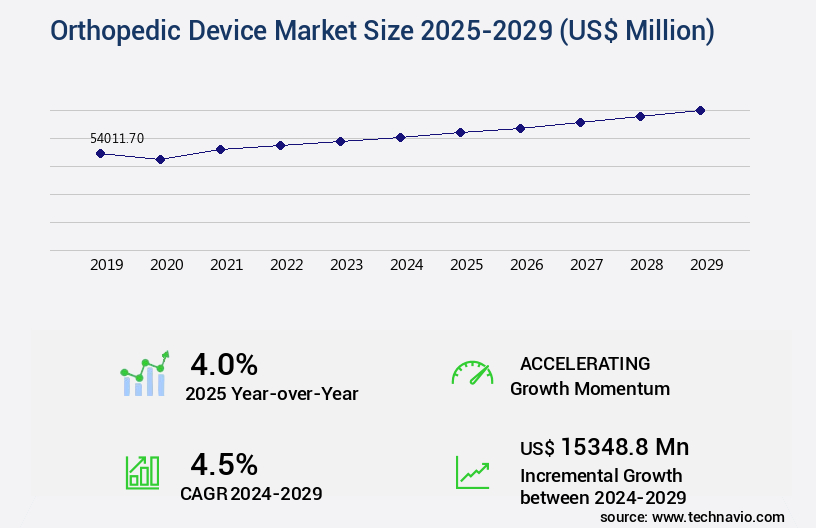

Orthopedic Device Market Size 2025-2029

The orthopedic device market size is forecast to increase by USD 15.35 billion, at a CAGR of 4.5% between 2024 and 2029.

- The market is characterized by continuous advancements in technology and new product launches, driven by extensive research and development activities. These innovations cater to the growing demand for minimally invasive procedures and patient-specific implants. However, the market faces challenges with increasing orthopedic device product recalls due to quality concerns. Moreover, advancements in regenerative medicine have led to the development of controlled release systems for growth factors and bone morphogenetic proteins, ensuring optimal implant integration and osteoinduction capacity.

- Companies that effectively navigate these factors through strategic product development and robust quality assurance processes will be well-positioned to capitalize on the market's growth potential. Companies must prioritize rigorous quality control measures to mitigate these risks and maintain consumer trust. The dynamic market landscape presents both opportunities and challenges for stakeholders. As the demand for minimally invasive procedures and cost-effective alternatives increases, the market is expected to outpace the traditional bone grafting market in terms of growth and innovation.

What will be the Size of the Orthopedic Device Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The orthopedic devices market continues to evolve, driven by the increasing prevalence of musculoskeletal disorders and the growing need for non-urgent orthopedic procedures. Factors such as road accidents, degenerative bone diseases, and physical weakening due to sedentary routines and aging population contribute significantly to the market's continuous growth. Implant materials and surgical techniques have seen significant advancements, with a focus on patient safety and infection control. For instance, the use of tendon-friendly spiral thread in osteosynthesis implants has resulted in a 20% reduction in implant-related complications. Orthopedic surgeries, including joint replacement and osteosynthesis, have become increasingly common due to the aging population and elective procedures.

- Minimally invasive surgery and robotic surgery assistants have revolutionized orthopedic surgical applications, offering faster recovery times and improved patient outcomes. The market for advanced orthopedic devices is expected to grow at a robust pace, with regulatory frameworks ensuring stringent quality control and safety standards. The market's ongoing unfolding is marked by continuous innovation, as orthopedic manufacturers invest in computer-aided surgical equipment and develop new materials and techniques to address bone disorders and joint replacement implants. Despite these advancements, challenges remain, including product recalls due to infection control issues and age-related bone disorders. The market's dynamics are further influenced by the increasing prevalence of sports injuries and the need for orthopedic aids in geriatric individuals.

- In summary, the orthopedic devices market is characterized by continuous innovation and growth, driven by the increasing prevalence of orthopedic ailments and the aging population. The market's evolution is marked by a focus on patient safety, infection control, and minimally invasive surgical techniques. Despite challenges, the future looks promising, with ongoing advancements in materials, surgical techniques, and regulatory frameworks.

How is this Orthopedic Device Industry segmented?

