Packaged Natural Mineral Water Market Size 2025-2029

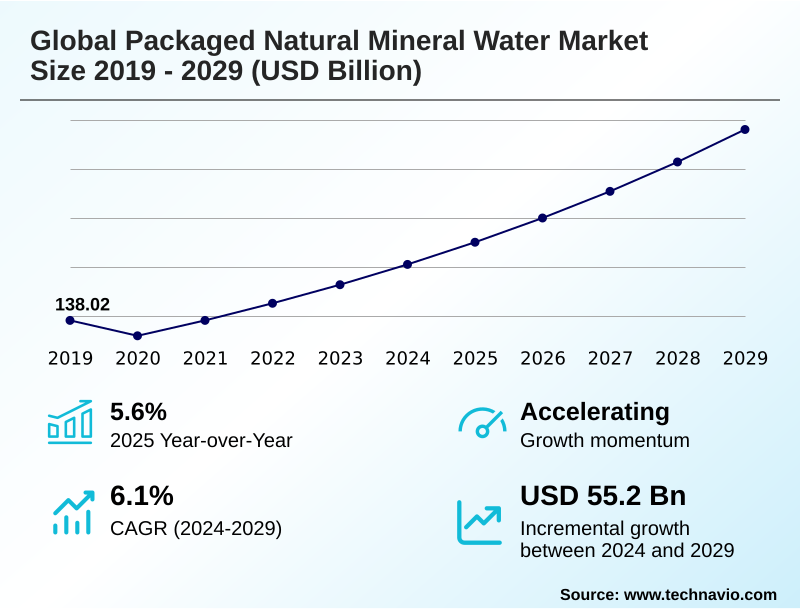

The packaged natural mineral water market size is valued to increase by USD 55.20 billion, at a CAGR of 6.1% from 2024 to 2029. Heightened health and wellness consciousness propelling market growth will drive the packaged natural mineral water market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 41.6% growth during the forecast period.

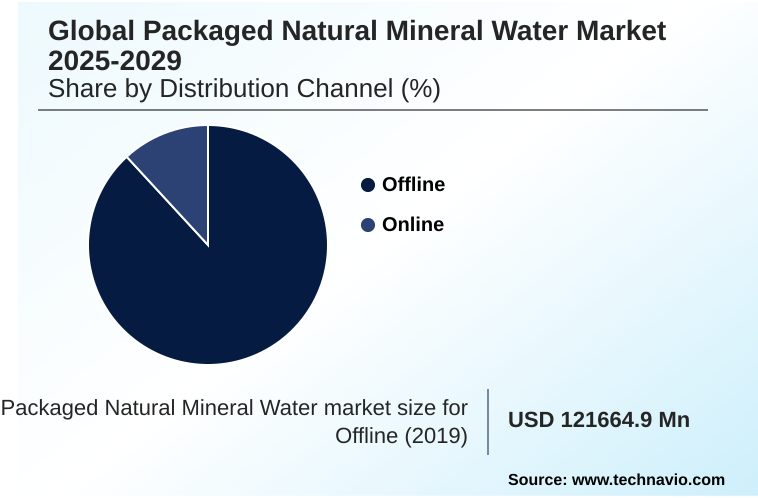

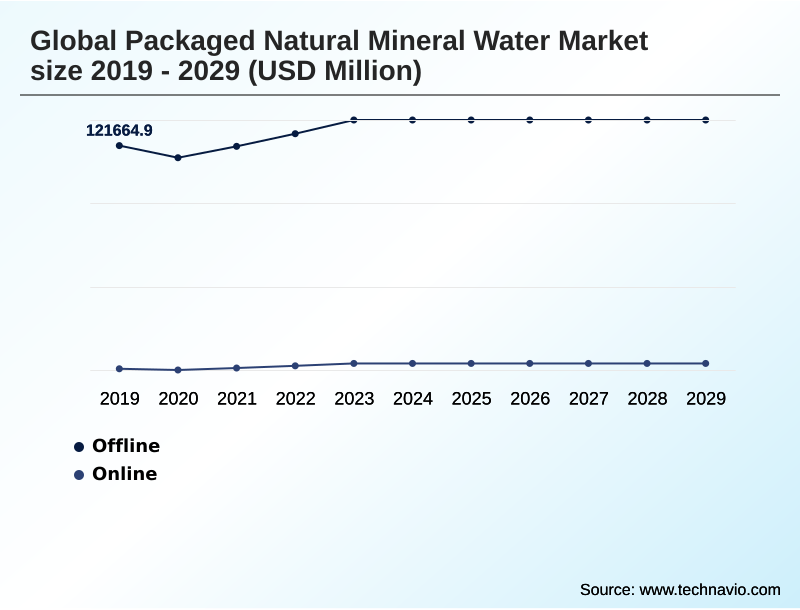

- By Distribution Channel - Offline segment was valued at USD 133.75 billion in 2023

