Pipelay Vessel Operator Market Size 2026-2030

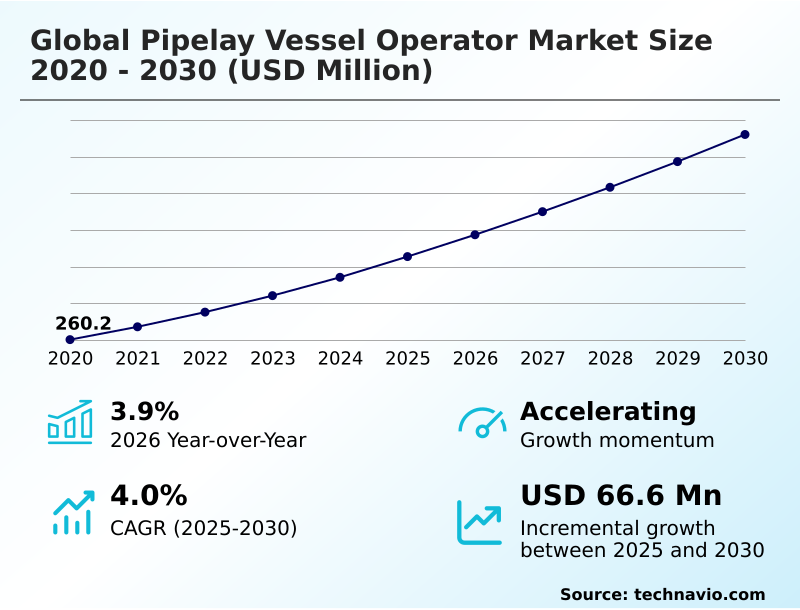

The pipelay vessel operator market size is valued to increase by USD 66.6 million, at a CAGR of 4% from 2025 to 2030. Rising demand for oil and gas globally will drive the pipelay vessel operator market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 52.6% growth during the forecast period.

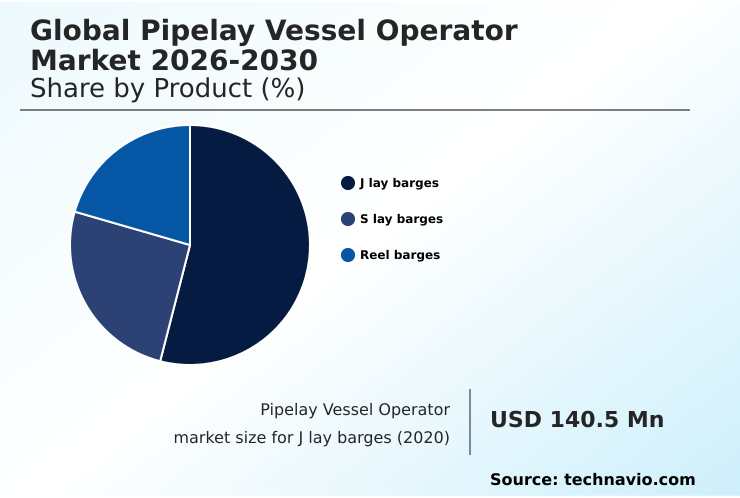

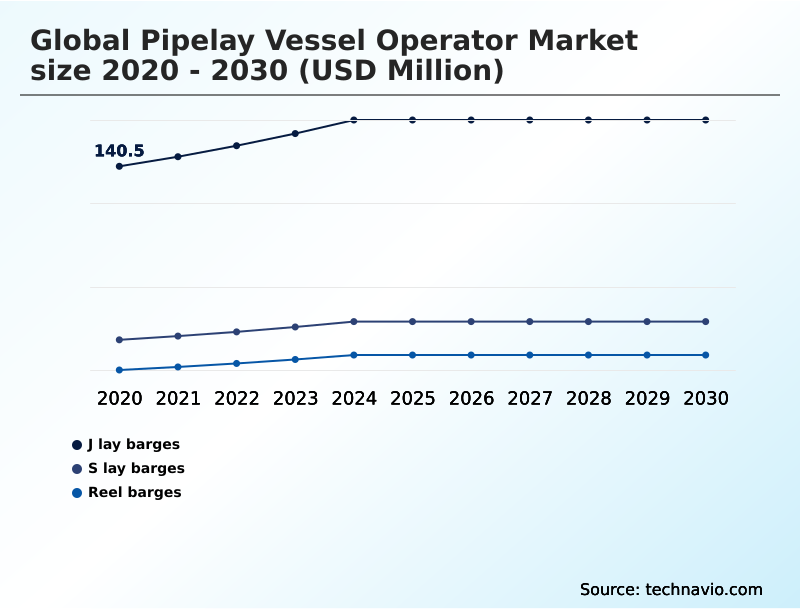

- By Product - J lay barges segment was valued at USD 160.3 million in 2024

- By Application - Oil and gas segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 111.9 million

