Organic Shampoo Market Size 2024-2028

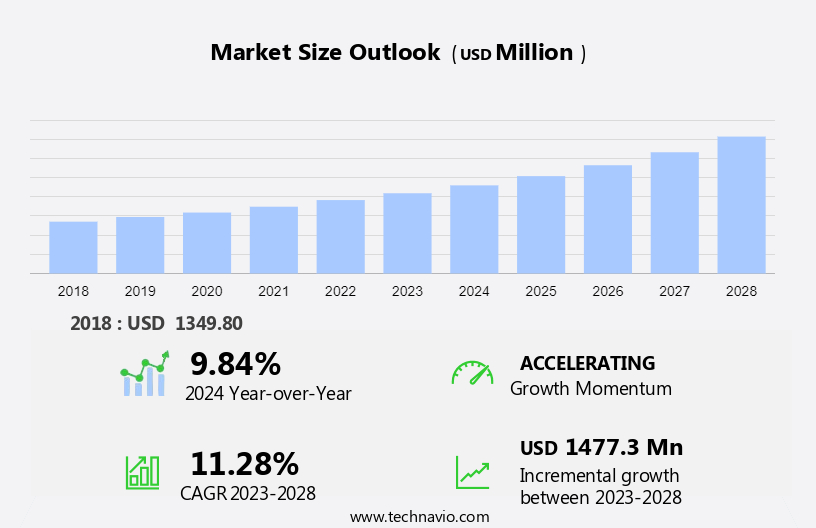

The organic shampoo market size is forecast to increase by USD 1.48 billion at a CAGR of 11.28% between 2023 and 2028.

- The market is experiencing significant growth due to several key trends. The increasing preference for natural ingredients is a major driving factor, as consumers become more health-conscious and seek products free from harsh chemicals. Another trend is the rise of online sales channels, making organic shampoo more accessible to a wider audience.

- However, the high cost associated with organic shampoo production and certification remains a challenge for market growth. Producers must find ways to reduce costs while maintaining quality and transparency to attract price-sensitive consumers. Unlike traditional shampoos, products are made with plant-based ingredients and are free from harmful chemicals such as sulfates, parabens, and synthetic fragrances, which can be harmful to both the hair and the environment. This market trends and analysis report delves deeper into these factors and provides insights into the future growth prospects of the market.

What will be the Organic Shampoo Market Size During the Forecast Period?

- Organic shampoos have gained significant traction in the hair care market due to their ability to provide effective cleansing while minimizing the chemical effects on the scalp and hair. Unlike traditional shampoos, organic shampoos are formulated with natural ingredients, making them ideal for individuals seeking scalp care and hair health. Hard water, excess oil, impurities, and environmental pollutants can cause hair breakage, split ends, and other hair-related issues. Organic shampoos, with their purifying properties, help combat these problems by gently cleansing the hair and scalp without stripping them of their natural oils. Seborrheic dermatitis and folliculitis are common scalp conditions that can lead to itching, inflammation, and dandruff. Organic shampoos, often infused with herbs and natural materials, offer nourishing properties that help soothe and alleviate these conditions, promoting a healthy sheen and fresh aroma. The rise of online influencers and the increasing awareness of cruelty-free products have further fueled the demand for organic shampoos.

- Additionally, these hair care solutions are free from harsh chemicals such as sodium lauryl sulphate and potassium sorbate, making them a more sustainable and eco-friendly choice for consumers. Organic conditioners, also made from natural ingredients, work in tandem with organic shampoos to provide comprehensive hair care. Unlike conventional shampoos containing synthetic ingredients, organic shampoos utilize natural materials such as herbs and essential oils like peppermint, aloe vera, and rosemary. The use of plant-based ingredients in these products ensures that they are not only effective but also gentle on the hair and scalp, promoting overall hair health. In conclusion, the market is driven by the growing demand for chemical-free, natural hair care solutions that offer effective cleansing, scalp care, and environmental sustainability. These products cater to various hair concerns, including hard water, excess oil, impurities, and scalp conditions, making them a popular choice for individuals seeking healthy, beautiful hair.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