- By Product - Packaged natural sparkling mineral water segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 78.10 billion

- Market Future Opportunities: USD 55.20 billion

- CAGR from 2024 to 2029 : 6.1%

Market Summary

- The packaged natural mineral water market is characterized by a fundamental consumer shift toward health and wellness, creating robust demand for pure hydration solutions. This movement away from sugary drinks underpins the market's expansion, with both packaged natural still mineral water and its sparkling counterpart gaining share.

- Concurrently, the industry grapples with the critical challenge of sustainability, as regulatory pressure on packaging and consumer demand for eco-friendly alternatives intensify. This has spurred innovation in materials and circular economy models. For instance, a beverage company facing complex supply chain logistics can achieve significant operational efficiencies by adopting lightweighting technologies for its PET bottle production.

- This strategic move not only reduces the carbon footprint by lowering transportation weight but also mitigates operational cost pressures associated with raw material usage. The market's trajectory is further shaped by the premiumization trend and the rise of functional waters, which offer added benefits like electrolytes or enhanced alkalinity, appealing to a discerning consumer base seeking more than simple hydration.

- Balancing the demand for pristine, high-quality water from sources like artesian aquifers with environmental stewardship and operational viability remains the central strategic focus for market participants.

What will be the Size of the Packaged Natural Mineral Water Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Packaged Natural Mineral Water Market Segmented?

The packaged natural mineral water industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Distribution channel

- Offline

- Online

- Product

- Packaged natural sparkling mineral water

- Packaged natural still mineral water

- Type of packaging

- Plastic bottles

- Glass bottles

- Cans

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Italy

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The offline distribution channel, encompassing supermarkets, convenience stores, and other physical retail outlets, remains the foundational pillar of the market.

This segment's dominance is sustained by impulse purchase behavior and the convenience demanded for on-the-go consumption, which physical stores are uniquely positioned to satisfy.

With bottled water accounting for 12.4% of all packaged beverage dollars in convenience stores, strategic product placement is critical. The segment is also experiencing a surge in private label brand growth, intensifying market competition.

As the premiumization trend continues, retailers are dedicating more shelf space to options like packaged natural sparkling mineral water, often sourced from an artesian aquifer, reflecting a sophisticated consumer palate and driving further diversification within the channel.

The Offline segment was valued at USD 133.75 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 41.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Packaged Natural Mineral Water Market Demand is Rising in APAC Get Free Sample

The global market exhibits diverse regional dynamics, with APAC holding an estimated 38% of the market share, driven by rising incomes and significant tap water quality concerns. In this region, demand is primarily for basic, safe hydration.

In contrast, mature markets like Europe and North America are characterized by high per capita consumption and a focus on premium and functional products. European consumer behavior reflects this, with 53% choosing bottled water for its perceived health benefits.

North America showcases a strong commitment to sustainability, where the average recycled content in PET bottles has reached 16.2%.

This focus on a circular economy is compelling brands to innovate in packaging, while the convenience of home and office delivery (HOD) services and direct-to-consumer (D2C) channels expands market access.

