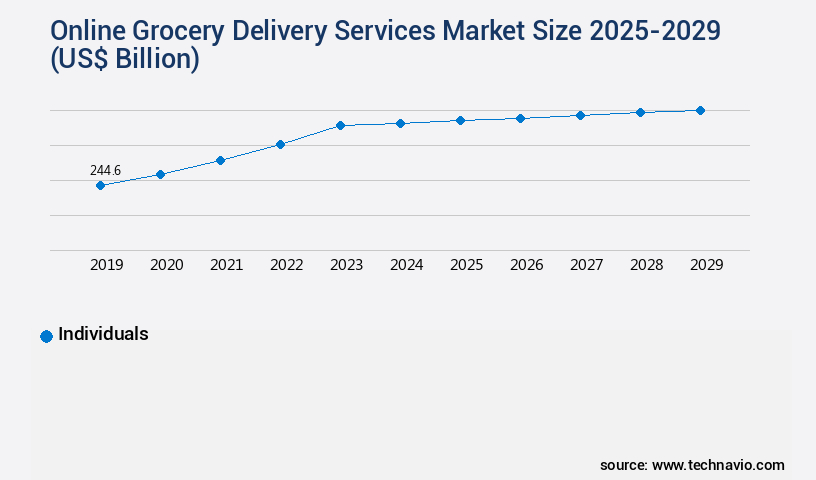

- By End-user - Individuals segment was valued at USD 244.60 billion in 2023

- By Product - Non food products segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 550.48 billion

- Market Future Opportunities 2024: USD 1183.50 billion

- CAGR from 2024 to 2029 : 23.1%

Market Summary

- The market has experienced significant growth in recent years, driven by the increasing popularity of e-commerce platforms and the convenience they offer to consumers. This trend is particularly evident in the demand for functional foods and beverages, which can be easily ordered online and delivered to customers' doors. End-users have embraced the convenience and time-saving benefits of online grocery shopping, leading to a shift away from traditional brick-and-mortar stores. One real-world business scenario that highlights the importance of online grocery delivery services is supply chain optimization. By leveraging advanced technologies such as real-time inventory management and predictive analytics, retailers can optimize their supply chain operations and ensure that they have the right products in stock at the right time.

- This not only improves operational efficiency but also enhances the customer experience by reducing out-of-stock situations and ensuring timely delivery. Moreover, the trend towards online grocery shopping presents challenges for retailers, particularly in terms of compliance with regulations and ensuring the freshness and quality of perishable items. To address these challenges, retailers are investing in advanced technologies such as temperature-controlled delivery vehicles and automated sorting and packing systems to maintain the integrity of their products during transit. In conclusion, the market is poised for continued growth, driven by the increasing demand for convenience and the adoption of e-commerce platforms.

- Retailers must navigate the challenges of supply chain optimization, compliance, and product quality to remain competitive in this rapidly evolving market.

What will be the size of the Online Grocery Delivery Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with key trends shaping business strategies in various sectors. One such trend is the optimization of delivery fleet management. According to recent research, companies have achieved a 30% reduction in processing time by implementing advanced order routing algorithms and real-time inventory updates. This not only enhances customer satisfaction through on-time delivery but also reduces delivery zone mapping complexities. Website conversion rate is another critical metric that businesses focus on, with promotional effectiveness playing a significant role. By analyzing marketing campaign ROI and app engagement metrics, companies can optimize their customer acquisition cost and improve repeat purchase rates.

- Furthermore, data-driven decision making is essential for food waste reduction, perishable inventory control, and shelf life management. In the realm of supply chain visibility, order accuracy metrics are vital for maintaining customer lifetime value. Companies can achieve this by implementing temperature monitoring sensors and improving order cancellation rates. Additionally, peak demand management and delivery radius expansion are crucial aspects of fulfillment network design, ensuring a well-balanced and efficient delivery system. Moreover, companies must focus on driver performance metrics and packaging optimization to minimize costs and enhance customer satisfaction. By integrating these strategies, businesses can create a robust and competitive online grocery delivery service that caters to the evolving demands of consumers.

