Organic Pet Food Market Size 2024-2028

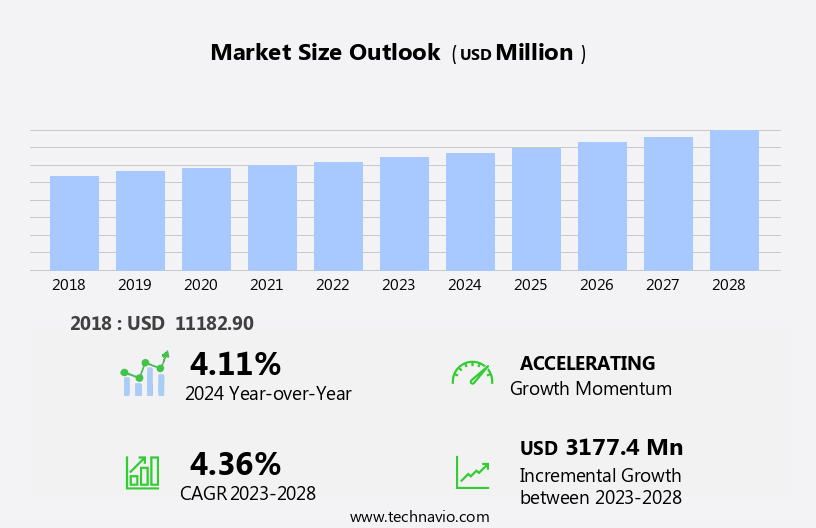

The organic pet food market size is forecast to increase by USD 3.18 billion, at a CAGR of 4.36% between 2023 and 2028.

- The market is driven by the growing awareness and concern for pet health and well-being. Consumers are increasingly recognizing the benefits of organic pet food, which aligns with their own dietary preferences and the desire to provide the best for their pets. companies in this market are capitalizing on this trend by offering organic pet food options with no artificial additives, preservatives, or synthetic ingredients. However, challenges persist in the market. Regulatory compliance is a significant hurdle, with varying definitions and standards for organic pet food across different regions. Additionally, the higher cost of organic ingredients compared to conventional alternatives poses a pricing challenge for companies.

- To overcome these obstacles, companies are adopting innovative strategies such as partnerships with organic farmers, direct-to-consumer sales, and targeted marketing campaigns emphasizing the health benefits of organic pet food. These approaches not only help differentiate their offerings but also enable them to cater to the evolving demands of health-conscious pet owners.

What will be the Size of the Organic Pet Food Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by shifting consumer preferences and advancements in technology. Ethical sourcing and product labeling are paramount, ensuring transparency and trust with pet owners. Palatability remains a critical factor, with pet food manufacturers employing various techniques to create appealing textures and flavors. Freeze-dried pet food and digestibility testing have gained traction, offering benefits such as increased nutrient retention and improved digestion. Functional ingredients, including antioxidants and omega fatty acids, are increasingly integrated into formulations to support pet health. Protein sources, such as novel alternatives, are under scrutiny for their sustainability and nutritional value.

Ingredient sourcing and traceability are essential for maintaining high standards and managing allergens. Pet food processing techniques, including extrusion, have advanced to optimize nutrient retention and texture. Packaging technology plays a crucial role in maintaining shelf life stability and ensuring food safety. Mineral balance and gut health support are key considerations in formulation optimization. Marketing claims and labeling requirements, such as those set by the Association of American Feed Control Officials (AAFCO), continue to shape the market. Quality control measures and supply chain management are essential components of maintaining consumer trust and regulatory compliance. In this dynamic landscape, pet food manufacturers must adapt to meet evolving consumer demands while adhering to strict regulations and ethical standards.

The market will continue to unfold, offering opportunities for innovation and growth.

How is this Organic Pet Food Industry segmented?