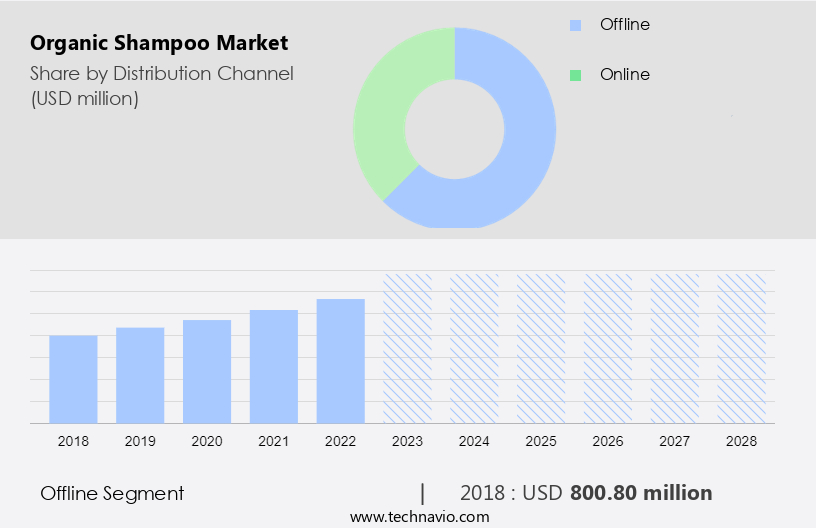

- Distribution Channel

- Offline

- Online

- Type

- Liquid

- Shampoo bars

- Dry shampoo

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- South America

- Middle East and Africa

- North America

By Distribution Channel Insights

- The offline segment is estimated to witness significant growth during the forecast period.

The offline distribution segment dominates The market, accounting for the largest market share in 2023. Offline retail channels offer consumers a tactile experience, which is a significant influencer in purchasing decisions. Hypermarkets, supermarkets, and specialty stores are projected to expand significantly, providing a wider reach and visibility for organic shampoos. Organic shampoos are readily available in organized retail stores, including departmental stores, contributing to their growing sales. The expanding retail industry and the proliferation of retail outlets are key drivers for the market through this segment. Consumers prefer organic shampoos for their ability to address excess oil and impurities, leaving hair with a healthy sheen. Organic conditioning agents are often used in conjunction with organic shampoos for optimal hair health. The natural fresh aroma of organic shampoos adds to their appeal, making them a popular choice among consumers seeking natural and sustainable personal care solutions.

Get a glance at the market report of share of various segments Request Free Sample

The offline segment was valued at USD 800.80 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

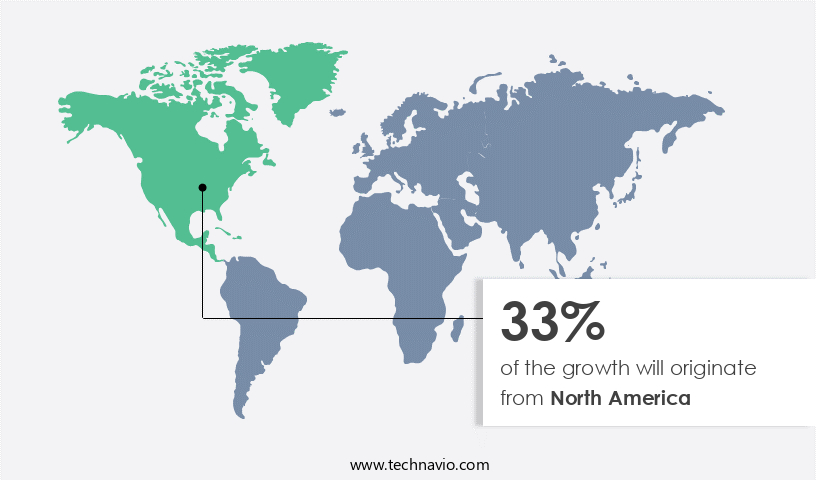

- North America is estimated to contribute 33% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The North American market holds a significant share in the global organic shampoo industry, driven by the presence of well-established retail sectors and an increasing number of companies, such as The Estée Lauder Companies Inc. And Colgate-Palmolive Co., offering organic shampoo options. The region's growth is further fueled by the rising adoption of online shopping and organized retailing, with major e-commerce platforms like Amazon and eBay contributing to substantial sales. In the US and Canada, the demand for organic shampoos is on the rise due to their benefits for scalp care and hair health, addressing issues like hard water damage, hair breakage, and split ends naturally. The market in North America is expected to continue its growth trajectory in the coming years.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Organic Shampoo Market?