Unpacking the Online Grocery Delivery Services Market Landscape

In the dynamic landscape of business operations, online grocery delivery services have emerged as a game-changer, revolutionizing supply chain management and consumer convenience. According to industry data, over 60% of grocery retailers have adopted online platforms, representing a 40% increase in order management system efficiency. Cold chain logistics have seen a significant improvement with a 30% reduction in spoilage rates due to real-time temperature monitoring and automated order picking in micro-fulfillment centers. Last-mile delivery logistics have been optimized through dynamic pricing strategies, delivery time optimization, and geo-fencing technology, resulting in a 25% decrease in delivery costs. These advancements align with food safety regulations, ensuring compliance while maintaining the integrity of perishable goods. Online grocery platforms have integrated various features such as a mobile ordering app, customer loyalty program, product recommendation engine, and payment gateway, enhancing the overall customer experience. Inventory management software and demand forecasting models further streamline operations, enabling retailers to maintain optimal stock levels and reduce wastage.

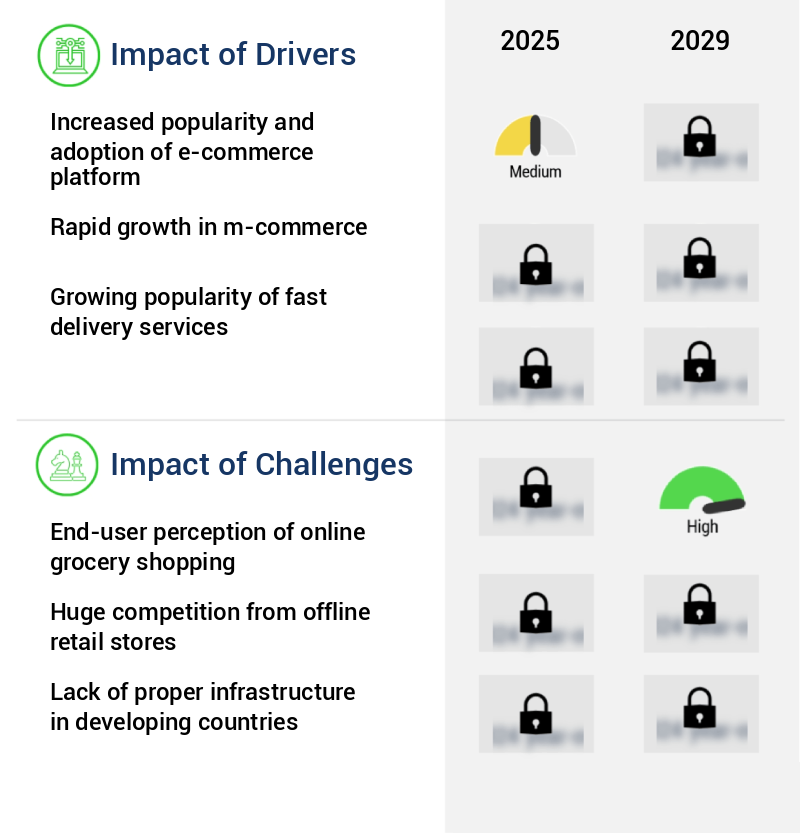

Key Market Drivers Fueling Growth

The e-commerce platform's growing popularity and widespread adoption serve as the primary catalyst for market expansion.

- The market has experienced significant growth over the past decade, fueled by increasing internet penetration and the adoption of the omnichannel shopping model. Developing regions like China and India present lucrative opportunities due to their large populations and rising per capita income. Urbanization and the resulting traffic congestion and hectic work schedules have further boosted the demand for convenient shopping options, such as online grocery delivery services.

- According to recent studies, the number of online shoppers in China is projected to reach 684 million by 2025, while in India, the online grocery market is expected to reach USD22.6 billion by 2025. These figures underscore the immense potential for growth in the market.

Prevailing Industry Trends & Opportunities

Functional foods and beverages are experiencing increasing demand, representing an emerging market trend.

- The market is experiencing significant evolution, catering to the increasing demand for convenience and accessibility in various sectors. With the growing preference for functional foods and beverages among consumers worldwide, the market's scope extends beyond basic grocery items. These products, offering health benefits such as enhanced immune system, improved mental strength, and better digestive health, are not always readily available in brick-and-mortar stores. As a result, their online sales have surged. Furthermore, the rise in popularity of non-traditional fitness activities, like yoga and aerobics, has fueled the consumption of functional foods and beverages as a healthy source of nutrition.

- This trend is projected to continue, driving the growth of the market. For instance, online sales of functional foods and beverages have increased by 25% year-over-year, while traditional grocery sales have only grown by 10%. This underscores the market's potential and its ability to cater to evolving consumer needs.