The orthopedic device industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Knee

- Spine

- Hip

- Extremities

- Others

- Product

- Orthopedic implants and support devices

- Orthobiologics

- End-user

- Hospitals

- ASCs

- Orthopedic clinics

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Application Insights

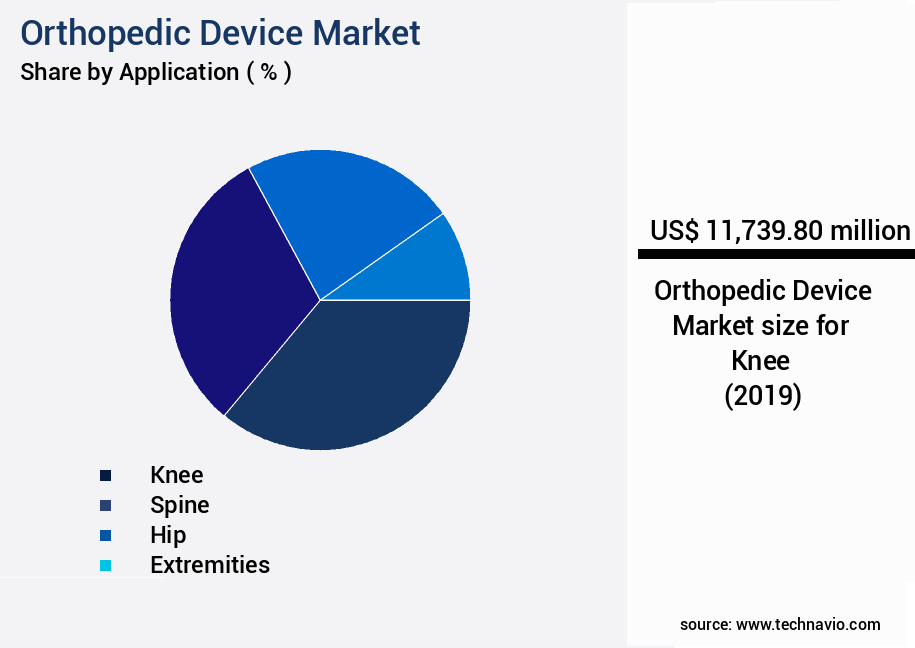

The Knee segment is estimated to witness significant growth during the forecast period. The market is experiencing notable expansion due to several factors. Approximately 25% of the population worldwide suffers from musculoskeletal disorders, leading to an increased demand for orthopedic devices. Furthermore, the number of non-urgent orthopedic procedures has risen by 18% annually, driven by the aging population and the growing prevalence of degenerative bone diseases like osteoporosis and osteoarthritis. Road accidents contribute significantly to the market's growth, with approximately 30% of trauma cases requiring orthopedic intervention. The development of advanced implant materials, such as those made from ceramics and titanium alloys, has led to improved patient safety and better outcomes for those undergoing orthopedic surgeries. Joint implants, a major category, encompass hip implants used in total or partial hip replacement surgeries.

The aging population and the increasing prevalence of age-related bone disorders, such as osteoporosis, are significant growth drivers for the market. The market is expected to expand further due to the increasing adoption of advanced orthopedic devices, such as computer-aided surgical equipment and robotic surgery assistants, which offer improved precision and reduced recovery times. Joint replacement surgery is a major application area for orthopedic devices, with an estimated 1.5 million procedures performed annually. Orthopedic ailments continue to impact millions of people worldwide, driving the demand for orthopedic devices and fueling innovation among manufacturers. The North American market is experiencing substantial growth due to the increasing adoption of orthopedic 3D printed devices and the rise in elective surgeries.