- Market Future Opportunities: USD 66.6 million

- CAGR from 2025 to 2030 : 4%

Market Summary

- The pipelay vessel operator market is undergoing a significant transformation, driven by the dual demands of energy security and the global energy transition. Operators are moving beyond traditional shallow water operations to facilitate complex deepwater and ultra-deepwater projects, which are essential for accessing new hydrocarbon reserves.

- These specialized fleets, equipped with advanced technologies like J-lay barges and S-lay barges, are the linchpins of offshore infrastructure development. In a typical business scenario, an energy firm planning a new subsea field development must evaluate vessel capabilities for flexible pipe installation and rigid pipe installation to optimize capital expenditure and long-term operational costs.

- Success hinges on selecting operators whose assets align with the project's specific geological and environmental challenges. Furthermore, the market's scope is expanding to include services for the offshore wind and carbon capture sectors, requiring the installation of subsea power cables and CO2 transport pipelines, underscoring the versatile and critical role of pipelay vessels in the evolving energy landscape.

- This diversification is crucial as the industry navigates a complex future, balancing conventional energy needs with sustainable development goals.

What will be the Size of the Pipelay Vessel Operator Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Pipelay Vessel Operator Market Segmented?

The pipelay vessel operator industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- J lay barges

- S lay barges

- Reel barges

- Application

- Oil and gas

- Power

- Others

- Type

- Shallow water operations

- Deep water operations

- Geography

- APAC

- China

- Japan

- India

- Europe

- UK

- Germany

- France

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Product Insights

The j lay barges segment is estimated to witness significant growth during the forecast period.

J-lay barges represent a critical asset for deepwater drilling projects, designed for subsea pipeline repair techniques in hostile environments.

This method, involving a nearly vertical pipe ramp, is essential for ultra-deepwater drilling and subsea construction, minimizing bending stress and enhancing pipeline integrity management.

The technique reduces pipe fatigue during offshore pipeline installation by up to 25% compared to other methods.

As upstream oil and gas companies push into more challenging deepwater basin exploration, the demand for vessels capable of this precise, albeit slower, installation process grows.

This segment's evolution is driven by the need for reliable infrastructure to support both deepwater hydrocarbon developments and emerging offshore renewable energy projects, requiring robust solutions for subsea infrastructure development.

The J lay barges segment was valued at USD 160.3 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 52.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Pipelay Vessel Operator Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by deepwater activity in regions like South America and West Africa, which together account for over 52% of new large-scale project sanctions.

Concurrently, APAC is the fastest-growing region, driven by offshore block liberalization and new greenfield well exploration. The global energy transition is reshaping demand, with European offshore wind farm installation projects now comprising a significant market segment.

This shift requires operators to adapt fleets for subsea cable laying alongside traditional offshore platform installation. Subsea tie-back projects in mature basins like the North Sea and Gulf of Mexico provide consistent demand, focusing on maximizing existing offshore energy infrastructure.

Investment in carbon capture infrastructure is creating new opportunities, particularly in North America and Europe.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning in the global pipelay vessel operator market 2026-2030 requires a deep understanding of multiple operational variables. When evaluating deepwater pipeline installation methods, decision-makers must weigh s-lay versus j-lay efficiency for specific project depths and conditions.

- The overall cost of pipelay vessel operations is a critical factor, influenced heavily by the sophistication of the pipelay vessel dynamic positioning and onboard systems. As the industry evolves, the role of a pipelay vessel for renewable energy, particularly for cable laying, is becoming a significant revenue stream.

- Concurrently, developing robust subsea pipeline repair techniques and effective offshore pipeline corrosion protection strategies are essential for asset longevity. Projects incorporating flexible pipe installation in deepwater often achieve faster completion times than those using rigid pipes. Technological innovations in pipelay vessels, such as integrating automation in pipelay operations and advanced remote monitoring for pipelay vessels, are key differentiators.