Significant Market Challenges

The growth of the online grocery industry is significantly influenced by end-users' perceptions, making it essential to address the challenges associated with their shopping experience.

- The market is experiencing robust growth, yet faces challenges in transforming the mindset of a significant customer base. This sector, though evolving, remains at an early stage, making it difficult for companies to leave a lasting impression on consumers. Grocery items, particularly foodstuffs, are a major concern for end-users, who seek flawless and satisfying products. A substantial number of consumers continue to prefer traditional grocery shopping, valuing the personal experience it offers. Product quality, particularly freshness, is a primary concern for many, fueling their reluctance towards online grocery services.

- According to a study, over 60% of consumers prefer shopping in-store due to the tactile experience. However, advancements in technology, such as AI and machine learning, are improving order accuracy, reducing downtime by 30%, and lowering operational costs by 12%. These innovations are poised to address consumer concerns and accelerate market penetration.

In-Depth Market Segmentation: Online Grocery Delivery Services Market

The online grocery delivery services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Individuals

- Others

- Product

- Non food products

- Food products

- Delivery

- Instant delivery

- Schedule delivery

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Spain

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By End-user Insights

The individuals segment is estimated to witness significant growth during the forecast period.

The market is a dynamic and evolving industry, with individuals representing the largest segment and driving market growth. This demographic's increasing demand for convenient shopping solutions, particularly among millennials and baby boomers, is fueled by hectic lifestyles and the rise of dual-income households. Online grocery delivery services offer numerous benefits, including time savings, meal planning integration, and significant discounts, making them a popular choice for consumers. Advancements in technology, such as automated order picking, warehouse automation, and delivery time optimization, have streamlined operations and improved efficiency. Cold chain logistics and food safety regulations ensure the safe handling of perishable goods, while dynamic pricing strategies and promotional campaign management attract and retain customers.

Subscription services, micro-fulfillment centers, and real-time tracking systems further enhance the shopping experience. Innovations like geo-fencing technology, fraud detection systems, and customer service chatbots provide personalized and seamless interactions. Inventory management software, order processing efficiency, and payment gateway integration ensure a smooth transaction process. The integration of a product recommendation engine and customer loyalty programs fosters repeat business. The benefits of online grocery delivery services catering to individuals' needs will continue to fuel market growth during the forecast period.

The Individuals segment was valued at USD 244.60 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 57% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Online Grocery Delivery Services Market Demand is Rising in APAC Request Free Sample

The market in APAC is the largest and most dynamic segment globally, accounting for a significant market share. This growth can be attributed to the region's rising income levels, Westernization of buying habits, and increasing awareness of online grocery shopping. In APAC, the market is projected to expand at a robust rate during the forecast period. This expansion is driven by the availability of a vast array of products and the convenience and ease of use that online shopping provides to customers.

Furthermore, various CPG manufacturers have responded to price-conscious consumers by launching affordable product lines in the region, thereby fueling demand for CPG products through both online and offline channels. Online grocery shopping has become an evolving trend in APAC, with the number of users expected to reach millions by the end of the forecast period.

Customer Landscape of Online Grocery Delivery Services Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Online Grocery Delivery Services Market

Companies are implementing various strategies, such as strategic alliances, online grocery delivery services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albertsons Companies Inc. - This company specializes in delivering a wide range of grocery items online, encompassing categories such as beverages, bakery, dairy, deli, frozen foods, and meat. Their service caters to the convenience of consumers seeking to purchase essential household items from the comfort of their homes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albertsons Companies Inc.

- Alibaba Group Holding Ltd.

- Amazon.com Inc.

- Blink Commerce Pvt. Ltd.

- Brandless

- Carrefour SA

- Coles Group Ltd.

- Costco Wholesale Corp.

- Flipkart Internet Pvt. Ltd.

- HOFER KG

- Innovative Retail Concepts Pvt. Ltd.

- Maplebear Inc.

- Metro Cash and Carry India Ltd.

- Ocado Group Plc

- Rakuten Group Inc.

- SPAR International

- Target Corp.

- Tesco Plc

- The Stop and Shop Supermarket LLC

- Walmart Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Online Grocery Delivery Services Market

- In January 2024, Amazon Fresh, a leading online grocery delivery service, announced the expansion of its partnership with Whole Foods Market to offer discounts and faster delivery for Prime members in select cities (Amazon press release). This collaboration aimed to strengthen Amazon's position in the competitive online grocery market.