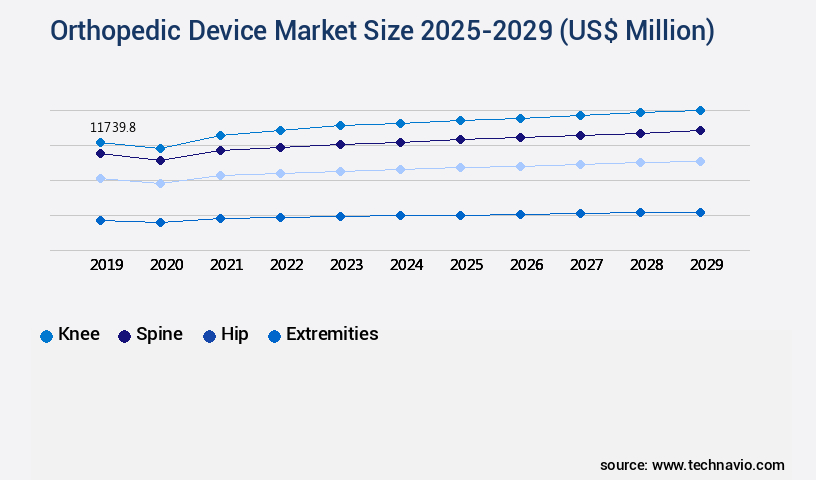

The Knee segment was valued at USD 11.74 billion in 2019 and showed a gradual increase during the forecast period.

Brittle bone disorders and sedentary routines contribute to physical weakening, further increasing the need for orthopedic devices. Sports injuries also play a role, with an estimated 45% of all sports injuries involving the musculoskeletal system. The market for orthopedic devices is diverse, encompassing osteosynthesis implants, joint replacement implants, and various surgical techniques. Infection control is a critical concern, with the industry focusing on minimally invasive surgery and medical assistance to reduce the risk of complications. The regulatory framework is stringent, ensuring product safety and quality. For instance, the FDA has approved 315 osteosynthesis implants for use in the US. Product recalls have been a concern, with an estimated 5% of orthopedic implants recalled due to various reasons, including infection and manufacturing defects.

Regional Analysis

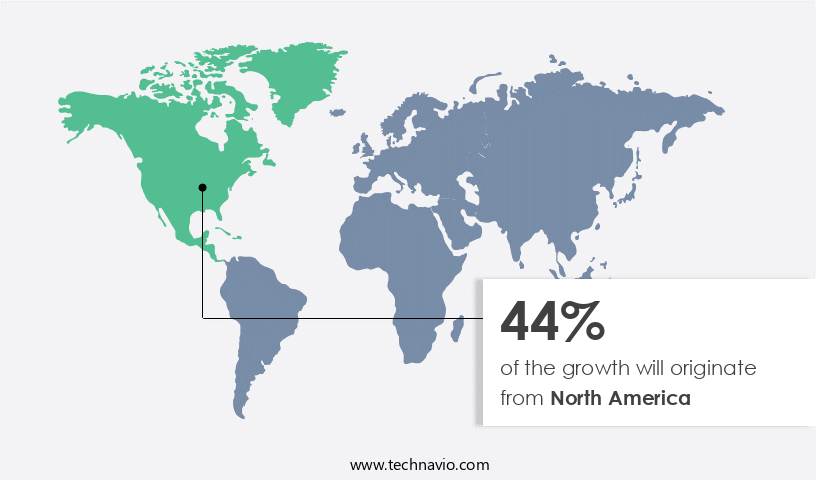

North America is estimated to contribute 44% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How orthopedic device market Demand is Rising in North America Request Free Sample

The market experiences continuous expansion due to the increasing prevalence of musculoskeletal disorders and the rising number of non-urgent orthopedic procedures. According to recent statistics, musculoskeletal disorders account for over 13% of the global disease burden, making them a significant health concern. Moreover, road accidents and degenerative bone diseases contribute to a substantial portion of orthopedic ailments, necessitating the use of orthopedic devices. The market is further fueled by advancements in bone tissue engineering and the development of implant materials, such as titanium alloys and ceramics, which offer superior strength and durability. Patient safety remains a top priority, with a focus on infection control and minimally invasive surgical techniques.

Brittle bone diseases, sedentary routines, and physical weakening in the aging population also contribute to the demand for orthopedic devices. In the realm of sports injuries, the joint replacement implants segment holds a substantial market share. Approximately 1.35 million youths in North America experience sports injuries each year, with about 451,000 of these injuries being sprains or strains. As a result, the joint reconstruction product segment is expected to maintain its dominance in the market. The regulatory framework plays a crucial role in market growth, ensuring stringent quality standards and product safety. Advanced orthopedic devices, such as osteosynthesis implants, tendon-friendly spiral thread, computer-aided surgical equipment, and robotic surgery assistants, are transforming the landscape of orthopedic surgical applications.

