Wet Pet Food Market Size 2025-2029

The wet pet food market size is forecast to increase by USD 12.8 billion at a CAGR of 7.6% between 2024 and 2029.

- The market is experiencing significant growth, fueled by the increasing number of pet owners worldwide. Wet pet food also contains essential minerals and vitamins that contribute to a balanced diet. Another key driver is the rising popularity of customized pet foods, catering to pets with specific dietary needs or preferences. However, the market faces challenges, including the increasing number of product recalls due to contamination issues and food safety concerns.

- Companies must prioritize product safety and quality to maintain consumer trust and mitigate the potential negative impact of recalls. To capitalize on market opportunities, businesses should focus on innovation, offering customized and premium wet pet food products that cater to diverse consumer needs and preferences. Navigating challenges effectively requires a robust quality control system, transparency, and effective communication with consumers. While grainfree pet food has gained popularity for pets with sensitivities, the demand for organic pet food and vegetablebased pet food reflects a broader shift toward cleaner, health-conscious ingredients.

What will be the Size of the Wet Pet Food Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market exhibits dynamic trends, with dietary restrictions and sustainability practices shaping consumer preferences. Sustainability-conscious pet owners seek out brands that prioritize ethical sourcing and waste reduction. Meanwhile, portion control and life stage nutrition remain key considerations for pet owners. Cognitive health supplements, joint health supplements, dental health supplements, and functional pet food are gaining popularity, driven by veterinary recommendations. Limited ingredient diets and single-source protein diets cater to pets with food sensitivities, while holistic pet food offers a more natural alternative. Premium pet food brands invest in pet owner education and clear feeding guidelines. Supply chain disruptions and food recalls have highlighted the importance of transparency and traceability in pet food production.

Subscription services and innovative packaging materials streamline the pet food delivery process, making it more convenient for busy pet owners. Novel protein sources and pet food formulations cater to the evolving palates and nutritional needs of pets. Overall, the market continues to evolve, driven by consumer demands for high-quality, sustainable, and health-focused options. This trend is driven by the humanization of pets and the growing perception of pets as family members, leading to an increased demand for high-quality, nutritious pet food options.

How is this Wet Pet Food Industry segmented?

The wet pet food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Cat food

- Dog food

- Others

- Source

- Animal-based

- Plant-based

- Synthetic

- Distribution Channel

- Pet-specialty stores and vet clinics

- Supermarkets and hypermarkets

- Convenience stores

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- Spain

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Product Insights

The Cat food segment is estimated to witness significant growth during the forecast period. The market in the US is driven by several factors. Wet pet food provides animals with essential hydration, making it a preferred choice for many pet owners, especially for older cats who find it easier to chew and consume. Consumer preferences lean towards wet food for cats due to its rich smell and flavor, which is more appealing to cats as they age and lose their olfactory senses. Wet food is also beneficial for cats with health issues, such as dental problems or digestive difficulties, which make it difficult for them to consume dry food. Price sensitivity is a significant consideration in the market, with organic and natural pet food options gaining popularity among pet owners.

Quality control is paramount in the production of wet pet food, with strict adherence to food safety regulations ensuring the safety and wellbeing of pets. Prescription pet food and senior pet food cater to specific dietary needs, while vegetable-based, grain-free, and meat-based options cater to various consumer preferences. Moisture content, fiber content, carbohydrate content, and protein content are essential nutritional considerations in wet pet food. E-commerce sales and retail sales are significant distribution channels, with sustainability initiatives and ingredient sourcing playing a crucial role in the market. The market also includes a range of products, such as puppy food, senior pet food, prescription pet food, raw pet food, canned pet food, and freeze-dried pet food, among others.

Fish food, bird food, and small animal food are also part of the market, with a focus on meeting the unique nutritional requirements of these animals. Pet nutrition is a top priority, with pet health and wellbeing driving demand for high-quality wet pet food options. Pet food additives and flavor enhancers are used to enhance the taste and nutritional value of wet pet food, while distribution channels ensure timely and efficient delivery to pet owners. The market in the US is a dynamic and evolving industry, with a focus on meeting the unique nutritional needs and preferences of pets.