The organic pet food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Dry organic food

- Wet organic food

- Animal Type

- Organic dog food

- Organic cat food

- Others

- Distribution Channel

- Pet-specialty stores

- Supermarkets and hypermarkets

- Convenience stores

- Others

- Source

- Animal-Based

- Plant-Based

- Others

- Packaging Type

- Bags

- Pouches

- Cans

- Trays

- Boxes

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

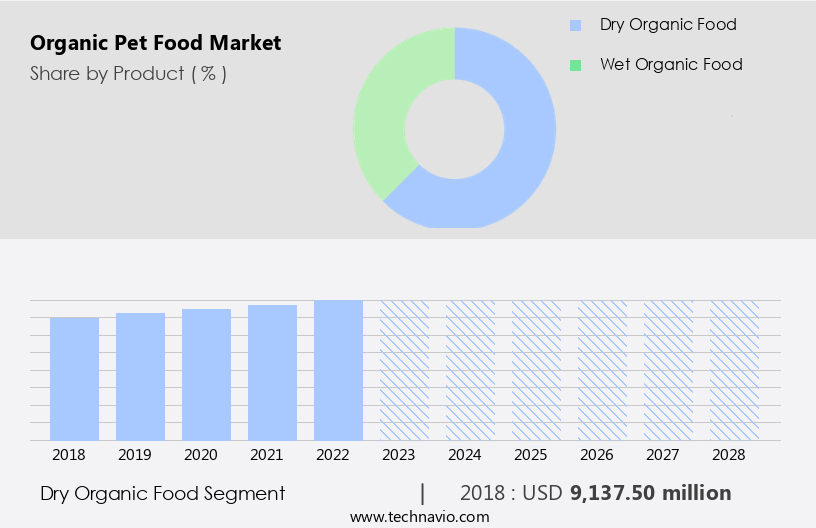

The dry organic food segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth, driven by the increasing demand for pet food that prioritizes safety, traceability, and natural ingredients. Dry organic pet food holds the largest market share due to its numerous benefits, including convenience, oral hygiene promotion, and ease of use in food puzzles. Pet owners value the longer shelf life and ability to leave measured portions out for their pets, ensuring consistent intake and reducing food waste. Aafco standards ensure the safety and nutritional adequacy of organic pet food, while vitamin supplementation and mineral balance contribute to overall pet health. Formulation optimization and functional ingredients cater to specific dietary needs, such as gut health support and allergen management.

Ethical sourcing and sustainable practices are essential considerations for pet food manufacturers, as consumers prioritize the welfare of their pets and the environment. Packaging technology plays a crucial role in maintaining the freshness and quality of organic pet food. Quality control measures, including digestibility testing and nutritional analysis, ensure that these products meet the highest standards. Novel protein sources and limited ingredient diets cater to pets with sensitivities or allergies, while omega fatty acids and antioxidant levels contribute to overall pet health and well-being. Wet pet food and freeze-dried pet food offer alternative options, with wet food providing essential hydration and freeze-dried food offering the benefits of fresh, raw ingredients without the preservatives typically found in canned or kibble form.

Regulations governing pet food safety and labeling ensure transparency and trust in the market. As the market evolves, pet food manufacturers continue to innovate, focusing on optimizing kibble texture, grain-free recipes, and exploring new protein sources to cater to the diverse needs of the pet population. Pet food processing techniques, such as pet food extrusion, ensure consistent quality and nutrient availability. The market is expected to continue growing, driven by these trends and the increasing awareness of the importance of pet health and well-being.

The Dry organic food segment was valued at USD 9.14 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

