- US, Germany, France, China, Japan - Size and Forecast 2024-2028")

Enjoy complimentary customisation on priority with our Enterprise License!

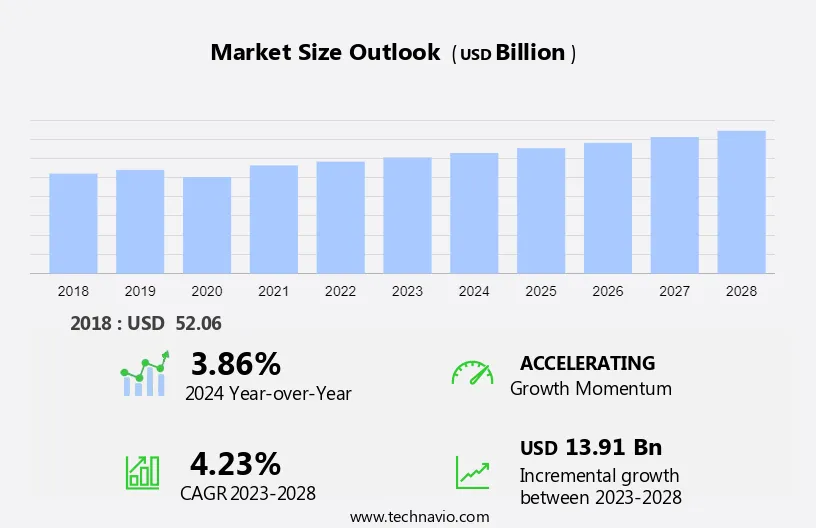

The global orthopedic device market size is estimated to grow by USD 13.91 billion at a CAGR of 4.23% between 2023 and 2028. The market has seen significant advancements with the introduction of minimally invasive (MI) techniques and robotic-assisted surgeries, enhancing surgical precision and patient outcomes. Surgeons now utilize robotic systems for joint replacements, providing better visualization and maneuverability in tight spaces. Integrated surgical tools and multi-armed robots are driving demand for surgical power tools. The adoption of robotic-assisted surgeries offers benefits like reduced complications and labor costs, leading to increased preference in hospitals worldwide. Vendors are actively innovating MI and robotic-assisted technologies, such as Stryker's Mako Robotic-Arm Assisted Technology and Smith and Nephew's NAVIO system, fueling market growth.

|

Study Period |

2024 |

|

Base Year For Estimation |

2023 |

|

CAGR |

4.23% |

|

Forecast period |

2024-2028 |

|

Fastest Growing Region |

North America at 44% |

|

Largest Segment |

Application |

To learn more about this report, Download Report Sample

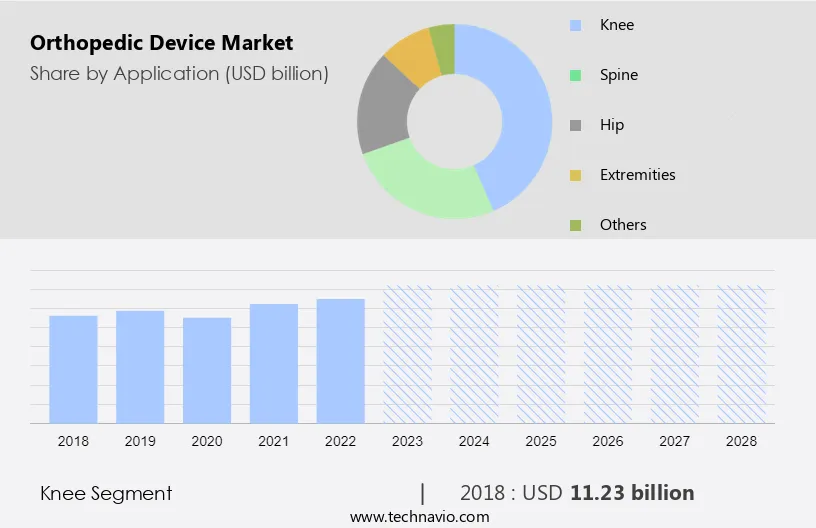

The market share growth by the knee segment will be significant during the forecast period. The knee segment of the market is witnessing significant growth due to factors such as an aging population, increased prevalence of knee-related disorders, and advancements in surgical techniques like minimally invasive procedures. Orthopedic companies are focusing on developing innovative knee implants to enhance patient outcomes and reduce costs.