- Proactive compliance in offshore pipeline projects and stringent safety protocols for pipelay operations are non-negotiable. Furthermore, a focus on reducing operational costs in pipelaying is paramount. As projects become more complex, the environmental impact of subsea pipelines is under greater scrutiny, influencing vessel selection.

- Finally, providing high-quality training for pipelay vessel crew ensures both safety and efficiency, as the reel-lay method for small pipelines and pipelay support vessel specifications become more specialized.

What are the key market drivers leading to the rise in the adoption of Pipelay Vessel Operator Industry?

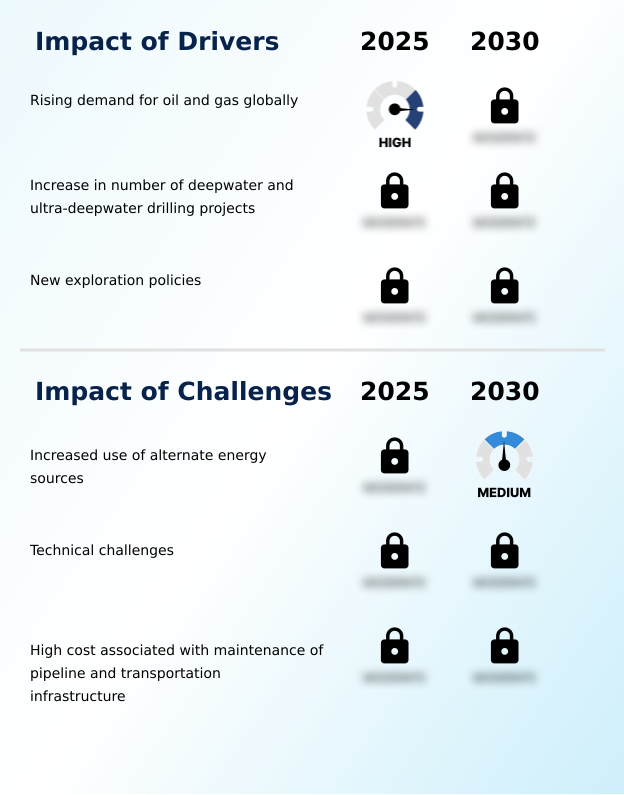

- The rising global demand for oil and gas serves as a key market driver, stimulating investment in exploration and production infrastructure.

- Rising global energy demand and a renewed focus on energy security initiatives are primary market drivers. The increase in deepwater and ultra-deepwater drilling projects, particularly in pre-salt field development zones, creates sustained demand for high-specification vessels.

- Favorable hydrocarbon exploration policies and the liberalization of offshore blocks have accelerated exploration timelines by over 15% in certain regions. This has led to a surge in greenfield well exploration and subsea tie-back projects, requiring extensive offshore pipeline installation.

- The strategic importance of liquefied natural gas (LNG) transport is also fueling investments in related subsea infrastructure.

- These factors collectively propel the need for advanced pipelay fleets capable of supporting large-scale offshore construction campaigns and ensuring the integrity of new and mature oilfield life extension projects.

What are the market trends shaping the Pipelay Vessel Operator Industry?

- The increasing integration of automation within the oil and gas industry is a notable upcoming market trend, enhancing operational efficiency and safety.

- The market is witnessing a significant trend towards automation and digitalization to enhance project execution. The adoption of the Internet of Things (IoT) in midstream oil and gas operations allows for real-time monitoring of pipelaying activities, with some operators reporting a 20% reduction in equipment downtime through predictive maintenance.

- This integration of technology facilitates more efficient decommissioning operations and pipeline replacement programs. Technological innovations boosting productivity are evident in new vessel designs that combine J-lay and reel-lay capabilities, improving operational flexibility. Furthermore, the use of advanced analytics in subsea project management optimizes vessel deployment and logistics, leading to project cost savings of up to 12%.

- These advancements are critical as operators expand into floating offshore wind technology and more complex subsea electrical interconnectors.

What challenges does the Pipelay Vessel Operator Industry face during its growth?

- The growing adoption of alternative energy sources presents a significant challenge to the industry's growth trajectory.

- Operators face significant challenges from the increasing use of alternative energy sources, which diverts investment from traditional hydrocarbon projects. Technical challenges associated with harsh environment operations and deepwater pipeline installation methods persist, with unexpected geological conditions contributing to project cost overruns in 1 out of every 5 deepwater projects.