Wet pet food offers several benefits, including hydration, ease of consumption, and rich flavor, making it a popular choice among pet owners. The market is diverse, with a range of options catering to various dietary needs, consumer preferences, and animal species. Quality control, food safety regulations, and sustainability initiatives are essential considerations in the production and distribution of wet pet food.

The Cat food segment was valued at USD 12.56 billion in 2019 and showed a gradual increase during the forecast period.

The Wet Pet Food Market is witnessing steady growth as pet parents increasingly seek out nutritious, specialized alternatives to dry pet food. These preferences are shaping innovation in wet formulas that prioritize digestibility and palatability. Accurate and transparent product labeling plays a key role in this market, helping consumers make informed choices about what goes into their pets' bowls. The high protein content in wet pet food makes it an attractive option for pets, particularly for those with active lifestyles.

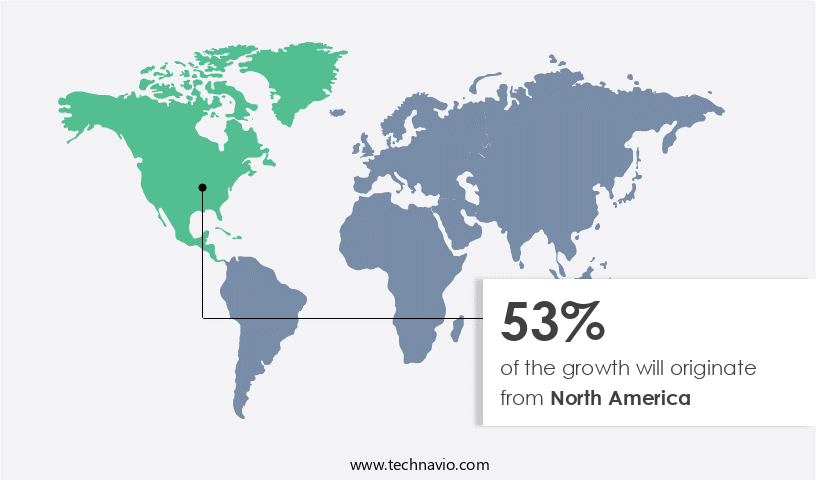

Regional Analysis

North America is estimated to contribute 53% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the Americas, the market is experiencing growth due to pet humanization trends. Consumers prioritize natural, grain-free, or raw diets for their pets, leading to increased demand. Labeling and nutritional analysis are crucial for North American pet owners, who closely examine ingredient sources and react to recalls. The Food and Drug Administration (FDA) enforces regulations under the Food Safety Modernization Act (FSMA), ensuring food safety and quality control. Canadian consumers are well-informed, utilizing the Internet to educate themselves on pet health. Wet pet food offerings include various types, such as puppy, senior, prescription, vegetable-based, meat-based, and prescription formulas. E-commerce sales and retail channels cater to diverse consumer preferences.

Sustainability initiatives are also influencing the market, with options for organic, free-range, and ethically-sourced ingredients. Wet pet food varieties include canned, raw, freeze-dried, and fish food, addressing the dietary needs of various species, including dogs, cats, birds, and small animals. Pet nutrition remains a top priority, with added vitamins, minerals, fiber, and protein content. The market also includes pet food additives and flavor enhancers. The distribution channels extend to retail and e-commerce platforms, ensuring accessibility and convenience for consumers. However, for non-vegan pet owners, wet pet food comes in various protein sources like beef and lamb.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Wet Pet Food market drivers leading to the rise in the adoption of Industry?