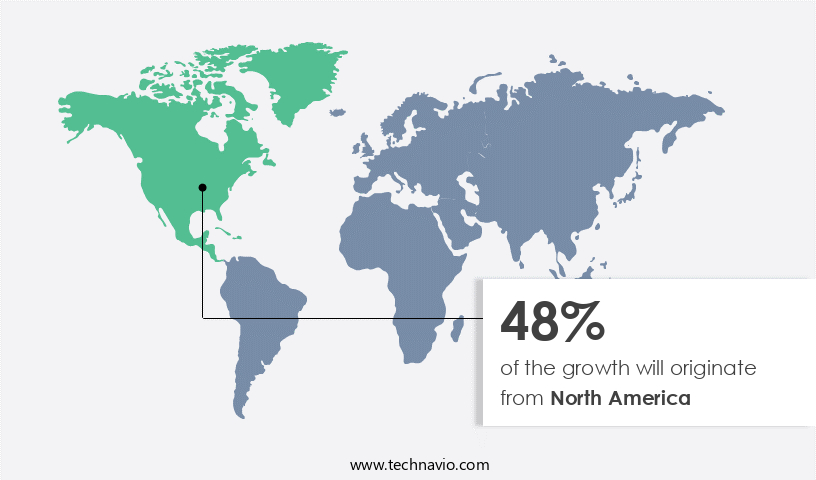

North America is estimated to contribute 48% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing significant growth due to the increasing trend of pet humanization and the large number of pet-owning households. With over 90.5 million pet dogs in the US alone, the demand for high-quality, organic pet food is on the rise. This demand is driven by consumer concerns over pet health and safety, leading to a focus on antioxidant levels, vitamin supplementation, and allergen management. Manufacturers prioritize raw material traceability and ethical sourcing to ensure the safety and quality of their products. Novel protein sources and limited ingredient diets cater to pets with food sensitivities, while formulation optimization and functional ingredients enhance pet health and gut support.

Packaging technology plays a crucial role in maintaining the shelf life stability of organic pet food, especially for wet and freeze-dried varieties. Sustainable sourcing and ethical pet food processing practices are also becoming increasingly important to consumers. Food safety regulations, such as AAFCO standards, ensure the safety and nutritional value of organic pet food. Quality control measures, supply chain management, and nutritional analysis are essential components of the manufacturing process. Marketing claims emphasize the benefits of organic pet food, such as improved digestibility and the presence of essential omega fatty acids. Kibble texture and grain-free recipes cater to various pet preferences.

Overall, the market in North America is expected to continue growing due to the increasing focus on pet health and well-being.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Organic Pet Food Industry?

- The health advantages of organic pet food serve as the primary catalyst for market growth.

- Organic pet food is gaining popularity due to its potential health benefits for pets. The market is driven by various factors, including the desire for weight control, improved gut health, and reduced allergies and skin irritations. Organic pet food formulations are optimized to provide high-quality carbohydrates, ensuring pets maintain a healthy weight and receive essential nutrients. The absence of synthetic additives and preservatives in organic pet food reduces the risk of digestive disorders and allergic reactions. Additionally, the use of sustainable sourcing and pet food processing methods, along with mineral balance, enhances physical vitality and potentially increases a pet's life expectancy.

- Packaging technology plays a crucial role in preserving the freshness and quality of wet pet food, ensuring pets receive optimal nutrition. Organic pet food offers a harmonious balance of essential nutrients, making it a preferred choice for pet owners seeking the best for their furry companions.

What are the market trends shaping the Organic Pet Food Industry?

- The adoption of strategic business approaches by companies is currently a significant market trend. This trend reflects the increasing importance of competitive differentiation and customer satisfaction in today's business landscape.

- The market is experiencing significant growth, driven by increasing consumer awareness and preference for ethical sourcing and product label transparency. companies are focusing on using functional ingredients, digestibility testing, and preserving the natural nutrients through methods like freeze-dried pet food. Protein sources and ingredient sourcing are crucial factors, with many companies emphasizing the use of high-quality, locally-sourced ingredients. Mergers and acquisitions are a primary growth strategy in the market, enabling companies to expand their reach and offerings. For instance, Phoebe, a family-owned manufacturer based in Kiel, Wisconsin, has grown through both co-packing and private labeling for industry leaders.

- These strategic partnerships not only provide cost savings but also open new markets and create multiple growth opportunities. Organic pet food manufacturers are also investing in research and development to improve palatability and maintain the nutritional integrity of their products. The focus on creating harmonious and immersive brand experiences further sets these companies apart in the competitive market. By prioritizing ethical sourcing, functional ingredients, and innovative production methods, companies are catering to the evolving needs and preferences of pet owners.

What challenges does the Organic Pet Food Industry face during its growth?

- The growth of the pet food industry is significantly impacted by marketing strategies surrounding organic labeling, presenting a substantial challenge that requires professional and knowledgeable handling.