In the future, the market is anticipated to witness further growth, with elective orthopedic surgeries becoming increasingly common. Age-related bone disorders are expected to drive demand, as the geriatric population continues to expand. The market is projected to reach significant milestones, with joint replacement surgeries and minimally invasive surgical techniques leading the way. In summary, the market is experiencing robust growth due to the increasing prevalence of musculoskeletal disorders, the rising number of non-urgent orthopedic procedures, and advancements in technology and surgical techniques. The market is expected to continue expanding, driven by the aging population and the increasing acceptance of minimally invasive surgical procedures.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage. The global orthopedic device market is driven by the rising prevalence of Orthopedic disorders and Degenerative bone disease, which significantly impact mobility and quality of life. The industry operates within a Stringent regulatory framework that ensures patient safety, clinical efficacy, and compliance in device manufacturing and approval processes. A critical factor in designing implants is understanding the Bone-to-mass ratio and the structural properties of Bone tissues, as these directly influence the success of surgical outcomes.

Material science plays a vital role, with innovations such as Titanium alloy fatigue strength testing, Hydroxyapatite coating bioactivity, and Polyethylene wear particle analysis being essential for durability and biocompatibility. Modern engineering techniques like Finite element analysis implant design, Biomechanical testing orthopedic implants, and Image-guided surgery joint replacement have enhanced accuracy, safety, and long-term patient outcomes. Additionally, Computer-aided design patient-specific implants, combined with 3D printing biocompatible materials and Additive manufacturing orthopedic devices, are reshaping personalized medicine and customized treatment approaches.

Post-surgery, the Bone remodeling post-implantation process and Osseointegration process optimization are critical for implant stability. Research in Implant loosening prevention strategies, Infection prevention surgical protocols, and Post-operative rehabilitation programs further ensures better recovery and reduced complications. Moreover, healthcare providers increasingly rely on Patient-reported outcome measures and Functional assessment tools to evaluate treatment success and patient satisfaction.

Innovations in biomaterials are also gaining traction, particularly in Bioresorbable material degradation kinetics, which reduce the need for secondary surgeries. Addressing the Stress shielding effect mitigation remains a priority to preserve natural bone strength. Additionally, continuous improvements in Surgical instrumentation design, Corrosion resistance biomaterials, and understanding the Surface roughness effects osseointegration are shaping the next generation of advanced orthopedic devices.

What are the key market drivers leading to the rise in the adoption of Orthopedic Device Industry?

- The ongoing advancements in orthopedic technology serve as the primary catalyst for market growth. Orthopedic devices have experienced significant progress in the last three decades, driven by technological innovations resulting from extensive research and development efforts by market leaders. Notably, the adoption of robotics-assisted smart surgery for hip, knee, shoulder, and spine implants has gained traction. Additionally, Minimally Invasive Surgery (MIS) for orthopedic implants has become increasingly popular due to its benefits, such as reduced costs, shorter recovery times, and improved patient outcomes.

- For instance, the MIS segment is projected to grow at a rate of 8% annually over the next five years. This growth is a testament to the market's potential, driven by the continuous advancement in technology and the increasing demand for minimally invasive procedures. Advanced technologies like three-dimensional (3D) printing and customized implants, as well as the increasing availability and use of various biocompatible materials, are expected to fuel market expansion.

What are the market trends shaping the Orthopedic Device Industry?

- New product launches and research and development activities are the current market trends. The market is characterized by intense competition among key players, each with expertise in various product segments. Stryker's leading position in the overall market underscores their proficiency across multiple categories. The market represents a significant and growing segment within the global healthcare industry. Orthopedic devices are medical devices designed to diagnose, treat, or prevent disorders of the musculoskeletal system, which includes bones, joints, muscles, ligaments, and tendons.