- The significant rise in pet ownership serves as the primary catalyst for market growth. Wet pet food has gained popularity among pet owners due to its ability to provide essential nutrients and cater to various dietary needs. Two common types of wet pet food are vegetable-based and grain-free. Vegetable-based options offer fiber-rich ingredients, making them suitable for pets with sensitive digestive systems or those requiring a fiber-rich diet. Grain-free options, on the other hand, cater to pets with grain allergies or sensitivities. Both types of wet pet food have different nutritional profiles. Vegetable-based options typically have a higher fiber content and lower carbohydrate and fat content compared to meat-based alternatives.

- Grain-free meat-based options, however, have a higher fat content and lower carbohydrate content. Shelf life is a crucial factor in the market. Proper food safety regulations ensure the production and distribution of safe and nutritious pet food. E-commerce sales have also rised, making it easier for pet owners to purchase wet pet food online. Natural pet food, including wet pet food, has become increasingly popular due to concerns about food safety and the desire for transparency in ingredient sourcing. Pet owners prioritize natural ingredients and minimal processing to ensure their pets receive the best nutrition possible. The market offers a range of options to cater to various dietary needs and preferences, including vegetable-based, grain-free, and natural options. Proper food safety regulations and the convenience of e-commerce sales have further fueled the growth of this market.

What are the Wet Pet Food market trends shaping the Industry?

- The increasing preference for customized pet foods signifies a notable market trend. This trend reflects the growing recognition of the unique nutritional needs of pets and the desire for personalized feeding options. The market is witnessing significant growth due to the increasing awareness among pet owners regarding pet nutrition and the customization of pet foods to meet individual nutritional needs. This trend is driven by the humanization of pets, as owners seek products that cater to their pets' dietary requirements, taste preferences, and caloric needs. Several companies are responding to this demand by offering customized pet food products. For instance, Nestle's Purina subsidiary provides the Just Right brand of dog food, formulated using organic, single-protein sources. Moreover, sustainability initiatives are gaining importance in the pet food industry, with some companies offering eco-friendly packaging and sourcing ingredients from sustainable sources.

- This trend is not limited to dog food but also extends to other categories such as fish food, bird food, raw pet food, and canned pet food. Flavor enhancers are also used in wet pet foods to improve palatability, making them more appealing to pets. However, there are concerns regarding the use of certain additives, and some pet owners prefer natural alternatives or no additives at all. Retail sales of wet pet food are expected to continue growing, driven by the convenience they offer and the increasing preference for premium pet food products. Overall, the market is dynamic and evolving, with companies continually innovating to meet the changing needs and preferences of pet owners.

How does Wet Pet Food market faces challenges during its growth?

- Product recalls posing a significant challenge to industry growth, the increasing frequency of such events necessitates a proactive response from manufacturers to mitigate potential risks and maintain consumer trust. The market faces a significant challenge due to the increasing number of product recalls, which can negatively impact revenue and erode consumer trust. Recalls can result in costly lawsuits, as seen in the case of Nestle Purina PetCare's voluntary recall of its Purina Pro Plan Veterinary Diets EN Gastroenteric Low Fat (PPVD EN Low Fat) wet dog food. The recall was due to a labeling mistake, with cans of a different complete and balanced adult dog food being mislabeled as PPVD EN Low Fat. This incident underscores the importance of stringent ingredient sourcing and manufacturing processes to ensure product accuracy and consumer safety.

- The market dynamics are further influenced by the demand for high-protein content in pet food, particularly for cats and kittens. Distribution channels continue to evolve, with online sales gaining popularity. Reptile food and small animal food are also growing segments within the market. Pet health remains a top priority for pet owners, driving the demand for additive-free and natural pet food options. Dental problems are a common concern for pet owners, and it can help address this issue as it promotes better oral hygiene.

Exclusive Customer Landscape

The wet pet food market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wet pet food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, wet pet food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Beaphar Beheer BV - This company specializes in providing a range of wet pet food options for dogs and cats, including brands like Baby Blue and Blue Freedom, Blue Wilderness, catering to the nutritional needs of various pet species.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Beaphar Beheer BV

- Blue Buffalo Co. Ltd.