- The high cost of pipeline maintenance and infrastructure, coupled with stringent environmental regulations, puts pressure on margins. Moreover, the industry grapples with a shortage of skilled labor proficient in managing new technologies, which can impede the adoption of efficiency-gaining systems.

- Navigating complex local content requirements and geopolitical risks in key operational regions further complicates offshore supply chain logistics and project financing, making risk management a critical competency.

Exclusive Technavio Analysis on Customer Landscape

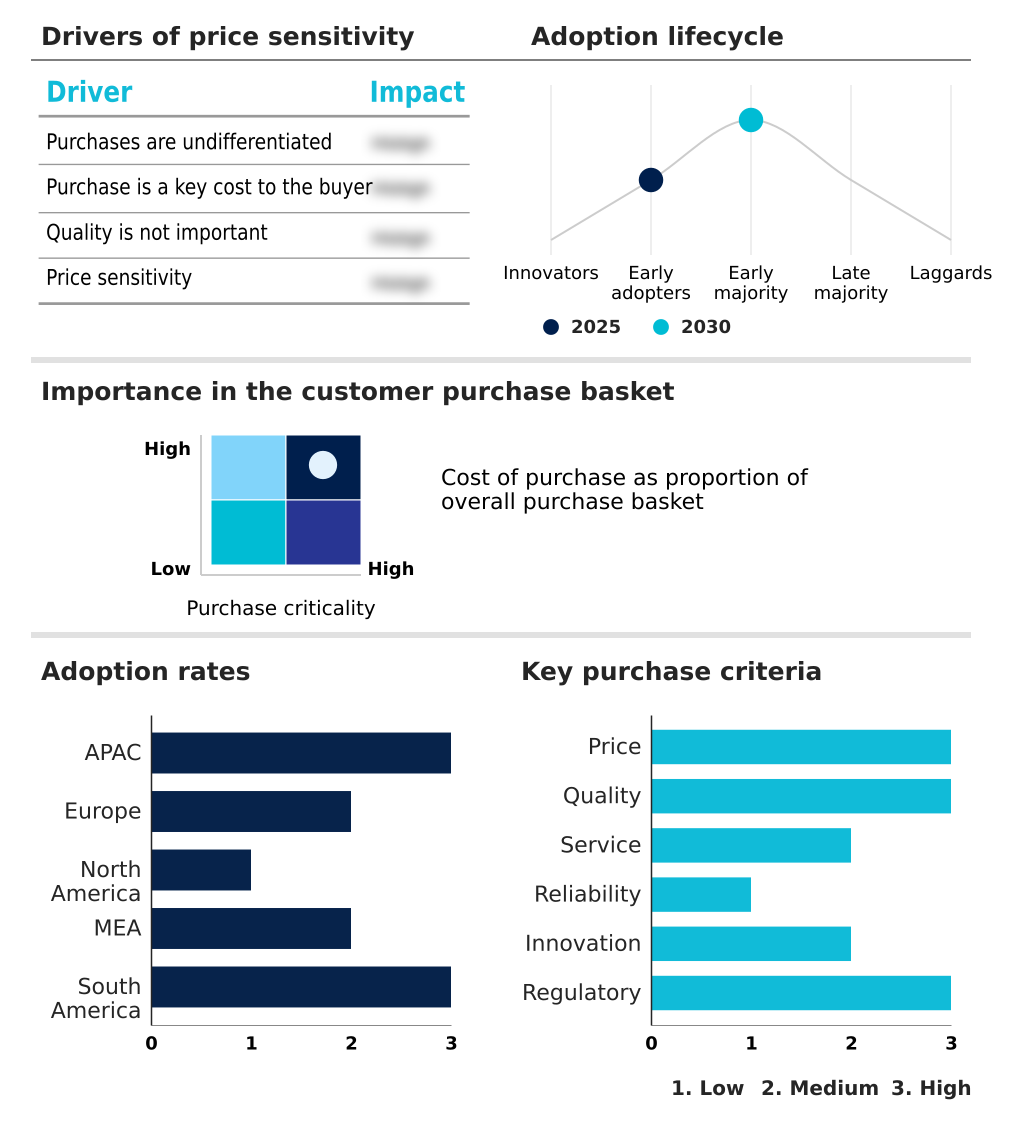

The pipelay vessel operator market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pipelay vessel operator market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Pipelay Vessel Operator Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, pipelay vessel operator market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Allseas Group SA - Delivers engineering-led offshore construction solutions, integrating automation and IoT technologies to optimize pipeline installation efficiency and project safety.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Allseas Group SA

- Boskalis

- BOURBON Maritime

- CIMIC Group

- Hanwha Group

- Havila Shipping ASA

- Hyundai Heavy Industries Group

- John Swire and Sons Ltd.