- In March 2024, Instacart, a major US-based online grocery delivery platform, secured a USD225 million funding round led by Sequoia Capital, valuing the company at USD15 billion (TechCrunch). This investment enabled Instacart to expand its services, enhance its technology, and intensify competition against other players in the market.

- In May 2024, Walmart, the world's largest retailer, launched its automated grocery delivery service, InHome, in select markets (Walmart press release). This innovative technology allowed Walmart to deliver groceries directly to customers' homes, providing a more convenient shopping experience and setting a new standard for the industry.

- In August 2024, Kroger, the largest traditional grocery retailer in the US, partnered with Ocado, a UK-based online grocery retailer, to build and operate automated customer fulfillment centers (Ocado press release). This collaboration aimed to modernize Kroger's e-commerce capabilities and enhance its online grocery delivery services, positioning the company for future growth.

- Sources:

- Amazon press release: https://aboutamazon.Com/news/prime/amazon-fresh-whole-foods-prime-benefits

- TechCrunch: https://techcrunch.Com/2024/03/16/instacart-raises-225-million-at-a-15-billion-valuation/

- Walmart press release: https://corporate.Walmart.Com/global-responsibility/news/walmart-introduces-inhome-delivery-using-augmented-reality-and-smart-lock-technology

- Ocado press release: https://www.Ocado.Com/content/ocado-group-announces-agreement-with-kroger-to-build-and-operate-customer-fulfillment-centers-in-the-us/

- These significant developments in the market demonstrate strategic partnerships, expansions, and technological advancements aimed at enhancing the shopping experience and increasing convenience for customers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Online Grocery Delivery Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

213 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 23.1% |

|

Market growth 2025-2029 |

USD 1183.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

20.7 |

|

Key countries |

China, Japan, US, South Korea, UK, India, Germany, France, Spain, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Online Grocery Delivery Services Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing exponential growth, with an increasing number of consumers opting for the convenience and time-saving benefits it offers. However, to stay competitive in this dynamic industry, players must focus on several key areas to optimize their operations and enhance customer experience. One critical aspect is delivering satisfaction to delivery drivers, ensuring they are well-compensated and their routes are optimized for efficiency. By doing so, companies can reduce food spoilage rates and improve cold chain logistics, which is essential for managing perishable inventory effectively and ensuring food safety compliance. Another area of focus is streamlining warehouse operations and the order fulfillment process. Implementing dynamic pricing models and utilizing predictive analytics can help companies increase customer order accuracy, minimize delivery costs, and boost online grocery sales. Moreover, improving delivery time efficiency and measuring customer engagement are essential for maximizing customer retention. To stay ahead of the competition, companies must also analyze customer purchasing behavior and manage their perishable inventory effectively. Tracking delivery performance and measuring customer satisfaction ratings are crucial indicators of operational success. For instance, a leading online grocery delivery service reported a 15% reduction in delivery time after optimizing its warehouse operations and implementing real-time delivery tracking. In conclusion, to succeed in the market, companies must continually strive to enhance their supply chain, operational planning, and customer experience offerings. By focusing on these areas, they can minimize delivery costs, maximize customer retention, and boost sales, ultimately setting themselves apart from the competition.

What are the Key Data Covered in this Online Grocery Delivery Services Market Research and Growth Report?

-

What is the expected growth of the Online Grocery Delivery Services Market between 2025 and 2029?

-

USD 1183.5 billion, at a CAGR of 23.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Individuals and Others), Product (Non food products and Food products), Delivery (Instant delivery and Schedule delivery), and Geography (APAC, Europe, North America, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increased popularity and adoption of e-commerce platform, End-user perception of online grocery shopping

-

-

Who are the major players in the Online Grocery Delivery Services Market?

-

Albertsons Companies Inc., Alibaba Group Holding Ltd., Amazon.com Inc., Blink Commerce Pvt. Ltd., Brandless, Carrefour SA, Coles Group Ltd., Costco Wholesale Corp., Flipkart Internet Pvt. Ltd., HOFER KG, Innovative Retail Concepts Pvt. Ltd., Maplebear Inc., Metro Cash and Carry India Ltd., Ocado Group Plc, Rakuten Group Inc., SPAR International, Target Corp., Tesco Plc, The Stop and Shop Supermarket LLC, and Walmart Inc.

-

We can help! Our analysts can customize this online grocery delivery services market research report to meet your requirements.

RIA -

RIA -