- C and D Foods Ltd.

- Champion Petfoods Holding Inc.

- Clearlake Capital Group L.P.

- Colgate Palmolive Co.

- Darling Ingredients Inc.

- De Haan Petfood

- Evangers Dog and Cat Food Co. Inc.

- FirstMate Pet Foods

- Freshpet Inc.

- Harringtons Pet Food

- Mars Inc.

- Nestle SA

- Phelps Pet Products

- Schell and Kampeter Inc.

- Simmons Foods Inc.

- Spectrum Brands Inc.

- Tiernahrung Deuerer GmbH

- VAFO Group a.s.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wet Pet Food Market

- In January 2024, Nestle Purina PetCare, a leading player in the market, announced the launch of a new line of grain-free, high-protein wet cat food products under its Pro Plan brand (Nestle Purina Press Release, 2024). This expansion aimed to cater to the growing demand for premium, health-conscious pet food options.

- In March 2024, Mars Petcare, another major player, formed a strategic partnership with Blue Buffalo, a US-based pet food manufacturer, to expand its presence in the US the market (Mars Petcare Press Release, 2024). This collaboration allowed Mars Petcare to leverage Blue Buffalo's strong brand reputation and innovative product offerings.

- In May 2024, Hill's Pet Nutrition, a US-based pet food company, received approval from the US Food and Drug Administration (FDA) for its new Science Diet Feline Adult Indoor Grain-Free Chicken Recipe canned cat food (Hill's Pet Nutrition Press Release, 2024). This approval marked the entry of a new product into the market, addressing the increasing demand for grain-free and indoor-specific cat food options.

- In February 2025, Royal Canin, a global leader in pet nutrition, completed the acquisition of Aguas Frescas, a Mexican wet pet food manufacturer, to expand its presence in the Latin American market (Royal Canin Press Release, 2025). This strategic move allowed Royal Canin to tap into the growing demand for wet pet food in the region and strengthen its market position.

Research Analyst Overview

The market continues to evolve, shaped by various dynamics and applications across sectors. Freeze-dried pet food and fish food are gaining traction due to their preservation benefits and unique textures. Pet nutrition remains a primary focus, with sustainability initiatives driving innovation. Moisture content, fiber, and protein are key considerations for meeting the diverse dietary needs of pets. Price sensitivity and consumer preferences influence the market, with organic and natural pet food seeing growth. Brand loyalty and senior pet food cater to specific demographics, while quality control and food safety regulations ensure industry standards. Prescription pet food and vegetable-based options address specific health concerns. Consumer preferences play a significant role in shaping the market, with an increasing trend towards non-vegan options made from high-quality ingredients such as beef, lamb, chicken, and salmon.

Grain-free and meat-based pet food cater to various dietary requirements, with fiber content and carbohydrate levels under scrutiny. Shelf life and distribution channels are crucial for maintaining product freshness and accessibility. E-commerce sales are on the rise, offering convenience and flexibility for pet owners. Pet health and wellbeing remain the ultimate priority, leading to the development of pet food additives and flavor enhancers. Ingredient sourcing and distribution channels continue to evolve, shaping the competitive landscape. Bird food, cat food, and kitten food each present unique market opportunities. Reptile food and small animal food cater to niche markets, expanding the market's reach. The ongoing unfolding of market activities underscores the continuous dynamism of the wet pet food industry.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wet Pet Food Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

224 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.6% |

|

Market growth 2025-2029 |

USD 12.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.7 |

|

Key countries |

US, Canada, Germany, UK, China, France, Japan, Italy, Mexico, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Wet Pet Food Market Research and Growth Report?

- CAGR of the Wet Pet Food industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the wet pet food market growth of industry companies

We can help! Our analysts can customize this wet pet food market research report to meet your requirements.

RIA -

RIA -