- McDermott International Ltd.

- New DOF ASA

- Royal IHC

- Saipem S.p.A.

- Siem Offshore Inc.

- Subsea 7 SA

- TechnipFMC plc

- Tidewater Inc.

- Van Oord nv

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pipelay vessel operator market

- In September, 2024, Allseas Group SA announced the commissioning of a new vessel featuring advanced automated welding systems and enhanced dynamic positioning, designed to reduce installation times for deepwater projects.

- In November, 2024, Subsea 7 SA secured a major SURF contract from Petrobras for the development of a pre-salt field offshore Brazil, valued at approximately $900 million.

- In February, 2025, TechnipFMC plc and Saipem S.p.A. formed a strategic joint venture to deliver integrated engineering, procurement, construction, and installation services for offshore carbon capture and storage (CCS) pipeline projects globally.

- In April, 2025, McDermott International Ltd. announced the successful completion of a complex pipeline installation project in the US Gulf of Mexico, utilizing innovative remote monitoring technologies that improved project efficiency by 15%.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Pipelay Vessel Operator Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4% |

| Market growth 2026-2030 | USD 66.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.9% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, UK, Germany, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Saudi Arabia, South Africa, UAE, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The pipelay vessel operator market is defined by high-capital assets and specialized technical expertise. Fleets are differentiated by their core systems, including J-lay barges, S-lay barges, and reel barges, which are deployed for shallow water operations or deep water operations based on project requirements.

- The effectiveness of these assets hinges on components like pipe tensioning systems, automated welding systems, and stinger fabrication. For boardroom decisions, the choice between mobilizing pipelay support vessels (PLSVs) for complex deepwater drilling projects versus utilizing derrick lay barges for more conventional offshore platform installation represents a significant capital allocation choice.

- Advanced operators are integrating remotely operated vehicles (ROVs) and wellhead protection systems to mitigate risk in ultra-deepwater drilling. Fleets with advanced dive support vessels capable of executing complex subsea production systems and mooring systems installations achieve a capital efficiency improvement of up to 10% on large-scale projects.

- The market's trajectory is increasingly influenced by subsea infrastructure development for both hydrocarbon and renewable energy, demanding proficiency in subsea umbilicals risers and flowlines (SURF), flexible pipe installation, and rigid pipe installation.

What are the Key Data Covered in this Pipelay Vessel Operator Market Research and Growth Report?

-

What is the expected growth of the Pipelay Vessel Operator Market between 2026 and 2030?

-

USD 66.6 million, at a CAGR of 4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (J lay barges, S lay barges, and Reel barges), Application (Oil and gas, Power, and Others), Type (Shallow water operations, and Deep water operations) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising demand for oil and gas globally, Increased use of alternate energy sources

-

-

Who are the major players in the Pipelay Vessel Operator Market?

-

Allseas Group SA, Boskalis, BOURBON Maritime, CIMIC Group, Hanwha Group, Havila Shipping ASA, Hyundai Heavy Industries Group, John Swire and Sons Ltd., McDermott International Ltd., New DOF ASA, Royal IHC, Saipem S.p.A., Siem Offshore Inc., Subsea 7 SA, TechnipFMC plc, Tidewater Inc. and Van Oord nv

-

Market Research Insights

- The market is shaped by a dynamic interplay between deepwater E&P investment and the expanding needs of the energy transition. The execution of brownfield project execution and subsea infrastructure inspection, repair, and maintenance (IRM) provides a stable demand floor. Operators employing advanced subsea project management methodologies see up to a 15% reduction in project schedule overruns compared to traditional approaches.

- As national oil companies (NOCs) and international oil companies (IOCs) pursue harsh environment operations, vessels with superior dynamic positioning systems command premium charter rates, reflecting a market where technological capability directly translates to commercial advantage.

- Moreover, adherence to stringent local content requirements can improve contract win rates by over 20% in key developing markets, highlighting the importance of strategic regional partnerships in the offshore supply chain logistics.

We can help! Our analysts can customize this pipelay vessel operator market research report to meet your requirements.

RIA -

RIA -