The knee segment was valued at USD 11.23 billion in 2018. Furthermore, programs like the CJR initiative are driving sales by providing advanced care at lower costs. Additionally, technological advancements like 3D-printed implants are further fueling market growth, with companies like Smith & Nephew and DePuy Synthes leading the way. Such advancements, along with new product launches, are expected to drive continued growth in the knee segment of the market during the forecast period.

The orthopedic implants and support devices segment will account for the largest share of this segment.?The market is growing significantly due to rising orthopedic disorders and demand for minimally invasive procedures. Innovations like robotic-assisted surgeries drive market growth, with key players investing heavily in technology development. Mergers and acquisitions, such as Nuvasive Inc. and Globus Medical's merger, fuel market expansion. Advanced imaging solutions like surgical navigation systems enhance surgical accuracy and recovery, further propelling market growth.

The orthobiologics segment is growing rapidly due to increased bone-related disorders like osteoarthritis and osteoporosis, especially in individuals aged 50 and above. Innovative products like hyaluronic acid by Sanofi aid bone lubrication, particularly in spinal fusion surgeries. Surgeons' reliance on ceramics with cellulose for bone strength during revision arthroplasty boosts demand for synthetic graft materials. Partnership formations and extensive advertising further contribute to the segment's growth in the market during the forecast period.

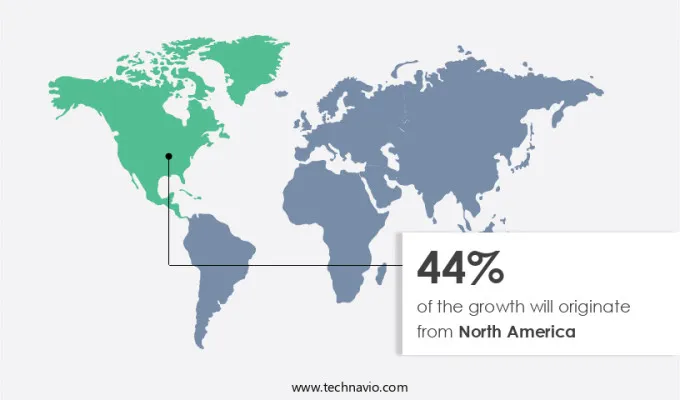

North America is estimated to contribute 44% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that will shape the market during the forecast period. The market in North America is experiencing significant growth due to the increased adoption of orthopedic devices and surgical procedures. Factors such as rising sports-related injuries, advancements in product design, technological upgrades, and favorable reimbursement policies are driving market expansion. Additionally, the implementation of the Affordable Care Act is reshaping the healthcare landscape, aiming to improve access, reduce costs, and enhance healthcare quality. New product launches, supported by ongoing clinical trials and regulatory approvals, are expected to further propel market growth in the region.

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

aap Implantate AG, Arthrex Inc., B.Braun SE, Boston Scientific Corp., Conformis Inc., Conmed Corp., CTL Amedica Corp., Enovis Corp., Exactech Inc., Globus Medical Inc., Integra Lifesciences Corp., Johnson and Johnson Services Inc., Medacta International SA, Medtronic, MicroPort Scientific Corp., OrthAlign Corp., Ossur hf, Smith and Nephew plc, Stryker Corp., TriMed Inc., Zimmer Biomet Holdings Inc., and CurvaFix Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

The market addresses various issues, such as orthopedic disorders and age-related bone disorders prevalent in an aging population. It tackles challenges like degenerative bone disease due to road accidents and sedentary routines, leading to musculoskeletal disorders. Despite disruptions in manufacturing and supply chain, advancements in implant materials and surgical techniques enhance patient safety. Innovations like minimally invasive surgery and robotics revolutionize orthopedic surgeries, supported by computer-aided surgical equipment. The market aligns with WHO guidelines, striving to offer advanced orthopedic devices for improved medical assistance and infection control in elective orthopedic surgeries. Our researchers analyzed the market research and growth data with 2023 as the base year, along with the key market growth analysis, trends, and challenges. A holistic analysis of drivers, trends, and challenges will help companies refine their marketing strategies to gain a competitive advantage.