- The market dynamics revolve around ensuring quality control measures and adherence to food safety regulations. Brands prioritize supply chain management to maintain the integrity of organic ingredients from farm to shelf. Grain-free recipes and kibble textures are popular trends, with consumers seeking alternatives to traditional pet food formulas. Omega fatty acids are a key focus for pet health, leading to increased demand for nutritionally balanced organic pet food. To meet consumer expectations, brands undergo rigorous nutritional analysis to ensure their products meet the highest standards. However, some brands employ misleading marketing tactics, such as labeling non-organic formulas as "natural" or "made with organic" without the USDA Organic seal.

- This can lead to confusion for consumers, as these labels may not accurately reflect the organic content of the product. Shelf life stability is another critical factor in the market. Brands must ensure their products maintain their nutritional value and texture throughout the entire shelf life to meet consumer expectations and regulatory requirements. By prioritizing these factors, organic pet food brands can build trust with consumers and differentiate themselves from competitors in the market.

Exclusive Customer Landscape

The organic pet food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the organic pet food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, organic pet food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Avian Organics - This company specializes in the production and distribution of premium organic pet food products. Their offerings include a range of items such as alfalfa, almonds, apple chips, banana chips, calendula, coconuts, and carrots, all sourced and processed organically to ensure optimal nutrition for pets.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Avian Organics

- Better Choice Company Inc.

- BiOpet Pet Care Pty Ltd.

- BrightPet Nutrition Group LLC

- Castor and Pollux Natural Petworks

- Darwins Natural Pet Products

- Evangers Dog and Cat Food Co. Inc.

- General Mills Inc.

- Grandma Lucys LLC

- Harrisons Bird Foods

- Hydrite Chemical Co.

- Native Pet

- Nestle SA

- Newmans Own Inc.

- Organic Paws

- PPN Ltd. Partnership

- Primal Pet Foods Inc.

- Raw Paw Pet Inc.

- Tender and True Pet Nutrition

- Yarrah Organic Petfood BV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Organic Pet Food Market

- In January 2024, leading organic pet food manufacturer, EarthBites Pet Nutrition, announced the launch of its new line of grain-free, certified organic dog treats, expanding its product portfolio and catering to the growing demand for allergy-friendly pet food options (EarthBites Press Release).

- In March 2024, organic pet food giants, Organix and Castor & Pollux, joined forces through a strategic partnership to strengthen their market position and offer a more comprehensive range of organic pet food products to consumers (Castor & Pollux Press Release).

- In May 2025, natural pet food company, Open Farm, secured a USD20 million Series C funding round, led by S2G Ventures, to support its continued growth and expansion into new markets, solidifying its commitment to providing ethically sourced, organic pet food options (S2G Ventures Press Release).

- In the same month, the European Union passed the Organic Farming Regulation (EU) 2025/30, mandating stricter regulations for organic pet food production, ensuring higher standards for animal welfare, and the use of organic feed and ingredients (European Parliament Press Release).

Research Analyst Overview

- The market is experiencing significant growth, driven by consumer demand for higher quality, healthier options for their pets. This trend is evident in the increasing focus on carbon footprint reduction and organic certification. Food allergies and sensitivities are common concerns, leading to the popularity of natural preservatives and hypoallergenic formulas. Energy requirements vary by life stage, from puppy food formulas to senior pet nutrition, necessitating product formulation adjustments. Quality assurance systems and animal welfare standards ensure the health and coat improvement of pets. Single-source protein and ingredient quality are crucial factors, as are manufacturing processes that prioritize waste reduction strategies and sustainable agriculture.

- Nutrient bioavailability and calorie density are essential considerations for metabolic rate management. Holistic pet food offerings cater to the growing interest in joint health support, digestive enzyme supplementation, and pest control methods. Packaging recyclability is another critical trend, reflecting the broader focus on sustainability. Overall, the market is dynamic, with a strong emphasis on health, sustainability, and transparency.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Organic Pet Food Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

185 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.36% |

|

Market growth 2024-2028 |

USD 3177.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.11 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Organic Pet Food Market Research and Growth Report?

- CAGR of the Organic Pet Food industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the organic pet food market growth of industry companies

We can help! Our analysts can customize this organic pet food market research report to meet your requirements.

RIA -

RIA -