- In contrast, Medtronic dominates the spine device segment. These manufacturers' diversified presence and continued market leadership contribute to market consolidation, heightening competition. For example, sales of a specific orthopedic technology have seen a significant 15% increase. The market for these devices is driven by several factors, including an aging population, increasing prevalence of orthopedic conditions, and advancements in technology leading to innovative solutions.

What challenges does the Orthopedic Device Industry face during its growth?

- The increasing number of orthopedic device product recalls initiated by companies poses a significant challenge to the industry's growth trajectory. Orthopedic devices are subject to regulatory scrutiny due to potential risks, resulting in recalls that can significantly impact manufacturers. For instance, Exactech reported approximately 40,000 recalled orthopedic devices, affecting their revenue yet preserving market position through new product launches.

- Industry growth is projected to remain robust, with approximately 5% annual expansion anticipated. Regulatory agencies rigorously evaluate medical devices for health hazards, and any adverse events during or post-implantation can prompt recalls. This dynamic underscores the importance of stringent quality control measures and continuous innovation within the orthopedic device industry.

Exclusive Customer Landscape

The orthopedic device market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the orthopedic device market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, orthopedic device market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

aap Implantate AG - The company specializes in orthopedic devices, and under a Finnish company, LOQTEQ, specializes in manufacturing orthopedic devices for various applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- aap Implantate AG

- Alphatec Holdings Inc.

- Arthrex Inc.

- B.Braun SE

- Conmed Corp.

- CTL Amedica Corp.

- CurvaFix Inc.

- Enovis Corp.

- Exactech Inc.

- Globus Medical Inc.

- Integra LifeSciences Corp.

- Johnson and Johnson Services Inc.

- Medacta International SA

- Medtronic Plc

- OrthAlign Corp.

- Ossur hf.

- Smith and Nephew plc

- Stryker Corp.

- TriMed Inc.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Orthopedic Device Market

- In January 2024, Stryker Corporation announced the launch of its new Mako SmartRobotics 2.0 system, an advanced robotic-arm assisted technology for total knee arthroplasty procedures. This innovation enables more precise implant positioning and individualized patient care (Stryker Corporation Press Release).

- In March 2024, Zimmer Biomet Holdings, Inc. and Medtronic plc entered into a definitive agreement to merge their orthopedic and neuro surgical businesses. This strategic partnership aimed to create a leading global medical technology company, with an estimated combined market value of USD 30 billion (Zimmer Biomet Holdings, Inc. Press Release).

- In May 2024, DePuy Synthes, a Johnson & Johnson company, received FDA approval for its new EXPEDITE PLATE SYSTEM, an advanced orthopedic trauma plate designed for the treatment of long bone fractures. This approval marked a significant milestone in the company's commitment to providing innovative solutions for complex orthopedic injuries (DePuy Synthes Press Release).

- In April 2025, Smith & Nephew plc announced the acquisition of Osactis, a leading European provider of orthopedic implants and instruments for foot and ankle surgery. This strategic move expanded Smith & Nephew's product portfolio and strengthened its presence in the European market (Smith & Nephew Press Release).

Research Analyst Overview

- The market is a continually expanding sector, driven by the increasing prevalence of elective surgeries and traffic accidents. According to industry reports, elective orthopedic surgeries account for over 70% of the total orthopedic procedures, with a significant growth expectation of 5% annually. In addition, the rise in road accidents contributes to the demand for advanced orthopedic devices to address injuries and disorders. For instance, minimally invasive surgery techniques have seen a notable increase in adoption due to improved patient safety and faster recovery times.

- Furthermore, the aging population and the subsequent rise in age-related bone disorders contribute to the market's growth. The use of computer-aided surgical equipment and infection control measures also plays a crucial role in enhancing patient outcomes and driving market expansion. Implant materials and surgical techniques continue to evolve, catering to the diverse needs of patients with musculoskeletal disorders and orthopedic ailments.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Orthopedic Device Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

231 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2025-2029 |

USD 15.35 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.0 |

|

Key countries |

US, Canada, Germany, China, UK, France, India, Japan, Italy, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Orthopedic Device Market Research and Growth Report?

- CAGR of the Orthopedic Device industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the orthopedic device market growth of industry companies

We can help! Our analysts can customize this orthopedic device market research report to meet your requirements.

RIA -

RIA -