Market Dynamics

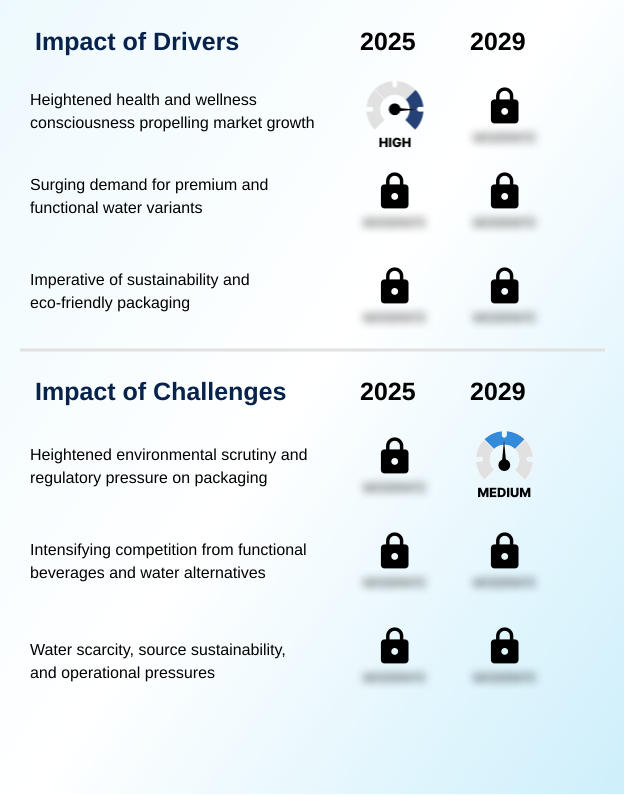

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The market's future is being defined by a complex interplay of consumer demands and operational realities. The impact of rPET on brand perception is undeniable, as eco-friendly packaging innovations in bottled water now directly influence purchasing decisions.

- This is tied to the growing consumer demand for functional mineral water, with the functional water market growth factors pointing toward personalized health benefits. Premiumization strategies for natural mineral water are evolving, moving beyond source to include unique mineral profiles and sustainable narratives.

- However, these strategies face the underlying challenges of water source sustainability and the logistical challenges in water distribution. The regulatory landscape for plastic packaging continues to tighten, forcing a re-evaluation of materials, with consumer perception of glass vs plastic bottles shifting toward more recyclable options. Competition from tap water filtration systems is compelling brands to reinforce their value proposition.

- The role of celebrity endorsements in water branding has proven effective for new entrants, but long-term success depends on managing supply chain risks in the water industry. Firms that successfully navigate the impact of deposit return schemes on recycling and trends in direct-to-consumer water sales, while demonstrating credible water stewardship in beverage manufacturing, are best positioned for growth.

- For example, brands that transparently report on sustainable sourcing of natural mineral water have seen positive consumer sentiment metrics improve by a greater margin than those relying solely on marketing spend.

What are the key market drivers leading to the rise in the adoption of Packaged Natural Mineral Water Industry?

- Heightened consumer consciousness regarding health and wellness is a primary driver propelling growth in the market.

- Market growth is fundamentally driven by a pronounced consumer preference shift toward healthier hydration, rooted in a powerful health and wellness trend.

- Consumers are actively choosing packaged natural still mineral water as a sugar-sweetened beverages alternative, a behavior that has solidified bottled water's position as the leading packaged beverage in major markets for nine consecutive years.

- This demand is amplified by the convenience of products designed for on-the-go consumption.

- Furthermore, the premiumization trend and rising disposable incomes are fueling interest in products with a stable mineral composition and functional benefits, such as vitamin-infused water and electrolyte-infused water.

- In Europe, over 70% of consumers now opt for healthier drinks, reflecting a deep-seated demand for personalized nutrition solutions that support an active and wellness-oriented lifestyle driven by urbanization-driven demand.

What are the market trends shaping the Packaged Natural Mineral Water Industry?

- The critical imperative for sustainable packaging is emerging as a defining trend, shaping corporate strategy and consumer purchasing decisions across the market.

- The market is undergoing a significant transformation driven by the ascent of functional and flavored waters and the critical imperative of sustainable packaging. A major trend is the expansion of the premium water segment, where products are differentiated by their unique water source and sophisticated packaging design.

- This is coupled with a move toward value-added hydration products that offer enhanced wellness benefits. Innovations in alternative packaging materials are accelerating, with launches in aluminum cans tripling in recent years, reflecting strong consumer demand for recyclability. Similarly, the use of recycled PET (rPET) is becoming standard practice, supported by advancements in lightweighting technologies and an emerging refillable bottle culture.

- The functional beverage category is also a key growth area, with European product launches featuring vitamin and mineral fortifications experiencing a 30% compound annual growth rate.

What challenges does the Packaged Natural Mineral Water Industry face during its growth?

- The industry faces a significant challenge from heightened environmental scrutiny and increasing regulatory pressure on packaging materials.

- The market faces considerable headwinds from intensifying market competition and stringent regulatory pressure on packaging, particularly single-use plastics. The proliferation of tap water filtration systems presents a low-cost alternative, eroding market share and impacting brand loyalty factors.

- Concurrently, operational cost pressures are mounting due to supply chain complexities and water scarcity impact, with disruptions from issues like cargo theft rising by over 10% in the last reporting period. The European Union's mandate for plastic bottles to contain at least 25% recycled plastic by 2025 exemplifies the stringent regulations forcing investment in new materials and processes.

- This environment fosters a challenging landscape where companies must innovate in both product and packaging to remain competitive against private label brand growth and shifting consumer preferences.

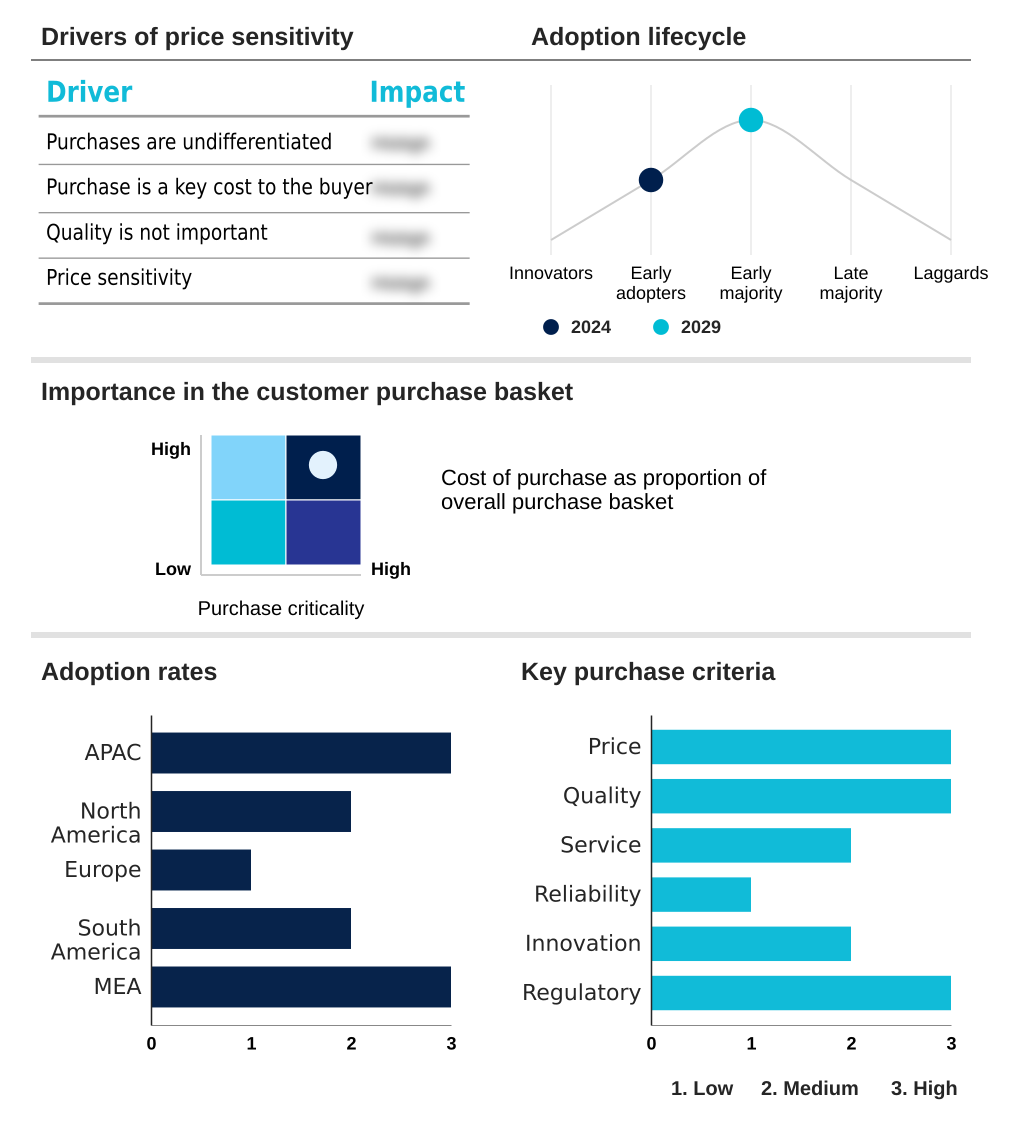

Exclusive Technavio Analysis on Customer Landscape

The packaged natural mineral water market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the packaged natural mineral water market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Packaged Natural Mineral Water Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, packaged natural mineral water market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agthia Group PJSC - Offerings include premium and functional waters, differentiated by source purity, natural mineral composition, and advanced packaging solutions that cater to health-conscious consumers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agthia Group PJSC

- Beverly Hills Drink Co.

- Bisleri International Pvt. Ltd.

- China Resources Beverages Ltd.

- Danone S.A.

- Gerolsteiner Brunnen GmbH

- Grupo Embotellador ATIC SA

- Masafi Co. LLC

- Mountain Valley Spring Co. LLC

- Nestle SA

- Parle Agro Pvt Ltd.

- PepsiCo Inc.

- Tata Consumer Products Ltd.

- The Coca Cola Co.

- The Wonderful Co. LLC

- United Breweries Ltd.

- VOSS Global Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Packaged natural mineral water market

- In August 2024, Flow Beverage Corp. announced the upcoming launch of its new Flow Sparkling Mineral Spring Water in aluminum bottles, made from over 70% recycled material, targeting both Canada and the US.

- In October 2024, Water Almighty launched its Mighty Pure and Mighty Minerals waters in infinitely recyclable aluminum bottles in the UK, directly addressing consumer concerns over plastic waste.

- In January 2025, Agthia Group PJSC completed its acquisition of Riviere, a UAE-based water company, to significantly bolster its home and office delivery segment.

- In March 2025, Gerolsteiner Brunnen GmbH and Co. KG initiated a product recall for certain glass bottles due to a production flaw that posed a risk of cracking.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Packaged Natural Mineral Water Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.1% |

| Market growth 2025-2029 | USD 55198.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 5.6% |

| Key countries | China, India, Japan, Indonesia, South Korea, Australia, US, Canada, Mexico, Germany, Italy, France, Spain, UK, Hungary, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Morocco |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The packaged natural mineral water market is evolving beyond basic hydration, driven by sophisticated consumer demands for both purity and purpose. Core offerings of packaged natural still mineral water and its sparkling counterpart are being augmented by a rapidly expanding functional beverage category, including vitamin-infused water and electrolyte-infused water.

- This shift reflects a broader health and wellness trend, pushing producers to innovate with offerings like alkaline water with antioxidants. However, the most significant strategic imperative is sustainability. The industry is actively transitioning away from single-use plastics toward sustainable packaging solutions such as recycled PET (rPET), glass bottle packaging, and aluminum can packaging.

- Initiatives promoting a circular economy and the development of a biodegradable water bottle are gaining traction. Sourcing from a geologically protected underground source or a pristine artesian aquifer remains a key differentiator, but companies must also demonstrate robust water stewardship programs.

- Firms that proactively manage their water resources exhibit an operational risk profile that is up to 20% lower than competitors in water-stressed regions, highlighting the connection between environmental responsibility and long-term viability.

What are the Key Data Covered in this Packaged Natural Mineral Water Market Research and Growth Report?

-

What is the expected growth of the Packaged Natural Mineral Water Market between 2025 and 2029?

-

USD 55.20 billion, at a CAGR of 6.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Product (Packaged natural sparkling mineral water, and Packaged natural still mineral water), Type of Packaging (Plastic bottles, Glass bottles, and Cans) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Heightened health and wellness consciousness propelling market growth, Heightened environmental scrutiny and regulatory pressure on packaging

-

-

Who are the major players in the Packaged Natural Mineral Water Market?

-

Agthia Group PJSC, Beverly Hills Drink Co., Bisleri International Pvt. Ltd., China Resources Beverages Ltd., Danone S.A., Gerolsteiner Brunnen GmbH, Grupo Embotellador ATIC SA, Masafi Co. LLC, Mountain Valley Spring Co. LLC, Nestle SA, Parle Agro Pvt Ltd., PepsiCo Inc., Tata Consumer Products Ltd., The Coca Cola Co., The Wonderful Co. LLC, United Breweries Ltd. and VOSS Global Inc.

-

Market Research Insights

- The market is shaped by a significant consumer preference shift toward healthier hydration, driven by a pervasive health and wellness trend. This dynamic has led to a notable pivot away from sugar-sweetened beverages. In response, companies are innovating with value-added hydration products that offer enhanced wellness benefits.

- For instance, firms that pivot to sustainable packaging formats, such as recycled PET, report customer engagement rates up to 20% higher than competitors using virgin materials.

- Furthermore, the push for a reduced carbon footprint through the adoption of alternative packaging materials is accelerating, with new product launches in cans or cartons capturing market share twice as fast as traditional offerings in some segments, reflecting a strong eco-conscious consumer demand.

We can help! Our analysts can customize this packaged natural mineral water market research report to meet your requirements.

RIA -

RIA -