The rising popularity of natural ingredients is the key driver of the market.

- The market in the US has witnessed significant growth due to the increasing awareness and concern for scalp care and hair health. Consumers are increasingly seeking out natural and organic hair care solutions, as they become more conscious of the potential chemical effects of traditional shampoos. Hard water, hair breakage, split ends, folliculitis, and dandruff are common hair issues that consumers aim to address with effective and chemical-free products. Natural ingredients, such as herbs and plant-based materials, are gaining popularity as they offer purifying properties, nourishing benefits, and a fresh aroma. Online influencers and e-commerce platforms have played a crucial role in promoting these products, making organic shampoos easily accessible for personal use and commercial purposes. Cruelty-free products have also gained traction, as consumers express their concern for animal welfare. Natural materials, such as sodium lauryl sulfate and potassium sorbate, are used as alternatives to synthetic chemicals, providing effective hair cleaning solutions without causing harm to the hair or the environment.

- Additionally, organic conditioners and hair setting sprays are also gaining popularity, as they offer additional benefits for hair health and maintenance. Water-based formulations and natural botanicals are increasingly preferred, as they align with the demand for personal hygiene and environmental sustainability. Chemical regulations have also played a role in driving the growth of the market, as consumers seek out sulfate-free, paraben-free, and sodium chloride-free alternatives. The availability of discounts and cashback offers on e-commerce platforms further encourages the adoption of these products. In conclusion, the market in the US is experiencing a growth in demand, driven by the desire for natural and chemical-free hair care solutions. These products offer various benefits, such as promoting healthy hair growth, reducing hair fall, and providing a healthy sheen, making them a popular choice for consumers seeking to prioritize their hair health and personal hygiene.

What are the market trends shaping the Organic Shampoo Market?

Increased online penetration is the upcoming trend in the market.

- Organic shampoos have experienced significant growth in the US market as consumers prioritize scalp and hair care solutions free from harsh chemicals. Concerns over chemical effects on hair health, such as hair breakage, split ends, folliculitis, and dandruff, have driven the demand for plant-based hair care. The rise of online influencers promoting natural ingredients, cruelty-free products, and environmental sustainability has further fueled this trend. Hard water and excess oil buildup can lead to impurities and a lackluster hair sheen, making organic shampoos an attractive alternative. These chemical-free products offer purifying properties and nourishing benefits, often derived from natural materials like herbs and herbal beauty and hygiene products. The COVID-19 pandemic has accelerated the shift towards online shopping for personal care items, including organic shampoos. This trend is expected to continue, as consumers appreciate the convenience and safety of shopping from home. E-commerce platforms offer discounts and cashback incentives, making organic shampoos more accessible to a broader audience. Organic conditioners and hair setting sprays are also gaining popularity, as consumers seek comprehensive, chemical-free hair care solutions.

- Additionally, the market for organic shampoos and related products is expected to continue growing, as consumers prioritize personal hygiene and health, and seek sustainable, cruelty-free alternatives to traditional shampoos. Sodium lauryl sulfate and potassium sorbate are common chemical ingredients found in many shampoos. However, organic shampoos rely on natural botanicals and water-based formulations to cleanse and condition hair, providing a healthy sheen and reducing the risk of hair fall. The use of artificial aromas and solvent-based formulations is minimized, making these products more desirable for those seeking a fresh aroma and chemical-free hair care.

What challenges does Organic Shampoo Market face during the growth?

The high cost associated with organic shampoo is a key challenge affecting the market growth.

- Organic shampoos offer scalp and hair care benefits without the chemical effects often found in conventional hair care products. These shampoos are made with natural ingredients, such as herbs and plant-based materials, which provide purifying and nourishing properties. In contrast, commercial shampoos may contain sulfates, parabens, and other synthetic chemicals that can cause hair breakage, split ends, folliculitis, and dandruff. Hard water can also impact hair health by leaving excess oil and impurities on the scalp, leading to a lackluster appearance. Organic shampoos, with their natural ingredients and water-based formulations, effectively cleanse the hair and scalp without stripping it of essential oils. Online influencers and consumers increasingly demand chemical-free products for personal use and salon and spa treatments.