Continuous advancements is the key factor driving the market. The orthopedic devices market faces challenges, including Class II medical device recalls and manufacturing disruptions, exacerbated by factors such as obesity, traffic accidents, and osteoarthritis, leading to delays in non-urgent orthopedic procedures for patients suffering from orthopedic ailments. Thus, such factors led to advancements in orthopedic devices.

Additionally, orthopedic devices have evolved significantly in the last three decades, driven by robust R&D efforts from key manufacturers. Recent advancements include robotics-assisted smart surgeries, minimally invasive procedures in osteoarthritis, and the utilization of biocompatible materials. Smart implants, such as spine and hip implants with sensors, and innovative knee systems, are gaining traction. Thus, such advancements are poised to propel market growth, offering improved patient outcomes and recovery times.

New product launches coupled with R&D activities is one of the primary market trends shaping the growth. The market is highly competitive, and vendors are increasingly focusing on the development and launch of new orthopedic devices. New product launches, coupled with research and development activities, will enable the vendors to sustain themselves in the competition and enhance their growth. This will have a positive impact on the market growth of orthopedic devices globally during the forecast period.

Additionally, market players are increasingly focusing on the development and launch of new orthopedic devices, specially customized implants, as per the patient's anatomy to reach the desired results post-surgery. Market players such as Stryker, Medtronic, DePuy Synthes, and other prominent vendors are actively involved in the development of innovative devices for improving the efficacy of orthopedic-related implant procedures. Thus, new product launches, coupled with companies growing focus on R&D activities, will have a positive impact on the market growth during the forecast period.

Rising product recalls by companies is the major challenge that affects market expansion. Regulatory agencies evaluate all medical devices for potential risks by conducting a health hazard evaluation. With respect to this, many orthopedic devices and implants have been recalled from the market due to their risk factor. The number of recalled products reported by Exactech was about 40,000, which affected its revenue to some extent; however, it maintained its market position intact owing to the launch of several new products.

Furthermore, any adverse events witnessed during or after the implantation procedure will force the regulators to put pressure on the manufacturers to recall their products. Additionally, most appliances are recalled because of issues with labeling, specification, sterilization, and fractures. Products are recalled voluntarily by the market player or after the US FDA issues warnings. Therefore, the number of products recalled by the company will affect its overall revenue, thereby restricting the market during the forecast period.

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market growth and forecasting report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Customer Landscape

The market report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2018 to 2028.

The market is witnessing significant growth due to advancements in minimally invasive surgical techniques and technologically advanced orthopedic devices. Factors like telemedicine and healthcare infrastructure are driving demand. Stringent regulatory frameworks ensure safety, with research from sources like the Journal of Orthopedic Surgery and Research guiding development. Innovative solutions, such as robotic surgery assistants and citregen, cater to various needs, from joint replacement surgery to addressing conditions like osteoporosis and brittle bone. Additionally, the market is thriving amidst challenges like manufacturing and supply chain disruptions. With advancements like robotic technology, joint replacement implants, and osteosynthesis implants, it addresses various conditions, including sports injuries, rickets, and osteomalacia.

Furthermore, tailored solutions cater to geriatric individuals facing physical weakening and issues with bone tissues. Innovations like tendon-friendly spiral threads enhance orthopedic surgical applications, ensuring better outcomes. Research from institutions like the National Institutes of Health (NIH) drives progress in understanding the molecular and mechanical features of these devices. Additionally, orthopedic manufacturers are increasingly incorporating robotic technologies to enhance surgical precision and outcomes, particularly focusing on optimizing bone-to-mass ratio for improved orthopedic procedures.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

178 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.23% |

|

Market Growth 2024-2028 |

USD 13.91 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.86 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 44% |

|

Key countries |

US, Germany, France, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

aap Implantate AG, Alphatec Holdings Inc., Arthrex Inc., B.Braun SE, Boston Scientific Corp., Conformis Inc., Conmed Corp., CTL Amedica Corp., Enovis Corp., Exactech Inc., Globus Medical Inc., Integra Lifesciences Corp., Johnson and Johnson Services Inc., Medacta International SA, Medtronic, MicroPort Scientific Corp., OrthAlign Corp., Ossur hf, Smith and Nephew plc, Stryker Corp., TriMed Inc., Zimmer Biomet Holdings Inc., and CurvaFix Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Application

7 Market Segmentation by Product

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.