- Additionally, e-commerce platforms offer convenient access to these products, often with discounts and cashback offers. Cruelty-free cosmetics are also gaining popularity, as consumers become more conscious of animal cruelty in the production of beauty products. Organic conditioners, made with natural botanicals, further enhance hair health by providing a healthy sheen and preventing hair fall. The fresh aroma of organic shampoos comes from natural essential oils, as opposed to artificial aromas found in conventional products. Certified organic shampoos undergo rigorous certification processes to ensure environmental sustainability and adherence to strict chemical regulations. While organic shampoos may be more expensive than their conventional counterparts, the benefits to hair health and the environment make them a worthwhile investment.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Beauty Inc.

- Amway Corp.

- Bentley Organic Ltd.

- Bio Veda Action Research Co.

- Colgate Palmolive Co.

- Giovanni Cosmetics Inc.

- Hindustan Unilever Ltd.

- John Masters Organics Inc.

- Johnson and Johnson Services Inc.

- LOreal SA

- LVMH Group.

- NATULIQUE Ltd.

- Onesta Hair Care LLC

- Organic Harvest

- Perse Beauty Inc.

- Real Purity Inc.

- The Body Shop International Ltd.

- The Estee Lauder Companies Inc.

- The Hain Celestial Group Inc.

- Virgin Scent Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Organic shampoos have emerged as a popular choice for consumers seeking to minimize the chemical load in their hair care routine. This market segment, which includes plant-based hair care products, is gaining traction due to increasing awareness of the potential effects of chemicals on scalp health and hair condition. Hard water, which contains minerals like calcium and magnesium, can lead to hair breakage and split ends. Organic shampoos, with their natural ingredients, offer a gentle solution to this problem. They are formulated to effectively cleanse the hair and scalp without stripping them of their natural oils, thereby promoting a healthy sheen. Folliculitis, dandruff, and hair fall are common hair and scalp issues that organic shampoos aim to address. These conditions can be aggravated by harsh chemicals found in conventional shampoos. Organic shampoos, on the other hand, rely on natural ingredients such as herbs and essential oils to purify the scalp and nourish the hair. The rise of online influencers promoting organic hair care products has significantly influenced consumer behavior. These influencers, who often share their personal experiences and product recommendations, have helped create a buzz around organic shampoos.

Additionally, this trend is particularly noticeable in the e-commerce space, where consumers can easily access a wide range of organic hair care products from the comfort of their homes. Cruelty-free products have become a must-have for many consumers, and organic shampoos are no exception. The growing concern for animal welfare has led to a growth in demand for hair care products that are not tested on animals. Organic shampoos, which are inherently cruelty-free, are well-positioned to cater to this demand. Environmental sustainability is another key factor driving the growth of the market. Consumers are increasingly conscious of the environmental impact of their choices, and organic shampoos, with their natural ingredients and eco-friendly packaging, offer a more sustainable alternative to conventional shampoos. The market is diverse, with a range of products catering to different hair types and concerns. Organic conditioners and hair cleaning solutions, including shampoo bars and dry shampoo, that use natural botanicals and water-based formulations are preferred over solvent-based formulations.

In summary, some organic shampoos are formulated to address specific issues like excess oil or impurities, while others focus on providing a fresh aroma and nourishing properties. Water-based formulations and natural botanicals are common ingredients in this market. Despite their benefits, organic shampoos may be more expensive than their conventional counterparts. However, the growing demand for chemical-free and cruelty-free hair care products, coupled with the availability of discounts and cashback offers, is making organic shampoos more accessible to a wider audience. Salons and spas are also embracing the organic shampoo trend, offering their clients a more natural and gentle hair care experience. This trend is particularly noticeable in the luxury segment, where consumers are willing to pay a premium for high-quality organic hair care products and services. In conclusion, the market is driven by consumer preferences for chemical-free and cruelty-free hair care products, as well as a growing awareness of the potential health and environmental benefits of natural ingredients. This market is expected to continue growing, as more consumers seek out gentle and effective hair care solutions that align with their values and promote scalp and hair health.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

157 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.28% |

|

Market growth 2024-2028 |

USD 1.48 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

9.84 |

|

Key countries |

US, Germany, China, UK, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -